Conocophillips Completes Acquisition of Concho Resources

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bakken Production Optimization Program Prospectus

Bakken Production Optimization Program BAKKEN PRODUCTION OPTIMIZATION PROGRAM 2.0 PROSPECTUS PROGRAM INTRODUCTION Led by the Energy & Environmental Research Center (EERC), the highly successful Bakken Production Optimization Program (BPOP), funded by its members and the North Dakota Industrial Commission, is continuing for the time frame of 2017–2020. The goal of this research program, BPOP 2.0, is to improve Bakken system oil recovery and reduce its environmental footprint. The results of the 3-year program will increase well productivity and the economic output of North Dakota’s oil and gas resources, decrease environmental impacts of wellsite operations, and reduce demand for infrastructure construction and maintenance. BPOP 1.0 PARTNERS A premier partnership program was recently completed which has been cited as an exemplary model by others nationwide. It has demonstrated that state lawmakers, state regulators, and industry can work together for positive results for shareholders and taxpayers alike. Phase I partners focused research on industry-driven challenges and opportunities. Continental Resources, Inc. ® Marathon Oil Corporation America’s Oil Champion Whiting Petroleum Corporation North Dakota Oil and Gas Research Program ConocoPhillips Company Nuverra Environmental Solutions Hitachi Hess Corporation Oasis Petroleum, Inc. SM Energy XTO Energy, Inc. BPOP 1.0 ACHIEVEMENTS (2013–2016) Continental’s Hawkinson Project Water Use and Handling Forecast Aimed at significantly increasing total production and A summary of trends in the Bakken, an estimation of production rates from North Dakota oil wells where oil future demand/disposal needs, an overview of treatment reserves of the second and third benches of the Three technologies, recycling/reuse considerations, and a Forks Formation, located just below the Bakken oil summary of implications for BPOP partners were created. -

Monthly Report on Petroleum Developments in the World Markets February 2020

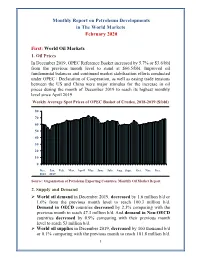

Monthly Report on Petroleum Developments in The World Markets February 2020 First: World Oil Markets 1. Oil Prices In December 2019, OPEC Reference Basket increased by 5.7% or $3.6/bbl from the previous month level to stand at $66.5/bbl. Improved oil fundamental balances and continued market stabilization efforts conducted under OPEC+ Declaration of Cooperation, as well as easing trade tensions between the US and China were major stimulus for the increase in oil prices during the month of December 2019 to reach its highest monthly level since April 2019. Weekly Average Spot Prices of OPEC Basket of Crudes, 2018-2019 ($/bbl) 80 70 60 50 40 30 20 10 0 Dec. Jan. Feb. Mar. April May June July Aug. Sept. Oct. Nov. Dec. 2018 2019 Source: Organization of Petroleum Exporting Countries, Monthly Oil Market Report. 2. Supply and Demand World oil demand in December 2019, decreased by 1.6 million b/d or 1.6% from the previous month level to reach 100.3 million b/d. Demand in OECD countries decreased by 2.3% comparing with the previous month to reach 47.3 million b/d. And demand in Non-OECD countries decreased by 0.9% comparing with their previous month level to reach 53 million b/d. World oil supplies in December 2019, decreased by 100 thousand b/d or 0.1% comparing with the previous month to reach 101.8 million b/d. 1 Non-OPEC supplies remained stable at the same previous month level of 67.2 million b/d. Whereas preliminary estimates show that OPEC crude oil and NGLs/condensates total supplies decreased by 0.6% comparing with the previous month to reach 34.5 million b/d. -

Peak Oil Demand and Long-Run Oil Prices

January 2018 Peak Oil Demand and Long-Run Oil Prices Abstract The prospect that global oil demand will gradually slow and eventually peak has created a cottage industry of executives and commentators trying to predict the point at which demand will peak. In this Energy Insight, we argue that this focus seems misplaced. The date at which oil demand will stop growing is highly uncertain and small changes in assumptions can lead to vastly different estimates. More importantly, there is little reason to believe that once it does peak, that oil demand will fall sharply. The world is likely to demand large quantities of oil for many decades to come. Rather, the significance of peak oil is that it signals a shift in paradigm – from an age of (perceived) scarcity to an age of abundance – and with it is likely to herald a shift to a more competitive market environment. This change in paradigm is also likely to pose material challenges for oil producing economies as they try both to ensure that their oil is produced and consumed, and at the same time diversify their economies fit for a world in which they can no longer rely on oil revenues to provide their main source of revenue for the indefinite future. We argue that the extent and pace of this diversification is likely to have an important bearing on oil prices over the next 20 or 30 years. It seems likely that many low-cost producers will delay the pace at which they adopt a more competitive “higher volume, lower price” strategy until they have made material progress in reforming their economies. -

Welcome to the 11Th Edition of Energy Perspectives! This Is An

Welcome to the 11th edition of Energy Perspectives! This is an independent report that informs Equinor’s strategy and offers a fact-based contribution to the energy transition debate. This year’s edition is an update of the edition from November last year, and with a lot happening on the global arena the last 6 months, there is a lot to consider when looking 30 years ahead. As always, this report and its data and conclusions would be impossible without the excellent work of many of my colleagues, to whom I extend my appreciation and gratitude. You are the best! 1 Covid19 is not over. In a global perspective, we are still dealing with its impact and the enormous effects it has on people, societies, economies, and markets. We are not through it yet. And we might have to live with recurring infection spikes, especially in parts of the world that do not get sufficient access to vaccines. Recurring lockdowns entailed that energy demand, and in particular oil demand due to its use as a transport fuel, was hit hard. Recovery is in the making, and faster than many feared, but oil demand, as an example, is still not back to pre-Covid19-levels. The map shows how the pandemic has affected economies across the globe, with almost all countries pink or red, that is, with negative economic development. Industrialised countries are on their way out of recession while disabling the virus, but the uncertainty is still high in many emerging economies. 2 We are seeing signs of recovery. Thanks to the development and rollout of vaccines and massive public spending to stimulate demand, there are signs that the situation is being brought under control so that we can live with the virus more like we do with normal flus. -

Market Indicators As at End*: August-2020

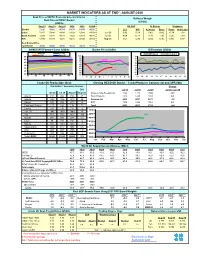

MARKET INDICATORS AS AT END*: AUGUST-2020 Spot Price of OPEC Basket & Selected Crudes Refiners' Margin Real Price of OPEC Basket (US$/b) (US$/b) Aug-18 Aug-19 Aug-20 2018 2019 2020# US Gulf N. Europe Singapore Basket 72.26 59.62 45.19 69.78 64.04 40.50 LLS WTI A. Heavy Brent Oman Arab Light Dubai 72.47 58.88 43.89 69.68 63.48 41.54 Jun-20 3.92 5.19 0.42 0.42 -0.74 1.02 North Sea Dtd 72.64 58.83 44.79 71.22 64.19 40.88 Jul-20 4.64 6.13 -1.86 1.30 1.26 1.99 WTI 67.99 54.84 42.36 65.16 57.02 38.15 Aug-20 3.67 5.30 -2.05 0.16 0.86 0.87 Real Basket Price Jun01=100 46.86 39.02 28.30 35.22 44.73 26.19 NYMEX WTI Forward Curve (US$/b) Basket Price (US$/b) Differentials (US$/b) May-20 Jun-20 WTI-Brent Brent-Dubai Jul-20 Aug-20 50 100 3 90 2 45 2018 80 1 70 40 0 60 35 2019 -1 50 30 40 -2 2020 -3 25 30 20 -4 20 10 -5 1M 3M 5M 7M 9M 11M J F M A M J J A S O N D 03 05 07 11 13 17 19 21 25 27 31 Crude Oil Production (tb/d) Closing OECD Oil Stocks - Crude/Products Commercial and SPR (Mb) Crude Oil Production (Tb/d) Production: Secondary Sources Change Diff. -

Stoxx® Global 1800 Oil & Gas Index

STOXX® GLOBAL 1800 OIL & GAS INDEX Components1 Company Supersector Country Weight (%) Exxon Mobil Corp. Oil & Gas US 14.06 Chevron Corp. Oil & Gas US 12.31 TOTAL Oil & Gas FR 7.51 BP Oil & Gas GB 5.82 ROYAL DUTCH SHELL A Oil & Gas GB 5.14 Enbridge Inc. Oil & Gas CA 4.57 ConocoPhillips Oil & Gas US 3.42 TC ENERGY Oil & Gas CA 2.97 PHILLIPS 66 Oil & Gas US 2.37 KINDER MORGAN Oil & Gas US 2.26 EOG Resources Inc. Oil & Gas US 2.20 Schlumberger Ltd. Oil & Gas US 1.98 Suncor Energy Inc. Oil & Gas CA 1.89 Valero Energy Corp. Oil & Gas US 1.87 ENI Oil & Gas IT 1.82 MARATHON PETROLEUM Oil & Gas US 1.79 Williams Cos. Oil & Gas US 1.68 Canadian Natural Resources Ltd Oil & Gas CA 1.47 VESTAS WIND SYSTEMS Oil & Gas DK 1.43 Occidental Petroleum Corp. Oil & Gas US 1.27 NESTE Oil & Gas FI 1.23 EQUINOR Oil & Gas NO 1.17 Pioneer Natural Resources Co. Oil & Gas US 1.12 ONEOK Inc. Oil & Gas US 1.05 PEMBINA PIPELINE CORP Oil & Gas CA 1.02 Woodside Petroleum Ltd. Oil & Gas AU 1.02 Hess Corp. Oil & Gas US 1.00 REPSOL Oil & Gas ES 0.97 JXTG HOLDINGS INC. Oil & Gas JP 0.86 Halliburton Co. Oil & Gas US 0.83 CONCHO RESOURCES Oil & Gas US 0.79 SNAM RETE GAS Oil & Gas IT 0.78 BAKER HUGHES Oil & Gas US 0.73 AUSTRALIAN PIPELINE Oil & Gas AU 0.57 DIAMONDBACK ENERGY Oil & Gas US 0.54 Inpex Corp. -

NEWS RELEASE June 15, 2021

925 North Eldridge Parkway Houston, TX 77079 Media Relations: 281-293-1149 www.conocophillips.com/media NEWS RELEASE June 15, 2021 ConocoPhillips to Host Market Update June 30 HOUSTON – ConocoPhillips (NYSE: COP) will host a virtual market update on Wednesday, June 30 beginning at 9:00 a.m. Central time. The meeting will feature presentations by ConocoPhillips executives, including Chairman and Chief Executive Officer Ryan Lance. A live webcast of the meeting will be made available on the ConocoPhillips Investor Relations website, www.conocophillips.com/investor. The event will be archived and available for replay later that day. The presentation, along with a transcript, will also be available on the Investor Relations website. --- # # # --- About ConocoPhillips Headquartered in Houston, Texas, ConocoPhillips had operations and activities in 15 countries, $84 billion of total assets, and approximately 10,300 employees at March 31, 2021. Production excluding Libya averaged 1,488 MBOED for the three months ended March 31, 2021, and proved reserves were 4.5 BBOE as of Dec. 31, 2020. For more information, go to www.conocophillips.com. Contacts Media Dennis Nuss 281-293-1149 [email protected] Investor Relations 281-293-5000 [email protected] CAUTIONARY STATEMENT FOR THE PURPOSES OF THE "SAFE HARBOR" PROVISIONS OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 This news release contains forward-looking statements as defined under the federal securities laws. Forward-looking statements relate to future events and anticipated results of operations, business strategies, and other aspects of our operations or operating results. Words and phrases such as “anticipate," “estimate,” “believe,” “budget,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict," “seek,” “should,” “will,” “would,” “expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target” and other similar words can be used to identify forward-looking statements. -

California Resources Corporation (The “Company”) Believes Will Or May Occur in the Future Are Forward-Looking Statements

FINANCIAL AND OPERATING HIGHLIGHTS Dollar and share amounts in millions, except per-share amounts as of and for the years ended December 31, 2015 2014 2013 Financial Highlights Revenues $ 2,403 $ 4,173 $ 4,284 Income / (Loss) Before Income Taxes $ (5,476 ) $ (2,421 ) $ 1,447 Net Income / (Loss) $ (3,554 ) $ (1,434 ) $ 869 Adjusted Net Income / (Loss) (a) $ (311) $ 650 $ 869 EPS – Basic and Diluted (b) $ (9.27 ) $ (3.75 ) $ 2.24 Adjusted EPS – Basic and Diluted (b) $ (0.81) $ 1.67 $ 2.24 Net Cash Provided by Operating Activities $ 403 $ 2,371 $ 2,476 Capital Investments $ (401 ) $ (2,089 ) $ (1,669 ) Proceeds from Debt, Net $ 379 $ 6,360 — Cash Dividends to Occidental — $ (6,000 ) — Net Cash Provided (Used) by Financing Activities $ 352 $ (45) $ (763) Total Assets $ 7,053 $ 12,429 $ 14,297 Long-Term Debt – Principal Amount $ 6,043 $ 6,360 — Deferred Gain and Issuance Costs, Net $ 491 $ (68 ) — Equity / Net Investment $ (916) $ 2,611 $ 9,989 Weighted Average Shares Outstanding 383.2 381.9 — Year-End Shares 388.2 385.6 — Operational Highlights 2015 2014 2013 Production: Crude Oil (MBbl/d) 104 99 90 NGLs (MBbl/d) 18 19 20 Natural Gas (MMcf/d) 229 246 260 Total (MBoe/d) 160 159 154 Average Realized Prices: Crude with hedge ($/Bbl) $ 49.19 $ 92.30 $ 104.16 Crude without hedge ($/Bbl) $ 47.15 $ 92.30 $ 104.16 NGLs ($/Bbl) $ 19.62 $ 47.84 $ 50.43 Natural Gas with hedge ($/Mcf) $ 2.66 $ 4.39 $ 3.73 Reserves: Crude Oil (MMBbl) 466 551 532 NGLs (MMBbl) 59 85 71 Natural Gas (Bcf) 715 790 844 Total (MBoe/d) 644 768 744 Acreage (in thousands): Net Developed 736 716 701 Net Undeveloped 1,653 1,691 1,604 Total 2,389 2,407 2,305 Closing Share Price $ 2.33 $ 5.51 (a) For discussion of, or reconciliation to the most closely-related GAAP measure, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Results,” in our Form 10-K. -

The Economic Impact of Oil Prices by Rurik Krymm

The Economic Impact of Oil Prices by Rurik Krymm During the last three months of 1973, the tax-paid costs of typical grades of crude petroleum in the main producing areas of the world, around the Persian Gulf, were roughly quadrupled, rising for typical Iranian and Arabian Ugh t crudes from about $1.85 per barrel in September 1973 to more than $7.00 by 1 January 1974, or from approximately $13.30 to more than $50.00per ton. Since the cost of production represents an insignificantly small fraction of the new cost level (less than 2%) and subject to complex adjustments reflecting varying qualities of crude oils and advantages of geographical location, the producing countries may expect to receive a minimum average revenue of $50.00 per ton of crude oil produced on their territory instead of $12.50. If we ignore the purchases which carried the prices of relatively small amounts of oil to the $100-$ 150range, this figure of $50.00per ton with future adjustments for inflation represents a probable guide line for future cost estimates. The change affects exports of close to 1.4 billion tons of oil and consequently involves an immediate shift of financial resources of close to 60 billion dollars per year from the oil-consuming to the oil-producing countries. Tables 1, 2 and 3 give an idea of the distribution of this burden by main geographical regions and of its possible evolution over the next seven years. The figures involved are so large that comparisons have been made by some authors with the reparations proposals advanced by the Allies at the end of the First World War. -

Construction to Start by Year's End Conocophillips Strikes $9.7B Deal

Leading Utica Producer Gulfport in Restructuring Talks with Lenders.............................2 Tuesday, October 20, 2020 - Vol. 11, No. 13 PERMIAN BASIN ConocoPhillips Strikes $9.7B Deal to Buy Concho, Create Permian Behemoth ConocoPhillips on Monday announced it is taking over Concho Resources Inc. for $9.7 billion in stock, forming a giant in the Permian Basin that would rival the output of the biggest players in the nation’s most produc- tive oilfield. Concho, a Permian pure-play, is the fifth-largest producer by volume in the massive field. The combina- tion marks the largest Lower 48 industry acquisition an- nounced since the pandemic arrived in the United States in March. The deal would elevate ConocoPhillips into a small pool of dominant players in the Permian, joining Trade Date: Oct 19; Flow Date(s): Oct 20 …cont' pg. 2 leaders such as Occidental Petroleum Corp. and Basin/Region Range Avg Chg Vol Deals Gulf Coast Barnett 2.130-2.300 2.260 0.175 198 38 BAKKEN SHALE Eagle Ford 2.650-2.850 2.685 0.270 348 57 Haynesville - E. TX 2.150-2.370 2.280 0.205 1,807 290 North Dakota Sees Oil, Natural Gas Haynesville - N. LA 2.300-2.360 2.315 0.255 162 36 Permian1 -0.750-2.100 -0.245 0.050 668 144 Production Climb in August Tuscaloosa Marine Shale 2.300-2.360 2.340 0.200 424 68 North Dakota oil and natural gas production shot up Midcontinent Arkoma - Woodford 2.100-2.280 2.200 0.160 188 32 in August along with gas capture volumes, but the produc- Cana - Woodford 2.400-2.550 2.470 0.445 64 13 tion surge is expected to fall back and continue declining Fayetteville 2.290-2.300 2.295 0.245 126 30 Granite Wash* 2.010-2.360 2.295 0.235 857 162 by the end of the year. -

OPEC Annual Statistical Bulletin 2019 1 Contents

2019 OPEC Annual Statistical Bulletin Organization of the Petroleum Exporting Countries 1965 – 2019 th edition 54 Team for the preparation of the OPEC Annual Statistical Bulletin Secretary General Editorial Team Chairman of the Editorial Board Head, Public Relations and Information Department Mohammad Sanusi Barkindo Hasan Hafidh Director, Research Division Editor Ayed S. Al-Qahtani Maureen MacNeill, Mathew Quinn Project Leader Coordinator, Design and Production Head, Data Services Department Carola Bayer Adedapo Odulaja Senior Production Assistant Coordinator, Statistics Team Diana Lavnick Hossein Hassani Graphic Designer Statistics Team Tara Starnegg Pantelis Christodoulides, Klaus Stöger, Mohammad Sattar, Mihni Mihnev, Justinas Pelenis, Ksenia Gutman Coordinator, IT Development Team Mohamed Mekerba IT Development Team Vedran Hrgovcic, Zairul Arifin Online Annual Statistical Bulletin 2019: asb.opec.org Download now: Smart App for OPEC Annual Statistical Bulletin iOS Android Questions on data Data queries: [email protected]. Advertising The OPEC Annual Statistical Bulletin now accepts advertising. For details, please contact the Head, PR and Information Department, at the following address: Organization of the Petroleum Exporting Countries Helferstorferstrasse 17, A-1010 Vienna, Austria Tel: +43 1 211 12/0 Fax: +43 1 216 43 20 Advertising: [email protected] Website: www.opec.org Photographs Courtesy OPEC. © 2019 Organization of the Petroleum Exporting Countries ISSN 0475-0608 Contents Foreword 5 Key messages 6 Tables Page Page Section -

Virtual Global Oil and Gas Conference Agenda

Virtual Global Oil and Gas Conference Agenda Tuesday, May 19, 2020 Times are listed in Central Daylight Time (CDT) (F) = Fireside Chat 8:00 a.m. Tourmaline Oil Corporation Mike Rose, President & CEO 8:50 a.m. Pembina Pipeline Corporation (F) Scott Burrows, Senior VP & CFO 9:40 a.m. Magellan Midstream Partners, L.P. (F) Aaron Milford, Chief Operating Officer 10:30 a.m. Evidence Lab Cody Rice, Solution Specialist –Energy Ben Nunnery, Engagement Manger 11:20 a.m. Rystad Energy (F) Artem Abramov, Head of Shale Research 12:10 p.m. Northern Oil & Gas Nicholas O'Grady, Chief Financial Officer Mike Kelly, EVP of Finance 1:00 p.m. Noble Energy (F) Brent Smolik, President & COO 1:50 p.m. TechnipFMC plc Doug Pferdehirt, Chairman & CEO 5:00 p.m. Conference concludes Companies hosting 1x1 meetings only: Berry Corporation, BP, Devon Energy Corporation, Eni SpA, Equinor ASA, GeoPark Limited, Magnolia Oil & Gas Corporation, Panhandle Oil and Gas Inc, Penn Virginia Corp, Schlumberger Ltd, Sundance Energy, Tellurian Inc, , Vista Oil & Gas, Western Midstream Partners. © UBS 2020. The key symbol and UBS are among the registered and unregistered trademarks of UBS. All rights reserved. All pictures or images presented herein are for illustrative purposes only. No relationship, association, sponsorship, or endorsement is suggested or implied between UBS and any landmarks or properties, o r with their respective owners, organizations, management, sponsors, investors or patrons Virtual Global Oil and Gas Conference Agenda Wednesday, May 20, 2020 Times are listed in Central Daylight Time (CDT) (F) = Fireside Chat 8:00 a.m.