Common Principles for Bank Account Switching’

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Jyske Bank H1 2014 Agenda

Jyske Bank H1 2014 Agenda • Jyske Bank in brief • Jyske Banks Performance 1968-2013 • Merger with BRFkredit • Focus in H1 2014 • H1 2014 in figures • Capital Structure • Liquidity • Credit Quality • Strategic Issues • Macro Economy & Danish Banking 2013-2015 • Danish FSA • Fact Book 2 Jyske Bank in brief 3 Jyske Bank in brief Jyske Bank focuses on core business Description Branch Network • Established and listed in 1967 • 2nd largest Danish bank by lending • Total lending of DKK 344bn • 149 domestic branches • Approx. 900,000 customers • Business focus is on Danish private individuals, SMEs and international private and institutional investment clients • International units in Hamburg, Zürich, Gibraltar, Cannes and Weert • A de-centralised organisation • 4,352 employees (end of H1 2013) • Full-scale bank with core operations within retail and commercial banking, mortgage financing, customer driven trading, asset management and private banking • Flexible business model using strategic partnerships within life insurance (PFA), mortgage products (DLR), credit cards (SEB), IT operations (JN Data) and IT R&D (Bankdata) 4 Jyske Bank in brief Jyske Bank has a differentiation strategy “Jyske Differences” • Jyske Bank wants to be Denmark’s most customer-oriented bank by providing high standard personal financial advice and taking a genuine interest in customers • The strategy is to position Jyske Bank as a visible and distinct alternative to more traditional providers of financial services, with regard to distribution channels, products, branches, layout and communication forms • Equal treatment and long term relationships with stakeholders • Core values driven by common sense • Strategic initiatives: Valuebased management Differentiation Risk management Efficiency improvement Acquisitions 5 1990 1996 2002 2006 (Q4) 2011/2012 Jyske Bank performance 1968-2013 6 ROE on opening equity – 1968-2013 Pre-tax profit Average: (ROE on open. -

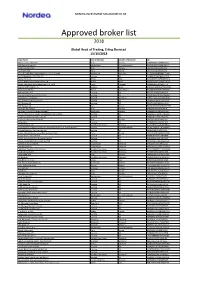

External Borkers List

NORDEA INVESTMENT MANAGEMENT AB Approved broker list 2018 Global Head of Trading, Erling Skorstad 15/10/2018 Legal Name City of Domicile Country of Domicile LEI ABG Sundal Collier ASA Oslo Norway 2138005DRCU66B8BNY04 ABN Amro Group NV Amsterdam The Netherlands BFXS5XCH7N0Y05NIXW11 Arctic Securities AS Oslo Norway 5967007LIEEXZX4RVS72 Aurel BGC SAS Paris France 5RJTDGZG4559ESIYLD31 Australia and New Zealand Banking Group Limited Melbourne Australia JHE42UYNWWTJB8YTTU19 AUTONOMOUS RESEARCH LLP London UK 213800LBM6PT85IGM996 Banca IMI S.p.A Milan Italy QV4Q8OGJ7OA6PA8SCM14 Banco Bilbao Vizcaya Argentaria S.A Bilbao Spain K8MS7FD7N5Z2WQ51AZ71 Banco Português de Investimento, S.A. (BPI) Porto Portugal 213800NGLJLXOSRPK774 BANCO SANTANDER S.A Madrid Spain 5493006QMFDDMYWIAM13 Bank Vontobel AG Zurich Switzerland 549300L7V4MGECYRM576 Barclays Bank PLC London UK G5GSEF7VJP5I7OUK5573 Barclays Capital Securities Limited London UK K9WDOH4D2PYBSLSOB484 Bayerische Landesbank Munich Germany VDYMYTQGZZ6DU0912C88 BCS Prime Brokerage Limited London UK 213800UU8AHE2B6QUI26 BGC Brokers LP London UK ZWNFQ48RUL8VJZ2AIC12 BNP Paribas SA Paris France R0MUWSFPU8MPRO8K5P83 Carnegie AS Norway Oslo Norway 5967007LIEEXZX57BC18 Carnegie Investment Bank AB (publ) Stockholm Sweden 529900BR5NZNQZEVQ417 China International Capital Corporation (UK) Limited London UK 213800STG3UV87MDGA96 Citigroup Global Markets Limited London UK XKZZ2JZF41MRHTR1V493 Clarksons Platou Securities AS Oslo Norway 5967007LIEEXZXA40G44 CLSA (UK) London UK 213800VZMAGVIU2IJA72 Commerzbank AG Frankfurt -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Contents More Information

Cambridge University Press 978-1-107-10685-7 - The Future of Financial Regulation: Who Should Pay for the Failure of American and European Banks? Johan A. Lybeck Table of Contents More information Contents List of figures x List of tables xii List of boxes xiv Preface xv Acknowledgements xix List of abbreviations xx Introduction xxv Part I A chronological presentation of crisis events January 2007 – December 2014 1 Part II Bail-out and/or bail-in of banks in Europe: a country-by-country event study on those European countries which did not receive outside support 143 1 United Kingdom: Northern Rock, Royal Bank of Scotland (RBS), Lloyds Banking Group 149 2 Germany: IKB, Hypo Real Estate, Commerzbank, Landesbanken 175 3 Belgium, France, Luxembourg: Dexia 191 4 Benelux: Fortis, ING, SNS Reaal 199 5 Italy: Monte dei Paschi di Siena 209 6 Denmark: Roskilde Bank, Fionia Bank and the others vs. Amagerbanken and Fjordbank Mors 216 vii © in this web service Cambridge University Press www.cambridge.org Cambridge University Press 978-1-107-10685-7 - The Future of Financial Regulation: Who Should Pay for the Failure of American and European Banks? Johan A. Lybeck Table of Contents More information viii Contents Part III Bail-out and/or bail-in of banks in Europe: a country-by-country event study on those European countries which received IMF/EU support 225 7 Iceland: Landsbanki, Glitnir and Kaupthing 227 8 Ireland: Anglo Irish Bank, Bank of Ireland, Allied Irish Banks 237 9 Greece: Emporiki, Eurobank, Agricultural Bank 259 10 Portugal: Caixa Geral, -

Lista Banków Przyjmujących Przelewy Europejskie (Stan Na 01.10.2010)

Lista banków przyjmujących przelewy Europejskie (stan na 01.10.2010) BELGIUM ING BELGIUM SA/NV BBRUBEBB FORTIS BANK NV/SA GEBABEBB DEXIA BANK BELGIUM N.V GKCCBEBB KBC BANK NV BRUSSELS KREDBEBB LA POST SA DE DROIT PUBLIC PCHQBEBB AACHENER BANK EG, FILIALE EUPEN AACABE41 ABN AMRO BANK (BRUSSELS BRANCH) BELGIUM ABNABEBR ABK ABERBE21 ANTWERPSE DIAMANTBANK NV ADIABE22 ARGENTA SPAARBANK NV ARSPBE22 AXA BANK NV AXABBE22 BANK OF BARODA BARBBEBB BANCO BILBAO VIZCAYA ARGENTARIA BRUSSELS BBVABEBB BANQUE CHAABI DU MAROC BCDMBEB1 BKCP BKCPBEB1 CREDIT PROFESSIONNEL SA (BKCP) BKCPBEBB BANCA MONTE PASCHI BELGIO BMPBBEBB DELTA LLOYD BANK SA BNAGBEBB BNP PARIBAS BELGIQUE BNPABEBB BANK OF AMERICA, ANTWERP BRANCH BOFABE3X BANK OF TOKYO MITSUBISHI NV BOTKBEBX BANK VAN DE POST BPOTBEB1 SANTANDER BENELUX BSCHBEBB BYBLOS BANK EUROPE BYBBBEBB JP MORGAN CHASE BANK BRUSSELS CHASBEBX CITIBANK INTERNATIONAL PLC CITIBEBX COMMERZBANK AG, ANTWERPEN COBA COBABEBB COMMERZBANK BELGIEN N.V/S.A. COBABEBB COMMERZBANK AG, BRUSSELS COBABEBX BANQUE CREDIT PROFESSIONEL DU HAINAUT SCRL CPDHBE71 CBC BANQUE SA BRUXELLES CREGBEBB CITIBANK BELGIUM SA CTBKBEBX BANK DEGROOF SA DEGRBEBB BANK DELEN NV DELEBE22 DEUTSCHE BANK BRUSSELS DEUTBEBE DRESDNER BANK BRUSSELS BRANCH DRESBEBX ETHIAS BANK NV ETHIBEBB EUROPABANK NV EURBBE99 VAN LANSCHOT BANKIERS BELGIË NV FVLBBE22 GOFFIN BANK NV GOFFBE22 HABIB BANK LTD BELGIUM HABBBEBB MERCATOR BANK NV HBKABE22 HSBC BANK PLC BRUSSELS HSBCBEBB THE BANK OF NEW YORK, BRUSSELS BRANCH IRVTBEBB BANK J. VAN BREDA JVBABE22 KBC ASSET MANAGEMENT KBCABEBB KBC FINANCIAL -

FHB Mortgage Bank Co. Plc. PUBLIC OFFERING the FHB Mortgage

FHB Mortgage Bank Co. Plc. PUBLIC OFFERING The FHB Mortgage Bank Co. Plc’s (registration number: 01-10-043638, date of registration: 18 March 1998, head office: 1082 Budapest, Üllői út 48.) (hereafter: “Issuer”, FHB Nyrt.” or “Bank”) Board of Directors has a regulation No. 89/2012. (14. December) to launch its Issue Program 2012-2013 with a HUF 200 billon total nominal value for issuance of Hungarian Covered Mortgage Bonds (jelzáloglevelek) and Notes, within the frameworks of it the Issuer is planning to issue different registered covered mortgage bonds’ and bonds’ series and within the series different tranches. Since there is no universal responsibility between the Issuer and the Managers, the securities issued under the auspices of the Base Prospectus have out of ordinary risks. The Issuer publishes its Base Prospectus on the website of its own and of the BSE the hard copies are available at the selling places. The number and date of the license granted by the Hungarian Financial Supervisory Authority (HFSA) to publish the Base Prospectus of the Issue Program and the disclosure of the public issue: KE-III-55/2012. 03. February 2012. The FHB Mortgage Bank Co. Plc’s (registration number: 01-10-043638, date of registration: 18 March 1998, head office: 1082 Budapest, Üllői út 48.) (hereafter: “Issuer”, FHB Nyrt.” or “Bank”) Board of Directors has a regulation No. 70/2012. (13. December) to launch its Issue Program 2013-2014 with a HUF 200 billon total nominal value for issuance of Hungarian Covered Mortgage Bonds (jelzáloglevelek) and Notes, within the frameworks of it the Issuer is planning to issue different registered covered mortgage bonds’ and bonds’ series and within the series different tranches. -

Beholdningsoversigt 31.03.2021 Jyske Bank.Xlsx

INSTRUMENT_TYPE ISIN ISSUER_NAME Formue Københavns Kommune i kr. 4.069.081.439,62 Equity GB00B0SWJX34 London Stock Exchange Group PLC 1.701.893,31 Equity GB00B24CGK77 Reckitt Benckiser Group PLC 3.564.881,56 Equity AU000000SYD9 Sydney Airport 1.337.059,47 Equity JP3435000009 Sony Corp 6.910.276,86 Equity US0091581068 Air Products and Chemicals Inc 3.520.243,74 Equity US87918A1051 Teladoc Health Inc 1.795.360,11 Equity NL0012169213 QIAGEN NV 1.219.259,56 Equity US12504L1098 CBRE Group Inc 1.615.018,42 Equity FR0013154002 Sartorius Stedim Biotech 1.136.250,30 Equity CH0432492467 Alcon Inc 1.661.975,62 Equity FR0000121667 EssilorLuxottica SA 2.339.599,76 Equity CH0010645932 Givaudan SA 2.497.439,42 Equity CH0013841017 Lonza Group AG 2.547.489,13 Equity FR0010533075 Getlink SE 1.081.032,87 Equity AU0000030678 Coles Group Ltd 1.716.338,55 Equity NO0003054108 Mowi ASA 988.624,03 Equity GB00BHJYC057 InterContinental Hotels Group PLC 1.324.892,92 Equity NL0013267909 Akzo Nobel NV 2.081.864,14 Equity CA12532H1047 CGI Inc 1.974.562,46 Equity SE0012455673 Boliden AB 1.168.396,04 Equity BMG475671050 IHS Markit Ltd 1.720.814,54 Equity CA82509L1076 Shopify Inc 5.815.734,65 Equity CA7677441056 Ritchie Bros Auctioneers Inc 1.079.486,62 Equity JP3198900007 Oriental Land Co Ltd/Japan 2.377.930,50 Equity US6516391066 Newmont Corp 3.214.940,55 Equity IE00BK9ZQ967 Trane Technologies PLC 1.962.517,98 Equity GB00B39J2M42 United Utilities Group PLC 1.586.616,23 Equity US0036541003 ABIOMED Inc 1.469.304,62 Equity US9553061055 West Pharmaceutical Services Inc 1.484.522,98 -

Standard Settlement Instructions of the MKB Bank

Standard settlement instructions of MKB Bank Zrt. for commercial transactions valid from December, 2017 Currency Name of the Bank & City SWIFT Code AUD Australia and New Zealand Banking Group Limited, ANZB AU 3M Melbourne BGN DSK Bank PLC, Sofia STSABGSF CAD Deutsche Bank AG, Frankfurt am Main DEUT DE FF CHF Zürcher Kantonalbank, Zürich ZKBK CH ZZ 80A CHF UBS AG, Zürich UBSW CH ZH 80A CZK Komercní Banka a.s., Prague KOMB CZ PP CNY Bank of China Limited, Budapest Branch BKCH HU HH DKK Danske Bank AS, Copenhagen DABA DK KK EUR Commerzbank AG, Frankfurt am Main COBA DE FF EUR Deutsche Bank AG, Frankfurt am Main DEUT DE FF EUR UniCredit Bank Austria AG, Vienna BKAU AT WW EUR Intesa Sanpaolo SpA, Milan BCIT IT MM EUR Société Générale, Paris SOGE FR PP GBP National Westminster Bank PLC, London NWBK GB 2L HRK Zagrebacka banka dd., Zagreb ZABA HR 2X JPY The Bank of Tokyo-Mitsubishi UFJ Ltd, Tokyo BOTK JP JT NOK DNB Bank ASA, Oslo DNBA NO KK PLN mBank S.A., Warsaw BREX PL PW RON Raiffeisen Bank S.A., Bucharest RZBR RO BU RUB AO Unicredit Bank, Moscow* IMBKRUMM SEK Skandinaviska Enskilda Banken AB, Stockholm ESSE SE SS TRY Akbank TAS, Istanbul AKBK TR IS USD JPMorgan Chase Bank NA, New York CHAS US 33 USD Deutsche Bank Trust Co. Americas, New York BKTR US 33 USD Citibank NA, New York CITI US 33 USD The Bank of New York Mellon, New York IRVT US 3N *Account details for RUB account: Account with AO Unicredit Bank (IMBKRUMM), account number 30111810700014652763, INN 9909336928, AO Unicredit Bank ’s account number with the Central Bank of the Russian Federation, Moscow,. -

Danmarks Nationalbank 2 Thedanmarks Response of Householdnationalbank Customers to Negative Deposit Rates Analyses

ANALYSIS DANMARKS NATIONALBANK 27 APRIL 2021 — NO. 9 The response of house- hold customers to negative deposit rates Negative deposit Reduction in Announcement rates more deposits following increases demand widespread announcements for investments Negative deposit rates There are indications Household customers for household custom that household cus appear to increase their ers are now being tomers reduce their de demand for investment applied by most banks posits when their bank fund shares and switch in Denmark. Further announces negative their deposits to pool more, the banks have interest rates. However, schemes when faced gradually reduced the household customers’ with prospects of nega thresholds for when total deposits have tive deposit rates. negative interest rates increased during the are imposed. period of negative deposit rates. Read more Read more Read more ANALYSIS — DANMARKS NATIONALBANK 2 THEDANMARKS RESPONSE OF HOUSEHOLDNATIONALBANK CUSTOMERS TO NEGATIVE DEPOSIT RATES ANALYSES Low for long Denmark was the first country to introduce negative ABOUT THIS ANALYSIS monetary policy rates in 2012. Since then, Switzer- land, Sweden, Japan and the euro area have followed Most banks in Denmark have now in suit. troduced negative deposit rates for household customers. Furthermore, Very low and in some cases negative interest rates the banks have gradually reduced the thresholds for when negative have characterised the past decade across the ad- interest rates are payable. vanced economies. There are several reasons why interest rates have fallen to the current low levels. Low There are indications that household interest rates reflect the fact that inflation has been customers reduce their deposits subdued in many countries, but structural changes when their bank announces negative in household and corporate savings and investment interest rates. -

Opting Into the Banking Union Before Euro Adoption1

OPTING INTO THE BANKING UNION BEFORE EURO ADOPTION1 Summary The main motivation for establishing the Banking Union (BU) was the need to reverse financial fragmentation that crippled monetary transmission within the common currency area in the wake of the euro crisis. By design, the BU would raise the credibility of the euro area bank supervision, eliminate distinction between home and host supervisors, and sever the link between banks and sovereigns. This would, in turn, lead to lower bank compliance costs, lower barriers to cross-border activity, and lower funding costs for banks under the BU. As host countries of euro area banks, the NMS-6 would benefit from improved resilience of the euro area financial system and lower funding costs for parent banks. The full benefits of the BU will be realized once all its elements are in place, which is not yet the case. Most notably an effective common backstop is still needed to break the sovereign-bank links. Furthermore, there is no equal treatment of the eurozone and non-eurozone members of the BU with regards to their role in the Single Supervisory Mechanism (SSM), access to common (ECB) liquidity support or to a common fiscal backstop (with ESM currently acting as de facto common fiscal backstop for euro area banks). When would opting into the BU make sense for the NMS-6? For those new member states (NMS) that have set a target date for euro adoption (Romania), this amounts to choosing to frontload the phase-in of some of the necessary institutional changes. For others, the BU opt-in decision requires a careful consideration of country characteristics, policy preferences as well as BU’s modalities and implementation: BU design: the lack of equal (or fully equivalent) treatment of euro area and non-euro area members of the BU tilts the NMS-6’s decision against early BU opt-in and in favor of waiting until euro adoption. -

Bad Bank Resolutions and Bank Lending by Michael Brei, Leonardo Gambacorta, Marcella Lucchetta and Bruno Maria Parigi

BIS Working Papers No 837 Bad bank resolutions and bank lending by Michael Brei, Leonardo Gambacorta, Marcella Lucchetta and Bruno Maria Parigi Monetary and Economic Department January 2020 JEL classification: E44, G01, G21 Keywords: bad banks, resolutions, lending, non-performing loans, rescue packages, recapitalisations BIS Working Papers are written by members of the Monetary and Economic Department of the Bank for International Settlements, and from time to time by other economists, and are published by the Bank. The papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of the BIS. This publication is available on the BIS website (www.bis.org). © Bank for International Settlements 2020. All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated. ISSN 1020-0959 (print) ISSN 1682-7678 (online) Bad bank resolutions and bank lending Michael Brei∗, Leonardo Gambacorta♦, Marcella Lucchetta♠ and Bruno Maria Parigi♣ Abstract The paper investigates whether impaired asset segregation tools, otherwise known as bad banks, and recapitalisation lead to a recovery in the originating banks’ lending and a reduction in non-performing loans (NPLs). Results are based on a novel data set covering 135 banks from 15 European banking systems over the period 2000–16. The main finding is that bad bank segregations are effective in cleaning up balance sheets and promoting bank lending only if they combine recapitalisation with asset segregation. Used in isolation, neither tool will suffice to spur lending and reduce future NPLs. Exploiting the heterogeneity in asset segregation events, we find that asset segregation is more effective when: (i) asset purchases are funded privately; (ii) smaller shares of the originating bank’s assets are segregated; and (iii) asset segregation occurs in countries with more efficient legal systems. -

Quarterly Report for Q1 2008 for Spar Nord Bank DKK 183 Million in Pre-Tax Profits - Forecast for Core Earnings for the Year Repeated

To Stock Exchange Announcement OMX The Nordic Exchange Copenhagen No. 5, 2008 and the press For further information, contact: Lasse Nyby Chief Executive Officer Tel. +45 9634 4011 30 April 2008 Ole Madsen, Communications Manager Tel. +45 9634 4010 Quarterly report for Q1 2008 for Spar Nord Bank DKK 183 million in pre-tax profits - forecast for core earnings for the year repeated • Annualized 18% return on equity before tax • Net interest income up 15% to DKK 313 million • Net income from fees, charges and commissions down 20% to DKK 104 million • Market-value adjustments reduced to DKK 8 million • Costs grew 11% • DKK 8 million recognized as net income due to reversed impairment of loans and advances and related items • Earnings from the trading portfolio and an extra payment regarding Totalkredit amount to DKK 37 million in total • Lending up 15%, and a 26% hike in deposits • Forecast for core earnings for the year repeated Spar Nord Bank A/S • Moody’s rating: C, A1, P-1 (unchanged, outlook stable) Skelagervej 15 Developments in Q1 2008 P. O. Box 162 • 13 consecutive quarterly periods with net growth in customers DK-9100 Aalborg • Net interest income DKK 13 million up on Q4 2007 • Net income from fees, charges and commissions in line with Q3 and Q4 2007 results Reg. No. 9380 • Sustained strong credit quality level – reporting recognition of net income from Telephone +45 96 34 40 00 impairment of loans, advances, etc. for the 10th consecutive quarterly period Telefax + 45 96 34 45 60 • Business volume at same level as at end-2007 Swift spno dk 22 • Leasing activities continue to develop on a very satisfactory note • Interest margin widening at a moderate pace www.sparnord.dk • Wider yield spread between Danish mortgage-credit bonds and government bonds means distinctively lower market-value adjustments and loss on earnings from invest- [email protected] ment portfolios • Improved excess coverage relative to strategic liquidity target CVR-nr.