Vienna University of Economics and Business Master Thesis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Market Outlook 2017–2036

MARKET OUTLOOK 2017–2036 Scientific research parades after idea, fantasy, and fairytale. K. Tsiolkovsky TABLE OF CONTENTS INTRODUCTION INTRODUCTION ....................................................................................................................................... 1 A decade of development of the United Aircraft Corporation attractive conditions for acquisition, leasing, lending in modern Russia makes it possible to speak more and and repurchase of aircraft with a guarantee of their AIR TRANSPORTATION MARKET ............................................................................................................ 2 more confidently of strengthening of the Company’s residual value. WORLD COMMERCIAL AIRCRAFT FLEET ............................................................................................... 6 positions in the global civil aircraft market. MARKET OF TURBOPROP AIRCRAFT ..................................................................................................... 10 The processes of globalization provided an opportunity to Having united the best traditions and design experience form effective international cooperation in the creation of MARKET OF NARROW-BODY AIRCRAFT WITH A CAPACITY OF 61–120 SEATS ................................... 12 of world’s famous aircraft manufacturers such as Tupolev, new aircraft. Currently, several UAC’s promising civil and MARKET OF NARROW-BODY AIRCRAFT WITH A CAPACITY EXCEEDING 120 SEATS........................... 14 Ilyushin and Yakovlev Design Bureaus, as well as -

Rostec Will Create a Single Corporate Aircraft Manufacturing Center in Moscow

50SKYSHADESImage not found or type unknown- aviation news ROSTEC WILL CREATE A SINGLE CORPORATE AIRCRAFT MANUFACTURING CENTER IN MOSCOW News / Manufacturer Image not found or type unknown © 2015-2021 50SKYSHADES.COM — Reproduction, copying, or redistribution for commercial purposes is prohibited. 1 Rostec State Corporation will unite UAC, Sukhoi and MiG companies into a single corporate aircraft manufacturing center, which will consolidate the management of aircraft programs and other UAC assets. The engineering and design functions of the group will be separated into a separate center, which will be located in Moscow - it will include all aviation design bureaus. Such decisions were announced by the General Director of the State Corporation Rostec Sergey Chemezov at a meeting with the management of the United Aircraft Corporation and its leading engineering centers, where the tasks of the development of the aircraft industry for the coming years were discussed. The objectives of the transformations being carried out are to increase the economic sustainability of the UAC Group, optimize the administrative and managerial staff, and reduce non-production costs and debt burden. To control the ongoing transformations, the head of Rostec, Sergey Chemezov, intends to personally head the UAC Board of Directors. The optimization will not affect the engineering staff. Design schools will remain independent, receive new opportunities for development, as well as improved working conditions in the format of the Unified Engineering and Design Center. The center will be located in Moscow, where the existing test and bench infrastructure of the UAC is concentrated. Moving aviation design bureaus to other regions is not on the agenda. -

(EU) 2018/336 of 8 March 2018 Amending Regulation

13.3.2018 EN Official Journal of the European Union L 70/1 II (Non-legislative acts) REGULATIONS COMMISSION REGULATION (EU) 2018/336 of 8 March 2018 amending Regulation (EC) No 748/2009 on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) THE EUROPEAN COMMISSION, Having regard to the Treaty on the Functioning of the European Union, Having regard to Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a scheme for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/ EC (1), and in particular Article 18a(3)(b) thereof, Whereas: (1) Directive 2008/101/EC of the European Parliament and of the Council (2) amended Directive 2003/87/EC to include aviation activities in the scheme for greenhouse gas emission allowance trading within the Union. (2) Commission Regulation (EC) No 748/2009 (3) establishes a list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006. (3) That list aims to reduce the administrative burden on aircraft operators by providing information on which Member State will be regulating a particular aircraft operator. (4) The inclusion of an aircraft operator in the Union’s emissions trading scheme is dependent upon the performance of an aviation activity listed in Annex I to Directive 2003/87/EC and is not dependent on the inclusion in the list of aircraft operators established by the Commission on the basis of Article 18a(3) of that Directive. -

![Su-30MKM Reliable Partner!” in RMAF Service [P.4]](https://docslib.b-cdn.net/cover/4564/su-30mkm-reliable-partner-in-rmaf-service-p-4-2154564.webp)

Su-30MKM Reliable Partner!” in RMAF Service [P.4]

december 2009 • Special edition for LIMA 2009 CHERNYSHEV jsc Moscow Machine-Building Enterprise “reliable engine – Su-30MKM reliable partner!” in RMAF service [p.4] MiG-29K back on deck Manufacturing, after-sale service, aero engines overhaul [p.16] • RD-33 (MiG-29, MiG-29UB, MiG-29SMT fighters) • RD-33MK (MiG-29K, MiG-35/MiG-35D fighters) • TV7-117SM (IL-114 regional airplane) Overhaul, spare parts delievery • R27F2M-300 (MiG-23UB fighter) MMRCA • R29-300 (MiG-23M, MiG-23MS, MiG-23MF fighters) trials • R-35 (MiG-23ML, MiG-23MLD, MiG-23P fighters) [p.10] TBO and TTL expansion of the overhaul engines Tikhomirov’s AESA [p.30] MC-21 programme 7, Vishnevaya Street, Moscow, 125362, Russia [p.24] Phone: +7 (495) 491-58-74, Fax: +7 (495) 490-56-00 e-mail: [email protected], http://www.avia500.ru/ aero engines Recent aerospace news from Russia & CIS [p.2,14, 20, 26, 32] OBORONPROM Corporation, a Russian Technologies State Corporation company, is a diversified industrial-investment group in the engineering and high technologies sectors. The Corporation integrates more than 25 leading Russian companies in helicopters and engines manufacturing. The enterprises of the Corporation produced goods and provided services SU 30MK worth over $4 billion in 2008 ONLY THE BEST St.Petersburg Rybinsk Moscow Rostov-Don Kazan Perm Ufa Samara Ekaterinburg Kumertau Novosibirsk Ula-Ude Arseniev “Russian Helicopters” Company, a whole subsidiary of OBORONPROM Corporation, is the leading Russian designer and manufacturer of rotary-wing aircraft equipment advertising -

List of Attendees

MRO Russia & CIS 11th international conference & exhibition February 25–26, 2016, Moscow, World Trade Center List of Attendees Company Name Position 3TOP Aviation Services Matthew Marshall Regional Manager Business Development and Sales 3TOP Aviation Services Vladislav Slyusar Executive A J Walter Aviation Natalja Dimitrova Senior Sales Executive A J Walter Aviation Tolkyn Rymkulova VP Sales & Marketing for CIS A J Walter Aviation Roger Wolstenholme Regional Director A J Walter Aviation Tommy Guttman Executive VP Regional A J Walter Aviation Evgeny Shuravin AJW Moscow Manager A J Walter Aviation Junaid Baig Engine Material Sales Manager, Engines Sales & Marketing Manager, Russia & A J Walter Aviation Natasha Meerman CIS AAR Aircraft Component Sales Manager, Aircraft Component Services Amsterdam Ed Muller Services - AMS AAR Aviation Supply Chain Elena Gontsarova Sales Support AAR Aviation Supply Chain Ana Marian Regional Sales Manager AAR Aviation Supply Chain Pascal Parant Vice President Corporate Marketing ABS Jets Pavel Hrdlicka Sales&Business Development Manager Manager Technical Marketing and Adria Airways Pavel Prhavc Material Support Adria Airways Tehnika Maksimiljan Pele CEO Adria Airways Tehnika Mirjana Tratnjek Ceh Deputy CEO AEM Limited Sandy Basu Business Development Manager AEM Limited Andrew Wheeler Commercial Director AerCap Andrej Belotelov Vice President Technical AerCap Joe Millar Vice President, Technical AerFin Ltd Nicholas Filce Director AERO BRAVO INTERNATIONAL B.V. Dennis Bravo CEO AERO INSTRUMENT AND AVIONICS Carl -

MRO Russia and CIS 14Th International Conference & Exhibition March 5-6, 2019, Moscow, World Trade Center

MRO Russia and CIS 14th international conference & exhibition March 5-6, 2019, Moscow, World Trade Center List of participants Company Name Position 1st Choice Aerospace Gokhan Sen Regional Sales Manager 218 ARZ Maksim Ishchenko Deputy Managing Director for Sales and Service 218 ARZ Vlad Krendelev Project Manager AAR Corporation Andre op`t Hof Director of Commercial Operations MRO Services AAR Corporation Anna Marian Regional Director, Eastern Europe, Russia & CIS AAR Corporation Paul Richardson Vice President of Sales EMEA ACS Logistics Company Pavel Fedorov Logistics Manager ACS Logistics Company Yurii Turovets Director AEM Ametek MRO Linares Ricardo tbc AEM Ametek MRO Sandy Basu Technical Sales Manager AerCap Niels van Antwerpen Vice President Leasing Aereos - Atlas Aerospace Alexey Dmitriev Sales Engineer Aereos - Atlas Aerospace David Baker Partner Aereos - Atlas Aerospace Haim Gettler VP of Sales AerFin Loreta Durell Senior Account Manager AerFin Scott Kelsey Regional Sales Director Aero Future Alexey Fisenko CEO Aero Norway AS Glenford Marston General Manager Aero Norway AS Sena Iyipilavci Sales Manager Aero Shop Elena Belova Bose Aviation Product Manager Head of Spare Parts Supply Quality Assurance Aeroflot Alexander Avramenko Division Aeroflot Amirdin Shamiev Aircraft Mechanic Chief of the MIS Department (MRO IT) Aeroflot Andrey Denisov Department of Information Systems Chief Specialist of the Corporate Insurance Aeroflot Andrey Sokolov Division, Corporate Finance Department Head of Projects, Continuing Airworthiness Aeroflot -

Ancra-Signs-Contract-With-Irkut Copy

For Immediate Release Ancra Signs Contract with Irkut for MC-21 Lower Deck Cargo Loading Systems MOSCOW, RU — Ancra International, LLC has signed a contract with Irkut Corporation to develop and deliver the lower deck cargo loading systems for the new MC-21-200 and MC-21-300 mainline passenger aircraft. Each aircraft has the option of a manual or powered-loading system – using 2-inch Power Drive Units – with all four systems being developed simultaneously. Integral to the design is an offering to the operator for future upgrade from manual to powered capability. The powered systems leverage technology from Ancra’s 747-400 and A330 converted freighter main deck powered cargo loading systems and are designed to load and unload IATA 40/1 and 50/0 containers with reduced manpower. Critical Design Review is scheduled for December 2015 and the first system delivery is scheduled in August 2016. “We are excited to be part of the Irkut team as they bring their decades of experience designing and building aircraft to the 150-210 passenger aircraft market space. This program is a blessing for us as we take our own extensive main deck cargo loading system experience and expand it into the passenger lower deck domain.” says Ed Dugic, Director of Sales and Marketing for Ancra Aircraft Systems. About Ancra International Ancra International was founded in 1969 to serve the cargo handling industry with a complete line of cargo restraint and conveyance equipment for the air, truck, and rail markets. Since its inception, Ancra International’s Aircraft Systems Division has evolved to become an international leader in the design and manufacture of aircraft cargo handling and restraint systems. -

Download Article (PDF)

Advances in Economics, Business and Management Research, volume 107 External Challenges and Risks for Russia in the Context of the World Community’s Transition to Polycentrism: Economics, Finance and Business (ICEFB 2019) Contemporary Civil Aviation Market: Seeking an Economic Niche for the Russian Products Olga G. Lebedinskaya, Maria O. Grigoryeva, Vladimir I. Kuznetsov, Vitaliy G. Minashkin Plekhanov Russian University of Economics Moscow, Russia Abstract—The paper covers an important theme of the assessing the trends in the Russian aircraft industry and the development of one of the basic industries of the Russian analysis of the comparative advantages of the Russian newly economy – the civil aviation production. The current situation in developed projects in the sphere of aircraft production (Sukhoi the Russian industry leaves much space for the development, as Superjet-100, Irkut MC-21 and the common Russia-China at the current stage, the stagnation, caused by the USSR fall has project CR929) with the most popular aircrafts of the same not yet passed. The article’s main aim is to develop a clear vision characteristics. of the market conjuncture of the Russian industry and to reveal the main prospects of its future development taking into account the development of the new products by the Russian aviation II. METHODOLOGY corporations and Russia-China joint project. The article The article is based on the methodologic approach of contributes to the estimation of the Russian aviation industry research of the market conjuncture in the economic sphere on potential. the national market of the country-exporter, which contributes to the understanding of the key institutional characteristics of Keywords—Russia; aviation; industry; projects; Sukhoi the industry and the development of the general strategy. -

Country Or Region

Russia: Opportunities in the Aviation Market 2012 Page 1 of 5 Russia 2013: Opportunities in the Commercial Aircraft Market Vladislav Borodulin February 26, 2013 Brief Industry and Market Overview The Russian aviation industry is controlled by state-owned corporations United Aircraft Corporation (UAC) and Russian Technologies (Rostech RT). The Russian government “strategic” significance of the aviation industry is explained by the integrative role it plays in the Russian economy. Due to its close relationship with other associated industries - component manufacturing and machine-building - the Russian aviation industry has a significant influence on Russia’s development towards a more innovative economy. The Russian government currently pursues the development of aviation through its state strategy “Development of the Aviation Industry for 2013-2025”. The program was approved in December 2012 and the total amount of funding to be allocated is 1.7 trillion Rubles (appx. $56.6 billion). The Russian aviation industry consists of the following manufacturing segments: aircraft, helicopter, aircraft engine, avionics, and air components. The industry includes 248 Russian enterprises. In 2011, total revenue was more than 608 billion Rubles (appx. $20.2 billion). The industry provides employment for 400,000 personnel and contributes more than 1.1% GDP to the Russian economy, according to the Russian Ministry of Industry and Trade. As part of the aviation development strategy, the Russian government is interested in international cooperation on new aircraft projects and the transfer of Western technology. This is an opportunity for U.S. companies to get a foothold in the Russian economy and to engage in mutually beneficial aviation projects. -

November 2018

www .rusaviainsider.com RRuussssii aa&&CCIISS OObbsseerrvveerr November 2018 special focus on airshow china 2018 Russi a &CIS Observer from the publisher of november 2018 2 24 10 18 21 • AEROSPACE INDUSTRY Russia becomes largest warplane Russia/CIS Observer is produced by: Russia keeps its ambition in manufacturer ....................................12 Publisher commercial aircraft ..............................2 Su-30SM to get new engines ..............12 Evgeny Semenov VSMPO and Boeing expand titanium EditiorinChief • AIR TRANSPORT Maxim Pyadushkin partnership in Russia ............................6 China-friendly Russia and Russia- Art Director Aerosila showcases hi-tech ..................7 Andrey Khorkov friendly China? ..................................14 Sales & Marketing Director Aeropribor-Voskhod goes innovative ....8 Oleg Abdulov PD-14 engine for Russian MC-21 • BUSINESS AVIATION Commercial Director Sergey Belyaev receives certification ............................9 Russian business aviation enjoys All rights reserved. upward cycle ......................................19 No part of this publication may be • DEFENSE reproduced in whole or in part without the written permission of TMC demonstrates precision-guided • SPACE BUSINESS A.B.E. Media. weapons ............................................10 Uncertain future of International A.B.E. Media cannot be held responsible for any claim, error, omission or inaccuracy in advertising Su-57 to enter service in 2019 ............10 Space Station ....................................22 -

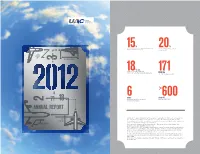

600 Years Aircraft Capacity Utilization for the Current Backlog of JSC “UAC” 2 71 18 Corporation’S Backlog ANNUAL REPORT

% % 15JSC «UAC»’s share of the global military aircraft 20civil aircraft share in JSC «UAC»’s market during the last 3 years revenue in 2012 SPECIAL AIRCRAFT 3 MILITARY AIRCRAFT % p.a. 18compound annual growth rate 171 of JSC “UAC”’s revenue during the last 5 years RUB bln JSC “UAC”’s revenue in 2012 6 >600 years aircraft capacity utilization for the current backlog of JSC “UAC” 2 71 18 Corporation’s backlog ANNUAL REPORT Joint Stock Company «United Aircraft Corporation» (hereinafter JSC «UAC», or the Corporation) CIVIL was established according to the presidential decree No. 140 of February 20, 2006 through AIRCRAFT the contribution of the state-owned shares of almost all Russian aircraft plants and design bureaus, as well as contributions from private shareholders. TRANSPORT AIRCRAFT The Corporation comprises all the known brands of Russian aircraft industry (Sukhoi, MiG, Ilyushin,Tupolev, Yak, Myasishchev and Beriev). The priorities of JSC «UAC» are design, development, construction, sales, operation maintenance, warranty, service, modernization, overhaul and utilization of civil and military aircraft equipment. Russian Federation through the Federal Agency for State Property Management owns 84.33% of JSC «UAC» stock and Vnesheconombank owns 9.11% of stock. The state will remain the major shareholder of JSC «UAC» for a considerable time in the future: according to the state privatization program, privatization of JSC «UAC» will be realized no later than in 2024. At the same time Russian Federation will retain its stake of 50% plus one share of the Corporation’s stock after 2024. DELIVERIES OF AIRCRAFT TO STRUCTURE OF JSC “UAC” INVESTMENTS AND RETURN ON DISCLAIMER CUSTOMERS, UNITS AIRCRAFT DELIVERIES BY INVESTMENTS This Annual Report of JSC “UAC” (hereinafter the “Annual SEGMENTS IN 2012 Report”) is not an offer or invitation to make an offer (advertisement) in relation to purchase of, or subscription to securities of JSC “UAC” (hereinafter – Corporation). -

The Way to Success 2004 Annual Report

«IRKUT» The way to success Corporation 2004 Annual Report «IRKUT» Corporation Annual Report 2004 2 «IRKUT» CORPORATION 2004 ANNUAL REPORT Section 1 01. Key Operational and Financial Highlights 4 02. Key Events in 2004 6 03. Message to the Shareholders 8 04. About IRKUT Corporation 12 Structure of IRKUT Board of Directors in 2004 12 Role of IRKUT Board of Directors in corporate management in 2004 16 Management Committee in 2004 17 Structure of IRKUT Corporation 18 05. Core Activities for 2004 20 Improved Production and Expanded Research and Development 21 Integration with the Global Aerospace Industry 23 Successful Contract Performance 24 Attracting Investment Resources 26 06. IRKUT Corporation in the Share Market 30 Share Issues, Chartered Capital 31 IRKUT Shares on the Capital Market 32 Dividend Policy and History 33 2004 ANNUAL REPORT «IRKUT» CORPORATION 3 Section 2 07. Financial Strategy: Message from the Vice-President for Corporate Finance 36 08. IRKUT Corporation Management Discussion and Analysis 2004 Part 1 Operating Results 39 Part 2 Critical Accounting 47 Part 3 Liquidity and Capital Resources 49 Part 4 Other Information 58 09. Consolidated Financial Report with Conclusions of Independent Auditors 60 10. General Information 92 Appendix: IRKUT Corporation Basic Products and Services Su-30MKI / MKM Multirole jet fighter Be-200 Multipurpose amphibious aircraft Yak-130 combat jet trainer Aircraft Components Production Unmanned Aerial Systems (Earth remote sensing systems based on unmanned and optionally piloted aerial vehicles)