OPEC Annual Statistical Bulletin 2019 1 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Coal and Oil: the Dark Monarchs of Global Energy – Understanding Supply and Extraction Patterns and Their Importance for Futur

nam et ipsa scientia potestas est List of Papers This thesis is based on the following papers, which are referred to in the text by their Roman numerals. I Höök, M., Aleklett, K. (2008) A decline rate study of Norwe- gian oil production. Energy Policy, 36(11):4262–4271 II Höök, M., Söderbergh, B., Jakobsson, K., Aleklett, K. (2009) The evolution of giant oil field production behaviour. Natural Resources Research, 18(1):39–56 III Höök, M., Hirsch, R., Aleklett, K. (2009) Giant oil field decline rates and their influence on world oil production. Energy Pol- icy, 37(6):2262–2272 IV Jakobsson, K., Söderbergh, B., Höök, M., Aleklett, K. (2009) How reasonable are oil production scenarios from public agen- cies? Energy Policy, 37(11):4809–4818 V Höök M, Söderbergh, B., Aleklett, K. (2009) Future Danish oil and gas export. Energy, 34(11):1826–1834 VI Aleklett K., Höök, M., Jakobsson, K., Lardelli, M., Snowden, S., Söderbergh, B. (2010) The Peak of the Oil Age - analyzing the world oil production Reference Scenario in World Energy Outlook 2008. Energy Policy, 38(3):1398–1414 VII Höök M, Tang, X., Pang, X., Aleklett K. (2010) Development journey and outlook for the Chinese giant oilfields. Petroleum Development and Exploration, 37(2):237–249 VIII Höök, M., Aleklett, K. (2009) Historical trends in American coal production and a possible future outlook. International Journal of Coal Geology, 78(3):201–216 IX Höök, M., Aleklett, K. (2010) Trends in U.S. recoverable coal supply estimates and future production outlooks. Natural Re- sources Research, 19(3):189–208 X Höök, M., Zittel, W., Schindler, J., Aleklett, K. -

Oil Shale and Tar Sands

Fundamentals of Materials for Energy and Environmental Sustainability Editors David S. Ginley and David Cahen Oil shale and tar sands James W. Bunger 11 JWBA, Inc., Energy Technology and Engineering, Salt Lake City, UT, USA 11.1 Focus 11.2 Synopsis Tar sands and oil shale are “uncon- Oil shale and tar sands occur in dozens of countries around the world. With in-place ventional” oil resources. Unconven- resources totaling at least 4 trillion barrels (bbl), they exceed the world's remaining tional oil resources are characterized petroleum reserves, which are probably less than 2 trillion bbl. As petroleum becomes by their solid, or near-solid, state harder to produce, oil shale and tar sands are finding economic and thermodynamic under reservoir conditions, which parity with petroleum. Thermodynamic parity, e.g., similarity in the energy cost requires new, and sometimes of producing energy, is a key indicator of economic competitiveness. unproven, technology for their Oil is being produced on a large commercial scale by Canada from tar sands, recovery. For tar sands the hydrocar- and to a lesser extent by Venezuela. The USA now imports well over 2 million barrels bon is a highly viscous bitumen; for of oil per day from Canada, the majority of which is produced from tar sands. oil shale, it is a solid hydrocarbon Production of oil from oil shale is occurring in Estonia, China, and Brazil albeit on called “kerogen.” Unconventional smaller scales. Importantly, the USA is the largest holder of oil-shale resources. oil resources are found in greater For that reason alone, and because of the growing need for imports in the USA, quantities than conventional petrol- oil shale will receive greater development attention as petroleum supplies dwindle. -

Peak Oil, Peak Energy Mother Nature Bats Last

Peak Oil, Peak Energy Mother Nature Bats Last Martin Sereno 1 Feb 2011 (orig. talk: Nov 2004) Oil is the Lifeblood of Industrial Civilization • 80 million barrels/day, 1000 barrels/sec, 1 cubic mile/year • highly energy-dense • easy to transport, store • moves goods and people • allows us to fly (there will never be a battery-operated jet plane) • digs huge holes and puts up huge buildings • ballooned our food supply (fertilize, cultivate, irrigate, transport) • our 'stuff' is made from it (iPods to the roads themselves) • we're not "addicted to oil" -- that's like saying a person has an "addiction to blood" Where Oil Comes From • raw organic material for oil (e.g., from plankton) is present in low concentrations in ‘all’ sedimentary rocks, but esp. from two warm periods 90 million and 140 million years ago • temperature rises with depth (radioactivity, Kelvin’s mistake) • oil is generated in rocks heated to 60-120 deg Celsius • rocks at this temp. occur at different depths in different places (N.B.: water depth doesn't count) • oil is ‘cracked’ to natural gas at higher temps (deeper) • abiotic oil from “crystalline basement” is negligible, if it exists • exhausted oil fields do not refill Recoverable Oil • oil must collect in a “trap” to be practically recoverable • a trap is a permeable layer capped by an impermeable one • obvious traps: anticlines, domes (“oil in those hills”) • less obvious traps found by seismic imaging: turned up edges of salt domes, near buried meteorite crater (Mexico) • harder-to-get-at traps: shallow continental shelf (GOM) • even-harder-to-get-at traps: edge continental slope (Macondo, resevoir pressure: 12,000 pounds [6 tons] per sq inch) • essentially no oil in basaltic ocean floor or granitic basement (Used to be!) Second Largest Oilfield Cantarell used to supply 2% of world oil (water) Guzman, A.E. -

Climate and Energy Benchmark in Oil and Gas Insights Report

Climate and Energy Benchmark in Oil and Gas Insights Report Partners XxxxContents Introduction 3 Five key findings 5 Key finding 1: Staying within 1.5°C means companies must 6 keep oil and gas in the ground Key finding 2: Smoke and mirrors: companies are deflecting 8 attention from their inaction and ineffective climate strategies Key finding 3: Greatest contributors to climate change show 11 limited recognition of emissions responsibility through targets and planning Key finding 4: Empty promises: companies’ capital 12 expenditure in low-carbon technologies not nearly enough Key finding 5:National oil companies: big emissions, 16 little transparency, virtually no accountability Ranking 19 Module Summaries 25 Module 1: Targets 25 Module 2: Material Investment 28 Module 3: Intangible Investment 31 Module 4: Sold Products 32 Module 5: Management 34 Module 6: Supplier Engagement 37 Module 7: Client Engagement 39 Module 8: Policy Engagement 41 Module 9: Business Model 43 CLIMATE AND ENERGY BENCHMARK IN OIL AND GAS - INSIGHTS REPORT 2 Introduction Our world needs a major decarbonisation and energy transformation to WBA’s Climate and Energy Benchmark measures and ranks the world’s prevent the climate crisis we’re facing and meet the Paris Agreement goal 100 most influential oil and gas companies on their low-carbon transition. of limiting global warming to 1.5°C. Without urgent climate action, we will The Oil and Gas Benchmark is the first comprehensive assessment experience more extreme weather events, rising sea levels and immense of companies in the oil and gas sector using the International Energy negative impacts on ecosystems. -

Statoil ASA Statoil Petroleum AS

Offering Circular A9.4.1.1 Statoil ASA (incorporated with limited liability in the Kingdom of Norway) Notes issued under the programme may be unconditionally and irrevocably guaranteed by Statoil Petroleum AS (incorporated with limited liability in the Kingdom of Norway) €20,000,000,000 Euro Medium Term Note Programme On 21 March 1997, Statoil ASA (the Issuer) entered into a Euro Medium Term Note Programme (the Programme) and issued an Offering Circular on that date describing the Programme. The Programme has been subsequently amended and updated. This Offering Circular supersedes any previous dated offering circulars. Any Notes (as defined below) issued under the Programme on or after the date of this Offering Circular are issued subject to the provisions described herein. This does not affect any Notes issued prior to the date hereof. Under this Programme, Statoil ASA may from time to time issue notes (the Notes) denominated in any currency agreed between the Issuer and the relevant Dealer (as defined below). The Notes may be issued in bearer form or in uncertificated book entry form (VPS Notes) settled through the Norwegian Central Securities Depositary, Verdipapirsentralen ASA (the VPS). The maximum aggregate nominal amount of all Notes from time to time outstanding will not exceed €20,000,000,000 (or its equivalent in other currencies calculated as described herein). The payments of all amounts due in respect of the Notes issued by the Issuer may be unconditionally and irrevocably guaranteed by Statoil A6.1 Petroleum AS (the Guarantor). The Notes may be issued on a continuing basis to one or more of the Dealers specified on page 6 and any additional Dealer appointed under the Programme from time to time, which appointment may be for a specific issue or on an ongoing basis (each a Dealer and together the Dealers). -

Monthly Report on Petroleum Developments in the World Markets February 2020

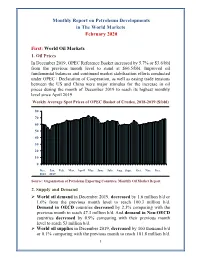

Monthly Report on Petroleum Developments in The World Markets February 2020 First: World Oil Markets 1. Oil Prices In December 2019, OPEC Reference Basket increased by 5.7% or $3.6/bbl from the previous month level to stand at $66.5/bbl. Improved oil fundamental balances and continued market stabilization efforts conducted under OPEC+ Declaration of Cooperation, as well as easing trade tensions between the US and China were major stimulus for the increase in oil prices during the month of December 2019 to reach its highest monthly level since April 2019. Weekly Average Spot Prices of OPEC Basket of Crudes, 2018-2019 ($/bbl) 80 70 60 50 40 30 20 10 0 Dec. Jan. Feb. Mar. April May June July Aug. Sept. Oct. Nov. Dec. 2018 2019 Source: Organization of Petroleum Exporting Countries, Monthly Oil Market Report. 2. Supply and Demand World oil demand in December 2019, decreased by 1.6 million b/d or 1.6% from the previous month level to reach 100.3 million b/d. Demand in OECD countries decreased by 2.3% comparing with the previous month to reach 47.3 million b/d. And demand in Non-OECD countries decreased by 0.9% comparing with their previous month level to reach 53 million b/d. World oil supplies in December 2019, decreased by 100 thousand b/d or 0.1% comparing with the previous month to reach 101.8 million b/d. 1 Non-OPEC supplies remained stable at the same previous month level of 67.2 million b/d. Whereas preliminary estimates show that OPEC crude oil and NGLs/condensates total supplies decreased by 0.6% comparing with the previous month to reach 34.5 million b/d. -

Press Release

Press Release First quarter 2021 results With results of more than $3 billion, Total fully benefits from rebound in hydrocarbon prices LNG and renewables represent one-third of results Change Change 1Q21 1Q20 1Q19 vs 1Q20 vs 1Q19 Oil price - Brent ($/b) 61.1 50.1 +22% 63.1 -3% Average price of LNG ($/Mbtu) 6.1 6.3 -4% 7.2 -16% Variable cost margin - Refining Europe, VCM ($/t) 5.3 26.3 -80% 33.0 -84% Adjusted net income (Group share)1 - in billions of dollars (B$) 3.0 1.8 69% 2.8 +9% - in dollars per share 1.10 0.66 +68% 1.02 +8% DACF1 (B$) 5.8 4.3 +34% 6.3 -8% Cash Flow from operations (B$) 5.6 1.3 x4.3 3.6 +54% Net income (Group share) of 3.3 B$ in 1Q21 Net-debt-to-capital ratio of 19.5% at March 31, 2021 vs. 21.7% at December 31, 20202 Hydrocarbon production of 2,863 kboe/d in 1Q21, a decrease of 7% compared to 1Q20 First 2021 interim dividend set at 0.66 €/share 2 Paris, April 29, 2021 - The Board of Directors of Total SE, meeting on April 28, 2021, under the chairmanship of Chairman and Chief Executive Officer Patrick Pouyanné, approved the Group's first quarter 2021 accounts. On this occasion, Patrick Pouyanné said: « In the first quarter, the Group fully benefited from rising oil and gas prices, up 38% and 24%, respectively quarter-to- quarter, and its strategy to grow LNG and Renewables and Electricity. -

The West African Oil & Gas Market 2013-2023

The West African Oil & Gas Market 2013-2023 Table 4.28 Exploration Fields that Gabon Oil Company is Involved in Fields Operator MAGHENA Addax AGALI Anadarko NKANI Atas E2 Eni D3 Eni D4 Eni F2 Eni F3 Eni F7 Eni EPAEMENO GGPC EOV GGPC DUSSAFU Harvest ETEKAMBA Maurel & Prom OMOUEYI Maurel & Prom NYANGA MAYOMBE Maurel & Prom KARI Maurel & Prom MOABI MPDC NGUMA MPDC SHAKTHI Oil India MBELI Ophir Gabon NTSINA Ophir Gabon MANGA Ophir Gabon GNONDO Ophir Gabon NZIEMBOU Perenco OGUEYI Perenco DE 7 Perenco AROUWE Perenco DUSSAFU Sasol IGOUMOU MARIN Shell Gabon BC9 Shell Gabon BCD10 Shell Gabon SALSICH Sino Gabon LOTUS Sinopec MBINDA Total Gabon ALOUMBE Total Gabon DIABA Total Gabon AZOBE Tullow Oil AKOUM Tullow Oil KIARSSENY Tullow Oil Source: Gabon Oil Company 4.7.5.3 Prospects for Pre-Salt Development As with Angola and several other West African countries, the rapid development of Brazil’s pre-salt formations has sparked considerable interest in the prospects for Gabon’s pre-salt regions, which were part of the same prehistoric supercontinent, Pangea. Gabon’s pre-salt regions had been www.visiongain.com Page 99 The West African Oil & Gas Market 2013-2023 4.8 Republic of the Congo Oil & Gas Market Forecast 2013-2023 Table 4.31, Figure 4.32 and Figure 4.33 show visiongain’s forecast for Republic of Congo’s oil & gas market over the next ten years. Table 4.31 Republic of the Congo Oil & Gas Market Forecast 2013-2023 ($bn, AGR %, CAGR%, Cumulative) 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2013-23 Capex $bn 1.55 1.70 2.57 4.15 4.55 2.70 2.50 1.80 1.87 2.10 2.40 2.80 29.14 AGR (%) 9.8 50.9 61.6 9.6 -40.7 -7.4 -28.0 3.9 12.3 14.3 16.7 CAGR (%) 2013-18 8.0 2018-23 2.3 CAGR (%) 2013-23 5.1 Source: Visiongain 2013 Figure 4.32 Republic of the Congo Oil & Gas Market Forecast 2013-2023 ($bn, AGR%) 5.0 80% 4.5 60% 4.0 3.5 40% 3.0 20% 2.5 $Bn AGR 0% 2.0 1.5 -20% 1.0 -40% 0.5 0.0 -60% 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 Year Source: Visiongain 2013 www.visiongain.com Page 103 The West African Oil & Gas Market 2013-2023 6. -

Crude Oil Reserves 1986

o un E I Introduction FACTS AND FIGURES is produced annually at the OPEC Secretariat in Vienna, to assist people requiring a means of rapidly assimilating important facts about the energy industry, without themselves having to delve into time- consuming research from an array of sources. Since it is the belief of OPEC Member Countries that energy cannot be viewed in isolation from other global economic considerations, parts of this booklet broach such related issues as comparisons between the economic fortunes of industrialized and developing nations. A wide range of authoritative sources have been con- sulted in producing this booklet. Where disparities have occurred among sources, great pains have been taken at the Secretariat to distill those figures which most faithfully reflect observed market trends. The graphs are presented in six sections. The first three examine energy issues on a global scale, the next two con- centrate on OPEC, while the final one makes broad econ- omic comparisons between different world groupings. It is hoped that this latest issue of FACTS AND FIGURES, which covers the period up to the end of 1986, will prove of interest and value to its readers. November 1987 Published by: The Secretariat, Organization of the Petroleum Exporting Countries, Obere Donaustrasse 93, A-1020 Vienna, Austria 1987 Printed in Austria by H Carl UeberreuterGes. m. b. H-, Vienna OPEC flows of crude and refined oil — 1986 I I OPEC Far East 4 Indonesia ^| OPEC Latin America - 2 Ecuador; 13 Venezuela • OPEC Africa 1 Algeria; 3 Gabon; 9 -

Peak Oil Demand and Long-Run Oil Prices

January 2018 Peak Oil Demand and Long-Run Oil Prices Abstract The prospect that global oil demand will gradually slow and eventually peak has created a cottage industry of executives and commentators trying to predict the point at which demand will peak. In this Energy Insight, we argue that this focus seems misplaced. The date at which oil demand will stop growing is highly uncertain and small changes in assumptions can lead to vastly different estimates. More importantly, there is little reason to believe that once it does peak, that oil demand will fall sharply. The world is likely to demand large quantities of oil for many decades to come. Rather, the significance of peak oil is that it signals a shift in paradigm – from an age of (perceived) scarcity to an age of abundance – and with it is likely to herald a shift to a more competitive market environment. This change in paradigm is also likely to pose material challenges for oil producing economies as they try both to ensure that their oil is produced and consumed, and at the same time diversify their economies fit for a world in which they can no longer rely on oil revenues to provide their main source of revenue for the indefinite future. We argue that the extent and pace of this diversification is likely to have an important bearing on oil prices over the next 20 or 30 years. It seems likely that many low-cost producers will delay the pace at which they adopt a more competitive “higher volume, lower price” strategy until they have made material progress in reforming their economies. -

Welcome to the 11Th Edition of Energy Perspectives! This Is An

Welcome to the 11th edition of Energy Perspectives! This is an independent report that informs Equinor’s strategy and offers a fact-based contribution to the energy transition debate. This year’s edition is an update of the edition from November last year, and with a lot happening on the global arena the last 6 months, there is a lot to consider when looking 30 years ahead. As always, this report and its data and conclusions would be impossible without the excellent work of many of my colleagues, to whom I extend my appreciation and gratitude. You are the best! 1 Covid19 is not over. In a global perspective, we are still dealing with its impact and the enormous effects it has on people, societies, economies, and markets. We are not through it yet. And we might have to live with recurring infection spikes, especially in parts of the world that do not get sufficient access to vaccines. Recurring lockdowns entailed that energy demand, and in particular oil demand due to its use as a transport fuel, was hit hard. Recovery is in the making, and faster than many feared, but oil demand, as an example, is still not back to pre-Covid19-levels. The map shows how the pandemic has affected economies across the globe, with almost all countries pink or red, that is, with negative economic development. Industrialised countries are on their way out of recession while disabling the virus, but the uncertainty is still high in many emerging economies. 2 We are seeing signs of recovery. Thanks to the development and rollout of vaccines and massive public spending to stimulate demand, there are signs that the situation is being brought under control so that we can live with the virus more like we do with normal flus. -

UK/Netherlands SNS Hackathon Output Report

UK/Netherlands SNS Hackathon Output Report April 2019 Contents Foreword ............................................................................................................................................................. 3 Executive Summary ............................................................................................................................................. 4 Introduction ......................................................................................................................................................... 4 How Does a Hackathon Event Work? ................................................................................................................... 5 Findings ............................................................................................................................................................... 6 Operator Challenges ............................................................................................................................................ 7 Operator 1: Shell .......................................................................................................................................... 7 Operator2: Oranje Nassau Energie B.V. ........................................................................................................ 8 Operator 3: Spirit Energy .............................................................................................................................. 9 Operator 4: Neptune Energy ......................................................................................................................