Fine Violins As an Alternative Investment: Strings Attached? Received (In Revised Form): 13Th December, 2007

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

B&F Magazine Issue 31

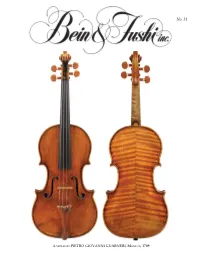

No. 31 A VIOLIN BY PIETRO GIOVANNI GUARNERI, MANTUA, 1709 superb instruments loaned to them by the Arrisons, gave spectacular performances and received standing ovations. Our profound thanks go to Karen and Clement Arrison for their dedication to preserving our classical music traditions and helping rising stars launch their careers over many years. Our feature is on page 11. Violinist William Hagen Wins Third Prize at the Queen Elisabeth International Dear Friends, Competition With a very productive summer coming to a close, I am Bravo to Bein & Fushi customer delighted to be able to tell you about a few of our recent and dear friend William Hagen for notable sales. The exquisite “Posselt, Philipp” Giuseppe being awarded third prize at the Guarneri del Gesù of 1732 is one of very few instruments Queen Elisabeth Competition in named after women: American virtuoso Ruth Posselt (1911- Belgium. He is the highest ranking 2007) and amateur violinist Renee Philipp of Rotterdam, American winner since 1980. who acquired the violin in 1918. And exceptional violins by Hagen was the second prize winner Camillo Camilli and Santo Serafin along with a marvelous of the Fritz Kreisler International viola bow by Dominique Peccatte are now in the very gifted Music Competition in 2014. He has hands of discerning artists. I am so proud of our sales staff’s Photo: Richard Busath attended the Colburn School where amazing ability to help musicians find their ideal match in an he studied with Robert Lipsett and Juilliardilli d wherehh he was instrument or bow. a student of Itzhak Perlman and Catherine Cho. -

A Violin by Giuseppe Giovanni Battista Guarneri

141 A VIOLIN BY GIUSEPPE GIOVANNI BATTISTA GUARNERI Roger Hargrave, who has also researched and drawn the enclosed poster, discusses an outstanding example of the work of a member of the Guarneri family known as `Joseph Guarneri filius Andrea'. Andrea Guarneri was the first He may never have many details of instruments by of the Guarneri family of violin reached the heights of his Joseph filius at this period recall makers and an apprentice of contemporary, the Amati school, this type of Nicola Amati (he was actually varnish, in combination with registered as living in the house Antonio Stradivarius, but he the freer hand of Joseph, gives of Nicola Amati in 1641). Andrea's does rank as one of the the instruments a visual impact youngest son, whose work is il - greatest makers of all time. never achieved by an Amati or , lustrated here, was called. We should not forget he with the exception of Stradi - Giuseppe. Because several of the sired and trained the great vari, by any other classical Guarneri family bear the same del Gesu' maker before this time. christian names, individuals have traditionally been identified by a It should be said, however, suffix attached to their names. that the varnish of Joseph filius Thus, Giuseppe's brother is known as `Peter Guarneri varies considerably. It is not always of such out - of Mantua' to distinguish him from Giuseppe's son, standing quality the same can be said of Joseph's pro - who is known as `Peter Guarneri of Venice'. duction in general. If I were asked to describe the instruments of a few of the great Cremonese makers Giuseppe himself is called 'Giuseppe Guarneri filius in a single word, I would say that Amatis (all of them) Andrea' or, more simply, `Joseph filius' to distinguish are `refined', Stradivaris are `stately', del Gesus are him from his other son, the illustrious 'Giuseppe `rebellious' and the instruments of Joseph filius An - Guarneri del Gesu'. -

Die Sammlung Historischer Streichinstrumente Der Oesterreichischen Nationalbank

OESTERREICHISCHE NATIONALBANK EUROSYSTEM Die Sammlung historischer Streichinstrumente der Oesterreichischen Nationalbank The collection of Historical String Instruments of the Oesterreichische Nationalbank Inhaltsverzeichnis Contents Impressum Medieninhaberin: Oesterreichische Nationalbank, Otto-Wagner-Platz 3, 1090 Wien, T: (+43 1) 404 20-6605, F: (+43 1) 404 20-6697, www.oenb.at Redaktion: Mag. Brigitte Alizadeh-Gruber, Muna Kadum, Martina Leitner, Mag. Irene Mühldorf Grafik, Layout und Satz: Melanie Schuhmacher Fotos: © Graphisches Atelier Neumann, Wien Druck: Oesterreichische Nationalbank, Abteilung für Öffentlichkeitsarbeit und Publikationen, Gruppe Multimedia-, Internet- und Print-Service. © Oesterreichische Nationalbank, 2013. Streichinstrumente/ String Instruments 9 Amati Andrea 10 Violoncello, Cremona, spätes 16. Jh. 10 Bergonzi Carlo 12 Violine, Cremona 1723 12 Violine, Cremona nach 1724 14 Bergonzi Michelangelo 16 Violine, Cremona um 1740 16 Violine, „ex Hamma-Segelman“, Cremona um 1750 18 Camilli Camillus 20 Violine, Mantua 1736 20 Ceruti Giovanni Battista 22 Viola, Cremona um 1810 22 Gagliano Alessandro 24 Violoncello, Neapel ca. 1710 24 Grancino Giovanni 26 Violoncello, „ex Piatti“ – „ex Dunlop“, Mailand 1706 26 Guadagnini Giovanni Battista 28 Violoncello, „ex von Zweygberg“, Piacenza 174. 28 Violine, Mailand 1749 30 Violine, „ex Meinel“, Turin um 1770–1775 32 Violine, Turin 1772 34 Violine, „Mantegazza“, Turin 1774 36 Violine, Turin 177. 38 Viola, Turin 1784 40 Guarneri Andrea 42 Violine, Cremona, Mitte 17. Jh. 42 Guarneri del Gesù Giuseppe 44 Violine, „ex Sorkin“, Cremona 1731 44 Violine, „ex Guilet“, Cremona nach 1732 46 Violine, „ex Carrodus“, Cremona 1741 48 Lorenzini Gaspare 50 Violine, Piacenza um 1760 50 Maggini Giovanni Paolo 52 Viola, Brescia, frühes 17. Jh. 52 Montagnana Domenico 54 Violine, Venedig 1727 54 Seraphin Sanctus 56 Violine, Venedig 1733 56 Violine, „ex Hamma“, Venedig nach 1748 58 Silvestre Pierre 60 Violine, „ex Moser“, Lyon ca. -

Reconstructing Lost Instruments Praetorius’S Syntagma Musicum and the Violin Family C

Prejeto / received: 3. 5. 2019. Odobreno / accepted: 12. 9. 2019. doi: 10.3986/dmd15.1-2.07 RECONSTRUCTING LOST INSTRUMENTS Praetorius’S Syntagma musicum and the Violin Family C. 1619 Matthew Zeller Duke University Izvleček: Knjigi De organographia in Theatrum Abstract: Michael Praetorius’s De organographia instrumentorum Michaela Praetoriusa vsebujeta and Theatrum instrumentorum provide valuable dragocene namige, ki pomagajo pri poznavanju clues that contribute to a new understanding glasbil iz družine violin okoli leta 1619; številna of the violin family c. 1619, many surviving ex- preživela glasbila so manjša, kot so bili izvirniki amples of which are reduced in size from their v 16. in 17. stoletju. Podatki o preživelih glas- sixteenth- and seventeenth-century dimensions. bilih – predvsem izdelki družine Amati – skupaj The record of surviving instruments – especially z metrologijo, sekundarno dokumentacijo in those of the Amati family – alongside metrologic, ikonografskim gradivom kažejo na to, da je documentary and iconographic evidence shows Michael Praetorius opisal veliko glasbilo, po that Michael Praetorius describes a large in- velikosti izjemno podobno violončelu (basso strument conforming remarkably well to the da braccio),kar je odličen primer predstavitve original dimensions of the basso da braccio glasbila iz družine violin in točne uglasitve, kot (violoncello), as well as furnishing an excellent so jih poznali v času izida Praetoriusovega dela. scale representation of the violin family as it was at the time of these works’ -

Violin Detective

COMMENT BOOKS & ARTS instruments have gone up in value after I found that their soundboards matched trees known to have been used by Stradivari; one subsequently sold at auction for more than four times its estimate. Many convincing for- KAMILA RATCLIFF geries were made in the nineteenth and early twentieth centuries, but the science did not exist then. Forgers now are aware of dendro- chronology, and it could be a problem if they use wood from old chalets to build sophisti- cated copies of historical instruments. How about unintentional deceit? I never like to ‘kill’ a violin — reveal it as not what it seems. But if the wood does not match the claims, I investigate. I was recently sent photos of a violin supposedly made by an Italian craftsman who died in 1735. The wood dated to the 1760s, so I knew he could not have made it. But I did see strong cor- relations to instruments made by his sons and nephews who worked in the 1770s. So Peter Ratcliff restores and investigates violins from his workshop in Hove, UK. I deduced that the violin might have been damaged and an entirely new soundboard made after the craftsman’s death. The violin Q&A Peter Ratcliff was pulled from auction, but not before it had received bids of more than US$100,000. Will dendrochronology change the market? Violin detective I think it already has, and has called into Peter Ratcliff uses dendrochronology — tree-ring dating — to pin down the age and suggest the question some incorrect historical assump- provenance of stringed instruments. -

The Working Methods of Guarneri Del Gesů and Their Influence Upon His

45 The Working Methods of Guarneri del Gesù and their Influence upon his Stylistic Development Text and Illustrations by Roger Graham Hargrave Please take time to read this warning! Although the greatest care has been taken while compiling this site it almost certainly contains many mistakes. As such its contents should be treated with extreme caution. Neither I nor my fellow contributors can accept responsibility for any losses resulting from information or opin - ions, new or old, which are reproduced here. Some of the ideas and information have already been superseded by subsequent research and de - velopment. (I have attempted to included a bibliography for further information on such pieces) In spite of this I believe that these articles are still of considerable use. For copyright or other practical reasons it has not been possible to reproduce all the illustrations. I have included the text for the series of posters that I created for the Strad magazine. While these posters are all still available, with one exception, they have been reproduced without the original accompanying text. The Labels mentions an early form of Del Gesù label, 98 later re - jected by the Hills as spurious. 99 The strongest evi - Before closing the body of the instrument, Del dence for its existence is found in the earlier Gesù fixed his label on the inside of the back, beneath notebooks of Count Cozio Di Salabue, who mentions the bass soundhole and roughly parallel to the centre four violins by the younger Giuseppe, all labelled and line. The labels which remain in their original posi - dated, from the period 1727 to 1730. -

The Strad Magazine

FRESH THINKING WOOD DENSITOMETRY MATERIAL Were the old Cremonese luthiers really using better woods than those available to other makers FACTS in Europe? TERRY BORMAN and BEREND STOEL present a study of density that seems to suggest otherwise Violins await testing on a CT scanner gantry S ALL LUTHIERS ARE WELL AWARE, of Stradivari. To test this conjecture, we set out to compare the business of making an instrument of the the wood employed by the classical Cremonese makers with violin family is fraught with pitfalls. There that used by other makers, during the same time period but are countless ways to ruin the sound of the from various regions across Europe. This would eliminate one fi nished product, starting with possibly the variable – the ageing of the wood – and allow the tracking of Amost fundamental decision of all: what wood to use. In the past geographical and topographical variation. In particular, we 35 years we have seen our knowledge of the available options wanted to investigate the densities of the woods involved, which expand greatly – and as we learn more about the different wood we felt could be the key to unlocking these secrets. choices, it is increasingly hard not to agonise over the decision. What are the characteristics we need as makers? Should we just WHY DENSITY? look for a specifi c grain line spacing, or a good split? Those were The three key properties of wood, from an instrument maker’s the characteristics that makers were once taught to watch out perspective, are density, stiffness (‘Young’s modulus’) and for, and yet results are diffi cult to repeat from instrument to damping (in its simplest terms, a measure of how long an object instrument when using the same pattern – suggesting these are will vibrate after being set in motion). -

Amati's Dream

Teacher’s Guide Amati’s Dream for Narrator, Violin & String Orchestra Amati’s Dream takes place in Cremona, Italy in the year 1666. The apprentice Raphael is learning to make violins in the shop of Nicolò Amati. Raphael enjoys his work, but he secretly yearns to be a violinist. His family cannot afford an instrument or music lessons, so Raphael tries his best to be content with working in the violin shop. Will Raphael fulfill his dream? The story is multi-layered and thought provoking. The children are introduced to the fascinating and magical world of the violin through narration and music. The information in the story is woven into the narrative and very accessible. The music is melodic and easy to comprehend. www.atlantic-crossing.com !1 Nicolo Amati Nicolò Amati was born in 1596 and died in 1684. He was an Italian violin maker; they are also known as luthiers. Amati built instruments over 300 years ago by candlelight, and without electric tools. Today, his instruments are very rare and extremely valuable. Nicolò Amati lived in the time known as the Renaissance; the word means rebirth. It is the time between the fourteenth and seventeenth centuries. The Renaissance was a time for the rebirth of science, education, music, art, and literature. The changes provided a better life for the people. Apprentice Raphael was an apprentice in the shop of Nicolò Amati. An apprentice trains for a craft or profession while working for an employer, as opposed to someone who learns by attending school. Often, the apprentice worked for his employer in exchange for lodging, food and training. -

Musical Instruments, 30 October 2013, Knightsbridge, London

Wednesday 30 October 2013 at 11am 30 October 2013 at Wednesday London Knightsbridge, Instruments Musical Musical 20770 Musical Instruments, 30 October 2013, Knightsbridge, London Musical Instruments Wednesday 30 October 2013 at 11am Knightsbridge, London Bonhams Enquiries Customer Services Please see back of catalogue Montpelier Street Director of Department Monday to Friday for Notice to Bidders Knightsbridge Philip Scott 8.30am to 6pm London SW7 1HH +44 (0) 20 7393 3855 +44 (0) 20 7447 7447 New bidders must also provide proof www.bonhams.com [email protected] of identity when submitting bids. Illustrations Failure to do this may result in your Viewing Specialist Front cover: Lot 230 bids not being processed. Sunday 27 October Thomas Palmer Back cover: Lot 3 +44 (0) 20 7393 3849 11am to 3pm [email protected] Monday 28 October 9am to 4.30pm Department Fax Tuesday 29 October +44 (0) 20 7393 3820 9am to 4.30pm Live online bidding is available for this sale Customer Services Bids Please email [email protected] Monday to Friday 8.30am to 6pm with “Live bidding” in the +44 (0) 20 7447 7448 +44 (0) 20 7447 7447 +44 (0) 20 7447 7401 fax subject line 48 hours before To bid via the internet the auction to register for Please register and obtain your this service. please visit www.bonhams.com customer number/ condition report for this auction at Please provide details of the lots [email protected] on which you wish to place bids at least 24 hours prior to the sale. New bidders must also provide proof of identity when submitting bids. -

Searching for Giuseppe Guarneri Del Gesù: a Paper-Chase and a Proposition

Searching for Giuseppe Guarneri del Gesù: a paper-chase and a proposition Nicholas Sackman © 2021 During the past 200 years various investigators have laboured to unravel the strands of confusion which have surrounded the identity and life-story of the violin maker known as Bartolomeo Giuseppe Guarneri del Gesù. Early-nineteenth-century commentators – Count Cozio di Salabue, for example – struggled to make sense of the situation through the physical evidence of the instruments they owned, the instruments’ internal labels, and the ‘understanding’ of contemporary restorers, dealers, and players; regrettably, misinformation was often passed from one writer to another, sometimes acquiring elaborations on the way. When research began into Cremonese archives the identity of individuals (together with their dates of birth and death) were sometimes announced as having been securely determined only for subsequent investigations to show that this certainty was illusory, the situation being further complicated by the Italian habit of christening a new- born son with multiple given names (frequently repeating those already given to close relatives) and then one or more of the given names apparently being unused during that new-born’s lifetime. During the early twentieth century misunderstandings were still frequent, and even today uncertainties still remain, with aspects of del Gesù’s chronology rendered opaque through contradictory or no documentation. The following account examines the documentary and physical evidence. ***** NB: During the first decades of the nineteenth century there existed violins with internal labels showing dates from the 1720s and the inscription Joseph Guarnerius Andrea Nepos. The Latin Dictionary compiled by Charlton T Lewis and Charles Short provides copious citations drawn from Classical Latin (as written and spoken during the period when the Roman Empire was at its peak, i.e. -

Tarisio June 2016 Highlights Catalogue Online Version

Violins June 2016 London 186 A FINE ITALIAN VIOLIN BY ALESSANDRO GAGLIANO, NAPLES, c.1700 Highlights Catalogue Unlabelled. Enlarged at the c-bouts. Catalogue online : 8 June LOB: 35.3 cm Bidding opens: 14 June Certificate: W. E. Hill & Sons, London, Oct 21, 1896 Bidding closes : 27 June Estimates: £150,000–180,000 185 A FINE ITALIAN VIOLIN BY GENNARO GAGLIANO, NAPLES, 1760 ‡ Labelled, "Januarius Gagliano filius, Alexandri fecit Neap. 1760." LOB: 35.2 cm Certificate: John & Arthur Beare, London, Aug 25, 2011 Estimates: £100,000–150,000 184 A GOOD ITALIAN VIOLIN FROM THE AMATI WORKSHOP, CREMONA, c. 1685, PROBABLY BY HIERONYMOUS II Labelled, "Hyeronimus Amati Cre... Nicolai Filius, Fecit 1692." LOB: 35.1 cm Dendrochronology dates the latest ring of both sides as 1682 and finds a tree match with the 1697 'Molitor' Stradivari. Written report by Peter Ratcliff available for purchase upon request Estimates: £50,000–80,000 183 A GOOD ITALIAN VIOLIN BY FRANCESCO MAURIZI, APPIGNANO, c. 1850 ‡ Unlabelled. Inscribed to inside back, "3958." LOB: 35.5 cm Certificate: Beare Violins Ltd, London, May 31, 2016 Estimates: £40,000–60,000 182 A GOOD FRENCH VIOLIN, ASCRIBED TO AND PROBABLY BY NICOLAS LUPOT, PARIS, c. 1800 Labelled, "Nicolas Lupot luthier rue de, Grammont a Paris l'an 1795." Inscribed to the inside bass c-bout in red ink, "6121." The head slightly recut at the final turn of the volute but probably original to the instrument. LOB: 35.9 cm Dendrochronology dates the latest ring of the bass and treble side as 1673 and 1671 respectively. -

1002775354-Alcorn.Pdf

3119 A STUDY OF STYLE AND INFLUENCE IN THE EARLY SCHOOLS OF VIOLIN MAKING CIRCA 1540 TO CIRCA 1800 THESIS Presented to the Graduate Council of the North Texas State University in Partial Fulfillment of the Requirements For the Degree of MASTER OF MUSIC By Allison A. Alcorn, B.Mus. Denton, Texas December, 1987 Alcorn, Allison A., A Study of Style and Influence in the Ear School of Violin Making circa 1540 to circa 1800. Master of Music (Musicology), December 1987, 172 pp., 2 tables, 31 figures, bibliography, 52 titles. Chapter I of this thesis details contemporary historical views on the origins of the violin and its terminology. Chapters II through VI study the methodologies of makers from Italy, the Germanic Countries, the Low Countries, France, and England, and highlights the aspects of these methodologies that show influence from one maker to another. Chapter VII deals with matters of imitation, copying, violin forgery and the differences between these categories. Chapter VIII presents a discussion of the manner in which various violin experts identify the maker of a violin. It briefly discusses a new movement that questions the current methods of authenti- cation, proposing that the dual role of "expert/dealer" does not lend itself to sufficient objectivity. The conclusion suggests that dealers, experts, curators, and musicologists alike must return to placing the first emphasis on the tra- dition of the craft rather than on the individual maker. o Copyright by Allison A. Alcorn TABLE OF CONTENTS Page LIST OF FIGURES.... ............. ........viii LIST OF TABLES. ................ ... x Chapter I. INTRODUCTION . .............. *.. 1 Problems in Descriptive Terminology 3 The Origin of the Violin.......