Anaysis Phase Appendix V2

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Der Neue SEAT Arona* Ist Die Beste Kaufoption

Autovista-Studie Der neue SEAT Arona* ist die beste Kaufoption / Crossover-Modell mit höchster Wertbeständigkeit im Segment / Exzellentes Zeugnis für den SEAT Arona / Kaufempfehlung durch unabhängige Experten / „Neue Kunden im Flottengeschäft gewinnen” Weiterstadt/London, 02.10.2017 – Dass sich die Modelle von SEAT durch ein attraktives Design, innovative Technologie, ein hohes Maß an Sicherheit und dynamische Fahrperfomance auszeichnen, dürfte mittlerweile weithin bekannt sein. Der neue SEAT Arona*, der erste kompakte Crossover der Marke und zugleich das zweite SEAT Modell, das exklusiv im spanischen Martorell auf Basis der neuen Konzernplattform MQB A0 gefertigt wird, bildet da keine Ausnahme. Hohe Qualität und Wertbeständigkeit Im Gegenteil: So bietet der SEAT Arona zahlreiche technische Vorzüge und eine überdurchschnittlich hohe Qualität über seinen gesamten Produktzyklus hinweg. Das lässt für den jüngsten Neuzugang der SEAT Modellfamilie schon heute einen hohen Wiederverkaufswert erwarten. Zu diesem Schluss kommt eine aktuelle Studie des Beratungsunternehmens Autovista Group. Viele Faktoren entscheiden beim Autokauf Die Entscheidung zum Kauf eines neuen Autos lässt sich nicht leichtfertig treffen. Sie setzt eine sorgfältige Bewertung verschiedenster Faktoren durch den Kunden voraus – egal ob es sich dabei um eine Privatperson oder einen Firmenkunden handelt. Dabei müssen nicht nur der Kaufpreis, sondern auch die Instandhaltungskosten und der Wertverlust über die gesamte Nutzungsdauer des Fahrzeugs in die Gesamtbetrachtung einbezogen werden. Aus diesem Grund hat SEAT die beiden genannten Aspekte schon bei der Entwicklung des neuen SEAT Arona in den Mittelpunkt gestellt. Studie: SEAT Arona hat den geringsten Wertverlust Mit Erfolg: In ihrer neuesten Studie, die speziell das Segment der Kompakt- Crossover-Modelle unter die Lupe nimmt, stellen die Experten der Autovista Group dem SEAT Arona ein exzellentes Zeugnis aus. -

BIL Swedens Nyregistreringsstatistik

2019-05-02 Elbilar ökade på en minskad totalmarknad i april - Nyregistreringarna av laddbara bilar, dvs elbilar och laddhybrider, ökade med 44 procent i april jämfört med april förra året. Uppgången var särskilt stor för rena elbilar, plus 271 procent. Närmare hälften av de laddbara bilarna i april i år var rena elbilar, jämfört med knappt var femte i april förra året. Totalmarknaden för nya personbilar minskade däremot med 11,6 procent. Det var väntat med en nedgång då vi har den bästa högkonjunkturen bakom oss och i linje med vår prognos för året. April förra året var den bästa aprilmånaden någonsin för nya personbilar med ökad efterfrågan inför det nya skattesystemet som infördes i juli. Den nya testmetoden WLTP (Worldwide Harmonized Light Vehicle Test Procedure), som medfört förlängda leveranstider, har en fortsatt negativ påverkan på registreringstakten med långa leveranstider för många modeller, säger Mattias Bergman, vd för BIL Sweden. Ökad andel laddbara bilar – viktigt steg för att nå våra klimatmål - Andelen laddbara bilar av de totala nyregistreringarna var 10,1 procent i april jämfört med 6,2 procent i april förra året. Under de fyra första månaderna i år var andelen 12,4 procent mot 6,7 procent motsvarande period förra året. Det är en glädjande utveckling och ett viktigt steg på vägen mot att minska utsläppen. Det ökade antalet laddbara bilar på våra vägar sätter fingret på behovet av att utbyggnaden av laddinfrastrukturen både för hemmaladdning och snabbladdning påskyndas. Andra åtgärder som bör vidtas är att introducera styrmedel även för användandet av laddbara bilar och inte bara vid köptillfället, säger Mattias Bergman. -

SEAT Adds a Raft of New Features and Enhancements to Its Vehicle Line-Up

Hola! SEAT adds a raft of new features and enhancements to its vehicle line-up ▪ The SEAT digital lives into the cabin ▪ The all-new SEAT Leon enters full production, increases its options list and improves its convenience ▪ The new SEAT Ateca 2020 starts rolling off the production line ▪ largest SUV, the SEAT Tarraco, adds new features improving its design, performance, convenience and comfort Martorell, 26/08/2020 SEAT is ramping up its product offensive with new vehicles joining the family while others receive additonal features and functionality to make them even more STAMPA desirable. New features and enhancements for the entire range and first all-electric vehicle, the SEAT Mii electric city car meets the demand to NEWS reduce the impact on the environment. The city car brings together a state-of-the-art powertrain and high levels of connectivity, but now adds DAB+ radio as standard. The technology offers access to a greater number of stations at even better audio quality. Connectivity is at the centre of the revisions to the SEAT Ibiza and SEAT Arona with both PRESSE vehicles benefitting from SEAT Connect. The technology brings new levels of digitalisation to the compact SEAT Ibiza hatchback and SEAT Arona SUV, meaning customers will be able to bring more of their connected infotainment system. Featuring in-car and out-car connectivity with online-based navigation function and services, PREMSA Full Link with Android Auto and Apple CarPlay and voice recognition for smoother, more natural interaction. But not only that, the SEAT Ibiza and SEAT Arona also now works with the SEAT Connect app. -

Noticias Completas Del 21-10-20 En

21-10-20 21/10/2020 Indice Estudiantes que se involucran en mejorar la sociedad en la era Covid 4 Álvaro Pérez García: «El emprendimiento es la salida profesional más segura para los jóvenes» Una formación de excelencia internacional 65 La IV edición del proyecto Marketing Experience se centra en el uso de videojuegos para la promoción de una marca Marketing 7 Seat ficha a un ejecutivo valenciano de Mitsubishi como director de diseño 8 «El emprendimiento es la salida profesional más segura para los jóvenes» 9 Una formación de excelencia internacional 13 Estudiantes que se involucran en mejorar la sociedad en la era Covid 16 La Universidad CEU Cardenal Herrera organiza un taller sobre prevención y autoexploración de la mama 18 EL CEU CARDENAL HERRERA DESARROLLA UN TALLER SOBRE PREVENCIÓN Y AUTOEXPLORACIÓN DE MAMA IMPARTIDO POR UNA MATRONA DEL… 26 El CEU organiza un taller sobre prevención y autoexploración de la mama 08:46 28 La hipertensión arterial es la comorbilidad más frecuente en el paciente COVID-19 31 Una investigación liderada por SEMI con datos de más de 12.000 pacientes descifra el vínculo entre hipertensión… 35 La hipertensión arterial aumenta el riesgo de muerte en pacientes con COVID-19 37 Fundación Vithas inaugura la IX edición del Máster Universitario en Técnicas Avanzadas Estéticas y Láser de la mano de… 39 Sham analiza el impacto jurídico-legal de la COVID-19 en el sector sanitario 41 Jorge Díez, nuevo director de Diseño para SEAT y CUPRA 42 El español Jorge Díez será el nuevo jefe de diseño de Seat y Cupra 46 El español -

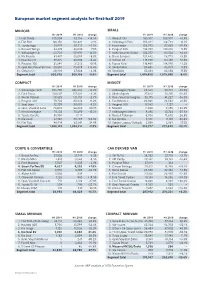

European Market Segment Analysis for First-Half 2019

European market segment analysis for first-half 2019 MINICAR SMALL H1 2019 H1 2018 change H1 2019 H1 2018 change 1. Fiat Panda 105,534 92,156 +14.5% 1. Renault Clio 185,517 183,907 +0.9% 2. Fiat 500 100,150 110,221 -9.1% 2. Volkswagen Polo 146,344 162,799 -10.1% 3. Toyota Aygo 51,479 50,713 +1.5% 3. Ford Fiesta 125,795 157,068 -19.9% 4. Renault Twingo 44,374 48,030 -7.6% 4. Peugeot 208 124,730 132,010 -5.5% 5. Volkswagen Up 43,732 50,950 -14.2% 5. Opel/Vauxhall Corsa 122,277 116,924 +4.6% 6. Kia Picanto 41,497 38,099 +8.9% 6. Dacia Sandero 121,442 114,779 +5.8% 7. Hyundai i10 38,375 43,802 -12.4% 7. Citroen C3 118,799 116,120 +2.3% 8. Peugeot 108 31,349 31,313 +0.1% 8. Toyota Yaris 116,469 114,990 +1.3% 9. Opel Karl/Vauxhall Viva 30,030 26,029 +15.4% 9. Skoda Fabia 86,485 95,979 9.9% 10. Citroen C1 28,993 27,866 +4.0% 10. Seat Ibiza 52,031 63,054 -17.5% Segment total 603,925 606,196 -0.4% Segment total 1,474,490 1,575,068 -6.4% COMPACT MIDSIZE H1 2019 H1 2018 change H1 2019 H1 2018 change 1. Volkswagen Golf 206,785 246,666 -16.2% 1. Volkswagen Passat 65,646 92,710 -29.2% 2. Ford Focus 128,087 117,204 +9.3% 2. -

Analisis Economico, Ambiental Y Social Seat ( Grupo Volkswagen ) 2015-2018

ANALISIS ECONOMICO, AMBIENTAL Y SOCIAL SEAT ( GRUPO VOLKSWAGEN ) 2015-2018 Elabora: Marta Ayala Benito Julio 2019 INDICE 1. SEAT ( GRUPO VOLKSWAGEN ) ............................................................................. Pag 3 2. ANALISIS ECONOMICO ............................................................................................ Pag 5 2.1. Estructura Patrimonial ............................................................................................ Pag 5 2.1.1.Analisis Liquidez ............................................................................ Pag 6 2.1.2.Analisis Solvencia .......................................................................... Pag 6 2.2. Resultados del Ejercicio ........................................................................................ Pag 8 2.2.1.Estructura costes ............................................................................. Pag 9 2.2.2.Evolucion de la actividad y resultados ......................................... Pag 10 2.2.3.Evolucion de la productividad ...................................................... Pag 15 3. ANALISIS SOCIAL Y AMBIENTAL ....................................................................... Pag 16 3.1. Análisis plantilla .................................................................................................. Pag 16 3.2. Indicadores Genero .............................................................................................. Pag 18 3.3. Formación ............................................................................................................ -

Cars-Models-Brochure-All-NA-July-2019.Pdf

SEAT FOR BUSINESS. Driver first. More than 60 years of expertise and passion. We’re committed to offering our best, always keeping the comfort and well-being of our drivers in mind. SEAT’s model range brings you dynamic and stylish cars, built with the highest standards and most up to date technology. Cost-effective. Fuel-efficient. Eco-friendly. And an exceptional aftersales service, as well as considerable savings for purchase managers. Are you ready to be our next fleet customer? Giuseppe Tommaso Director of International Fleet Sales & Remarketing. Our global range of cars and product specifications varies from country to country. Please, visit your local SEAT website to know more about the product offer available for you. 01 02 Competitive total cost of ownership. Safety and 03 technologies for Business. TGI Range. 04 Exclusive B2B service 05 network. Fleet 06 portfolio. New SEAT Tarraco. 07 SEAT Ateca. International SEAT Arona. framework SEAT Leon range. 08 SEAT Ibiza. agreement. SEAT Alhambra. Micromobility. A dedicated team. Our global range of cars and product specifications varies from country to country. Please, visit your local SEAT website to know more about the product offer available for you. Competitive total cost of ownership. The road ahead TCO Segmentation matters. by cost. 8% Financing cost SEATs are cost-effective today – and tomorrow. 5% Taxes We offer you some of the lowest costs per 8% kilometre in the industry. Service packages Maintenance that keep your maintenance expenses low. /repairs And optimal residual value, a key component 5% Tyres of long-term overhead. 47%Depreciation Insurance12% Residual Value corresponds nearly to 50% of TCO. -

SEAT Arona. De Crossover Is Geland

SEAT Arona. De crossover is geland. Gedraag je zus. Kleed je zo. Rijd met dit, rijd met dat. Het leven zit vol stemmen die je vertellen wat je moet doen. De echte durvers luisteren alleen naar hun eigen stem. Bewandelen hun eigen pad. En nu krijgen ze ruggensteun. De SEAT Arona is de stadscrossover ontworpen voor de onvervaarden. Slim. Krachtig. Dynamisch. Zodat je overal en altijd je eigen ding kunt doen. Wat dat ook moge zijn. 2 01 SEAT. 06 Gemaakt in Barcelona 08 Easy Mobility 02 Jouw Arona. 03 12 Exterieurdesign 22 Interieurdesign 26 Technologie Jouw 28 Veiligheid manier. 04 32 FR 36 Xcellence Jouw 40 Style 44 Reference 46 Velgen accessoires. 48 Kleuren 54 Prestaties 50 Bekleding 56 Interieur 05 58 Interieurpersonalisering 62 Interieurpersonalisering Tot je 66 Transport 72 Bescherming 74 Infotainment & Veiligheid dienst. 76 Crossover Line 82 Milieu-informatie 4 Gemaakt in Barcelona. 1953. De eerste SEAT rolt van onze productielijn in Barcelona en een heel land komt in beweging. Meer dan 60 jaar later brengen wij overal ter wereld mensen in beweging. Maar Barcelona blijft ons inspireren. Haar creatieve geest zit ons in het bloed. Iedere auto die wij produceren is ervan doordrenkt. (50% van de energie die wij gebruiken om onze wagens te maken, halen wij namelijk rechtstreeks uit de mediterraanse zon.) Dit is een stad die nooit stilvalt. Net zomin als wij. Waarom? Omdat er zoveel te beleven valt. 6 Easy mobility. De wereld zit vol mogelijkheden. SEAT maakt het je gemakkelijk om ze te benutten. Stippel je eigen route uit. Kies je eigen doelen. -

European Market Segment Analysis for 2020

European market segment analysis for 2020 Minicar Small 2020 2019 change 2020 2019 change 1. Fiat Panda 144,348 183,604 -21.4% 1. Renault Clio 247,351 316,733 -21.9% 2. Fiat 500 137,265 170,892 -19.7% 2. Peugeot 208 198,570 223,810 -11.3% 3. Toyota Aygo 83,277 99,483 -16.3% 3. Opel/Vauxhall Corsa 197,192 220,246 -10.5% 4. Renault Twingo 73,191 86,495 -15.4% 4. Toyota Yaris 179,674 212,064 -15.3% 5. VW Up 59,299 79,271 -25.2% 5. VW Polo 167,826 255,180 -34.2% 6. Hyundai i10 50,043 78,971 -36.6% 6. Dacia Sandero 167,291 223,222 -25.1% 7. Kia Picanto 48,997 75,044 -34.7% 7. Ford Fiesta 155,145 227,675 -31.9% 8. Peugeot 108 43,216 55,013 -21.4% 8. Citroen C3 148,555 211,937 -29.9% 9. Citroen C1 40,223 50,316 -20.1% 9. Renault Zoe 99,686 45,729 -- 10. Smart ForTwo 19,623 77,373 -74.6% 10. Skoda Fabia 98,356 157,177 -37.4% Segment total 735,481 1,130,092 -34.9% Segment total 2,029,376 2,687,918 -24.5% Compact Midsize 2020 2019 change 2020 2019 change 1. VW Golf 283,651 408,077 -30.5% 1. VW Passat 115,763 125,049 -7.4% 2. Skoda Octavia 181,039 220,127 -17.8% 2. Skoda Superb 60,254 68,926 -12.6% 3. Ford Focus 172,565 223,374 -22.7% 3. -

SEAT Pricelist Jul 2021

SEAT (Singapore) Price List Price EIective from 12th July to 21st July 2021 DEMO PRICE FROM $89,999 Enjoy trade-in price of up to $20,000 * above market valuation for selected models $0 DRIVE-AWAY AVAILABLE VES Band Fuel Consumption List Price Promo Price From SEAT IBIZA SEAT IBIZA Style Plus (1.0) B 4.7 L/100km $137,999 $95,999 SEAT IBIZA FR (1.5) New Variant A2 5.0 L/100km $145,999 $104,999 SEAT ARONA SEAT ARONA Style (1.0) A2 5.0 L/100km $157,999 $102,999 SEAT ARONA Style Plus (1.0) A2 5.0 L/100km $159,999 $104,999 SEAT ARONA FR (1.0) A2 5.0 L/100km $159,999 $110,999 SEAT ARONA FR (1.5) New Variant B 5.0 L/100km $165,999 $120,999 SEAT LEON NEW MODEL NEW SEAT LEON FR 1.5 mHEV A2 5.0 L/100km $165,999 $125,999 SEAT LEON SPORTSTOURER NEW MODEL SEAT LEON SPORTSTOURER FR 1.5 mHEV A2 5.0 L/100km $170,999 $130,999 LOCATE US: CONNECT WITH US: AUTHORISED DISTRIBUTOR SEAT Centre (Ubi) SEAT Centre (Leng Kee) Address: 3 Ubi Road 4, Address: 2 Kung Chong Road Singapore 408608 (oI Hoy Fatt Road) Singapore 159140 Tel: +65 6742 3393 Tel: +65 6970 7889 WWW.SEAT.SG SEAT.SG SEATSINGAPORE New SEAT Ateca Free upgrade to SEAT Tarraco FREE UPGRADE* from 7 SEATER SEAT 5 SEATER to VES Band Fuel Consumption List Price Promo Price From SEAT ATECA (8-SPEED TRANSMISSION) SEAT ATECA Style (1.4) B 6.2 L/100km SOLD OUT SEAT ATECA Xcellence (1.4) B 6.2 L/100km $178,999 $143,999 NEW SEAT ATECA (8-SPEED TRANSMISSION) NEW MODEL NEW SEAT ATECA Style (1.4) B 6.2 L/100km $183,999 $146,999 NEW SEAT ATECA Xperience (1.4) B 6.2 L/100km $189,999 $154,999 SEAT TARRACO (7-SEATER SUV) SEAT TARRACO Style (1.4) C1 7.4 L/100km $202,999 $167,999 SEAT TARRACO Xcellence (1.4) C1 7.4 L/100km $208,999 $173,999 SEAT ALHAMBRA (7-SEATER MPV) SEAT ALHAMBRA Style (1.4) C1 7.1 L/100km $212,999 $168,999 SEAT ALHAMBRA Style (2.0) C1 7.5 L/100km $220,999 $178,999 TERMS & CONDITIONS 1. -

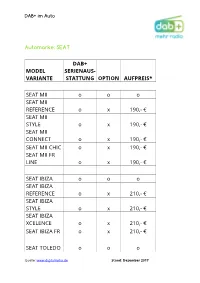

Automarke: SEAT MODEL VARIANTE DAB+ SERIENAUS

DAB+ im Auto Automarke: SEAT DAB+ MODEL SERIENAUS- VARIANTE STATTUNG OPTION AUFPREIS* SEAT MII o o o SEAT MII REFERENCE o x 190,- € SEAT MII STYLE o x 190,- € SEAT MII CONNECT o x 190,- € SEAT MII CHIC o x 190,- € SEAT MII FR LINE o x 190,- € SEAT IBIZA o o o SEAT IBIZA REFERENCE o x 210,- € SEAT IBIZA STYLE o x 210,- € SEAT IBIZA XCELENCE o x 210,- € SEAT IBIZA FR o x 210,- € SEAT TOLEDO o o o Quelle: www.digitalradio.de Stand: Dezember 2017 DAB+ im Auto SEAT TOLEDO EURO o x 210,- € SEAT TOLEDO REFERENCE o x 210,- € SEAT TOLEDO STYLE o x 210,- € SEAT TOLEDO STYLE PLUS o x 210,- € SEAT TOLEDO FR LINE o x 210,- € SEAT LEON o o o SEAT LEON REFERENCE o x 210,- € SEAT LEON STYLE o x 210,- € SEAT LEON 210,- €/805,- XCELLENCE o x € 210,- €/805,- SEAT LEON FR o x € SEAT LEON SC o o o SEAT LEON SC REFERENCE o o 210,- € SEAT LEON 210,- STYLE o x €/1350,- € SEAT LEON SC 210,- €/805,- FR o x € Quelle: www.digitalradio.de Stand: Dezember 2017 DAB+ im Auto SEAT LEON ST o o o SEAT LEON ST REFERENCE o o o SEAT LEON ST 210,- STYLE o x €/1310,- € SEAT LEON ST 210,- €/805,- XCELLENCE o x € SEAT LEON ST 210,- €/805,- FR o x € SEAT LEON X- 210,- PERIANCE o x €/1210,- € SEAT LEON SC CUPRA o x 210,- € SEAT ARONA FR o x 210,- € SEAT ARONA XCELLENCE o x 210,- € SEAT ARONA STYLE o x 210,- € SEAT ARONA REFERENCE o x 210,- € SEAT ATECA REFERENCE o x 215,- € Quelle: www.digitalradio.de Stand: Dezember 2017 DAB+ im Auto SEAT ATECA STYLE o x 215,- € SEAT ATECA XCELLENCE o x 215,- € SEAT ATECA FR o x 215,- € SEAT ALHAMBRA REFERENCE o x 210,- € SEAT ALHAMBRA 210,- STYLE o x €/1115,- € SEAT ALHAMBRA FR 210,- LINE o x €/1115,- € Legende: O = nein X = ja *Diese Angaben sind UVP-Preise. -

Alfa-Romeo Audi Ua Mit Den Motoren EA189 Oder EA288

Liste betroffener PKW (alphabetisch nach Hersteller sortiert) Alfa-Romeo Alfa-Romeo Giulietta 2.0 (Euro 5) Audi u. a. mit den Motoren EA189 oder EA288 3,0 Liter-V6-Motoren der Schadstoffklasse Euro 6: Audi A4 3.0 TDI, Typ B8 (Modelljahre 2009 – 2017) Audi A5 3.0 TDI, Typ B8 (Modelljahre 2011 – 2017) Audi A6 3.0 TDI, Typ 4G (Modelljahre 2011 – 2018) mit 155 kW, 160 kW, 180 kW und 200 kW sowie der 3.0 TDI Biturbo mit 235 kW und 240 kW Audi A7 3.0 TDI, Typ 4G (Modelljahre 2011 – 2018) mit 155 kW, 160 kW, 180 kW und 200 kW sowie der 3.0 TDI Biturbo mit 235 kW und 240 kW Audi A8 3.0 TDI Typ 4H (Modelljahre 2010 – 2017) mit 150 kW, 155 kW, 184 kW, 190 kW und 193 kW Audi A8 4.2 TDI Typ 4H (Modelljahre 2010 – 2017) mit 283 kW Audi Q53.0 TDI Typ 8R (Modelljahre 2014 – 2017) mit 184 kW und 190 kW Audi SQ5 3.0 TDI Typ 8R (Modelljahre 2015 – 2018) mit 230 kW und 240 kW Audi SQ5 plus 3.0 TDI Typ 8R (Modelljahre 2015 – 2018) mit 250 kW Audi Q7 3.0 TDI Typ 4L (Modelljahre 2008 – 2015) mit 176 kW und 180 kW 3,0 Liter-V6-Motoren der Schadstoffklasse Euro 5: neu Audi A6 3.0 TDI, Typ 4G, 230 kW (Modelljahre 2010 – 2015) neu Audi S6 3.0 TDI, Typ 4G, 230 kW (Modelljahre 2010 – 2015) neu Audi A6 3.0 TDI, Typ 4G, 230 kW (Modelljahre 2010 – 2015) neu Audi S7 3.0 TDI, Typ 4G, 230 kW (Modelljahre 2010 -2015) Audi A8 3.0 TDI, Typ 4H (Modelljahre 2010 – 2014) 2,0 Liter oder 1,6 Liter Motoren der Schadstoffklasse Euro 5: Audi A1 (1.6 TDI, 2.0 TDI) (Sportback) Audi A3 (1.6 TDI, 2.0 TDI) (Cabriolet, Sportback) Audi A4 (2.0 TDI) (Cabriolet, Allroad, Avant, Quattro) Audi A5 (2.0 TDI) (Cabriolet.