Wills--Deceased Residuary Legatee's Share Held Not to Pass by Way Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Spring 2014 Melanie Leslie – Trusts and Estates – Attack Outline 1

Spring 2014 Melanie Leslie – Trusts and Estates – Attack Outline Order of Operations (Will) • Problems with the will itself o Facts showing improper execution (signature, witnesses, statements, affidavits, etc.), other will challenges (Question call here is whether will should be admitted to probate) . Look out for disinherited people who have standing under the intestacy statute!! . Consider mechanisms to avoid will challenges (no contest, etc.) o Will challenges (AFTER you deal with problems in execution) . Capacity/undue influence/fraud o Attempts to reference external/unexecuted documents . Incorporation by reference . Facts of independent significance • Spot: Property/devise identified by a generic name – “all real property,” “all my stocks,” etc. • Problems with specific devises in the will o Ademption (no longer in estate) . Spot: Words of survivorship . Identity theory vs. UPC o Abatement (estate has insufficient assets) . Residuary general specific . Spot: Language opting out of the common law rule o Lapse . First! Is the devisee protected by the anti-lapse statute!?! . Opted out? Spot: Words of survivorship, etc. UPC vs. CL . If devise lapses (or doesn’t), careful about who it goes to • If saved, only one state goes to people in will of devisee, all others go to descendants • Careful if it is a class gift! Does not go to residuary unless whole class lapses • Other issues o Revocation – Express or implied? o Taxes – CL is pro rata, look for opt out, especially for big ticket things o Executor – Careful! Look out for undue -

Lost Wills: the Wisconsin Law, 60 Marq

Marquette Law Review Volume 60 Article 3 Issue 2 Winter 1977 Lost Wills: The iW sconsin Law Robert C. Burrell Jack A. Porter Follow this and additional works at: http://scholarship.law.marquette.edu/mulr Part of the Law Commons Repository Citation Robert C. Burrell and Jack A. Porter, Lost Wills: The Wisconsin Law, 60 Marq. L. Rev. 351 (1977). Available at: http://scholarship.law.marquette.edu/mulr/vol60/iss2/3 This Article is brought to you for free and open access by the Journals at Marquette Law Scholarly Commons. It has been accepted for inclusion in Marquette Law Review by an authorized administrator of Marquette Law Scholarly Commons. For more information, please contact [email protected]. LOST WILLS: THE WISCONSIN LAW ROBERT C. BURRELL* and JACK A. PORTER** I. INTRODUCTION The law of Wisconsin is well settled that once a will has been validly executed and has not been revoked, it may be admitted to probate even though the original copy of the will cannot be located at the death of the testator.1 Wisconsin Statutes section 856.17 provides as follows: Lost will, how proved. Whenever any will is lost, de- stroyed by accident or destroyed without the testator's con- sent the probate court has power to take proof of the execu- tion and validity of the will and to establish the same. The petition for the probate of the will shall set forth the provi- 2 sions thereof. Therefore, where the testator had a will which was valid at the time of execution but which cannot be located upon the death of the testator, the statute, in effect, prescribes the procedure for establishing that the will has not been subsequently re- voked by the testator. -

G L O S S a R Y

G L O S S A R Y A Administrator: A court appointed person or corporation in charge of managing the estate of a person who dies without leaving a will. Administrators have the same duties as Executors. In Minnesota, the administrator or executor is called the Personal Representative. Affiant: A person who makes an oath or affirmation and acknowledges the same in writing. In Minnesota this is usually done before a notary public. Affidavit: A voluntary written statement of facts confirmed by the oath or affirmation of the affiant. Affidavit of Collection of Personal Property: A sworn, notarized statement, used to collect assets of a small estate without going through the probate process. (aka Affidavit of a Small Estate). Agent: A person authorized by another to act for him. AKA: Also Known As (also lower case: aka). Amendment: A change or modification. See Codicil. Ancestor (an Ascendant): A deceased relative such as a parent or grandparent from whom one is descended. Ancillary Administration: A secondary administration in a state where the decedent owned property and which is not the state where the decedent was domiciled. Annuity: The right to receive fixed sums of money at regular intervals. Appoint: To designate and empower particular person(s) with authority to perform specified duties. Appraisal: An evaluation by disinterested and qualified persons as to the value of assets. Assets: All property of a person, corporation or estate of a decedent; real or personal, tangible or intangible. Attorney-in-fact: A person with the power granted under a power of attorney. B Beneficiary: An entity who benefits from the act of another. -

Uniform Probate Code Article Ii Intestacy, Wills, and Donative Transfers

UNIFORM PROBATE CODE ARTICLE II INTESTACY, WILLS, AND DONATIVE TRANSFERS [Sections to be Revised in Bold] Table of Sections PART 1 INTESTATE SUCCESSION § 2-101. Intestate Estate. § 2-102. Share of Spouse. § 2-102A. Share of Spouse. § 2-103. Share of Heirs Other Than Surviving Spouse. § 2-104. Requirement That Heir Survive Decedent for 120 Hours. § 2-105. No Taker. § 2-106. Representation. § 2-107. Kindred of Half Blood. § 2-108. Afterborn Heirs. § 2-109. Advancements. § 2-110. Debts to Decedent. § 2-111. Alienage. § 2-112. Dower and Curtesy Abolished. § 2-113. Individuals Related to Decedent Through Two Lines. § 2-114. Parent and Child Relationship. § 2-101. Intestate Estate. (a) Any part of a decedent’s estate not effectively disposed of by will passes by intestate succession to the decedent’s heirs as prescribed in this Code, except as modified by the decedent’s will. (b) A decedent by will may expressly exclude or limit the right of an individual or class to succeed to property of the decedent passing by intestate succession. If that individual or a member of that class survives the decedent, the share of the decedent’s intestate estate to which that individual or class would have succeeded passes as if that individual or each member of that class had disclaimed his [or her] intestate share. § 2-102. Share of Spouse. The intestate share of a decedent’s surviving spouse is: (1) the entire intestate estate if: (i) no descendant or parent of the decedent survives the decedent; or (ii) all of the decedent’s surviving descendants are also -

The Personal Representative's Power to Sell Realty in Virginia

William & Mary Law Review Volume 15 (1973-1974) Issue 4 Article 8 May 1974 The Personal Representative's Power to Sell Realty in Virginia Follow this and additional works at: https://scholarship.law.wm.edu/wmlr Part of the Estates and Trusts Commons Repository Citation The Personal Representative's Power to Sell Realty in Virginia, 15 Wm. & Mary L. Rev. 949 (1974), https://scholarship.law.wm.edu/wmlr/vol15/iss4/8 Copyright c 1974 by the authors. This article is brought to you by the William & Mary Law School Scholarship Repository. https://scholarship.law.wm.edu/wmlr COMMENT THE PERSONAL REPRESENTATIVE'S POWER TO SELL REALTY IN VIRGINIA At common law, tide to personal property passed to an executor or administrator upon the death of the owner, while tide to realty vested immediately in the decedent's heirs or devisees.' During the period of administration, the personal representative's control over personalty was, and under present law remains, analogous to that of a trustee, there being few restrictions upon the power to dispose of the property for the benefit of the estate. With respect to realty, however, a personal representative at common law had neither tide nor power to sell. Two general exceptions to the common law rules have evolved to expand the personal representative's power ovex realty. First, realty may be subjected by statute to the payment of debts of the estate when the personalty is insufficient for that purpose. Second, and more sig- nificantly, an executor may sell realty when vested with such power by the will.3 This Comment will examine the development and present status in Virginia of these exceptions to the general rule against sale 'of realty by a personal representative and will suggest statutory reforms designed to bring Virginia law more in line with that in other jurisdic- tions in reflecting modem conditions. -

Attorney and Client - Unauthorized Practice - Practice of Law by Corporations John T

Marquette Law Review Volume 21 Article 5 Issue 1 December 1936 Attorney and Client - Unauthorized Practice - Practice of Law by Corporations John T. McCarrier Follow this and additional works at: http://scholarship.law.marquette.edu/mulr Part of the Law Commons Repository Citation John T. McCarrier, Attorney and Client - Unauthorized Practice - Practice of Law by Corporations, 21 Marq. L. Rev. 55 (1936). Available at: http://scholarship.law.marquette.edu/mulr/vol21/iss1/5 This Article is brought to you for free and open access by the Journals at Marquette Law Scholarly Commons. It has been accepted for inclusion in Marquette Law Review by an authorized administrator of Marquette Law Scholarly Commons. For more information, please contact [email protected]. 1936] RECENT DECISIONS in the end would retain the amount received by them and the residuary legatee would not be relieved in the slightest. The result would be effected only if costs consumed the corpus of the residuary legatee's portion or if such legatee was bankrupt. The banking commission seems to have been fully satisfied on this score and hence its resolve to bring the action only against the residuary legatee is perfectly intel- ligible. Just why the court should not be satisfied with this arrange- ment which would do complete justice between the parties and save expense and trouble is difficult to understand in view of the two other cases above mentioned in which the liability was enforced against dis- tributees. In all three cases all that really happened was that property of the deceased stockholder came to the legatee subject to a lien for the superadded liability. -

The Intestate Claims of Heirs Excluded by Will: Should "Negative Wills" Be Enforced?

The Intestate Claims of Heirs Excluded by Will: Should "Negative Wills" Be Enforced? When a testator's will fails to provide for the disposition of his entire estate, the portion of the estate that is not disposed of usu- ally passes to the testator's heirs under the intestacy laws.' These laws reflect a presumption about what the testator would have wanted had he considered the matter.2 In some cases, however, the testator may have expressed a contrary intent. For example, a will may expressly disinherit an heir and leave the estate to someone else; or it may leave a small sum "and no more" to an heir, while giving the bulk of the estate to someone else; or a "will" may con- tain no devise at all, but express a desire that an heir receive no part of the estate.3 If the will does not fully dispose of the testa- tor's property and some or all of his estate must pass by intestacy, an issue arises as to whether the intestacy statute requires the ex- cluded heir to receive an intestate share, contrary to the testator's intent. This comment discusses the circumstances in which a will that expressly disinherits an heir or limits the heir's gift to the devise in the will (a "negative will") may foreclose the award of an intestate share to that heir where some or all of the testator's estate passes by intestacy. Since the mid-nineteenth century, English courts have enforced negative wills where (1) the testator clearly intended to exclude an heir or to limit an heir's share in the estate to the devise in the will, and (2) at least one other heir remains eligible to take the property that passes by intestacy.4 Under this approach, the exclusion of the heir (or limitation of the heir's gift) in the will See, e.g., UNIF. -

Conflicts of International Inheritance Laws in the Age of Multinational Lives Adam F

\\jciprod01\productn\C\CIN\52-4\CIN403.txt unknown Seq: 1 17-JUL-20 14:56 Conflicts of International Inheritance Laws in the Age of Multinational Lives Adam F. Streisand† & Lena G. Streisand‡ Introduction ..................................................... 675 R I. Ancient Rome ............................................ 678 R II. Historical Development of the Civil Law Tradition ........ 683 R III. Historical Development in the Common Law Nations ..... 687 R IV. The Islamic Model ....................................... 695 R V. Inheritance Laws in Russia ............................... 698 R VI. Modern Rules of Forced Heirship in Civil Law ............ 701 R VII. Common Law Freedoms of Testation ..................... 706 R VIII. Who Claims This Decedent? .............................. 709 R Conclusion ...................................................... 715 R Introduction Today, more than ever, we have multinational lives. That is to say, we may have more than one home or spend significant amounts of time in more than one country. There can be nothing more sublime than to immerse oneself in a foreign culture, converse in a different language than one’s own native tongue, and open the mind to ways of thinking that may even be anathema to the values instilled in us from our very first years. One can only benefit. But what if you were someone like Douglas Raines Tompkins, founder of The North Face and Esprit apparel companies, and adventurist-turned- philanthropist? When Tompkins sold his companies, which he founded in San Francisco, California, where he lived most of his life, he committed to donating his entire wealth to land conservation and wildlife preservation.1 Tompkins acquired millions of acres of land in Chile and Argentina and made grand bargains with the governments of those nations: he offered to donate his land to the governments as long as they too contributed land, and agreed to dedicate the entirety of those lands for national parks and wildlife preserves. -

CHINA and the UNITED STATES: YIN and YANK INTESTACY Andrew Watson Brown

Masthead Logo Santa Clara Law Review Volume 59 | Number 1 Article 7 4-7-2019 CHINA AND THE UNITED STATES: YIN AND YANK INTESTACY Andrew Watson Brown Follow this and additional works at: https://digitalcommons.law.scu.edu/lawreview Part of the Law Commons Recommended Citation Andrew Watson Brown, Case Note, CHINA AND THE UNITED STATES: YIN AND YANK INTESTACY, 59 Santa Clara L. Rev. 239 (2019). Available at: https://digitalcommons.law.scu.edu/lawreview/vol59/iss1/7 This Case Note is brought to you for free and open access by the Journals at Santa Clara Law Digital Commons. It has been accepted for inclusion in Santa Clara Law Review by an authorized editor of Santa Clara Law Digital Commons. For more information, please contact [email protected], [email protected]. 7_BROWN FINAL.DOCX (DO NOT DELETE) 4/6/2019 5:19 PM CHINA AND THE UNITED STATES: YIN AND YANK INTESTACY Andrew Watson Brown* TABLE OF CONTENTS I. Introduction ..................................................................................... 240 II. Background .................................................................................... 241 III. Testamentary Freedom or Support? ............................................. 242 A. American Inheritance Model .............................................. 242 B. The Family Paradigm .......................................................... 243 1. Wrinkles in the Family Paradigm ................................. 245 a. Capacity .................................................................. 245 b. Anti-Lapse Statutes -

Chapter 5 Managing Incapacity

1 CHAPTER 5 MANAGING INCAPACITY 5.1 INTRODUCTION As nature and human affairs change the human condition over time, each individual struggles to maintain the greatest amount of control over life. This strug- gle is tempered by the fragility of the human body and mind. As Sophocles observed in Oepidus Rex: Let every man in mankind’s frailty Consider his last day; and let none Presume on his good fortune until he find Life, at his death, a memory without pain. The ability to make one’s own decisions about family, property, social and business affairs, health care, and testamentary dispositions can be destroyed or severely impaired by the ravages of disease and injury. Society strives through tradi- tion and laws to give the individual suffering from these afflictions the greatest possible control over life’s affairs, and ultimately, one’s final wishes as to death. This chapter addresses the legal structures for managing and responding to the possibility that diseases and injuries of the mind and body will win the war over the individual’s autonomy. The legal bulwarks of protection against incapacity are primarily the power of attorney and the advance medical directive. The former safe- guards a person’s decisions regarding business, financial, and property transactions and the latter preserves authority over one’s affairs of life, health care, and death. 5.2 THE EVALUATION PROCESS 5.201 In General. It is to be expected that many of an elder law attorney’s clients will have some degree of age-related cognitive impairment.1 An informal evaluation of the mental capacity of every elderly client is therefore prudent. -

Wills and Trusts (4Thed

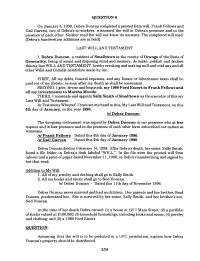

QUESTION 6 On January 5, 1990, Debra Duncan completed a printed form will. Frank Fellows and Gail Garven, two of Debra's co-workers, witnessed the will in Debra's presence and in the presence of each other. Neither read the will nor knew its contents. The completed will read: [Debra's handwritten additions are in bold] LAST WILL AND TESTAMENT I, Debra Duncan, a resident of Smalltown in the county of Orange of the State of Generality, being of sound and dsposing mind and memory, do make, publish and declare this my last WILL AND TESTAMENT, hereby revoking and making null and void any and all other Wills and Codicils heretofore made by me. FIRST, All my debts, funeral expenses, and any Estate or Inheritance taxes shall be paid out of my Estate, as soon after my death as shall be convenient. SECOND, I give, devise and bequeath, my 1989 Ford Escort to Frank Fellows and all my investments to Martha Murdo. THIRD, I nominate and appoint Sally Smith of Smalltown as the executor of this my Last Wlll and Testament. In Testimony Whereof, I have set my hand to this, My Last Will andTestarnent, on this 5th day of January, in the year 1990. IS/ Debra Duncan The foregoing instrument was signed by Debra Duncan in our presence who at her request and in her presence and in the presence of each other have subscribed our names as witnesses. Is/ Frank Fellows Dated this 5th day of January 1990. Is1 Gail Garven Dated this 5th day of January 1990. -

TAXATION of INCOME of DECEDENTS George Craven T

1953] TAXATION OF INCOME OF DECEDENTS George Craven t The federal income tax statute dealing with income in respect of decedents 1 has been in force for eleven years, and during that period the courts have solved many of the income tax problems arising under that statute as well as companion problems arising under the estate tax statute. As an aid to understanding the purpose and meaning of the income tax statute, it is helpful to review the considerations which gave rise to its enactment. TREATMENT PRIOR TO 1942 OF INCOME ACCRUED AT DEATH Prior to the Revenue Act of 1934, if an individual filed his fed- eral income tax returns on a cash basis, income which had accrued to him but was uncollected at the time of his death was not taxable to the decedent, because it had not been received by him. It was subject to estate tax as an asset of his estate, and it was held to be corpus and not income to the estate and therefore not subject to income tax to the estate2 The result was that the income escaped income tax entirely. The Revenue Act of 1934 provided for the first time for including in the final return of a cash basis decedent amounts of income accrued but uncollected at the time of death.' Similarly, that Act allowed as deductions in such decedent's final income tax return items other- wise deductible which had accrued but were unpaid at the time of his death.4 Those provisions remained in force until the enactment of the Revenue Act of 1942.