Global Finance Announces the Winners' Circle a Ranking of the Top

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

18 February 2019 Solvency and Diversification in Insurance Remain Key Strengths Despite Change in Structure

FINANCIAL INSTITUTIONS ISSUER IN-DEPTH Lloyds Banking Group plc 18 February 2019 Solvency and diversification in insurance remain key strengths despite change in structure Summary RATINGS In 2018, Lloyds Banking Group plc (LBG) altered its structure to comply with the UK's ring- Lloyds Banking Group plc Baseline Credit a3 fencing legislation, which requires large banks to separate their retail and SME operations, Assessment (BCA) and deposit taking in the European Economic Area (EEA) from their other activities, including Senior unsecured A3 Stable the riskier capital markets and trading business. As part of the change, LBG designated Lloyds Bank plc as the“ring-fenced” entity housing its retail, SME and corporate banking operations. Lloyds Bank plc It also assumed direct ownership of insurer Scottish Widows Limited, previously a subsidiary Baseline Credit A3 Assessment (BCA) of Lloyds Bank. The changes had little impact on the creditworthiness of LBG and Lloyds Adjusted BCA A3 Bank, leading us to affirm the deposit and senior unsecured ratings of both entities. Scottish Deposits Aa3 Stable/Prime-1 Widows' ratings were unaffected. Senior unsecured Aa3 Stable » LBG's reorganisation was less complex than that of most UK peers. The Lloyds Lloyds Bank Corporate Markets plc Banking Group is predominantly focused on retail and corporate banking, and the Baseline Credit baa3 required structural changes were therefore relatively minor. The group created a small Assessment (BCA) separate legal entity, Lloyds Bank Corporate Markets plc (LBCM), to manage its limited Adjusted BCA baa1 Deposits A1 Stable/Prime-1 capital markets and trading operations, and it transferred its offshore subsidiary, Lloyds Issuer rating A1 Stable Bank International Limited (LBIL), to LBCM from Lloyds Bank. -

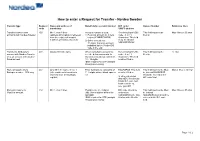

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Banks List (May 2011)

LIST OF BANKS AS COMPILED BY THE FSA ON 31 MAY 2011 This list of banks is intended to be used solely as a guide. The FSA does not warrant, nor accept any responsibility for the accuracy or completeness of the list or for any loss which may arise from reliance by any person on information in the list. (Amendments to the List of Banks since 30 April 2011 can be found on page 6) Banks incorporated in the United Kingdom Abbey National Treasury Services plc DB UK Bank Limited ABC International Bank plc Dunbar Bank plc Access Bank UK Limited, The Duncan Lawrie Ltd Adam & Company plc Ahli United Bank (UK) plc EFG Private Bank Ltd Airdrie Savings Bank Egg Banking plc Aldermore Bank Plc European Islamic Investment Bank Plc Alliance & Leicester plc Europe Arab Bank Plc Alliance Trust Savings Ltd Allied Bank Philippines (UK) plc FBN Bank (UK) Ltd Allied Irish Bank (GB)/First Trust Bank - (AIB Group (UK) plc) FCE Bank plc Alpha Bank London Ltd FIBI Bank (UK) plc AMC Bank Ltd Anglo-Romanian Bank Ltd Gatehouse Bank plc Ansbacher & Co Ltd Ghana International Bank plc ANZ Bank (Europe) Ltd Goldman Sachs International Bank Arbuthnot Latham & Co, Ltd Guaranty Trust Bank (UK) Limited Gulf International Bank (UK) Ltd Banc of America Securities Ltd Bank Leumi (UK) plc Habib Allied International Bank plc Bank Mandiri (Europe) Ltd Habibsons Bank Ltd Bank of Beirut (UK) Ltd Hampshire Trust plc Bank of Ceylon (UK) Ltd Harrods Bank Ltd Bank of China (UK) Limited Havin Bank Ltd Bank of Ireland (UK) Plc HFC Bank Ltd Bank of London and The Middle East plc HSBC Bank -

Chronology, 1963–89

Chronology, 1963–89 This chronology covers key political and economic developments in the quarter century that saw the transformation of the Euromarkets into the world’s foremost financial markets. It also identifies milestones in the evolu- tion of Orion; transactions mentioned are those which were the first or the largest of their type or otherwise noteworthy. The tables and graphs present key financial and economic data of the era. Details of Orion’s financial his- tory are to be found in Appendix IV. Abbreviations: Chase (Chase Manhattan Bank), Royal (Royal Bank of Canada), NatPro (National Provincial Bank), Westminster (Westminster Bank), NatWest (National Westminster Bank), WestLB (Westdeutsche Landesbank Girozentrale), Mitsubishi (Mitsubishi Bank) and Orion (for Orion Bank, Orion Termbank, Orion Royal Bank and subsidiaries). Under Orion financings: ‘loans’ are syndicated loans, NIFs, RUFs etc.; ‘bonds’ are public issues, private placements, FRNs, FRCDs and other secu- rities, lead managed, co-managed, managed or advised by Orion. New loan transactions and new bond transactions are intended to show the range of Orion’s client base and refer to clients not previously mentioned. The word ‘subsequently’ in brackets indicates subsequent transactions of the same type and for the same client. Transaction amounts expressed in US dollars some- times include non-dollar transactions, converted at the prevailing rates of exchange. 1963 Global events Feb Canadian Conservative government falls. Apr Lester Pearson Premier. Mar China and Pakistan settle border dispute. May Jomo Kenyatta Premier of Kenya. Organization of African Unity formed, after widespread decolonization. Jun Election of Pope Paul VI. Aug Test Ban Take Your Partners Treaty. -

Hsbc to Acquire Lloyds Banking Group Onshore Assets in the Uae

Ab c 29 March 2012 HSBC TO ACQUIRE LLOYDS BANKING GROUP ONSHORE ASSETS IN THE UAE HSBC Bank Middle East Ltd (‘HSBC’), an indirect wholly-owned subsidiary of HSBC Holdings plc, has entered into an agreement to acquire the onshore retail and commercial banking business of Lloyds Banking Group (‘Lloyds’) in the United Arab Emirates (‘UAE’). The value of the gross assets being acquired is US$769m as at 31 December 2011. The transaction, which is subject to regulatory approvals, is expected to complete in 2012. HSBC’s largest operations in the MENA region are based in the UAE where HSBC enjoys a market-leading trade and commercial banking presence, in addition to the largest international retail banking and wealth management business. The business being acquired from Lloyds has approximately 8,800 personal and commercial customers and a loan book of approximately US$573m as at 31 December 2011. Commenting on the acquisition, Simon Cooper, Deputy Chairman and Chief Executive Officer of HSBC in MENA, said: “HSBC is the leading international bank in the UAE and the addition of Lloyds’ strong presence in retail and commercial banking is highly complementary to our business. The acquisition underscores the strategic importance of the UAE, and of the MENA region as a whole, to HSBC.” Media enquiries to: Tim Harrison + 971 4 4235632 [email protected] Brendan McNamara +44 (0) 20 7991 0655 [email protected] ends/more Registered Office and Group Head Office: This news release is issued by 8 Canada Square, London E14 5HQ, United Kingdom Web: www.hsbc.com HSBC Holdings plc Incorporated in England with limited liability. -

World Bank Document

CONFIDENTIAL FOR RESTRICTED USE ONLY (NOT FOR USE BY THIRD PARTIES) Public Disclosure Authorized BOLIVIA FINANCIAL SECTOR NOTES Public Disclosure Authorized ASSESSING THE SECTOR’S POTENTIAL ROLE IN FOSTERING RURAL DEVELOPMENT AND GROWTH OF THE PRODUCTIVE SECTORS DECEMBER 2011 Public Disclosure Authorized THE WORLD BANK FINANCIAL AND PRIVATE SECTOR DEVELOPMENT VICE PRESIDENCY Public Disclosure Authorized LATIN AMERICA AND CARIBBEAN REGIONAL VICE PRESIDENCY i Table of Contents Executive Summary ...................................................................................................................................... 1 Chapter 1 Introduction ......................................................................................................................... 12 Chapter 2 Composition and depth of the financial system ................................................................... 15 2.1 A brief overview over the core players ....................................................................................... 15 2.2 Financial depth and level of financial inclusion – an international comparison ......................... 17 Chapter 3 Competition and financial soundness of the financial system ............................................. 25 3.1 Concentration and competition ................................................................................................... 25 3.2 Selected financial soundness indicators and potential vulnerabilities ........................................ 27 Chapter 4 The regulatory and supervisory -

Microcapital Monitor the CANDID VOICE for MICROFINANCE INVESTMENT

SEPTEMBER 2008 | VOLUME.3 ISSUE.9 MicroCapital Monitor THE CANDID VOICE FOR MICROFINANCE INVESTMENT MICROCAPITAL BRIEFS | TOP STORIES Peru’s Mibanco to Issue IPO, Aiming to Raise $15.5m INSIDE Page Shareholders of Peruvian microfinance lender Mibanco have agreed to raise up to the MicroCapital Briefs 2 equivalent of USD 15.5 million via an IPO, according to a regulatory report. Mibanco holds Microfinance news USD 740 million in assets and equity worth USD 70 million. September 22. 2008 Market Indicators 8 Dutch SNS Fundraising for Second Institutional Microfinance Fund Courtesy of the MIX SNS Asset Management (SAM) is reportedly fundraising for a successor to the SNS Institutional Microfinance Fund. The new fund, targeted at USD 140 million, was created in Upcoming Events 9 response to high demand from Dutch institutional investors. Run by Developing World Markets, it will invest 70 percent in microfinance institution debt and 30 percent in equity. Industry conferences Holding USD 28 billion in assets, SAM is a subsidiary of Dutch banking and insurance company SNS REAAL. The original SNS Institutional Microfinance Fund was the Pioneers in Microfinance company’s first fund dedicated to microfinance. September 8. 2008 Will return in October Nigerian Microfinance Banks to Set Up Interbank Market Paper Wrap-ups 10 Twenty-four microfinance banks and five discount houses in Nigeria are reportedly Latest research and reports establishing an interbank money market for the sub-sector. Such a market would allow banks to borrow and lend among one another, as well as provide opportunities to invest excess Monitor Subscriptions 11 funds and borrow to cover temporary liquidity shortfalls. -

National Bank of Kuwait S.A.K

National Bank of Kuwait S.A.K. U.S. Tailored Resolution Plan PUBLIC SECTION Submitted on: December 29, 2014 National Bank of Kuwait S.A.K. Public Section U.S. Resolution Plan Table of Contents (a) Public Section .................................................................................................................... 3 (1) Introduction ................................................................................................................... 3 (2) Overview of NBK ............................................................................................................ 4 (3) Material entities ............................................................................................................. 6 (4) Critical Operations and Core Business Lines .................................................................. 6 (5) Summary of financial information regarding assets, liabilities, capital and major funding sources ................................................................................................................................ 8 (6) Derivatives and hedging activities .................................................................................. 8 (7) Membership in material payment, clearing and settlement systems .............................. 9 (8) Foreign operations ......................................................................................................... 9 (9) Material supervisory authorities .................................................................................... -

Annual Report the Bank of N.T. Butterfield & Son Limited

The Bank of N.T. Butterfield & Son Limited Annual Report 2012 Annual Report Cover 2012_final.indd 1-3 13-03-14 5:12 PM line scope essence In brief focus sight tune Butterfield is committed to environmentally conscious printing. The following savings to our natural resources were realised in the printing of this Annual Report: Energy: 5,874,649 BTUs Air Emissions: 348 kg Trees: 8 Solid Waste: 177 kg 2012 Overview Wastewater: 13,336 liters Cover 2012_final.indd 4-6 13-03-14 5:12 PM As at 31 December 2012 United Kingdom Guernsey In depth Switzerland Find out more at: Bermuda www.butterfieldgroup.com The Bahamas Cayman Islands Two Core Businesses billion $8.9 - Community Banking 1,210 Assets - Wealth Management Employees Efficiency Ratio ROE* Core Earnings improved by 0 281bps 0 45.2% *Core cash return on tangible 479 bps common equity Credit Ratings Fitch Moody’s Standard & Poor’s Short-Term Long-Term Short-Term Long-Term Short-Term Long-Term Senior Senior Senior F1A- P-1 A2 A-2 A- Accolades Six Butterfield employees named to Capital Strength Citywealth International Financial Total Capital Ratio Tier 1 Capital Ratio Centre Leaders List 2012 Euromoney 2012 Global Private Banking Survey Best Private Banking Services Overall (First in Bermuda, Eighth in Caribbean Region) Best Relationship Management (First in Bermuda and Cayman, Fourth in Caribbean Region) Best Range of Investment Products (First in Bermuda) 11.2% 7.5% 10.1% 7.2% 21.6% 15.7% 23.5% 17.7% 24.2% 18.5% Best Net-Worth-Specific Services for 2008 2009 2010 2011 2012 Super-Affluent Clientele (First in Cayman, Third in Caribbean Region) 1 time order sight In review motion brief hand Chairman2 & Chief Executive Officer’s Report to the Shareholders Chairman & Chief Executive Officer’s Report to the Shareholders 2012 was a year of continued recovery for Butterfield. -

Investment Insights

CHIEF INVESTMENT OFFICE Investment Insights AUGUST 2017 Matthew Diczok A Focus on the Fed Head of Fixed Income Strategy An Overview of the Federal Reserve System and a Look at Potential Personnel Changes SUMMARY After years of accommodative policy, the Federal Reserve (Fed) is on its path to policy normalization. The Fed forecasts another rate hike in late 2017, and three hikes in each of the next two years. The Fed also plans to taper reinvestments of Treasurys and mortgage-backed securities, gradually reducing its balance sheet. The market thinks differently. Emboldened by inflation persistently below target, it expects the Fed to move significantly more slowly, with only one to three rate hikes between now and early 2019. One way or another, this discrepancy will be reconciled, with important implications for asset prices and yields. Against this backdrop, changes in personnel at the Fed are very important, and have been underappreciated by markets. The Fed has three open board seats, and the Chair and Vice Chair are both up for reappointment in 2018. If the administration appoints a Fed Chair and Vice Chair who are not currently governors, then there will be five new, permanent voting members who determine rate moves—almost half of the 12-member committee. This would be unprecedented in the modern era. Similar to its potential influence on the Supreme Court, this administration has the ability to set the tone of monetary policy for many years into the future. Most rumored candidates share philosophical leanings at odds with the current board; they are generally hawkish relative to current policy, favor rules-based decision-making over discretionary, and are unconvinced that successive rounds of quantitative easing were beneficial. -

Bank of England List of Banks

LIST OF BANKS AS COMPILED BY THE BANK OF ENGLAND AS AT 31 October 2017 (Amendments to the List of Banks since 30 September 2017 can be found on page 5) Banks incorporated in the United Kingdom Abbey National Treasury Services Plc DB UK Bank Limited ABC International Bank Plc Diamond Bank (UK) Plc Access Bank UK Limited, The Duncan Lawrie Limited (Applied to cancel) Adam & Company Plc ADIB (UK) Ltd EFG Private Bank Limited Agricultural Bank of China (UK) Limited Europe Arab Bank plc Ahli United Bank (UK) PLC AIB Group (UK) Plc FBN Bank (UK) Ltd Airdrie Savings Bank FCE Bank Plc Al Rayan Bank PLC FCMB Bank (UK) Limited Aldermore Bank Plc Alliance Trust Savings Limited Gatehouse Bank Plc Alpha Bank London Limited Ghana International Bank Plc ANZ Bank (Europe) Limited Goldman Sachs International Bank Arbuthnot Latham & Co Limited Guaranty Trust Bank (UK) Limited Atom Bank PLC Gulf International Bank (UK) Limited Axis Bank UK Limited Habib Bank Zurich Plc Bank and Clients PLC Habibsons Bank Limited Bank Leumi (UK) plc Hampden & Co Plc Bank Mandiri (Europe) Limited Hampshire Trust Bank Plc Bank Of America Merrill Lynch International Limited Harrods Bank Ltd Bank of Beirut (UK) Ltd Havin Bank Ltd Bank of Ceylon (UK) Ltd HSBC Bank Plc Bank of China (UK) Ltd HSBC Private Bank (UK) Limited Bank of Cyprus UK Limited HSBC Trust Company (UK) Ltd Bank of Ireland (UK) Plc HSBC UK RFB Limited Bank of London and The Middle East plc Bank of New York Mellon (International) Limited, The ICBC (London) plc Bank of Scotland plc ICBC Standard Bank Plc Bank of the Philippine Islands (Europe) PLC ICICI Bank UK Plc Bank Saderat Plc Investec Bank PLC Bank Sepah International Plc Itau BBA International PLC Barclays Bank Plc Barclays Bank UK PLC J.P. -

Interview of Stanley Fischer by Olivier Blanchard

UBRARIBS Digitized by the Internet Archive in 2011 with funding from Boston Library Consortium IVIember Libraries http://www.archive.org/details/interviewofstanlOOblan 2 DEWEY HB31 .M415 Massachusetts Institute of Technology Department of Economics Working Paper Series Interview of Stanley Fischer By Olivier Blanchard Working Paper 05-1 April 1 9, 2005 Room E52-251 50 Memorial Drive Cambridge, MA 021 42 This paper can be downloaded without charge from the Social Science Research Networl< Paper Collection at http://ssrn.com/abstract=707821 MASSACHUSETTS INSTITUTE OF TECHNOLOGY APR 2 6 2005 LIBRARIES Interview of Stanley Fischer, by Olivier Blanchard.i Abstract Stanley Fischer is a macroeconomist par excellence. After three careers, the first in academia at Chicago, and at MIT, the second at the World Bank and at the International Monetary Fund, the third in the private sector at Citigroup, he is starting a fourth, as the head of the Central Bank of Israel. This interview, to be published in Macroeconomic Dynamics, took place in April 2004, before the start of his fourth career. This interview took place long before Stan had any idea he would become Governor of the Bank of Israel, a position he took up in May 2005. We have not changed the text to reflect this latest stage. Introduction. The interview took place in April 2004 in my office at the Russell Sage Foundation in New York City, where I was spending a sabbatical year. We completed it while running together in Central Park during the following weeks. Our meeting at Russell Sage was just like the many meetings we have had over the years.