Financialization and the Returns to Commodity Investments Scott Main

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

GUIDANCE Position Management Regime for ICE Futures Europe

GUIDANCE Position Management Regime for ICE Futures Europe Soft Commodities September 2018 Copyright IntercontinentalExchange, Inc. 2015. All Rights Reserved www.theice.com Contents 1. Introduction 3 2. Accountability Levels 4 3. Delivery Limits 5 4. Delivery Limit Exemptions 5 5. Aggregation 12 6. Enforcement 12 7. Changes to the Accountability Levels, Delivery Limits and Delivery Limit Exemption levels 13 Attachment 1 14 ICE Futures Europe – September 2018 Page 2 of 15 www.theice.com ICE Futures Europe Implementation of the Position Management Regime for ICE Futures Europe Soft Commodities 1. Introduction 1.1. In accordance with Rules A.2 and G.2 the Exchange may adopt such procedures as it deems appropriate to establish. With respect to Rule P.0A, this shall include procedures in respect of any specified delivery/expiry month of any Exchange Contract, or in the case of ICE Futures Europe London Cocoa and Euro Cocoa Contracts, a group of Exchange Contracts, or in respect of a combination of delivery/expiry months thereof, limits on the maximum open position that may be held by a Member for his own account or on behalf of his Client. 1.2. The purpose of this Guidance Document ("Guidance Document") is then to set out, pursuant to Rule P.0A, the procedures and associated guidance in respect of the regime for the monitoring and regulation of ICE Futures Europe London Cocoa and Euro Cocoa (for the purposes of this Guidance, “the Cocoa Contracts”), Robusta Coffee, White Sugar and Containerised White Sugar ( for the purposes of this Guidance “the Sugar Contracts”) and Wheat Futures and Options Contracts (collectively, the “Soft Commodity Contracts”). -

Updated Trading Participants' Trading Manual

Annexure 3 TRADING MANUAL BURSA MALAYSIA DERIVATIVES BHD TRADING MANUAL (Version 4.10) This manual is the intellectual property of BURSA MALAYSIA. No part of the manual is to be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording or any information storage and retrieval system, without permission in writing from Head of BMD Exchange Operations. TRADING MANUAL Version History Version Date Author Comments V 1.0 9 Aug 2010 BMDB Initial Version V 1.1 27 Aug 2010 BMDB Updated # 6.6.3 Review of Trades – Price Adjustments and Cancellations V1.2 6 Sep 2010 BMDB Inserted 15. Operator ID (“Tag 50 ID”) Required for All BMD orders traded on CME Globex V1.3 9 Sep 2010 BMDB Update 1. Introduction – 1.6 TPs’ compliance in relation to access, connectivity, specification or use of CME Globex V1.4 13 Sep 2010 BMDB Updated 13. Messaging And Market Performance Protection Policy V1.5 9 Nov 2011 BMDB Inserted 16 Negotiated Large Trade V1.6 18 Nov 2011 BMDB Amended section 16 for typo errors, consistency and clarity. V1.7 24 Nov 2011 BMDB Amended section 16 - Extended NLT cut-off time for FKLI, FKB3 and FMG5 to 4.00pm and for FCPO to 5.00pm. -Amended the NLT Facility Trade Registration form. V1.8 10 Feb 2012 BMDB Updated section 11 EFP to EFRP V1.9 23 Mar 2012 BMDB Amended sections 11 and 16 (forms and processes) V2.0 5 Apr 2012 BMDB Renamed to “Trading Manual” V2.1 14 May 2012 BMDB Updated Section 6 for OKLI and to align with CME practice V2.2 29 May 2012 BMDB i) Updated for OCPO ii) Change of terminology to be consistent with CME iii) Updated Sections 7.7 & 14.1 for consistency with Rules iv) Updated Sections 12.3 & 12.4 for accuracy v) Updated Section 3.1 on options naming convention V2.3 18 Feb 2013 BMDB Updated Section 16 NLT V2.4 3 Apr 2013 BMDB Updated Section 9 Circuit Breaker on timing V2.5 2 Jul 2013 BMDB Updated FGLD. -

The Pricing of Stock Index Futures During the Asian Financial Crisis: Evidence from Four Asian Index Futures Markets”

“The Pricing of Stock Index Futures During the Asian Financial Crisis: Evidence from Four Asian Index Futures Markets” AUTHORS Janchung Wang Janchung Wang (2007). The Pricing of Stock Index Futures During the Asian ARTICLE INFO Financial Crisis: Evidence from Four Asian Index Futures Markets. Investment Management and Financial Innovations, 4(2) RELEASED ON Saturday, 23 June 2007 JOURNAL "Investment Management and Financial Innovations" FOUNDER LLC “Consulting Publishing Company “Business Perspectives” NUMBER OF REFERENCES NUMBER OF FIGURES NUMBER OF TABLES 0 0 0 © The author(s) 2021. This publication is an open access article. businessperspectives.org Investment Management and Financial Innovations, Volume 4, Issue 2, 2007 77 THE PRICING OF STOCK INDEX FUTURES DURING THE ASIAN FINANCIAL CRISIS: EVIDENCE FROM FOUR ASIAN INDEX FUTURES MARKETS Janchung Wang* Abstract Market imperfections are traditionally measured individually. Hsu and Wang (2004) and Wang and Hsu (2006) recently proposed the concept of the degree of market imperfections, which reflects the total effects of all market imperfections between the stock index futures market and its underlying index market when implementing arbitrage activities. This study discusses some useful applications of this concept. Furthermore, Hsu and Wang (2004) developed an imperfect market model for pricing stock index futures. This study further compares the relative pricing perform- ance of the cost of carry and the imperfect market models for four Asian index futures markets (particularly for the Asian crisis period). The evidence indicates that market imperfections are im- portant in determining the stock index futures prices for immature markets and turbulent periods with high market imperfections. Nevertheless, market imperfections are excluded from the cost of carry model. -

Foreign Exchange Training Manual

CONFIDENTIAL TREATMENT REQUESTED BY BARCLAYS SOURCE: LEHMAN LIVE LEHMAN BROTHERS FOREIGN EXCHANGE TRAINING MANUAL Confidential Treatment Requested By Lehman Brothers Holdings, Inc. LBEX-LL 3356480 CONFIDENTIAL TREATMENT REQUESTED BY BARCLAYS SOURCE: LEHMAN LIVE TABLE OF CONTENTS CONTENTS ....................................................................................................................................... PAGE FOREIGN EXCHANGE SPOT: INTRODUCTION ...................................................................... 1 FXSPOT: AN INTRODUCTION TO FOREIGN EXCHANGE SPOT TRANSACTIONS ........... 2 INTRODUCTION ...................................................................................................................... 2 WJ-IAT IS AN OUTRIGHT? ..................................................................................................... 3 VALUE DATES ........................................................................................................................... 4 CREDIT AND SETTLEMENT RISKS .................................................................................. 6 EXCHANGE RATE QUOTATION TERMS ...................................................................... 7 RECIPROCAL QUOTATION TERMS (RATES) ............................................................. 10 EXCHANGE RATE MOVEMENTS ................................................................................... 11 SHORTCUT ............................................................................................................................... -

Exploring Environmental Tradeoffs in Soft Commodity Production

Exploring Environmental Tradeoffs in Soft Commodity Production Jen Bowe, Kenny Fahey, Mallory McLaughlin, Julia Ruedig, Sheena VanLeuven, Jay Wolfgram March 2013-April 2014 Modeling Environmental Tradeoffs in Soft Commodity Production 1 TABLE OF CONTENTS Introduction ..................................................................................................................................... 5 Transforming Markets: The 2050 Criteria .................................................................................. 5 Beyond The 2050 Criteria: Sustainable Sourcing....................................................................... 6 Commodity Sourcing and Environmental Tradeoffs .................................................................. 7 Project Goals and Objectives .......................................................................................................... 9 Research Methodology ................................................................................................................. 11 Research Sources....................................................................................................................... 11 Commodity Research ................................................................................................................ 12 Environmental Indicators .......................................................................................................... 13 Dimensions of Environmental Tradeoffs ................................................................................. -

Optimal Hedging Under Departures from the Cost-Of-Carry Valuation: Evidence from the Spanish Stock Index Futures Market

Journal of Banking & Finance 27 (2003) 1053–1078 www.elsevier.com/locate/econbase Optimal hedging under departures from the cost-of-carry valuation: Evidence from the Spanish stock index futures market Juan A. Lafuente a, Alfonso Novales b,* a Departamento de Finanzas y Contabilidad, Universidad Jaume I, 12071 Castellon, Spain b Departamento de Economııa Cuantitativa, Universidad Complutense, Somosaguas, 28223 Madrid, Spain Received 2 October 2000; accepted 11 January 2002 Abstract We provide an analytical discussion of the optimal hedge ratio under discrepancies between the futures market price and its theoretical valuation according to the cost-of-carry model. As- suming a geometric Brownian motion for spot prices, we model mispricing as a specific noise component in the dynamics of futures market prices. Empirical evidence on the model is pro- vided for the Spanish stock index futures. Ex-ante simulations with actual data reveal that hedge ratios that take into account the estimated, time varying, correlation between the com- mon and specific disturbances, lead to using a lower number of futures contracts than under a systematic unit ratio, without generally losing hedging effectiveness, while reducing transaction costs and capital requirements. Besides, the reduction in the number of contracts can be sub- stantial over some periods. Finally, a mean–variance expected utility function suggests that the economic benefits from an optimal hedge can be substantial. Ó 2003 Elsevier Science B.V. All rights reserved. JEL classification: C51; G11; G13 Keywords: Optimal hedging; Futures contract; Stock index; GARCH models; Mispricing 1. Introduction Since its launching in January 1992, the Ibex 35 futures contract quickly became the most actively traded derivative contract in Meff Renta Variable, the Spanish * Corresponding author. -

Options Trading

OPTIONS TRADING: THE HIDDEN REALITY RI$K DOCTOR GUIDE TO POSITION ADJUSTMENT AND HEDGING Charles M. Cottle ● OPTIONS: PERCEPTION AND DECEPTION and ● COULDA WOULDA SHOULDA revised and expanded www.RiskDoctor.com www.RiskIllustrated.com Chicago © Charles M. Cottle, 1996-2006 All rights reserved. No part of this publication may be printed, reproduced, stored in a retrieval system, or transmitted, emailed, uploaded in any form or by any means, electronic, mechanical photocopying, recording, or otherwise, without the prior written permission of the publisher. This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that neither the author or the publisher is engaged in rendering legal, accounting, or other professional service. If legal advice or other expert assistance is required, the services of a competent professional person should be sought. From a Declaration of Principles jointly adopted by a Committee of the American Bar Association and a Committee of Publishers. Published by RiskDoctor, Inc. Library of Congress Cataloging-in-Publication Data Cottle, Charles M. Adapted from: Options: Perception and Deception Position Dissection, Risk Analysis and Defensive Trading Strategies / Charles M. Cottle p. cm. ISBN 1-55738-907-1 ©1996 1. Options (Finance) 2. Risk Management 1. Title HG6024.A3C68 1996 332.63’228__dc20 96-11870 and Coulda Woulda Shoulda ©2001 Printed in the United States of America ISBN 0-9778691-72 First Edition: January 2006 To Sarah, JoJo, Austin and Mom Thanks again to Scott Snyder, Shelly Brown, Brian Schaer for the OptionVantage Software Graphics, Allan Wolff, Adam Frank, Tharma Rajenthiran, Ravindra Ramlakhan, Victor Brancale, Rudi Prenzlin, Roger Kilgore, PJ Scardino, Morgan Parker, Carl Knox and Sarah Williams the angel who revived the Appendix and Chapter 10. -

Overview of the World's Commodity Exchanges – 2007

United Nations Conference on Trade and Development Overview of the world’s commodity exchanges – 2007 Study prepared by the UNCTAD secretariat United Nations New York and Geneva, 2009 Overview of the world’s commodity exchanges – 2007 Note Symbols of United Nations documents are composed of capital letters combined with figures. Mention of such a symbol indicates a reference to a United Nations document. Material in this publication may be freely quoted or reprinted, but acknowledgement is requested. A copy of the publication containing the quotation or reprint should be sent to the UNCTAD secretariat at: Palais des Nations, CH-1211 Geneva 10, Switzerland. The views expressed in this publication are those of the author and do not necessarily reflect the views of the United Nations Secretariat. The designations employed and the presentation of the material in this document do not imply the expression of any opinion whatsoever on the part of the secretariat of UNCTAD concerning the legal status of any country, territory, city or area, or of this authorities or concerning the definition of its frontiers or boundaries. This document was prepared by Leonela Santana-Boado and Adam Gross of the UNCTAD secretariat, with substantial input and research assistance provided by Ms. Leticia Gennes Beltrán. The extensive contributions of Alexander Belozertsev to the sections on Russia and Ukraine are also gratefully acknowledged. Recent publications by the UNCTAD secretariat on the subject of commodity exchanges include “Overview of the world’s commodity -

What Drives Commodity Price Booms and Busts?

What Drives Commodity Price Booms and Busts? David S. Jacks and Martin Stuermer Federal Reserve Bank of Dallas Research Department Working Paper 1614 What drives commodity price booms and busts?* David S. Jacks (Simon Fraser University and NBER) Martin Stuermer (Federal Reserve Bank of Dallas, Research Department) November 2016 Abstract What drives commodity price booms and busts? We provide evidence on the dynamic effects of commodity demand shocks, commodity supply shocks, and inventory demand shocks on real commodity prices. In particular, we analyze a new data set of price and production levels for 12 agricultural, metal, and soft commodities from 1870 to 2013. We identify differences in the type of shock driving prices of the various types of commodities and relate these differences to commodity types which reflect differences in long-run elasticities of supply and demand. Our results show that demand shocks strongly dominate supply shocks. * The views in this paper are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Dallas or the Federal Reserve System. Jacks gratefully acknowledges the Social Science and Humanities Research Council of Canada for research support. We are grateful for comments and suggestions from participants at the Summer Meeting of the Association of Environmental and Resource Economists, at the Bank of Canada and Federal Reserve Bank of Dallas joint conference on commodity price cycles, at the Norges Bank/CAMP workshop, and at seminars at the Bundesbank and the European Central Bank. 1 JEL classification: E30, Q31, Q33, N50 Keywords: Commodity prices, natural resources, structural VAR 1. -

The Term Structures of Oil Futures Prices

The Term Structures of Oil Futures Prices Jacques Gabillon Oxford Institute for Energy Studies WPM 17 1991 The contents of this paper are the author’s sole responsibility. They do not necessarily represent the views of the Oxford Institute for Energy Studies or any of its Members. Copyright 0 1991 Oxford Institute for Energy Studies Registered Charity, No: 286084 All rights resewed. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without prior permission of the Oxford Institute for Energy Studies. This publication is sold subject to the condition that it shall not, by way of trade or otherwise, be lent, resold, hired out, or otherwise circulated without the publisher’s prior consent in any form of binding or cover other than that in which it is published and without a similar condition including this condition being imposed on the subsequent purchaser. ISBN 0 948061 59 6 EXECUTIVE SUMMARY In recent years, there has been a massive development of derivative financial products in oil markets. The main interest came from large energy end-users who found in them a welcome opportunity to lock in fixed or maximum prices for their supplies over a period of time. Oil companies and oil traders were able to provide tailor-made swaps or options for the specific needs of the end-users. It all started with refined petroleum product swaps traded only for short maturities. Soon after, a new interest in long-term swaps and options on crude oil emerged. -

Bloomberg Link

Market Commentary 1 Energy 6 Bloomberg Commodity Outlook – May 2018 Edition Metals 9 Agriculture 14 Bloomberg Commodity Index (BCOM) DATA PERFORMANCE: 17 Overview, Commodity TR, Prices, Volatility Broad Commodities Taking the Bull Horns CURVE ANALYSIS: 22 Contango/Backwardation, - Commodity bull appearing young & vibrant vs. mature stock market Roll Yields, Forwards/Forecasts - Carry is a positive but crude oil prices remain extended MARKET FLOWS: 25 - Copper to gold: metals in bull-market transition with stocks Open Interest, Volume, COT, ETFs - Agriculture indicates early recovery from loss-of-faith lows - A potential commodities perfect storm is brewing for 2018 Gold Outlook Webinar – May 3, 10:00 EDT Commodity Investing Outlook Webinar – May 9, 11:00 EDT Data and outlook as of April 30 Mike McGlone – BI Senior Commodity Strategist BI COMD (the commodity dashboard) recipe for higher commodity prices. The nascent Commodity Bull Appears Young and commodity bull is gaining on the elderly stock-market Vibrant Vs. Mature Stock Market rally. A sustained dollar recovery is a key risk, but Performance: April +2.7%, YTD +2.3%, Spot +3.4%. unlikely. (Returns are total return (TR) unless noted) Commodities Looking Beyond April Dollar Gain. (Bloomberg Intelligence) -- Less than three years into a Despite a sharp recovery in the dollar, commodities' recovery, commodities are gaining momentum vs. the divergent strength in April indicates their outperformance decade-long rally in stocks. Favorable demand vs. supply vs. equities and bonds should accelerate. The 2018 and a multiyear price decline vs. bottoming equity-market increase of about 3% through April vs. a flat S&P 500 volatility from the lowest in decades should continue to may be just the beginning as the Bloomberg Commodity favor commodities. -

Circular 18/236 Ifeu Soft Commodity Futures and Options - Changes to Exchange and Clearing Fees

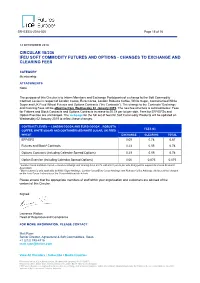

SR-ICEEU-2018-025 Page 15 of 16 14 DECEMBER 2018 CIRCULAR 18/236 IFEU SOFT COMMODITY FUTURES AND OPTIONS - CHANGES TO EXCHANGE AND CLEARING FEES CATEGORY Membership ATTACHMENTS None The purpose of this Circular is to inform Members and Exchange Participants of a change to the Soft Commodity Contract Levies in respect of London Cocoa, Euro Cocoa, London Robusta Coffee, White Sugar, Containerized White Sugar and UK Feed Wheat Futures and Options Contracts (“the Contracts”). The change to the Contracts’ Exchange and Clearing Fees will be effective from Wednesday 02 January 2019. The new fee structure is outlined below. Fees for Futures and Block Contracts and Options Contracts increase to £0.78 per lot per side. Fees for EFP/EFSs and Option Exercise are unchanged. The webpage for the full set of fees for Soft Commodity Products will be updated on Wednesday 02 January 2019 to reflect these changes. CONTRACT LEVIES — LONDON COCOA AND EURO COCOA1 , ROBUSTA FEES (£) COFFEE, WHITE SUGAR AND CONTAINERISED WHITE SUGAR, UK FEED WHEAT EXCHANGE CLEARING TOTAL EFP/EFS 0.09 0.78 0.87 Futures and Block2 Contracts 0.23 0.55 0.78 Options Contracts (including Calendar Spread Options) 0.23 0.55 0.78 Option Exercise (including Calendar Spread Options) 0.00 0.075 0.075 1 London Cocoa and Euro Cocoa — futures exchange and clearing fee is £0.79, with £0.01 per lot per side being paid to support the Cocoa Research Association. 2 Block contract is only applicable to White Sugar Arbitrage, London Cocoa/Euro Cocoa Arbitrage and Robusta Coffee Arbitrage.