1 Fiddling with Value: Violins As an Investment?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

B&F Magazine Issue 31

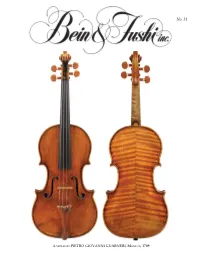

No. 31 A VIOLIN BY PIETRO GIOVANNI GUARNERI, MANTUA, 1709 superb instruments loaned to them by the Arrisons, gave spectacular performances and received standing ovations. Our profound thanks go to Karen and Clement Arrison for their dedication to preserving our classical music traditions and helping rising stars launch their careers over many years. Our feature is on page 11. Violinist William Hagen Wins Third Prize at the Queen Elisabeth International Dear Friends, Competition With a very productive summer coming to a close, I am Bravo to Bein & Fushi customer delighted to be able to tell you about a few of our recent and dear friend William Hagen for notable sales. The exquisite “Posselt, Philipp” Giuseppe being awarded third prize at the Guarneri del Gesù of 1732 is one of very few instruments Queen Elisabeth Competition in named after women: American virtuoso Ruth Posselt (1911- Belgium. He is the highest ranking 2007) and amateur violinist Renee Philipp of Rotterdam, American winner since 1980. who acquired the violin in 1918. And exceptional violins by Hagen was the second prize winner Camillo Camilli and Santo Serafin along with a marvelous of the Fritz Kreisler International viola bow by Dominique Peccatte are now in the very gifted Music Competition in 2014. He has hands of discerning artists. I am so proud of our sales staff’s Photo: Richard Busath attended the Colburn School where amazing ability to help musicians find their ideal match in an he studied with Robert Lipsett and Juilliardilli d wherehh he was instrument or bow. a student of Itzhak Perlman and Catherine Cho. -

A Violin by Giuseppe Giovanni Battista Guarneri

141 A VIOLIN BY GIUSEPPE GIOVANNI BATTISTA GUARNERI Roger Hargrave, who has also researched and drawn the enclosed poster, discusses an outstanding example of the work of a member of the Guarneri family known as `Joseph Guarneri filius Andrea'. Andrea Guarneri was the first He may never have many details of instruments by of the Guarneri family of violin reached the heights of his Joseph filius at this period recall makers and an apprentice of contemporary, the Amati school, this type of Nicola Amati (he was actually varnish, in combination with registered as living in the house Antonio Stradivarius, but he the freer hand of Joseph, gives of Nicola Amati in 1641). Andrea's does rank as one of the the instruments a visual impact youngest son, whose work is il - greatest makers of all time. never achieved by an Amati or , lustrated here, was called. We should not forget he with the exception of Stradi - Giuseppe. Because several of the sired and trained the great vari, by any other classical Guarneri family bear the same del Gesu' maker before this time. christian names, individuals have traditionally been identified by a It should be said, however, suffix attached to their names. that the varnish of Joseph filius Thus, Giuseppe's brother is known as `Peter Guarneri varies considerably. It is not always of such out - of Mantua' to distinguish him from Giuseppe's son, standing quality the same can be said of Joseph's pro - who is known as `Peter Guarneri of Venice'. duction in general. If I were asked to describe the instruments of a few of the great Cremonese makers Giuseppe himself is called 'Giuseppe Guarneri filius in a single word, I would say that Amatis (all of them) Andrea' or, more simply, `Joseph filius' to distinguish are `refined', Stradivaris are `stately', del Gesus are him from his other son, the illustrious 'Giuseppe `rebellious' and the instruments of Joseph filius An - Guarneri del Gesu'. -

The Working Methods of Guarneri Del Gesů and Their Influence Upon His

45 The Working Methods of Guarneri del Gesù and their Influence upon his Stylistic Development Text and Illustrations by Roger Graham Hargrave Please take time to read this warning! Although the greatest care has been taken while compiling this site it almost certainly contains many mistakes. As such its contents should be treated with extreme caution. Neither I nor my fellow contributors can accept responsibility for any losses resulting from information or opin - ions, new or old, which are reproduced here. Some of the ideas and information have already been superseded by subsequent research and de - velopment. (I have attempted to included a bibliography for further information on such pieces) In spite of this I believe that these articles are still of considerable use. For copyright or other practical reasons it has not been possible to reproduce all the illustrations. I have included the text for the series of posters that I created for the Strad magazine. While these posters are all still available, with one exception, they have been reproduced without the original accompanying text. The Labels mentions an early form of Del Gesù label, 98 later re - jected by the Hills as spurious. 99 The strongest evi - Before closing the body of the instrument, Del dence for its existence is found in the earlier Gesù fixed his label on the inside of the back, beneath notebooks of Count Cozio Di Salabue, who mentions the bass soundhole and roughly parallel to the centre four violins by the younger Giuseppe, all labelled and line. The labels which remain in their original posi - dated, from the period 1727 to 1730. -

The Strad Magazine

FRESH THINKING WOOD DENSITOMETRY MATERIAL Were the old Cremonese luthiers really using better woods than those available to other makers FACTS in Europe? TERRY BORMAN and BEREND STOEL present a study of density that seems to suggest otherwise Violins await testing on a CT scanner gantry S ALL LUTHIERS ARE WELL AWARE, of Stradivari. To test this conjecture, we set out to compare the business of making an instrument of the the wood employed by the classical Cremonese makers with violin family is fraught with pitfalls. There that used by other makers, during the same time period but are countless ways to ruin the sound of the from various regions across Europe. This would eliminate one fi nished product, starting with possibly the variable – the ageing of the wood – and allow the tracking of Amost fundamental decision of all: what wood to use. In the past geographical and topographical variation. In particular, we 35 years we have seen our knowledge of the available options wanted to investigate the densities of the woods involved, which expand greatly – and as we learn more about the different wood we felt could be the key to unlocking these secrets. choices, it is increasingly hard not to agonise over the decision. What are the characteristics we need as makers? Should we just WHY DENSITY? look for a specifi c grain line spacing, or a good split? Those were The three key properties of wood, from an instrument maker’s the characteristics that makers were once taught to watch out perspective, are density, stiffness (‘Young’s modulus’) and for, and yet results are diffi cult to repeat from instrument to damping (in its simplest terms, a measure of how long an object instrument when using the same pattern – suggesting these are will vibrate after being set in motion). -

Searching for Giuseppe Guarneri Del Gesù: a Paper-Chase and a Proposition

Searching for Giuseppe Guarneri del Gesù: a paper-chase and a proposition Nicholas Sackman © 2021 During the past 200 years various investigators have laboured to unravel the strands of confusion which have surrounded the identity and life-story of the violin maker known as Bartolomeo Giuseppe Guarneri del Gesù. Early-nineteenth-century commentators – Count Cozio di Salabue, for example – struggled to make sense of the situation through the physical evidence of the instruments they owned, the instruments’ internal labels, and the ‘understanding’ of contemporary restorers, dealers, and players; regrettably, misinformation was often passed from one writer to another, sometimes acquiring elaborations on the way. When research began into Cremonese archives the identity of individuals (together with their dates of birth and death) were sometimes announced as having been securely determined only for subsequent investigations to show that this certainty was illusory, the situation being further complicated by the Italian habit of christening a new- born son with multiple given names (frequently repeating those already given to close relatives) and then one or more of the given names apparently being unused during that new-born’s lifetime. During the early twentieth century misunderstandings were still frequent, and even today uncertainties still remain, with aspects of del Gesù’s chronology rendered opaque through contradictory or no documentation. The following account examines the documentary and physical evidence. ***** NB: During the first decades of the nineteenth century there existed violins with internal labels showing dates from the 1720s and the inscription Joseph Guarnerius Andrea Nepos. The Latin Dictionary compiled by Charlton T Lewis and Charles Short provides copious citations drawn from Classical Latin (as written and spoken during the period when the Roman Empire was at its peak, i.e. -

1002775354-Alcorn.Pdf

3119 A STUDY OF STYLE AND INFLUENCE IN THE EARLY SCHOOLS OF VIOLIN MAKING CIRCA 1540 TO CIRCA 1800 THESIS Presented to the Graduate Council of the North Texas State University in Partial Fulfillment of the Requirements For the Degree of MASTER OF MUSIC By Allison A. Alcorn, B.Mus. Denton, Texas December, 1987 Alcorn, Allison A., A Study of Style and Influence in the Ear School of Violin Making circa 1540 to circa 1800. Master of Music (Musicology), December 1987, 172 pp., 2 tables, 31 figures, bibliography, 52 titles. Chapter I of this thesis details contemporary historical views on the origins of the violin and its terminology. Chapters II through VI study the methodologies of makers from Italy, the Germanic Countries, the Low Countries, France, and England, and highlights the aspects of these methodologies that show influence from one maker to another. Chapter VII deals with matters of imitation, copying, violin forgery and the differences between these categories. Chapter VIII presents a discussion of the manner in which various violin experts identify the maker of a violin. It briefly discusses a new movement that questions the current methods of authenti- cation, proposing that the dual role of "expert/dealer" does not lend itself to sufficient objectivity. The conclusion suggests that dealers, experts, curators, and musicologists alike must return to placing the first emphasis on the tra- dition of the craft rather than on the individual maker. o Copyright by Allison A. Alcorn TABLE OF CONTENTS Page LIST OF FIGURES.... ............. ........viii LIST OF TABLES. ................ ... x Chapter I. INTRODUCTION . .............. *.. 1 Problems in Descriptive Terminology 3 The Origin of the Violin....... -

The Working Methods of Guarneri Del Gesů and Their Influence Upon His

9 The Working Methods of Guarneri del Gesù and their Influence upon his Stylistic Development Text and Illustrations by Roger Graham Hargrave Please take time to read this warning! Although the greatest care has been taken while compiling this site it almost certainly contains many mistakes. As such its contents should be treated with extreme caution. Neither I nor my fellow contributors can accept responsibility for any losses resulting from information or opin - ions, new or old, which are reproduced here. Some of the ideas and information have already been superseded by subsequent research and de - velopment. (I have attempted to included a bibliography for further information on such pieces) In spite of this I believe that these articles are still of considerable use. For copyright or other practical reasons it has not been possible to reproduce all the illustrations. I have included the text for the series of posters that I created for the Strad magazine. While these posters are all still available, with one exception, they have been reproduced without the original accompanying text. The Mould and the Rib Structure they were not, in their basic form, the result of any innovative mathematical composition. The elegance and purity of the violin form exer - cises such fascination that it has been the subject of The outline of a violin is only one element of its enquiry for more than two centuries; questions about complex design. It is still not known which was es - its design have generated almost as much interest as tablished first, the mould around which the violin the subject of Cremonese varnish and its composi - was constructed (which represents the chamber of tion. -

SAURET 24 Études-Caprices, Op

Émile SAURET 24 Études-Caprices, Op. 64 Vol. 2 (Nos. 8–13) Nazrin Rashidova, Violin Émile Sauret (1852–1920) control of the bow at the peak of the G and D strings, and ‘aria’ on the G string, showcasing the instrument’s 24 Études-Caprices, Op. 64 – Vol. 2 (Nos. 8–13) its distribution in the double-stopped material to follow, all capacity, tonal palette and the miraculous non-existence within the same piano dynamic range. The second section of ‘wolf notes’ on a string that is most prone to them. The The extraordinary 19th-century violin virtuoso, composer Paganini’s ‘Il Cannone’ of the same year. In Perlman’s [05:35], accompanied by a con spirito marking could leave second section embodies a sequence of sextuplets and pedagogue Émile Sauret carved himself an enviable hands, especially in his 1986 recording of Bach’s a player short-breathed in juggling a series of extreme accompanied by a delicatamente expressive marking in reputation during his lifetime and was acclaimed by the Chaconne, it is clear that it has the extraordinary ‘power registral leaps while retaining the suggested expressive the piano dynamic, encouraging a balanced control of the greatest musicians of the century, including Brahms, Liszt, and reserve’ that The Strad admired. marking: however, the ‘compactness’ of the Stradivari bow, thus securing subtle changes of the bow while Rubenstein, Tchaikovsky, Saint-Saëns and Sarasate, with The Stradivari embodies a different kind of quality and makes this a pleasurable challenge. tackling complex string crossings. whom he often played duets. refinement – though not itself lacking power and reserve – Étude-Caprice No. -

Fine Violins As an Alternative Investment: Strings Attached? Received (In Revised Form): 13Th December, 2007

Fine violins as an alternative investment: Strings attached? Received (in revised form): 13th December, 2007 R.A.J. Campbell completed her PhD on risk management in international fi nancial markets at Erasmus University, Rotterdam in 2001. She currently works at the University of Maastricht as an assistant professor of fi nance. Her work has been published in a number of leading journals, including the Journal of International Money and Finance , Journal of Banking and Finance , Financial Analysts Journal , Journal of Portfolio Management , Journal of Empirical Finance , Journal of Risk and Derivatives Weekly . She teaches for Euromoney Financial Training on art investment and works as an independent economic advisor for The Fine Art Fund in London, and for Fine Art Wealth Management, UK. She currently is a member of the supervisory board of ARTESTATE GmbH, based in Germany. Abstract The continual search to reap higher risk-adjusted returns has led to a number of highly alternative assets to be considered for fi nancial investment purposes. Recently, a number of funds have emerged to indirectly invest in the arts sector. The focus has been on fi ne art, wine and more recently into the possibility of investing into other collectible items and memorabilia. One such area is musical instruments. In this paper, we take a look at the violin sector in particular, which has shown steady annual growth in market value over the past half century; fuelled by a combination of a shortage in supply at the high end of the market and a continued increase in global demand. Using data collected from auction houses and private dealers, we analyse the risk-return characteristics of the violin sector, compare it to other fi nancial assets and assess the implications for portfolio diversifi cation and the ability of pension houses to benefi t from this sector. -

Nicolò Paganini: the Virtuosity, His Violin, the Legend

Presents: Nicolò Paganini: The Virtuosity, His Violin, The Legend Nicolò Paganini (1782-1840) was arguably the greatest violinist of all time, leaving his mark on history as a composer, accomplished guitarist and the best virtuoso violin soloist the world had ever known. Hailing from Genoa, Italy, he began the violin at 7 years of age, making his public debut at age 9, while receiving instruction from Giacomo Costa and later under Alessandro Rolla. His father was so strict that Nicolò wouldn’t be allowed to eat until he would have practiced enough time, a habit that would carry on into his adulthood as he was rumoured to have practised incredibly long hours each day. He suffered from Marfan syndrome, a connective tissue disorder that leaves one typically very tall and thin, flexible with increased dexterity in the fingers. It is said that he could bend his finger to 90 degrees with his hand, giving him quite an advantage for playing the violin very fast and stretching over the finger board like no one else could, thus turning a misfortune into one of the largest contributors to Paganini’s virtuosity. Amongst his musical compositions Paganini is surely mostly known for his 24 Caprices which are considered amongst the most difficult music ever composed for the violin. Composed in three different stages of his life, the first of which whilst serving a prison term that has fuelled the rumour mill and left much speculation over how long and what for. Each Caprice addresses different technical challenges requiring a high-level command of the instrument to perform. -

The Ex-Isenberg

The Ex-Isenberg An Important Italian Violin by Pietro Guarneri, Mantua c 1700 Fine & Rare Instruments Property of a Gentleman The Ex-Isenberg An Important Italian Violin by Pietro Guarneri, Mantua c 1700 The one piece back of medium flame, descending to the right, the ribs of similar flame, the scroll of plainer maple, the one piece table of fine to medium grain widening towards the flanks, the plentiful varnish of a lustrous golden- brown colour. Length of back: 353mm The violin is in a very fine state of preservation. Sold with the certificate of Jacques Francais, New York. A full dendrochronology report from Peter Ratcliff. The oldest ring dating from AD 1549 and the youngest ring dating from AD 1700. “Examining the whole of the results, it is immediately apparent that no data belonging to instruments made outside Italy feature in the list of correlations. The other striking aspect that a disproportionately large number of these cross-match with instruments made in the workshop of Antonio Stradivari. In fact, 55% of the instruments listed are from the Stradivarius workshop, almost 80% of which were made before 1705.” Pietro Guarneri (1655-1720) Pietro Guarneri was the eldest son of Andrea Guarneri and older brother of Giuseppe filius Andrea. Pietro started in the workshop of his father from around 1670. Pietro was also a talented violinist and viol player and left Cremona to further his musical career in Mantua, playing violin as a soloist for the Duke of Mantua, and as a viol player in the Gonzaga court orchestra. His playing career must have been busy and successful, as his superbly elegant instruments, are comparatively rare. -

Signature Violins

VIOLINS signature instruments INSTRUMENTS THAT PROVIDE NEW QUALITY AND NEW POTENTIAL 4 simple reasons why you should discover the new Bobak Violino violins Signature Instruments INSTRUMENTS THAT PROVIDE NEW QUALITY AND NEW POTENTIAL We would like to introduce a new line of our violins inspired by the work of greatest violin makers of the 18th century. * Giovanni Battista Guadagnini * Guarneri del Gesu * * Antonio Stradivari * Carlo Bergonzi * Each of the four models retains its original character. They directly refer to the old Italian instrument masters in their overall concept, form as well as in terms of style. We obviously cannot forget the sound, which is a very subjective experience but it needs to be dened at a given specied level. SIGNATURE VIOLIN ANTIQUE FINISH Each violin is fully hand-crafted by a luthier These are not exact copies but each model from our workshop under the watchful eye of strongly refers to the original. Our violins the master. The most important elements of correspond to the originals in construction, the construction as well as details and varnish form, measurements and style. These all are nished by Grzegorz Bobak who is makes them unique in character and allows to responsible for the overall look of the think of an old Italian instrument... instrument. Each instrument is set up by Wood used to build violins is properly Grzegorz personally what allows him to label seasoned and carefully chosen for each this project under personal brand. particular instrument. It is always top quality material. Why should you discover Bobak Violino violins? ORIGINAL LABEL & CERTIFICATE AFORDABLE PRICE Each of four models has its own, original label This project is mainly aimed to young and what determines the instrument and makes it promising musicians, students, people who look more friendly and less anonymous.