Value Capture Finance in Transit Oriented Development

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Jaipur Metro Rail Corporation Ltd. (A Govt

RFP No.F.1 (R-139)/JMRC/DC/Rev./OD-05/2020-21/15 Dated: 26.03.2021 (Package: OD-05 for Chandpole Metro Station area) Price Rs. 2360 (Inclusive of GST) LICENSING OF EXCLUSIVE RIGHTS FOR OUTDOOR ADVERTISEMENT ALONG THE JAIPUR METRO RAIL CORRIDOR [Chandpole Metro Station area] [Package: OD-05] REQUEST FOR PROPOSAL Jaipur Metro Rail Corporation Ltd. (A Govt. of Rajasthan undertaking) Admin Building, Metro Depot, Bhrigu Path, Mansarovar, Jaipur 302020. Website: www.jaipurmetrorail.in | CIN: U60221RJ2010SGC030630 RFP No.F.1 (R-139)/JMRC/DC/Rev./OD-05/2020-21/15 Dated: 26.03.2021 (Package: OD-05 for Chandpole Metro Station area) TABLE OF CONTENTS DISCLAIMER ...................................................................................................................................................... 1 1. NOTICE INVITING BIDS ................................................................................................................................ 2 1.1 INTRODUCTION ........................................................................................................................................ 2 1.2 SCHEDULE AND DATES TO THE INVITATION OF RFP .................................................................... 2 1.3 ELIGIBILITY CRITERION OF BIDDERS ................................................................................................ 4 2. DEFINITIONS .................................................................................................................................................. 6 3. INSTRUCTIONS TO -

RRP: Sector Assessment (Summary): Transport (Rail and Urban)

Bengaluru Metro Rail Project (RRP IND 53326) SECTOR ASSESSMENT (SUMMARY): TRANSPORT (RAIL AND URBAN) A. Sector Road Map I. Sector Performance, Problems, and Opportunities 1. Urban transport in India. Efficient and sustainable urban transport systems and mobility are critical for the smooth functioning of India’s cities. Although national population growth has slowed to 1.02% per year in 2019 from its peak at 2.33% in 1974,1 the urban population continues to grow rapidly. It is estimated that more than 50% of Indians will be living in urban areas by 2050, compared with 34% in 2018.2 Growing urbanization will result in the total number of Indian cities with populations of 1 million or more growing from 19 cities to 71 cities by 2050. About 70% of net new jobs generated by 2030 will be in urban areas.3 2. Rapid urbanization is intensifying demand for urban transport. India continues to rely heavily on private vehicles for urban transport. From 2003 to 2017, the number of total registered vehicles in India increased 318%, from 67 million to 253 million, an annual growth rate of 10%.4 The rapid increase in private vehicles on the roads has led to congestion and severe air pollution, causing serious health problems in many cities. Severe traffic congestion in just four major metropolises— Bengaluru, Delhi, Kolkata, and Mumbai—is estimated to cause $22 billion in economic losses annually.5 Consequently, the government is strongly committed to promoting public mass transport. Public transportation infrastructure in India needs high levels of investment and massive upgrading to spur a shift away from private vehicles to more sustainable forms of transport. -

Metro Rail Projects in India

MEMBERS' REFERENCE SERVICE LARRDIS LOK SABHA SECRETARIAT, NEW DELHI REFERENCE NOTE No. 49/RN/Ref/November/2016 For the use of Members of Parliament NOT FOR PUBLICATION1 METRO RAIL PROJECTS IN INDIA Prepared by Smt. Sunanda Das Mohanty, Additional Director (23035036) and Shri S.L. Dogra, Deputy Director of Lok Sabha Secretariat under the supervision of Smt. Kalpana Sharma, Joint Secretary. The reference material is for personal use of the Members in the discharge of their Parliamentary duties, and is not for publication. This Service is not to be quoted as the source of information as it is based on the sources indicated at the end/in the text. This Service does not accept any responsibility for the accuracy or veracity of the information or views contained in the note/collection. METRO RAIL PROJECTS IN INDIA INTRODUCTION Metros are major capital assets of cities. Urban Metro1 Projects have proven to be very useful in decongesting large cities. There are around 148 cities around the world which has a metro system with nearly 540 metro lines, 9,000 stations and 11,000 kilometres of line infrastructure . The world’s metro systems carry 150 million passengers per day. The earliest metro system, the London Underground, first electrified underground line opened in 1890, was the world's first metro system. With more than 500 km of infrastructure, Shanghai has the world’s longest Metro network. London is the longest non Asian Metro network in the ranking, with New York, Moscow, Madrid and Paris. INDIAN SCENARIO Metro systems2 are often given preference as mass transit options for Indian cities due to the belief that road-based bus systems cannot cater to capacity requirements as much as metro systems. -

Proceedings of UMI 2012

Proceedings of UMI 2012 Proceedings of UMI 2012 Institute of Urban Transport (India) HP Urban Mobility India 2011 Page 1 Proceedings of UMI 2012 Preface The National Urban Transport Policy of the Government of India, 2006 (NUTP), lays strong emphasis on building capabilities at the state and city level to address problems associated with urban transport and lays down the guidelines for developing sustainable urban transport systems as well. The Ministry of Urban Development, Government of India has taken two important steps to encourage cities to reform their city transport: Organizing an annual conference-cum-exhibition on 'Urban Mobility' at New Delhi every year (UMI) for dissemination of information and to facilitate exchange of ideas; According recognition to good urban transport initiatives by giving awards to selected good practice projects. The Ministry of Urban Development (MOUD), Government of India; held the annual conference cum exhibition on “Smart Mobility” from 5th to 8thDecember 2012 at New Delhi, India. The event was organized at the Manekshaw Centre, Dhaula Kuan, New Delhi, India, by the Institute of Urban Transport (India) New Delhi. It was attended by approximately 1100 participants, comprising urban transport practitioners, resource persons, researchers, scholars and senior government officials from 21 countries, including The United States of America, Australia, Singapore, Korea, France, Germany etc. Additionally, there were representatives from 18 state governments and several urban local bodies and para-statals as well as academia, students, nongovernmental organizations (NGOs), and representatives from the private sector also. 13% of r all participants were foreign nationals, and 14% were students. E Representatives from the private sector added another 23% while that from the government organizations, 51%. -

Jaipur Metro Rail Corporation Limited

JAIPUR METRO RAIL CORPORATION LIMITED (A Government of Rajasthan Undertaking) Registered Office: Admin Building, Metro Depot, Bhrigu Path, Mansarovar, Jaipur-302020 Website: www.jaipurmetrorail.in, CIN: U60221RJ2010SGC030630 No. F.1(H-214)/JMRC/DCA/SS-XV/2020/9075 Dated: 1st April, 2020 VACANCY CIRCULAR INVITING APPLICATIONS FOR DEPUTATION Jaipur Metro Rail Corporation Ltd. (JMRC), a Government of Rajasthan Undertaking registered under the Companies Act, 1956, is implementing Metro Rail Transit System in Jaipur city and its commercial operations started on 3rd June, 2015. Through this circular, JMRC seeks applications for deputation by Special Selection from amongst the employees of Indian Railways and its subsidiary/sister concerns, Metro Rail Corporations or any Ministry, Department, Office, Undertaking, Board or Organisation of the Central Government or a State Government. The list of vacant posts to be filled, along with details of pay, qualification and experience for each post, is enclosed as Annexure-I. The posts indicated in Annexure-I are tentative which also include the posts likely to become vacant in near future. JMRC reserves the right to change/ cancel the vacancies or to defer selection/screening process for any of these posts at any stage depending upon developments in the meanwhile. Selection for appointment to the posts shall be made from amongst the applicants who possess requisite qualification and experience for the post as on the Last Date for Receipt of Applications and hold lien on a regular post in the parent department/organization. The process of selection from amongst those who apply for deputation is called special selection and is described in JMRC Recruitment and Service Rules, 2012, hosted on JMRC website, i.e., www.jaipurmetrorail.in, or http://transport.rajasthan.gov.in/jmrc. -

Trams Der Welt / Trams of the World 2021 Daten / Data © 2021 Peter Sohns Seite / Page 1

www.blickpunktstrab.net – Trams der Welt / Trams of the World 2021 Daten / Data © 2021 Peter Sohns Seite / Page 1 Algeria ... Alger (Algier) ... Metro ... 1435 mm Algeria ... Alger (Algier) ... Tram (Electric) ... 1435 mm Algeria ... Constantine ... Tram (Electric) ... 1435 mm Algeria ... Oran ... Tram (Electric) ... 1435 mm Algeria ... Ouragla ... Tram (Electric) ... 1435 mm Algeria ... Sétif ... Tram (Electric) ... 1435 mm Algeria ... Sidi Bel Abbès ... Tram (Electric) ... 1435 mm Argentina ... Buenos Aires, DF ... Metro ... 1435 mm Argentina ... Buenos Aires, DF - Caballito ... Heritage-Tram (Electric) ... 1435 mm Argentina ... Buenos Aires, DF - Lacroze (General Urquiza) ... Interurban (Electric) ... 1435 mm Argentina ... Buenos Aires, DF - Premetro E ... Tram (Electric) ... 1435 mm Argentina ... Buenos Aires, DF - Tren de la Costa ... Tram (Electric) ... 1435 mm Argentina ... Córdoba, Córdoba ... Trolleybus Argentina ... Mar del Plata, BA ... Heritage-Tram (Electric) ... 900 mm Argentina ... Mendoza, Mendoza ... Tram (Electric) ... 1435 mm Argentina ... Mendoza, Mendoza ... Trolleybus Argentina ... Rosario, Santa Fé ... Heritage-Tram (Electric) ... 1435 mm Argentina ... Rosario, Santa Fé ... Trolleybus Argentina ... Valle Hermoso, Córdoba ... Tram-Museum (Electric) ... 600 mm Armenia ... Yerevan ... Metro ... 1524 mm Armenia ... Yerevan ... Trolleybus Australia ... Adelaide, SA - Glenelg ... Tram (Electric) ... 1435 mm Australia ... Ballarat, VIC ... Heritage-Tram (Electric) ... 1435 mm Australia ... Bendigo, VIC ... Heritage-Tram -

Rolling Stock for Metro Railways

GOVERNMENT OF INDIA MINISTRY OF URBAN DEVELOPMENT REPORT OF THE SUB-COMMITTEE ON ROLLING STOCK FOR METRO RAILWAYS NOVEMBER 2013 2 Preface 1. Metro systems are already operational in Delhi and Bangalore and construction work is progressing at a fast pace in Chennai, Kolkata, Hyderabad, Jaipur, Kochi and Gurgaon. There are plans to have Metro Systems in cities with population more than 2 million. MOUD with a view to promote the domestic manufacturing for Metro Systems and formation of standards for such systems in India, has constituted a Group for preparing a Base paper on Standardization and Indigenization of Metro Railway Systems vide Order of F.No.K- 14011/26/2012 MRTS/Coord dated 30th May 2012. 2. The Group has identified certain issues which require detailed deliberations / review cost benefit analysis / study. The Group suggested that Sub-Committees may be constituted consisting of officers/professional drawn from relevant field/ profession from Ministry of Urban Development/Railways/Metros and industries associated with rail based systems / Metro Railway Systems. 3. Accordingly following Sub-Committees for various systems were constituted by Ministry of Urban Development vide order No. K-14011/26/2012-MRTS/Coorddt. 30.05.2012/25.07.2012: · Traction system · Rolling stock · Signaling system · Fare collection system · Operation & Maintenance · Track structure · Simulation Tools 4. The Sub-committee on Rolling Stock has following members: Shri Sanchit Pandey CGM/Rolling Stock/P/DMRC. Shri Amit Banerjee, GM/Technology Divn. BEML, Bangaluru. Shri Naresh Aggarwal, Chairman CII, Railway Equipment Divn. & MD & Co- Chairman, VAE, VKN Industries Pvt. Ltd. Shri Raminder Singh, Siemens Ltd. -

Analysis of Metro Rail Project Selection Bias with Principal-Agent Model

Analysis of Metro rail Project selection Bias with Principal-Agent Model A case of Delhi,Bangalore,Mumbai,Jaipur and Chennai Vinod Rathod Background Urban Metro Projects have proven to be very useful in decongesting large cities. 148 cities around the world had Metro System. In World Metro systems carry 150 million passengers per day. In India, many cities are now considering the Metro system as an alternative The 12th fifth year plan Urban Transport group has recommended, Metro is only one of the Options for decongestion. Growth of Metro rail system Growth of Metro rail system in India 300 250 200 150 kms 100 50 0 2002 2004 2006 2008 2010 2012 2014 2016 (Canavan, 2015) UnderConstruction (in Kms) Operational (in Kms) Background Metro rail Transit is attached with the High capital and operating costs. It found that most of the metro systems around the world are not financially viable. Public investment in rail transit has long been controversial (Wenling, 2006) Failures of rail projects to materialize the targeted performance in terms of ridership speed, operating costs, and development benefits, on which grounds they had been justified (Pickrell ,1989) Anticipated project objectives are moderately met but at very high costs. Under-investment on low-cost and more cost-effective transit alternatives, such as the conventional bus or Bus Rapid Transit (BRT), because resources are often allocated to light rail investments. (Wenling, 2006) Need of Study Why Such a huge Capital Intensive Project ??? Analysis of Metro Rail Project Selection -

Transportation Jaipur Metro Railway, India

Solutions Hytera ACCESSNET-T IP mobile radio system for the Shenzhen metro mainly consists of: --72 base stations are connected to the switching node via the IP backbone. --2 IPN switch nodes are redundant to each other. The failure of one IPN site will not affect the radio Jaipur Metro Railway, India operation. Hytera TETRA Solutions Serve India Metro --The newly-built OCC includes 27 multi-user customized dispatcher systems to meet their high level requirements. -- 1500 portables, 80 fixed stations and 266 train-borne. Hytera will also provide DMR Trunking products for station service management like security, cleaning and station staff, with 1 set DMR switch center, 72 BSs, 1950 portables. Both TETRA and DMR signal will be combined transmitting by leaky coaxial cables (LCX) along whole elevated viaduct and underground tunnel trackside to ensure good signal coupling and constant line of sight between transmitter and receiver. T User r Jaipur Metro Railway, India anspor tation Hightlights Market segment Metro tation 1. Comprehensive range of redundancy Project time anspor r 2015 T The particularity of the system for Shenzhen Metro is the high-level reliability which is achieved by Geographical redundancy of the switching unit, redundancy of control channel and fallback Products operation of the base stations. It allows continuously voice and data communication even in the CZT802H&GDT801Train borne event of failure of entire sites. Customized Dispatch Work System, Network Manage System, 2. One stop service Centralized Digital Recording system Whatever the needs or the challenges of the MRT customers they have, Hytera can offer sincere and tailored solutions for their radio communications with complete MRT product line, including the standard TETRA infrastructure, dispatcher & train-borne, plus abundant coverage design and on-site experience in the process of construction. -

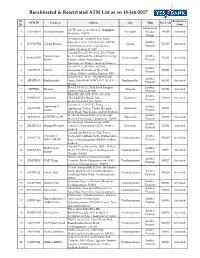

Recalibrated & Reactivated ATM List.Xlsx

Recalibrated & Reactivated ATM List as on 18-Jan-2017 Sr. Reactivation ATM ID Location Address City State Pin Code No. Status Andaman & GF/FF, Survey no. 104/1/2, Junglighat, 1 EPOAB650 Port Blair branch Port Blair Nicobar 744103 Activated Port blair - 744103 Islands Yes Bank Ltd., Ground Floor, Satya Akarsha, T S No. 2/5, Door No. 5-87-32, Andhra 2 SGUNC554 Guntur Branch Guntur 522007 Activated Lakshmipuram main road, Guntur, Pradesh Andhra Pradesh 522 007. Ground Floor, H. No. 9-9-2, New Ward Narasaoropet no. 16, Old Ward No. 4, Block No. 2, Opp. Andhra 3 SNAWN551 Narasaoropet 522601 Activated Branch Angele Talkies, Arundalpeta, Pradesh Narasaraopet, Guntur, Andhra Pradesh – Ground floor, KO Rise, 16/2961, Andhra 4 SNEPB671 Nellore Jawaharlal Nehru Road, Near V R Nellore 524001 Activated Pradesh College, Nellore, Andhra Pradesh. PIN – Ground floor, D. No. 75-6-25,Prakash Andhra 5 SRAPB651 Rajahmundry Nagar, RAJAHMUNDRY, E.G. Dt. A.P - - Rajahmundry 533103 Activated Pradesh 533103. Floor, 13-3-92/A1 Tilak Road Tirupati, Andhra 6 STIPB483 Tirupati Tirupati 517501 Activated Andhra Pradesh 517501 Pradesh KRANTI ARCADE, D NO. 40/1/59, Andhra 7 SVJWN217 Vijaywada NEAR BENZ CIRCLE, M.G. Vijaywada 520010 Activated Pradesh ROAD,VIJAYWADA- 520010 Ground floor, 29-37-21, Durga Vijaywada II Andhra 8 SELNC884 Agraharam, Next to Vijetha Hospital, Vijaywada 520002 Branch Pradesh Eluru Road, Vijayawada, Andhra Pradesh K.T.Road, Beside Muthoot Gold, Opp. Andhra 9 SCPO1218 CHITTINAGAR Vijaywada 520001 Activated Musizd, Chittinagar, Vijayawada - 520001 Pradesh Do- No-Near Kanada durga vardhi, Andhra 10 SMAPO363 Manipal Hospital Tadepalli, Vijayawada-522501, Andhra Vijaywada 522501 Activated Pradesh pradesh. -

JAIPUR METRO JAIPUR Introduction… …

JAIPUR METRO JAIPUR introduction… … . URBAN SPREAD O F JAIPUR JAIPUR M ETRO RO UTE E-W Corridor N-S Corridor • Routes planned along two of the major arterial roads of Jaipur Key Features of East W est Corridor • • 9 a / • Ü / . / • KEY FEATURES O F N O RTH SO UTH CO RRIDO R • 23. 099 kms length • 15 elevated and 5 underground stations • Elevated Section from Ambabari to Pani Petch • Underground from Pani Petch to Ajmeri Gate • Elevated from Ajmeri Gate to Sitapura • Initially the N-S Corridor was envisaged from Ambabari to Durgapura, which is now being extended to Sitapura. Rapid Im plem entation • Jaipur Metro œ one of the fastest metro projects ever implemented worldwide 3 First Stage to commence operations by June 2013, 3 Prime concern œ Cost optimisation and minimum cost escalation Kickstart the project and attracting partners for the second stage A hybrid approach Stage œI to kickstart the project through EPC Operational in 3 years Stage œ II through PPP O7&1M of the entire network by PPP Concessionaire IN ITIAL PRO JECT STRUCTURE JAIPUR METRO RAIL PROJECT EAST WEST NORTH EAST WEST (A) CORRIDOR (B) SOUTH CORRIDOR CORRIDOR ROLLING CIVIL WORK STOCK, S&T, AFC ENTIRE SCOPE ENTIRE SCOPE EPC (through Etc PPP PPP DMRC) PPP REVISED PRO JECT STRUCTURE JAIPUR METRO RAIL PROJECT EAST WEST (B) NORTH EAST WEST (A) CORRIDOR SOUTH CORRIDOR CORRIDOR ROLLING STOCK, CIVIL WORK ENTIRE SCOPE ENTIRE SCOPE S&T, AFC ETC. EPC EPC PPP EPC Operation & Maintenance for initial 5 years Pre œ Operative Own manpower Phase (PPP) PRO JECT CO -

D E L H I M E T

D E L H I M E T R O DMRC ACHIEVEMENTS Travel without air and noise pollution Reduced journey time Introduction of rapid construction techniques Pioneer in safe construction Introduction of precast and prefab structures in massive construction projects First Railway project registered by the United Nations for energy conservation Shining example for completing a project before time and within budgeted cost SIX TO EIGHT COACHES SIX LINES 35 UNDERGROUND 140 STATIONS 105 ELEVATED DELHIGLIMPSES GHAZIABAD OF NCR METRO DELHI NCR METRO NOIDA DELHI OF GLIMPSES FARIDABAD GURGAON 60000-80000 PHPDT CARRYING CAPACITY FUTURE EXPANSION Planning for extension to Greater Noida covering 86 kms with around 19 stations and Faridabad covering 105 kms. Involved with the implementation and construction of Kochi Metro, Jaipur Metro and Lucknow Metro. Served as the project consultant and has prepared detailed project reports (DPR) for most of the metro and monorail project in India DMRC NEXT POSSIBLE DESTINATION... CURRENT WORKS & FUTURE POSSIBILITIES ELEVATED STATIONS Noida City Centre Dubai Metro Station CURRENT WORKS & FUTURE POSSIBILITIES Surajmal Stadium Huda City Centre Dubai Metro Station CURRENT WORKS & FUTURE POSSIBILITIES Dwarka Vancouver Brentwood Metro Station CURRENT WORKS & FUTURE POSSIBILITIES Indraprastha Vaishali Hague Beatrixkwartier Light-rail station Vancouver Brentwood Metro Station CURRENT WORKS & FUTURE POSSIBILITIES Kashmere Gate Airport Express Conceptual Design of Ningbo Metro Station CURRENT WORKS & FUTURE POSSIBILITIES Dhaula