Saskatchewan Municipal Board Assessment Appeals Committee

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Gazette Part I, March 29, 2018

THIS ISSUE HAS NO PART III THE SASKATCHEWAN GAZETTE, 2 FÉVRIER 2018 609 (REGULATIONS)/CE NUMÉRO NE CONTIENT PAS DE PARTIE III (RÈGLEMENTS) The Saskatchewan Gazette PUBLISHED WEEKLY BY AUTHORITY OF THE QUEEN’S PRINTER/PUBLIÉE CHAQUE SEMAINE SOUS L’AUTORITÉ DE L’IMPRIMEUR DE LA REINE PART I/PARTIE I Volume 114 REGINA, THURSDAY, MARCH 29, 2018/REGINA, JEUDI 29 MARS 2018 No. 13/nº13 TABLE OF CONTENTS/TABLE DES MATIÈRES PART I/PARTIE I SPECIAL DAYS/JOURS SPÉCIAUX ................................................................................................................................................. 610 PROGRESS OF BILLS/RAPPORT SUR L’ÉTAT DES PROJETS DE LOI (Second Session, Twenty-Eighth Legislative Assembly/Deuxième session, 28e Assemblée législative) .......................................... 610 ACTS NOT YET PROCLAIMED/LOIS NON ENCORE PROCLAMÉES ..................................................................................... 612 ACTS IN FORCE ON ASSENT/LOIS ENTRANT EN VIGUEUR SUR SANCTION (Second Session, Twenty-Eighth Legislative Assembly/Deuxième session, 28e Assemblée législative) .......................................... 615 ACTS IN FORCE ON SPECIFIC EVENTS/LOIS ENTRANT EN VIGUEUR À DES OCCURRENCES PARTICULIÈRES..... 615 ACTS PROCLAIMED/LOIS PROCLAMÉES (2018) ........................................................................................................................ 616 CORPORATE REGISTRY NOTICES/AVIS DU REGISTRE DES SOCIÉTÉS .......................................................................... 616 The -

Bylaw No. 3 – 08

BYLAW NO. 3 – 08 A bylaw of The Urban Municipal Administrators’ Association of Saskatchewan to amend Bylaw No. 1-00 which provides authority for the operation of the Association under the authority of The Urban Municipal Administrators Act. The Association in open meeting at its Annual Convention enacts as follows: 1) Article V. Divisions Section 22 is amended to read as follows: Subsection (a) DIVISION ONE(1) Cities: Estevan, Moose Jaw, Regina and Weyburn Towns: Alameda, Arcola, Assiniboia, Balgonie, Bengough, Bienfait, Broadview, Carlyle, Carnduff, Coronach, Fleming, Francis, Grenfell, Indian Head, Kipling, Lampman, Midale, Milestone, Moosomin, Ogema, Oxbow, Pilot Butte, Qu’Appelle, Radville, Redvers, Rocanville, Rockglen, Rouleau, Sintaluta, Stoughton, Wapella, Wawota, White City, Whitewood, Willow Bunch, Wolseley, Yellow Grass. Villages: Alida, Antler, Avonlea, Belle Plaine, Briercrest, Carievale, Ceylon, Creelman, Drinkwater, Fairlight, Fillmore, Forget, Frobisher, Gainsborough, Gladmar, Glenavon, Glen Ewen, Goodwater, Grand Coulee, Halbrite, Heward, Kendal, Kennedy, Kenosee Lake, Kisbey, Lake Alma, Lang, McLean, McTaggart, Macoun, Manor, Maryfield, Minton, Montmarte, North Portal, Odessa, Osage, Pangman, Pense, Roch Percee, Sedley, South Lake, Storthoaks, Sun Valley, Torquay, Tribune, Vibank, Welwyn, Wilcox, Windthorst. DIVISION TWO(2) Cities: Swift Current Towns: Burstall, Cabri, Eastend, Gravelbourg, Gull Lake, Herbert, Kyle, Lafleche, Leader, Maple Creek, Morse, Mossbank, Ponteix, Shaunavon. Villages: Abbey, Aneroid, Bracken, -

The Capacity Edition

1 PARCS UPDATE #35 THE CAPACITY JUNE, 2013 EDITION 1. PROVINCE CLAMPING DOWN ON NEW COTTAGE COMMUNITIES The province is about to introduce changes to The Municipalities Act which will severely reduce, if not eliminate, the establishment of new Organized Hamlets or new Resort Villages in the Saskatchewan. The rationale for raising the bar for the establishment of new cottage In this issue communities is the assertion that many of our current communities do not have the CAPACITY to operate 1. Province clamping down . p. 1 effectively. 2. PARCS meets Ministry . p. 1 CAPACITY is the buzz word of the day. It refers to 3. What’s being proposed . p. 2 the ability of a community “to meet the 4. What’s your capacity? . p. 3 accountability, fiduciary and legislative requirements 5. More about PARCS lobby . P. 4 to operate independently and to generate sufficient More about PARCS survey . p. 4 revenue for services and administration”. 1 On page 3 of this issue, PARCS presents a summary of some of 6. Addendum - Villages the criteria the province uses to determine capacity. & resort villages today . p. 5, 6 2. PARCS DIRECTORS MEETS WITH MINISTRY OF GOVERNMENT AFFAIRS On May 28, a delegation from the PARCS Board of Directors met with officials from the Ministry of Government Relations to provide input into the proposed changes to the rules for forming new resort villages and new organized hamlets. 2 PARCS delegates acknowledged that many of our smaller resort villages are struggling due to lack of capacity to meet their obligations (see page 3). -

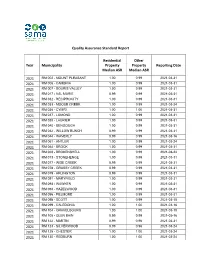

2021 Quality Assurance Standards Aggregate Report Apr. 1, 2021

Quality Assurance Standard Report Residential Other Year Municipality Property Property Reporting Date Median ASR Median ASR 2021 RM 002 - MOUNT PLEASANT 1.00 0.99 2021-03-31 2021 RM 006 - CAMBRIA 1.00 0.99 2021-03-31 2021 RM 007 - SOURIS VALLEY 1.00 0.99 2021-03-31 2021 RM 017 - VAL MARIE 0.99 0.99 2021-03-31 2021 RM 032 - RECIPROCITY 1.00 0.99 2021-03-31 2021 RM 033 - MOOSE CREEK 1.00 0.99 2021-03-24 2021 RM 036 - CYMRI 1.00 1.00 2021-03-31 2021 RM 037 - LOMOND 1.00 0.99 2021-03-31 2021 RM 038 - LAURIER 1.00 0.99 2021-03-31 2021 RM 040 - BENGOUGH 1.00 0.99 2021-03-31 2021 RM 042 - WILLOW BUNCH 0.99 0.99 2021-03-31 2021 RM 044 - WAVERLY 0.99 0.99 2021-03-16 2021 RM 061 - ANTLER 1.00 0.99 2021-03-24 2021 RM 064 - BROCK 1.00 0.99 2021-03-31 2021 RM 068 - BROKENSHELL 1.00 0.99 2021-03-24 2021 RM 073 - STONEHENGE 1.00 0.99 2021-03-31 2021 RM 077 - WISE CREEK 0.99 0.99 2021-03-31 2021 RM 078 - GRASSY CREEK 0.99 0.99 2021-03-31 2021 RM 079 - ARLINGTON 0.99 0.99 2021-03-31 2021 RM 091 - MARYFIELD 1.00 0.99 2021-03-31 2021 RM 093 - WAWKEN 1.00 0.99 2021-03-31 2021 RM 094 - HAZELWOOD 1.00 0.99 2021-03-31 2021 RM 096 - FILLMORE 1.00 0.99 2021-03-31 2021 RM 098 - SCOTT 1.00 0.99 2021-03-10 2021 RM 099 - CALEDONIA 1.00 1.00 2021-03-16 2021 RM 104 - GRAVELBOURG 1.00 1.00 2021-03-10 2021 RM 105 - GLEN BAIN 0.99 0.99 2021-03-16 2021 RM 122 - MARTIN 0.99 0.96 2021-03-31 2021 RM 123 - SILVERWOOD 0.99 0.96 2021-03-24 2021 RM 125 - CHESTER 1.00 1.00 2021-03-24 2021 RM 130 - REDBURN 1.00 1.00 2021-03-24 Residential Other Year Municipality Property Property -

Sask Gazette, Part I, Mar 24, 1995

MARCH 24, 1995 277 THIS ISSUE HAS NO PART II (REVISED REGULATIONS) OR PART III (REGULATIONS) The Saskatchewan Gazette PUBLISHED WEEKLY BY AUTHORITY OF THE QUEEN’S PRINTER PART I Volume 91 REGINA, FRIDAY, MARCH 24, 1995 No. 12 TABLE OF CONTENTS PART I APPOINTMENT................................................................................................................... 278 PROGRESS OF BILLS ....................................................................................................... 278 ACTS PROCLAIMED.......................................................................................................... 278 MINISTER’S ORDERS ....................................................................................................... 279 The Oil and Gas Conservation Act ........................................................................................ 279 CORPORATIONS BRANCH NOTICES .......................................................................... 281 The Business Corporations Act .............................................................................................. 281 The Business Names Registration Act................................................................................... 283 The Non-profit Corporations Act ........................................................................................... 286 PUBLIC NOTICES .............................................................................................................. 286 The Agricultural Implements Act ......................................................................................... -

SK COMMUNITY WATER USE RECORDS 1996 to 2010

SASKATCHEWAN COMMUNITY WATER USE RECORDS 1996 to 2010 REPORT NO. 24 PREPARED AND SUBMITTED BY: SASKATCHEWAN WATERSHED AUTHORITY INTEGRATED WATER SERVICES DIVISION 111 FAIRFORD STREET EAST MOOSE JAW SASKATCHEWAN S6H 7X9 October 2011 Disclaimer Notice The data presented is provided by the various communities listed in this report. While every effort is made to ensure that the content of this report is accurate, the report is provided “as is” and Saskatchewan Watershed Authority makes no representations or warranties in relation to the accuracy or completeness of the information found on it. Nothing in this report should be taken to constitute professional advice or a formal recommendation and we exclude all representations and warranties relating to the content and use of this report. In no event will Saskatchewan Watershed Authority be liable for any direct or incidental, indirect, consequential or special damages of any kind, or any damages whatsoever, including, without limitation, those resulting from loss of profit, loss of contracts, goodwill, data, information, income, anticipated savings or business relationships, whether or not advised of the possibility of such damage, arising out of or in connection with the use of this report. Please check Disclaimer Notice on Title Page (first page of report) INTRODUCTION This document reflects water consumption data for the majority of Saskatchewan municipalities from 1996 to 2010. The information contains Saskatchewan Ministry of Health population statistics, monthly, yearly, average day, peak day and per capita water consumption as well as peak day factors. For 2010, the Saskatchewan Watershed Authority obtained water consumption records from approximately 604 communities including 33 Provincial and Regional Parks and campgrounds and 74 First Nations. -

Saskatchewan Official Road

PRINCE ALBERT MELFORT MEADOW LAKE Population MEADOW LAKE PROVINCIAL PARK Population 35,926 Population 40 km 5,992 5,344 Prince Albert Visitor Information Centre Visitor Information 4 3700 - 2nd Avenue West Prince Albert National Park / Waskesieu Nipawin 142 km Northern Lights Palace Meadow Lake Tourist Information Centre Phone: 306-682-0094 La Ronge 88 km Choiceland and Hanson Lake Road Open seasonally 110 Mcleod Avenue W 79 km Hwy 4 and 9th Ave W GREEN LAKE 239 km 55 Phone: 306-752-7200 Phone: 306-236-4447 ve E 49 km Flin Flon t A Chamber of Commerce 6 RCMP 1s 425 km Open year-round 2nd Ave W 3700 - 2nd Avenue West t r S P.O. Phone: 306-764-6222 3 e iv M e R 5th Ave W r e Prince Albert . t Open year-round e l e n c f E v o W ru e t p 95 km r A 7th Ave W t S C S t y S d Airport 3 Km 9th Ave W H a 5 r w 3 Little Red 55 d ? R North Battleford T River Park a Meadow Lake C CANAM o Radio Stations: r HIGHWAY Lions Regional Park 208 km 15th St. N.W. 15th St. N.E. Veteran’s Way B McDonald Ave. C CJNS-Q98-FM e RCMP v 3 Mall r 55 . A e 3 e Meadow Lake h h v RCMP ek t St. t 5 km Northern 5 A Golf Club 8 AN P W Lights H ark . E Airport e e H Ave. -

THE SASKATCHEWAN GAZETTE, March 22, 2013 565 (REGULATIONS)/CE NUMÉRO NE CONTIENT PAS DE PARTIE III (RÈGLEMENTS)

THIS ISSUE HAS NO PART III THE SASKATCHEWAN GAZETTE, MARCH 22, 2013 565 (REGULATIONS)/CE NUMÉRO NE CONTIENT PAS DE PARTIE III (RÈGLEMENTS) The Saskatchewan Gazette PUBLISHED WEEKLY BY AUTHORITY OF THE QUEEN’S PRINTER/PUBLIÉE CHAQUE SEMAINE SOUS L’AUTORITÉ DE L’ImPRIMEUR DE LA REINE PART I/PARTIE I Volume 109 REGINA, FRiday, MARCH 22, 2013/REGINA, VENDREDI, 22 MARS 2013 No. 12/nº 12 TABLE OF CONTENTS/TABLE DES MATIÈRES PART I/PARTIE I APPOINTMENT/NOMINATION ........................................................................................................................................................ 566 PROGRESS OF BILLS/RAPPORT SUR L’éTAT DES PROJETS DE LOI (Second Session, Twenty-Seventh Legislative Assembly/Deuxième session, 27e Assemblée législative) ........................................ 566 ACTS NOT YET PROCLAIMED/LOIS NON ENCORE PROCLAMÉES ..................................................................................... 567 ACTS IN FORCE ON ASSENT/LOIS ENTRANT EN VIGUEUR SUR SANCTION (Second Session, Twenty-Seventh Legislative Assembly/Deuxième session, 27e Assemblée législative) ........................................ 570 ACTS IN FORCE ON SPECIFIC EVENTS/LOIS ENTRANT EN VIGUEUR À DES OCCURRENCES PARTICULIÈRES..... 571 ACTS PROCLAIMED/LOIS PROCLAMÉES (2013) ........................................................................................................................ 571 CORPORATE REGISTRY NOTICES/AVIS DU REGISTRE DES SOCIÉTÉS .......................................................................... 572 -

EXPRESSION of INTEREST (Artist Proposal)

EXPRESSION OF INTEREST (Artist Proposal) Prepared for: City of Prince Albert Arts and Culture Call for Artist Concept 2nd Avenue Art Installation c/o City of Prince Albert, Purchasing Department Municipal Service Centre 11 – 38th Street East Prince Albert, SK S6W 1A5 E: [email protected] Prepared By: Joanne Churko 914 Broad Street North Regina, SK S4R 5Z1 P: 306-359-7886 Email: [email protected] [email protected] Thank you for creating this artistic creative design opportunity. I am excited to participate in the bid process for this competition. Please accept the following as an application/expression of interest for: City of Prince Albert Call For Artist Concept - 2nd Avenue Art Installation Prince Albert, SK as advertised. Deadline: Wednesday April 21, 2021 2:30p.m. 1 2 1.0 Expression of Interest 1.1 Project Description & Summary Public art has the ability to inspire, engage and connect people in extraordinary ways. The City of Prince Albert supports an Art and Culture program and policies that allow artists of all mediums, skill types and abilities to develop their crafts and create works that are truly inspiring. This particular opportunity is of interest because it aligns with my skillset as a multi-medium artist and combines my technical expertise as a multi-disciplined and creative designer and technical consultant of more than thirty years, into one single scope of work. This expression of interest proposes to design, develop, construct and install a collection of five (5) double-sided, open-faced, artistic fence panels (in duplicate), similar to the five concepts shown herein. -

RPT 21-250 That the Community Services Advisory Committee

RPT 21-250 TITLE: Beautification of City Entrance Ways DATE: May 13, 2021 TO: Community Services Advisory Committee PUBLIC: X INCAMERA: RECOMMENDATION: That the Community Services Advisory Committee approve the 2021 Focus Areas for Beautification identified by the Community Services Department and forward the recommendation to Council for consideration. TOPIC AND PURPOSE To provide background on the beautification process, the accomplishments in 2019 & 2020, and the suggested plan moving into 2021 related to the topic of beautification of the City Entrance Ways. BACKGROUND The following resolution was approved during the 2021 Budget Committee Regular meeting. “That the total 2021 Operating Budget for the City Beautification Functional Area be approved at a cost of $75,800, as presented.” PROPOSED APPROACH AND RATIONALE: Beginning with the 2019 Season, Community Services has been tasked with looking at implementing various beautification initiatives including how to best use the funds allocated in the annual budget to plan the beautification process. Preliminary discussions have taken place around the Development of a Comprehensive Plan involving various City Departments as it relates to general maintenance, signage, landscaping and promotion. Community RPT 21-250 Page 2 of 10 beautification should be considered a high priority, specifically highway entrances, as they are the first contact that residents and visitors have, creating that first impression of the City. When we talk about beautification, the immediate thought was to look at the addition of landscaping which would include flowerbeds to brighten the entryways. Suggestions were brought forth to look at designing options to communicate to the public providing an opportunity for input into a Comprehensive Plan. -

Saskatchewan Tire Collection Zones

Legend Saskatchewan 0255075 Tire Zones First Nation Reserve Highway Kilometres Tire Collection Zones Urban Municipality Park R.M. Water Creation Date 01/13/2018 Version 1.0 Mahigan UV165 Oskikebuk Lake MISTIK 184 106 Lake 203 UV Map 1 of 1 WASKWAYNIKAPIK Lake Vance 228 Wildfong Annabel 919 Dore Lake Bryans Lake UV Casat 911 Lake UVViney Lake Lake Lake Lake NAKISKATOWANEEK 227 Neagle FLIN FLON 165 Lake UV CREIGHTON Flotten UV903 Sarginson MCKAY IM Lake Lake 209 PISIWIMINIWAT Hanson Smoothstone 207 Lake Lake Deschambault NARE BEACH DORE 106 DE Waterhen LAK 912 MUSKWAMINIWATIM Lake UV E UV Chisholm Spectral 924 Limestone Shuttleworth UV 225 Lake UV2 Lake Lake Lake McNally Lake W ATERHEN UV969 AMISK Lake Hollingdale 130 Stringer LAKE M Beaupre 916 Lake EADOW UV Lake 184 BI LA Lake Molanosa Cobb Kerr G KE GREIG L 167 IS AKE UV 21 LAND PROVINCIA UV155 Lake Lake Hobbs Lake Amisk UV G L SO OO UT PIE DSOIL H Sled Clarke Lake Lake Nepe RCELA PAR WATERH GLADUE Edgelow ND K EN Lake Lake Oatway Balsam Lake LAKE LAKE Lake Meeyomoot Shallow Renown Lake Lake Maraiche 105 SLED Lake UV55 Nipekamew Lake Lake Lake DORIN L Lake Saskoba 622 TOSH AKE Lake WEYAKWIN Big Sandy Harrington AMISKOSAKAHIKAN Wanner Lake Narrow Herman Lake 210 Lake Lake Goulden Lake Lake UV924 East Trout Saunders GRE Lake Lake Suggi Windy EN Montre 26 4 al 927 UV106 Lake Lake UV UV LAK Lake UV Little Bear E Lake Leonard STURGEON WEIR Marquis Lake 184 Lake Red Bobs T 55 CLARENCE-STEEPBANK Waterfall HUNDERCHILD FLYING DUST UV Lake O'Leary Lake 115 UV55 105 LAKES PROVINCIAL PARK Lake Namew -

Saskatchewan Population Report 2016 Census of Canada

Saskatchewan Population Report 2016 Census of Canada 2016 CENSUS POPULATION Saskatchewan’s Census population for 2016 Villages and Resort Villages accounted for was 1,098,352, according to Statistics Canada. This represents an increase of 64,971 persons 47,308 persons in 2016. This is an increase of 228 persons (0.5 percent) from the 2011 village (6.3 percent) from the 2011 Census population of 1,033,381. and resort village population of 47,080. These people live in a total of 21,159 dwellings. Table 1 shows the Census population counts Indian Reserves also decreased in population and growth rates for Saskatchewan for the past between 2011 and 2016. Reserve population 55 years. fell by 172 persons (0.3 percent) to 56,050 in 2016 from 56,222 in 2011. These people live in Table 1: Census Population, 1961 - 2016 a total of 13,995 dwellings. Saskatchewan Rural Municipality population increased by Date Census Population Growth Rate 1,934 to 176,535 persons in 2016 from 174,601 1961 925,181 5.1% persons in 2011. This represents an increase of 1966 955,344 3.3% 1.1 percent. These people live in a total of 1971 926,242 -3.0% 65,770 dwellings. 1976 921,323 -0.5% 1981 968,313 5.1% Northern Villages, Hamlets, Crown Colonies, 1986 1,009,613 4.3% Unorganized and other populations fell 1,201 1991 988,928 -2.0% persons between 2011 and 2016 from 14,630 1996 990,237 0.1% persons to 13,429 persons. These people live in 2001 978,933 -1.1% a total of 4,183 dwellings.