World Oil Outlook 2040

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Petroleum Extension-The University of Texas at Austin ROTARY DRILLING SERIES

Petroleum Extension-The University of Texas at Austin ROTARY DRILLING SERIES Unit I: The Rig and Its Maintenance Lesson 1: The Rotary Rig and Its Components Lesson 2: The Bit Lesson 3: Drill String and Drill Collars Lesson 4: Rotary, Kelly, Swivel, Tongs, and Top Drive Lesson 5: The Blocks and Drilling Line Lesson 6: The Drawworks and the Compound Lesson 7: Drilling Fluids, Mud Pumps, and Conditioning Equipment Lesson 8: Diesel Engines and Electric Power Lesson 9: The Auxiliaries Lesson 10: Safety on the Rig Unit II: Normal Drilling Operations Lesson 1: Making Hole Lesson 2: Drilling Fluids Lesson 3: Drilling a Straight Hole Lesson 4: Casing and Cementing Lesson 5: Testing and Completing Unit III: Nonroutine Operations Lesson 1: Controlled Directional Drilling Lesson 2: Open-Hole Fishing Lesson 3: Blowout Prevention Unit IV: Man Management and Rig Management Unit V: Offshore Technology Lesson 1: Wind, Waves, and Weather Lesson 2: Spread Mooring Systems Lesson 3: Buoyancy, Stability, and Trim Lesson 4: Jacking Systems and Rig Moving Procedures Lesson 5: Diving and Equipment Lesson 6: Vessel Inspection and Maintenance Lesson 7: Helicopter Safety Lesson 8: Orientation for Offshore Crane Operations Lesson 9: Life Offshore Lesson 10: Marine Riser Systems and Subsea Blowout Preventers Petroleum Extension-The University of Texas at Austin Library of Congress Cataloging-in-Publication Data Vieira, João Luiz, 1958– Controlled directional drilling / by João Luiz Vieira. — 4th ed. p. cm. — (Rotary drilling series ; unit 3, lesson 1) Rev. ed. of: Controlled directional drilling. 1984 Includes index. ISBN-10 0-88698-254-5 (alk. paper) ISBN-13 978-0-88698-254-6 (alk. -

Shell Midstream Partners / Crestwood Permian Basin Holdings / Crestwood Permian Basin

Disclaimer : The Competition DG makes the information provided by the notifying parties in section 1.2 of Form CO available to the public in order to increase transparency. This information has been prepared by the notifying parties under their sole responsibility, and its content in no way prejudges the view the Commission may take of the planned operation. Nor can the Commission be held responsible for any incorrect or misleading information contained therein. M.8638 - SHELL MIDSTREAM PARTNERS / CRESTWOOD PERMIAN BASIN HOLDINGS / CRESTWOOD PERMIAN BASIN SECTION 1.2 Description of the concentration The Commission has received notification of a proposed concentration pursuant to article 4 of Council Regulation (EC) No 139/2004 (the “EUMR”). On 8 September 2017, Shell Midstream Partners, L.P. (a solely-controlled subsidiary of Royal Dutch Shell plc (“Shell”)) notified its intention to acquire indirect joint control of Crestwood Permian Basin LLC along with current owner Crestwood Permian Basin Holdings LLC (itself a joint venture between First Reserve Management L.P. and Crestwood Equity Partners LP.) within the meaning of Article 3(1)(b) of the EUMR. The areas of activities of the undertakings concerned by the notified concentration are as follows: − Shell – a global group of energy and petrochemical companies; − Crestwood Permian Basin Holdings – a joint venture between First Reserve and Crestwood, and currently the sole owner of Crestwood Permian Basin; − Crestwood Permian Basin – owns and operates a natural gas gathering system in the Permian Basin, the largest petroleum-producing basin in the United States. Commission européenne, DG COMP MERGER REGISTRY, 1049 Bruxelles, BELGIQUE Europese Commissie, DG COMP MERGER REGISTRY, 1049 Brussel, BELGIË Tel: +32 229-91111. -

WTI Crude Oil West Texas Intermediate

WTI Crude Oil West Texas Intermediate Alexander Filitz Minh Khoa Nguyen Outline • Crude Oil • Value Chain • Politics • Market • Demand • Facts & Figures • Discussion Crude Oil • Flammable liquid consisting of a complex mixture of hydrocarbons of various molecular weights and other liquid organic compounds • Is recovered mostly through oil drilling • In its strictest sense, petroleum includes only crude oil, but in common usage it includes all liquid, gaseous, and solid hydrocarbons. • An oil well produces predominantly crude oil, with some natural gas dissolved in it Classification • By the geographic location it is produced in • Its API gravity (an oil industry measure of density) • Its sulfur content • Some of the common reference crudes are: • West Texas Intermediate (WTI), a very high-quality, sweet, light oil delivered at Cushing, Oklahoma for North American oil. • Brent Blend, comprising 15 oils from fields in the North Sea. • Dubai-Oman, used as benchmark for Middle East sour crude oil flowing to the Asia-Pacific region • The OPEC Reference Basket, a weighted average of oil blends from various OPEC (The Organization of the Petroleum Exporting Countries) countries West Texas Intermediate • Also known as Texas light sweet, used as a benchmark in oil pricing • API gravity of around 39.6 and specific gravity of 0.827 and 0.24% sulfur • WTI is refined mostly in the Midwest and Gulf Coast regions in the U.S • It is the underlying commodity of New York Mercantile Exchange's (NYMEX) oil futures contracts • Often referenced in news reports -

Climate and Energy Benchmark in Oil and Gas Insights Report

Climate and Energy Benchmark in Oil and Gas Insights Report Partners XxxxContents Introduction 3 Five key findings 5 Key finding 1: Staying within 1.5°C means companies must 6 keep oil and gas in the ground Key finding 2: Smoke and mirrors: companies are deflecting 8 attention from their inaction and ineffective climate strategies Key finding 3: Greatest contributors to climate change show 11 limited recognition of emissions responsibility through targets and planning Key finding 4: Empty promises: companies’ capital 12 expenditure in low-carbon technologies not nearly enough Key finding 5:National oil companies: big emissions, 16 little transparency, virtually no accountability Ranking 19 Module Summaries 25 Module 1: Targets 25 Module 2: Material Investment 28 Module 3: Intangible Investment 31 Module 4: Sold Products 32 Module 5: Management 34 Module 6: Supplier Engagement 37 Module 7: Client Engagement 39 Module 8: Policy Engagement 41 Module 9: Business Model 43 CLIMATE AND ENERGY BENCHMARK IN OIL AND GAS - INSIGHTS REPORT 2 Introduction Our world needs a major decarbonisation and energy transformation to WBA’s Climate and Energy Benchmark measures and ranks the world’s prevent the climate crisis we’re facing and meet the Paris Agreement goal 100 most influential oil and gas companies on their low-carbon transition. of limiting global warming to 1.5°C. Without urgent climate action, we will The Oil and Gas Benchmark is the first comprehensive assessment experience more extreme weather events, rising sea levels and immense of companies in the oil and gas sector using the International Energy negative impacts on ecosystems. -

Monthly Report on Petroleum Developments in the World Markets February 2020

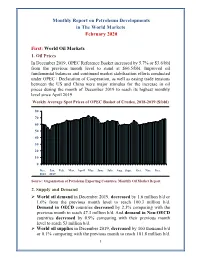

Monthly Report on Petroleum Developments in The World Markets February 2020 First: World Oil Markets 1. Oil Prices In December 2019, OPEC Reference Basket increased by 5.7% or $3.6/bbl from the previous month level to stand at $66.5/bbl. Improved oil fundamental balances and continued market stabilization efforts conducted under OPEC+ Declaration of Cooperation, as well as easing trade tensions between the US and China were major stimulus for the increase in oil prices during the month of December 2019 to reach its highest monthly level since April 2019. Weekly Average Spot Prices of OPEC Basket of Crudes, 2018-2019 ($/bbl) 80 70 60 50 40 30 20 10 0 Dec. Jan. Feb. Mar. April May June July Aug. Sept. Oct. Nov. Dec. 2018 2019 Source: Organization of Petroleum Exporting Countries, Monthly Oil Market Report. 2. Supply and Demand World oil demand in December 2019, decreased by 1.6 million b/d or 1.6% from the previous month level to reach 100.3 million b/d. Demand in OECD countries decreased by 2.3% comparing with the previous month to reach 47.3 million b/d. And demand in Non-OECD countries decreased by 0.9% comparing with their previous month level to reach 53 million b/d. World oil supplies in December 2019, decreased by 100 thousand b/d or 0.1% comparing with the previous month to reach 101.8 million b/d. 1 Non-OPEC supplies remained stable at the same previous month level of 67.2 million b/d. Whereas preliminary estimates show that OPEC crude oil and NGLs/condensates total supplies decreased by 0.6% comparing with the previous month to reach 34.5 million b/d. -

Assessment of a 72-Hour Repeated Exposure to Swedish Snus Extract

Food and Chemical Toxicology 125 (2019) 252–270 Contents lists available at ScienceDirect Food and Chemical Toxicology journal homepage: www.elsevier.com/locate/foodchemtox Assessment of a 72-hour repeated exposure to Swedish snus extract and total T particulate matter from 3R4F cigarette smoke on gingival organotypic cultures ∗ Filippo Zanettia, , Alain Sewera, Bjoern Titza, Walter K. Schlageb, Anita R. Iskandara, Athanasios Kondylisa, Patrice Leroya, Emmanuel Guedja, Keyur Trivedia, Ashraf Elamina, Florian Martina, Stefan Frentzela, Nikolai V. Ivanova, Manuel C. Peitscha, Julia Hoenga a PMI R&D, Philip Morris Products S.A., Quai Jeanrenaud 5, CH-2000 Neuchâtel, Switzerland b Biology Consultant, Max-Baermann-Str. 21, 51429 Bergisch Gladbach, Germany ARTICLE INFO ABSTRACT Keywords: Swedish snus is a smokeless tobacco product that contains reduced levels of harmful compounds compared with Cigarette smoke cigarette smoke. In Sweden, where snus use exceeds smoking among men, relatively low rates of major smoking- Oral health related diseases have been recorded. To better understand how snus use could align with current tobacco harm Swedish snus reduction strategies, its potential mechanisms of toxicity must be investigated. Systems toxicology This study aimed to determine, via a systems toxicology approach, the biological impact of repeated 72-hour Air-liquid interface exposure of human gingival epithelial organotypic cultures to extracts from both a commercial and a reference Smokeless tobacco product snus and the total particulate matter (TPM) from cigarette smoke. At concentrations relevant for human use, cultures treated with snus extracts induced mild, generally reversible biological changes, while TPM treatment induced substantial morphological and inflammatory alterations. Network enrichment analysis and integrative analysis of the global mRNA and miRNA expression profiles indicated a limited and mostly transient impact of the snus extracts, in particular on xenobiotic metabolism, while the effects of TPM were marked and sustained over time. -

BP Midstream Partners LP (Exact Name of Registrant As Specified in Its Charter) Delaware 001-38260 82-1646447 (State Or Other Jurisdiction of (Commission (I.R.S

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (date of earliest event reported): February 25, 2021 BP Midstream Partners LP (Exact name of registrant as specified in its charter) Delaware 001-38260 82-1646447 (State or other jurisdiction of (Commission (I.R.S. Employer incorporation or organization) file number) Identification No.) 501 Westlake Park Boulevard, Houston, Texas 77079 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (281) 366-2000 Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2): Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) ☐ Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol Name of each exchange on which registered Common Units, Representing Limited Partner Interests BPMP New York Stock Exchange Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter). -

Public Information Summary Aleph Midstream S.A. 9000093267

Public Information Summary Aleph Midstream S.A. Argentine Republic Name of Borrower Aleph Midstream S.A. Project Description Develop and expand existing oil and gas transportation and processing facilities in order to provide independent transportation and processing services. These services include gathering, processing, and transportation of shale oil and associated gas production from concessions owned by Vista Oil & Gas Argentina S.A.U. in Argentina’s Vaca Muerta basin (the “Project”). Proposed OPIC USD 150.0 million for up to 10 years Loan/Guaranty Total Project Costs USD 351.3 million U.S. Sponsor Riverstone/Gower Management Co. Holdings LP Foreign Sponsor Vista Oil & Gas S.A.B. de C.V. Policy Review U.S. Economic Impact The Project is not expected to have a negative impact on the U.S. economy or employment. U.S. procurement associated with the Project is expected to have a de minimis positive impact on U.S. employment. The Project is expected to have a positive five-year U.S. balance of trade impact. Developmental Effects This Project is expected to have a highly developmental impact on Argentina by providing wellhead to pipeline processing services for companies drilling oil and gas in the Vaca Muerta reserves in the Neuquén Basin in northern Patagonia. This Project is integral to the success of the development of Vaca Muerta by providing the critical infrastructure necessary to attract additional investment. Development of the shale resources in Vaca Muerta is expected to increase export earnings from the sale of oil and improve the country’s energy independence by reducing the country’s reliance on imported fuel. -

Carbon Dioxide Enhanced Oil Recovery (CO2 EOR)

Carbon Dioxide Enhanced Oil Recovery (CO2 EOR): Factors Involved in Adding Carbon Capture, Utilization and Storage (CCUS) to Enhanced Oil Recovery L. Stephen Melzer CO2 Consultant and Annual CO2 Flooding Conference Director Midland, TX February 2012 Carbon Dioxide Enhanced Oil Recovery (CO2 EOR): Factors Involved in Adding Carbon Capture, Utilization and Storage (CCUS) to Enhanced Oil Recovery Table of Contents I. Introduction II. The Background and Fundamentals of Oil Production and CO2 EOR a. Primary Production Phase b. Secondary Production Phase c. Tertiary Phase III. Current and Projected Flooding CO2 EOR Activity In the U.S. & Permian Basin a. Long-Term Nature of The Industry b. U.S. Project Planning Underway IV. The Effectiveness of CO2 Storage in an EOR Project V. Monitoring CO2 Within The Reservoir: Existing Practices VI. CCUS: Incremental Requirements VII. CO2 Recycle, Reservoir Retention, and CO2 ‘Losses’ During EOR: The Metrics and Experience Base a. Purchases and Recycle Volumes b. CO2 Retention c. CO2 Losses During EOR: Causes and the Experience Base VIII. How to Move Forward? The Urgency and Areas for Caution a. Storage Frameworks b. Recommended Action References FIGURES AND TABLES Figure 1: Number of CO2 EOR Projects (Worldwide, U.S. and Permian Basin) Figure 2: U.S. CO2 EOR Projects, Supply Sources and Pipelines Figure 3: CO2 EOR Production (U.S. and Permian Basin, 1992-2010) Table 1: Basin Scale Criteria for Storage Figure 4: Crossectional Representation of the Various Types of Geologic Basins Table 2: Reservoir Surveillance Tools Commonly Used in CO2 EOR Figure 5: CO2 Flood Surveillance vs. CCUS Monitoring, Measurement and Verification Figure 6: Example CO2 Purchase vs. -

Sustainability Report LETTER from OUR CEO

2017 Sustainability Report LETTER FROM OUR CEO Dear stakeholders In 2017 we presented our strategy: always safe, high value, low In Statoil we believe the winners in the energy transition will be carbon, and we set clear ambitions for the future. Statoil is now a the producers that can deliver at low cost and with low carbon stronger, more resilient and more competitive company. emissions. We believe there are attractive business opportunities in the transition to a low-carbon economy. The safety of our people and integrity of our operations is our top priority. Over the past decade we have steadily improved our We prepare for continued volatility in our markets. Last year safety results. Following some negative developments in 2016, we improved our cash flow and generated USD 3.1 billion in we reinforced our efforts, and last year we again saw a positive free cash flow, tripled adjusted earnings to USD 12.6 billion, development. For the year as a whole, our serious incident and net operating income was to USD 13.8 billion. Statoil’s frequency came in at 0.6. We will use this as inspiration and portfolio continued to improve its robustness in 2017 achieving continue our efforts. The “I am safety” initiative, launched across a breakeven oil price of USD 21 per barrel for next generation the company is an important part of these efforts. projects. Statoil has created substantial value and contributed to the CO2 emissions from our oil and gas production were reduced development of society for almost 50 years. Today we supply by 10% per barrel last year. -

Peak Oil Demand and Long-Run Oil Prices

January 2018 Peak Oil Demand and Long-Run Oil Prices Abstract The prospect that global oil demand will gradually slow and eventually peak has created a cottage industry of executives and commentators trying to predict the point at which demand will peak. In this Energy Insight, we argue that this focus seems misplaced. The date at which oil demand will stop growing is highly uncertain and small changes in assumptions can lead to vastly different estimates. More importantly, there is little reason to believe that once it does peak, that oil demand will fall sharply. The world is likely to demand large quantities of oil for many decades to come. Rather, the significance of peak oil is that it signals a shift in paradigm – from an age of (perceived) scarcity to an age of abundance – and with it is likely to herald a shift to a more competitive market environment. This change in paradigm is also likely to pose material challenges for oil producing economies as they try both to ensure that their oil is produced and consumed, and at the same time diversify their economies fit for a world in which they can no longer rely on oil revenues to provide their main source of revenue for the indefinite future. We argue that the extent and pace of this diversification is likely to have an important bearing on oil prices over the next 20 or 30 years. It seems likely that many low-cost producers will delay the pace at which they adopt a more competitive “higher volume, lower price” strategy until they have made material progress in reforming their economies. -

CMTC-485111-MS Feasibility of CO2-EOR in Shale-Oil

CMTC-485111-MS Feasibility of CO2-EOR in Shale-Oil Reservoirs: Numerical Simulation Study and Pilot Tests Dheiaa Alfarge, Iraqi Ministry of Oil, Missouri University of Science and Technology; Mingzhen Wei and Baojun Bai, Missouri University of Science and Technology Copyright 2017, Carbon Management Technology Conference This paper was prepared for presentation at the Carbon Management Technology Conference held in Houston, Texas, USA, 17-20 July 2017. This paper was selected for presentation by a CMTC program committee following review of information contained in an abstract submitted by the author(s). Contents of the paper have not been reviewed and are subject to correction by the author(s). The material does not necessarily reflect any position of the Carbon Management Technology Conference, its officers, or members. Electronic reproduction, distribution, or storage of any part of this paper without the written consent of the Carbon Management Technology Conference is prohibited. Permission to reproduce in print is restricted to an abstract of not more than 300 words; illustrations may not be copied. The abstract must contain conspicuous acknowledgment of CMTC copyright. Abstract Shale oil reservoirs such as Bakken, Niobrara, and Eagle Ford have become the main target for oil and gas investors as conventional formations started to be depleted and diminished in number. These unconventional plays have a huge oil potential; however, the predicted primary oil recovery is still low as an average of 7.5 %. Injecting carbon dioxide (CO2) to enhance oil recovery in these poor-quality formations is still a debatable issue among investigators. In this study, three steps of research have been integrated to investigate the parameters which control the success of CO2 huff-n-puff process in the field scale of shale oil reservoirs.