Pa Perspectives on Nordic Financial Services

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

External Borkers List

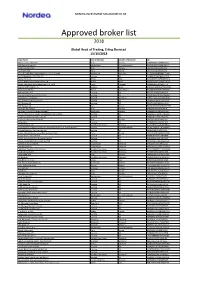

NORDEA INVESTMENT MANAGEMENT AB Approved broker list 2018 Global Head of Trading, Erling Skorstad 15/10/2018 Legal Name City of Domicile Country of Domicile LEI ABG Sundal Collier ASA Oslo Norway 2138005DRCU66B8BNY04 ABN Amro Group NV Amsterdam The Netherlands BFXS5XCH7N0Y05NIXW11 Arctic Securities AS Oslo Norway 5967007LIEEXZX4RVS72 Aurel BGC SAS Paris France 5RJTDGZG4559ESIYLD31 Australia and New Zealand Banking Group Limited Melbourne Australia JHE42UYNWWTJB8YTTU19 AUTONOMOUS RESEARCH LLP London UK 213800LBM6PT85IGM996 Banca IMI S.p.A Milan Italy QV4Q8OGJ7OA6PA8SCM14 Banco Bilbao Vizcaya Argentaria S.A Bilbao Spain K8MS7FD7N5Z2WQ51AZ71 Banco Português de Investimento, S.A. (BPI) Porto Portugal 213800NGLJLXOSRPK774 BANCO SANTANDER S.A Madrid Spain 5493006QMFDDMYWIAM13 Bank Vontobel AG Zurich Switzerland 549300L7V4MGECYRM576 Barclays Bank PLC London UK G5GSEF7VJP5I7OUK5573 Barclays Capital Securities Limited London UK K9WDOH4D2PYBSLSOB484 Bayerische Landesbank Munich Germany VDYMYTQGZZ6DU0912C88 BCS Prime Brokerage Limited London UK 213800UU8AHE2B6QUI26 BGC Brokers LP London UK ZWNFQ48RUL8VJZ2AIC12 BNP Paribas SA Paris France R0MUWSFPU8MPRO8K5P83 Carnegie AS Norway Oslo Norway 5967007LIEEXZX57BC18 Carnegie Investment Bank AB (publ) Stockholm Sweden 529900BR5NZNQZEVQ417 China International Capital Corporation (UK) Limited London UK 213800STG3UV87MDGA96 Citigroup Global Markets Limited London UK XKZZ2JZF41MRHTR1V493 Clarksons Platou Securities AS Oslo Norway 5967007LIEEXZXA40G44 CLSA (UK) London UK 213800VZMAGVIU2IJA72 Commerzbank AG Frankfurt -

Danmarks Nationalbank 2 Thedanmarks Response of Householdnationalbank Customers to Negative Deposit Rates Analyses

ANALYSIS DANMARKS NATIONALBANK 27 APRIL 2021 — NO. 9 The response of house- hold customers to negative deposit rates Negative deposit Reduction in Announcement rates more deposits following increases demand widespread announcements for investments Negative deposit rates There are indications Household customers for household custom that household cus appear to increase their ers are now being tomers reduce their de demand for investment applied by most banks posits when their bank fund shares and switch in Denmark. Further announces negative their deposits to pool more, the banks have interest rates. However, schemes when faced gradually reduced the household customers’ with prospects of nega thresholds for when total deposits have tive deposit rates. negative interest rates increased during the are imposed. period of negative deposit rates. Read more Read more Read more ANALYSIS — DANMARKS NATIONALBANK 2 THEDANMARKS RESPONSE OF HOUSEHOLDNATIONALBANK CUSTOMERS TO NEGATIVE DEPOSIT RATES ANALYSES Low for long Denmark was the first country to introduce negative ABOUT THIS ANALYSIS monetary policy rates in 2012. Since then, Switzer- land, Sweden, Japan and the euro area have followed Most banks in Denmark have now in suit. troduced negative deposit rates for household customers. Furthermore, Very low and in some cases negative interest rates the banks have gradually reduced the thresholds for when negative have characterised the past decade across the ad- interest rates are payable. vanced economies. There are several reasons why interest rates have fallen to the current low levels. Low There are indications that household interest rates reflect the fact that inflation has been customers reduce their deposits subdued in many countries, but structural changes when their bank announces negative in household and corporate savings and investment interest rates. -

Approved Broker List 2016

NORDEA INVESTMENT MANAGEMENT AB Approved broker list 2016 Head of Trading, Miles Kumaresan 07/04/2016 NORDEA INVESTMENT MANAGEMENT AB Legal Name City name Country name LEI ABG Sundal Collier ASA Oslo Norway 2138005DRCU66B8BNY04 ABNAMRO Bank N.V Amsterdam The Netherlands BFXS5XCH7N0Y05NIXW11 Ak Yatirim Menkul Degerler A.S Istanbul Turkey 789000ZSYXQD4Y7YRG72 Arctic Securities AS Oslo Norway 5967007LIEEXZX4RVS72 Aurel BGC SAS Paris France 5RJTDGZG4559ESIYLD31 Australia and New Zealand Banking Group Limited Melbourne Australia JHE42UYNWWTJB8YTTU19 AUTONOMOUS RESEARCH LLP London UK 213800LBM6PT85IGM996 Banca IMI S.p.A Milan Italy QV4Q8OGJ7OA6PA8SCM14 Banco Bilbao Vizcaya Argentaria S.A Bilbao Spain K8MS7FD7N5Z2WQ51AZ71 Banco Português de Investimento, S.A. (BPI) Porto Portugal 213800NGLJLXOSRPK774 BANCO SANTANDER S.A Madrid Spain 5493006QMFDDMYWIAM13 Bank Vontobel AG Zurich Switzerland 549300L7V4MGECYRM576 Barclays Bank PLC London UK G5GSEF7VJP5I7OUK5573 Barclays Capital Securities Limited London UK K9WDOH4D2PYBSLSOB484 Bayerische Landesbank Munich Germany VDYMYTQGZZ6DU0912C88 BMO Capital Markets Limited London UK L64HM9LHPDOS1B9HJC68 BNP Paribas SA Paris France R0MUWSFPU8MPRO8K5P83 Canaccord Genuity Limited London UK ZBU7VFV5NIMN4ILRFC23 Carnegie Holding AB Stockholm Sweden 529900BR5NZNQZEVQ417 China International Capital Corporation (UK) Limited London UK 213800STG3UV87MDGA96 Citigroup Global Markets Europe Limited London UK 5493004FUULDQTMX0W20 Citigroup Global Markets Limited London UK XKZZ2JZF41MRHTR1V493 Clarksons Platou Securities -

Governmental Assistance to the Financial Sector: an Overview of the Global Responses (V9)

Economic Stabilization Advisory Group | October 2, 2009 Governmental Assistance to the Financial Sector: an Overview of the Global Responses (v9) The measures that Governments have taken to protect the financial sector have settled down to a large extent. We have, however, decided to publish a further update on the measures following a renewed interest in developments and the recent G20 Summit. This memorandum summarizes the measures Governments across the world have taken to protect the financial sector and prevent a recession. The measures fall into the following categories: guarantees of bank liabilities; retail deposit guarantees; central bank assistance measures; bank recapitalization through equity investments by private investors and Governments; and open-market or negotiated acquisitions of illiquid or otherwise undesirable assets from weakened financial institutions. The purpose of this publication is to provide an overview of the principal measures that have been taken in the major financial jurisdictions to support the financial system. The first version of this note was published on November 12, 2008. Since then, Governments in some jurisdictions have adopted further measures or amended measures previously adopted. The current version of the note takes into account those measures and is based on information available to us on September 30, 2009. Table of Contents Page AUSTRALIA.......................................................................................................................................................................................................................... -

12Thjune 2014 Helsinki Eba Clearing Shareholders

REPORT OF THE BOARD EBA CLEARING SHAREHOLDERS MEETING 12TH JUNE 2014 HELSINKI Contents 1. Introduction 3 2. The Company’s activities in 2013 5 2.1 EURO1/STEP1 Services 5 2.2 STEP2 Services 8 2.3 Operations 15 2.4 Legal, Regulatory & Compliance 18 2.5 Risk Management 20 2.6 Other corporate developments 21 2.7 The MyBank initiative 23 2.8 Activities of Board Committees 23 2.9 Corporate matters 26 2.10. Financial situation 29 3. The Company’s activities in 2014 32 3.1 EURO1/STEP1 Services 32 3.2 STEP2 Services 33 3.3 PRETA S.A.S. 35 3.4 Other relevant matters of interest 36 Appendix 1: Changes in EURO1/STEP1 participation 37 Appendix 2: List of participants in EURO1/STEP1 40 Appendix 3: List of direct participants in STEP2 45 Appendix 4: Annual accounts for 2013 53 2 EBA CLEARING SHAREHOLDERS MEETING // 12th June 2014 // Report of the Board 1. Introduction 2013 was marked by the major changeover that the SEPA migration end-date for euro retail payments of 1st February 2014 represented for payment service providers in the Eurozone and their customers. SEPA migration-related activities were also the top priority for EBA CLEARING throughout 2013. The Company continued to strengthen and enhance the STEP2 platform and intensified its customer support activities to assist its users across Europe in ensuring a disruption-free changeover to the SEPA instruments for their customers. SEPA migration affirmed the position of the STEP2 platform among the leading retail payment systems in Europe. The timely delivery of its SEPA Services as well as the processing capacity, operational robustness and rich functionality of the system made STEP2 the platform of first choice of many European communities in preparation of and during this migration. -

Target2 List of Participants

Participants BIC Participant's company name Participation type AABAFI22XXX Bank of Aland Plc 1 AACSDE33XXX Sparkasse Aachen 1 AARBDE5WXXX Aareal Bank AG 1 ABANSI2XXXX NOVA KREDITNA BANKA MARIBOR D. D. 1 ABCADEFFXXX Arab Banking Corporation SA Zweigniederlassung Frankfurt 1 ABCOFRPPXXX ARAB BANKING CORPORATION 2 ABCOITMMXXX ABC INTERNATIONAL BANK PLC MILAN MILANO 2 ABGRDEFFXXX PIRAEUS BANK A.E., Athen Zweigniederlassung Frankfurt am Main 1 ABKBDEB1XXX ABK Allgemeine Beamten Bank AG 2 ABKBDEBBXXX ABK Allgemeine Beamten Bank AG 1 ABKLCY2NXXX ALPHA BANK CYPRUS LIMITED 1 ABNABE2AIDJ ABN AMRO II N.V. 2 ABNABE2AIPC ABN AMRO II N.V. 2 ABNANL2AXXX ABN AMRO BANK NV 1 ABNCNL2AISA ABN AMRO CLEARING BANK N.V. 1 ABNCNL2AXXX ABN AMRO CLEARING BANK N.V. 1 ABOCDEFFXXX Agricultural Bank of China Limited Frankfurt Branch 1 ACTVPTPLXXX BANCO ACTIVOBANK, S.A. 2 ADYBNL2AXXX ADYEN B.V. 1 AEBAGRAAXXX Aegean Baltic Bank S.A.. 1 AEGONL2U100 AEGON BANK 1 AEGONL2UXXX AEGON BANK NV 1 AFFAATWWXXX Oesterreichische Bundes- finanzierungsagentur 2 AFRIFRPPXXX BOA-FRANCE 1 AGBACZPPXXX MONETA Money Bank, a.s. 1 AGBLLT2XXXX LUMINOR BANK AS LITHUANIAN BRANCH 1 AGBMDEMMTGT Airbus Bank GmbH 1 AGBMDEMMXXX Airbus Bank GmbH 2 AGFBFRCCXXX ALLIANZ BANQUE S.A 2 AGFBFRPPXXX ALLIANZ BANQUE SA 1 AGFOFR21XXX AGENCE FRANCE LOCALE 1 AGRIFRP1ACF CA CONSUMER FINANCE 2 AGRIFRP1EFG CREDIT AGRICOLE LEASING ET FACTORING 2 AGRIFRPP802 CRCAM NORD EST 2 AGRIFRPP810 CRCAM CHAMPAGNE BOURGOGNE 2 AGRIFRPP812 CRCAM NORD MIDI PYRENEES 2 AGRIFRPP813 CRCAM ALPES PROVENCE 2 AGRIFRPP817 CRCAM CHARENTE MARITIME -

Banking Automation Bulletin | Media Pack 2021

Banking Automation BULLETIN Media Pack 2021 Reaching and staying in touch with your commercial targets is more important than ever Curated news, opinions and intelligence on Editorial overview banking and cash automation, self-service and digital banking, cards and payments since 1979 Banking Automation Bulletin is a subscription newsletter Independent and authoritative insights from focused on key issues in banking and cash automation, industry experts, including proprietary global self-service and digital banking, cards and payments. research by RBR The Bulletin is published monthly by RBR and draws 4,000 named subscribers of digital and printed extensively on the firm’s proprietary industry research. editions with total, monthly readership of 12,000 The Bulletin is valued by its readership for providing independent and insightful news, opinions and 88% of readership are senior decision makers information on issues of core interest. representing more than 1,000 banks across 106 countries worldwide Regular topics covered by the Bulletin include: Strong social media presence through focused LinkedIn discussion group with 8,500+ members • Artificial intelligence and machine learning and Twitter @RBRLondon • Biometric authentication 12 issues per year with bonus distribution at key • Blockchain and cryptocurrency industry events around the world • Branch and digital transformation Unique opportunity to reach high-quality • Cash usage and automation readership via impactful adverts and advertorials • Deposit automation and recycling • Digital banking and payments Who should advertise? • Financial inclusion and accessibility • Fintech innovation Banking Automation Bulletin is a unique and powerful • IP video and behavioural analytics advertising medium for organisations providing • Logical, cyber and physical bank security solutions to retail banks. -

List of Market Makers and Authorised Primary Dealers Who Are Using the Exemption Under the Regulation on Short Selling and Credit Default Swaps

Last update 11 August 2021 List of market makers and authorised primary dealers who are using the exemption under the Regulation on short selling and credit default swaps According to Article 17(13) of Regulation (EU) No 236/2012 of the European Parliament and of the Council of 14 March 2012 on short selling and certain aspects of credit default swaps (the SSR), ESMA shall publish and keep up to date on its website a list of market makers and authorised primary dealers who are using the exemption under the Short Selling Regulation (SSR). The data provided in this list have been compiled from notifications of Member States’ competent authorities to ESMA under Article 17(12) of the SSR. Among the EEA countries, the SSR is applicable in Norway as of 1 January 2017. It will be applicable in the other EEA countries (Iceland and Liechtenstein) upon implementation of the Regulation under the EEA agreement. Austria Italy Belgium Latvia Bulgaria Lithuania Croatia Luxembourg Cyprus Malta Czech Republic The Netherlands Denmark Norway Estonia Poland Finland Portugal France Romania Germany Slovakia Greece Slovenia Hungary Spain Ireland Sweden Last update 11 August 2021 Austria Market makers Name of the notifying Name of the informing CA: ID code* (e.g. BIC): person: FMA ERSTE GROUP BANK AG GIBAATWW FMA OBERBANK AG OBKLAT2L FMA RAIFFEISEN CENTROBANK AG CENBATWW Authorised primary dealers Name of the informing CA: Name of the notifying person: ID code* (e.g. BIC): FMA BARCLAYS BANK PLC BARCGB22 BAWAG P.S.K. BANK FÜR ARBEIT UND WIRTSCHAFT FMA BAWAATWW UND ÖSTERREICHISCHE POSTSPARKASSE AG FMA BNP PARIBAS S.A. -

BIC Rozrachunkowy

BIC Nazwa BIC reprezentanta BIC rozrachunkowy AABAFI22 BANK OF ALAND PLC AABAFI22XXX ABKLCY2N ALPHA BANK CYPRUS LTD ABKLCY2NXXX ABNANL2A ABN AMRO BANK NV ABNANL2AXXX ADYBNL2A ADYEN B.V. ADYBNL2AXXX AGRIFRPP CREDIT AGRICOLE SA AGRIFRPPXXX AIBKIE2D ALLIED IRISH BANKS PLC AIBKIE2DXXX ALBADKKK ARBEJDERNES LANDSBANK ALBADKKKXXX APSBMTMT APS Bank APSBMTMTXXX BACRIT22 CREDITO EMILIANO SPA BACRIT22XXX BAPPIT22 Banco BPM s.p.a. BAPPIT22XXX BARCBEBB Barclays Bank Ireland - Belgium Branch BARCBEBBXXX BARCDEFF BARCLAYS BANK IRELAND - FRANKFURT BRANCH BARCDEFFXXX BARCFRPC Barclays Bank Ireland Plc, France branch BARCFRPCXXX BARCGB22 BARCLAYS BANK PLC BARCGB22XXX BARCIE2D BARCLAYS BANK IRELAND PLC BARCIE2DXXX BARCLULL Barclays Bank Ireland - Luxembourg Branch BARCLULLXXX BARCNL22 Barclays Bank Ireland - Netherlands Branch BARCNL22XXX BARCPTPC Barclays Bank Ireland Plc, Portugal branch BARCPTPCXXX BBPIPTPL BANCO BPI SA BBPIPTPLXXX BBRUBEBB ING BANK NV BRUSSELS BBRUBEBBXXX BBRUBEBC ING BELGIUM NV/SA BBRUBEBCXXX BBVAESMM BANCO BILBAO VIZCAYA BBVAESMMXXX BCEELULL BANQUE ET CAISSE DEPARGNE DE BCEELULLXXX BCITITMM INTESA SANPAOLO SPA BCITITMMXXX BCOEESMM BANCO COOPERATIVO BCOEESMMXXX BCOMPTPL BANCO COMERCIAL PORTUGUES SA BCOMPTPLXXX BCYPCY2N BANK OF CYPRUS PUBLIC COMPANY LTD BCYPCY2NXXX BDFEFRPP BANQUE DE FRANCE BDFEFRPPXXX BESCPTPL NOVO BANCO, SA BESCPTPLXXX BGLLLULL BGL BNP PARIBAS BGLLLULLXXX BILLLULL BANQUE INTERNATIONALE A LUXEMBOURG BILLLULLXXX BITAITRR BANCA DITALIA BITAITRRXXX BKAUATWW UNICREDIT BANK AUSTRIA AG BKAUATWWXXX BKBKESMM BANKINTER SA BKBKESMMXXX BLUXLULL BANQUE DE LUXEMBOURG BLUXLULLXXX BMPBBEBB AION S.A. BMPBBEBBXXX BNGRGRAA BANK OF GREECE S.A. BNGRGRAAXXX BNIFMTMT BNF BANK PLC BNIFMTMTXXX BNPAFRPP BNP PARIBAS SA BNPAFRPPXXX BNPAIE2D BNP PARIBAS DUBLIN BRANCH BNPAIE2DXXX BOFADEFX BANK OF AMERICA FRANKFURT BOFADEFXXXX BOFIIE2D BANK OF IRELAND BOFIIE2DXXX BOTKFRPX MUFG BANK, LTD. PARIS BRANCH BOTKFRPXXXX BPCEFRPP BPCE BPCEFRPPXXX BPLCESMM Barclays Bank Ireland Plc, Spain branch BPLCESMMXXX BPOTBEBE BPOST BANK N.V. -

Practitioners Creating Pan-European Payment Infrastructures WELCOME

ANNUAL REPORT 2020 Practitioners Creating Pan-European Payment Infrastructures WELCOME 2 The Company’s Mission 3 Chairperson’s Statement 7 CEO’s Statement and Strategic Aims THE COMPANY’S ACTIVITIES IN 2020 AND OUTLOOK FOR 2021 12 Services 41 Risk Management 53 Governance 69 Financials 13 Introduction 42 Corporate Risk 54 Corporate Governance 70 Statutory Accounts 15 EURO1 Service Management 68 Environmental, Societal 79 Subsidiary Report 18 STEP1 Service 45 Internal Audit and Governance Statement 20 STEP2 SEPA Services 46 Legal and Regulatory 24 RT1 Service 50 Oversight of EBA CLEARING 29 STEP2 Card Clearing Service 32 SEDA 34 Operations 37 R2P Project 40 IXB Initiative APPENDICES 81 List of EBA CLEARING 82 List of EURO1/STEP1 88 List of STEP2 CC 90 Annual Accounts for 2020 Shareholders Participants Participants 84 List of Participants 89 List of RT1 Participants in STEP2-T WELCOME EBA CLEARING ANNUAL REPORT 2020 / PAGE 1 OF 92 CONTENT OVERVIEW WELCOME SERVICES RISK MANAGEMENT GOVERNANCE FINANCIALS APPENDICES MISSION AND STRATEGIC AIMS The Company’s OUR MISSION OUR OBJECTIVES EBA CLEARING’s mission is to deliver market infra- EBA CLEARING aims to allow cost optimisation for its structure solutions for the pan-European payments in- users, and is not seeking profit or shareholder value Mission and dustry, to support its users’ needs in line with user re- maximisation. In pursuing its mission, EBA CLEARING quirements. is guided by the objective to offer its users solutions Strategic Aims that are fit for purpose and efficient, with a special fo- The strategic aims of the Company are to ensure a cus on safety and ensuring compliance with regulato- pan-European and country-neutral approach for the ry and oversight requirements. -

Spar Nord Changes It-Platform from Sdc to Bec

Dette billede kan ikke vises i øjeblikk et. SPAR NORD CHANGES IT-PLATFORM FROM SDC TO BEC Investor and analyst briefing CHANGING FROM SDC TO BEC IS A GOOD IDEA BECAUSE… 1 The solution is feasible – a full-scale merger is not at the present time 2 The transition to BEC will result in substantial savings and synergies 3 We will team up with stronger partners – and be well equipped for the future 4 BEC’s focuses on standard solutions – great match for AN UNCOMPLICATED BANK Page 2 THE NEW COMPETITIVE LANDSCAPE AMONG IT-PROVIDERS BEC SDC Bankdata Danske Bank Nordea Page 3 A HIGHLY ATTRACTIVE BUSINESS CASE Spar Nord’s investment – Write-down of shareholding in SDC: DKK 195 million (Q4 2014) – Conversion costs of approx. DKK 40 million (2016) – At the time of our withdrawal from SDC, BEC will grant us a discount roughly the same size as our costs of withdrawal BEC’s pricing structure ensures economical operation – More attractive prices for key account customers – Spar Nord’s annual IT bill will be cut by DKK 35 million in 2016 and by DKK 55 million from 2017 and onwards – Viewed in isolation, Spar Nord’s cost/income ratio will be reduced by 2 percentage points Some of our wholesale customers in Trading, Financial Markets & the International Division may choose to leave us – But we will do our best to remain an attractive provider – and hold on to them – Our base case scenario includes a reduction in income Synergies expected to arise from better cohesion between work processes and IT platform – Not yet quantified and factored in Page 4 BUSINESS -

Euroclear Bank Participants List

Euroclear Bank Participants List Participant Name BIC Code Participant Code AARGAUISCHE KANTONALBANK KBAGCH22XXX 92304 AB SVENSK EXPORTKREDIT SEKXSESSXXX 97147 ABAXBANK SPA ICBBITMMXXX 27431 ABBEY NATIONAL TREASURY SERVICES PL ANTSGB2LXXX 21391 ABBEY NATIONAL TREASURY SERVICES PL ANTSGB2LXXX 24587 ABBEY NATIONAL TREASURY SERVICES PL ANTSGB2LXXX 90281 ABLV BANK AS AIZKLV22XXX 18576 ABN AMRO BANK (SWITZERLAND) AG UBPGCHZ8XXX 12180 ABN AMRO BANK N.V. (FORMERLY FBN) FTSBNL2RXXX 12826 ABN AMRO BANK N.V. (FORMERLY FBN) FTSBNL2RXXX 12827 ABN AMRO BANK NV ABNAJESHXXX 13030 ABN AMRO BANK NV ABNANL2AXXX 90105 ABN AMRO BANK NV, RODERVELTLAAN ABNABE2AIPCXXX 93170 ABN AMRO GLOBAL CUSTODY NV n.a. 21900 ABN AMRO GLOBAL CUSTODY NV n.a. 24936 ABN AMRO GLOBAL CUSTODY SERVICES N. FTSBNL2RXXX 10937 ABN AMRO GLOBAL CUSTODY SERVICES N. FTSBNL2RXXX 11963 ABN AMRO GLOBAL CUSTODY SERVICES N. FTSBNL2RXXX 14447 ABN AMRO GLOBAL CUSTODY SERVICES N. FTSBNL2RXXX 14448 ABN AMRO GLOBAL CUSTODY SERVICES N. FTSBNL2RXXX 94763 ABN AMRO GLOBAL CUSTODY SERVICES N. FTSBNL2RXXX 97465 ABSA BANK LTD ABSAZAJJXXX 18440 ABU DHABI COMMERCIAL BANK PJSC ADCBAEAATRYXXX 15438 ABU DHABI INVESTMENT COMPANY ADICAEAAXXX 93301 ADAM & COMPANY PLC ADAGGB2SXXX 13446 ADAM & COMPANY PLC ADAGGB2SXXX 13458 ADAM & COMPANY PLC ADAGGB2SXXX 13460 1 ADAM & COMPANY PLC ADAGGB2SXXX 13504 ADAM & COMPANY PLC ADAGGB2SXXX 13576 ADAM & COMPANY PLC ADAGGB2SXXX 13638 ADAM & COMPANY PLC ADAGGB2SXXX 13641 ADAM & COMPANY PLC ADAGGB2SXXX 13646 ADM INVESTOR SERVICES INTERNATIONAL n.a. 10123 AFRICAN DEVELOPMENT BANK