March 24, 20162017 the FOUR-RING CIRCUS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Liste Des Actions Concernées Par L'interdiction De Positions Courtes Nettes

Liste des actions concernées par l'interdiction de positions courtes nettes L’interdiction s’applique aux actions listées sur une plate-forme française et relevant de la compétence de l’AMF au titre du règlement 236/2012 (information disponible dans les registres ESMA). Cette liste est fournie à titre informatif. L'AMF n'est pas en mesure de garantir que le contenu disponible est complet, exact ou à jour. Compte tenu des diverses sources de données sous- jacentes, des modifications pourraient être apportées régulièrement. Isin Nom FR0010285965 1000MERCIS FR0013341781 2CRSI FR0010050773 A TOUTE VITESSE FR0000076887 A.S.T. GROUPE FR0010557264 AB SCIENCE FR0004040608 ABC ARBITRAGE FR0013185857 ABEO FR0012616852 ABIONYX PHARMA FR0012333284 ABIVAX FR0000064602 ACANTHE DEV. FR0000120404 ACCOR FR0010493510 ACHETER-LOUER.FR FR0000076861 ACTEOS FR0000076655 ACTIA GROUP FR0011038348 ACTIPLAY (GROUPE) FR0010979377 ACTIVIUM GROUP FR0000053076 ADA BE0974269012 ADC SIIC FR0013284627 ADEUNIS FR0000062978 ADL PARTNER FR0011184241 ADOCIA FR0013247244 ADOMOS FR0010340141 ADP FR0010457531 ADTHINK FR0012821890 ADUX FR0004152874 ADVENIS FR0013296746 ADVICENNE FR0000053043 ADVINI US00774B2088 AERKOMM INC FR0011908045 AG3I ES0105422002 AGARTHA REAL EST FR0013452281 AGRIPOWER FR0010641449 AGROGENERATION CH0008853209 AGTA RECORD FR0000031122 AIR FRANCE -KLM FR0000120073 AIR LIQUIDE FR0013285103 AIR MARINE NL0000235190 AIRBUS FR0004180537 AKKA TECHNOLOGIES FR0000053027 AKWEL FR0000060402 ALBIOMA FR0013258662 ALD FR0000054652 ALES GROUPE FR0000053324 ALPES (COMPAGNIE) -

2012-13 Annual Report of Private Giving

MAKING THE EXTRAORDINARY POSSIBLE 2012–13 ANNUAL REPORT OF PRIVATE GIVING 2 0 1 2–13 ANNUAL REPORT OF PRIVATE GIVING “Whether you’ve been a donor to UMaine for years or CONTENTS have just made your first gift, I thank you for your Letter from President Paul Ferguson 2 Fundraising Partners 4 thoughtfulness and invite you to join us in a journey Letter from Jeffery Mills and Eric Rolfson 4 that promises ‘Blue Skies ahead.’ ” President Paul W. Ferguson M A K I N G T H E Campaign Maine at a Glance 6 EXTRAORDINARY 2013 Endowments/Holdings 8 Ways of Giving 38 POSSIBLE Giving Societies 40 2013 Donors 42 BLUE SKIES AHEAD SINCE GRACE, JENNY AND I a common theme: making life better student access, it is donors like you arrived at UMaine just over two years for others — specifically for our who hold the real keys to the ago, we have truly enjoyed our students and the state we serve. While University of Maine’s future level interactions with many alumni and I’ve enjoyed many high points in my of excellence. friends who genuinely care about this personal and professional life, nothing remarkable university. Events like the surpasses the sense of reward and Unrestricted gifts that provide us the Stillwater Society dinner and the accomplishment that accompanies maximum flexibility to move forward Charles F. Allen Legacy Society assisting others to fulfill their are one of these keys. We also are luncheon have allowed us to meet and potential. counting on benefactors to champion thank hundreds of donors. -

2011 Registration Document Annual Financial Report SUMMARY

2011 Registration Document Annual Financial Report SUMMARY 1 PRESENTATION OF THE GROUP 3 6 ADDITIONAL INFORMATION 227 1.1 Main key figures 4 6.1 Information about the Company 228 1.2 The Group’s strategy and general structure 5 6.2 Information about the share capital 232 1.3 Minerals 10 6.3 Shareholding 238 1.4 Minerals for Ceramics, Refractories, 6.4 Elements which could have an impact Abrasives & Foundry 17 in the event of a takeover bid 241 1.5 Performance & Filtration Minerals 26 6.5 Imerys stock exchange information 242 1.6 Pigments for Paper & Packaging 32 6.6 Dividends 244 1.7 Materials & Monolithics 36 6.7 Shareholder relations 244 1.8 Innovation 43 6.8 Parent company/subsidiaries organization 245 1.9 Sustainable Development 48 ORDINARY AND EXTRAORDINARY REPORTS ON THE FISCAL YEAR 2011 65 7 SHAREHOLDERS’ GENERAL MEETING 2 OF APRIL 26, 2012 247 2.1 Board of Directors’ management report 66 2.2 Statutory Auditors' Reports 77 7.1 Presentation of the resolutions by the Board of Directors 248 7.2 Agenda 254 7.3 Draft resolutions 255 3 CORPORATE GOVERNANCE 83 3.1 Board of Directors 84 3.2 Executive Management 103 PERSONS RESPONSIBLE FOR THE 3.3 Compensation 105 8 REGISTRATION DOCUMENT AND THE AUDIT 3.4 Stock options 109 OF ACCOUNTS 261 3.5 Free shares 114 8.1 Person responsible for the Registration Document 262 3.6 Specific terms and restrictions applicable to grants 8.2 Certificate of the person responsible to the Chairman and Chief Executive Officer 116 for the Registration Document 262 3.7 Corporate officers’ transactions in securities -

Growth of the Internet

Growth of the Internet K. G. Coffman and A. M. Odlyzko AT&T Labs - Research [email protected], [email protected] Preliminary version, July 6, 2001 Abstract The Internet is the main cause of the recent explosion of activity in optical fiber telecommunica- tions. The high growth rates observed on the Internet, and the popular perception that growth rates were even higher, led to an upsurge in research, development, and investment in telecommunications. The telecom crash of 2000 occurred when investors realized that transmission capacity in place and under construction greatly exceeded actual traffic demand. This chapter discusses the growth of the Internet and compares it with that of other communication services. Internet traffic is growing, approximately doubling each year. There are reasonable arguments that it will continue to grow at this rate for the rest of this decade. If this happens, then in a few years, we may have a rough balance between supply and demand. Growth of the Internet K. G. Coffman and A. M. Odlyzko AT&T Labs - Research [email protected], [email protected] 1. Introduction Optical fiber communications was initially developed for the voice phone system. The feverish level of activity that we have experienced since the late 1990s, though, was caused primarily by the rapidly rising demand for Internet connectivity. The Internet has been growing at unprecedented rates. Moreover, because it is versatile and penetrates deeply into the economy, it is affecting all of society, and therefore has attracted inordinate amounts of public attention. The aim of this chapter is to summarize the current state of knowledge about the growth rates of the Internet, with special attention paid to the implications for fiber optic transmission. -

In the United States Bankruptcy Court for the District of Delaware

Case 19-10684 Doc 16 Filed 04/01/19 Page 1 of 1673 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE x In re: : Chapter 11 : HEXION HOLDINGS LLC, et al.,1 : Case No. 19-10684 ( ) : Debtors. : Joint Administration Requested x NOTICE OF FILING OF CREDITOR MATRIX PLEASE TAKE NOTICE that the above-captioned debtors and debtors in possession have today filed the attached Creditor Matrix with the United States Bankruptcy Court for the District of Delaware, 824 North Market Street, Wilmington, Delaware 19801. 1 The Debtors in these cases, along with the last four digits of each Debtor’s federal tax identification number, are Hexion Holdings LLC (6842); Hexion LLC (8090); Hexion Inc. (1250); Lawter International Inc. (0818); Hexion CI Holding Company (China) LLC (7441); Hexion Nimbus Inc. (4409); Hexion Nimbus Asset Holdings LLC (4409); Hexion Deer Park LLC (8302); Hexion VAD LLC (6340); Hexion 2 U.S. Finance Corp. (2643); Hexion HSM Holdings LLC (7131); Hexion Investments Inc. (0359); Hexion International Inc. (3048); North American Sugar Industries Incorporated (9735); Cuban-American Mercantile Corporation (9734); The West India Company (2288); NL Coop Holdings LLC (0696); and Hexion Nova Scotia Finance, ULC (N/A). The address of the Debtors’ corporate headquarters is 180 East Broad Street, Columbus, Ohio 43215. RLF1 20960951V.1 Case 19-10684 Doc 16 Filed 04/01/19 Page 2 of 1673 Dated: April 1, 2019 Wilmington, Delaware /s/ Sarah E. Silveira Mark D. Collins (No. 2981) Michael J. Merchant (No. 3854) Amanda R. Steele (No. 5530) Sarah E. Silveira (No. 6580) RICHARDS, LAYTON & FINGER, P.A. -

The Great Telecom Meltdown for a Listing of Recent Titles in the Artech House Telecommunications Library, Turn to the Back of This Book

The Great Telecom Meltdown For a listing of recent titles in the Artech House Telecommunications Library, turn to the back of this book. The Great Telecom Meltdown Fred R. Goldstein a r techhouse. com Library of Congress Cataloging-in-Publication Data A catalog record for this book is available from the U.S. Library of Congress. British Library Cataloguing in Publication Data Goldstein, Fred R. The great telecom meltdown.—(Artech House telecommunications Library) 1. Telecommunication—History 2. Telecommunciation—Technological innovations— History 3. Telecommunication—Finance—History I. Title 384’.09 ISBN 1-58053-939-4 Cover design by Leslie Genser © 2005 ARTECH HOUSE, INC. 685 Canton Street Norwood, MA 02062 All rights reserved. Printed and bound in the United States of America. No part of this book may be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without permission in writing from the publisher. All terms mentioned in this book that are known to be trademarks or service marks have been appropriately capitalized. Artech House cannot attest to the accuracy of this information. Use of a term in this book should not be regarded as affecting the validity of any trademark or service mark. International Standard Book Number: 1-58053-939-4 10987654321 Contents ix Hybrid Fiber-Coax (HFC) Gave Cable Providers an Advantage on “Triple Play” 122 RBOCs Took the Threat Seriously 123 Hybrid Fiber-Coax Is Developed 123 Cable Modems -

Designated Agents for Local Exchange Carriers

Designated Agents for Local Exchange Carriers Document Processor Document Processor 321 Communications, Inc. Access Point, Inc. InCorp Services, Inc. Illinois Corporation Service Company 2501 Chatham Rd., Ste. 110 801 Adlai Stevenson Dr. Springfield IL 62704-7100 Springfield IL 62703-4261 Lisa Brown John Petrakis 321 Communications, Inc. Access2Go, Inc. Regulatory and Tax Consultants 4700 N. Prospect Rd. 3483 Satellite Blvd., Ste. 202 Peoria Heights IL 61616 Duluth GA 30096-5800 Document Processor Document Processor ACN Communication Services, Inc. 360networks (USA) inc. C T Corporation System C T Corporation System 208 S. LaSalle St. 208 S. LaSalle St. Chicago IL 60604 Chicago IL 60604 Doug Forster Document Processor ACN Communication Services, Inc. AboveNet Communications, Inc. Technologies Management, Inc. d/b/a AboveNet Media Networks PO Drawer 200 Illinois Corporation Service Company Winter Park FL 32790-0200 801 Adlai Stevenson Dr. Springfield IL 62703-4261 James W. Broemmer Jr Adams Telephone Co-Operative Robert Sokota PO Box 217 AboveNet Communications, Inc. Golden IL 62339 d/b/a AboveNet Media Networks 360 Hamilton Blvd. James W. Broemmer Jr White Plains NY 10601 Adams TelSystems, Inc. PO Box 217 Robert Neumann Golden IL 62339 Access Media 3, Inc. 900 Commerce Dr., Ste. 200 Gary Pieper Oak Brook IL 60523 Advanced Integrated Technologies Inc. PO Box 51 Brian McDermott Columbia IL 62236 Access Media 3, Inc. Synergies Law Group, PLLC Mark Lammert 1002 Parker St. Advanced Integrated Technologies Inc. Falls Church VA 22046 Compliance Solutions Inc. 740 Florida Central Pkwy., Ste. 2028 Document Processor Longwood FL 32750 Access One, Inc. Corporation Service Company Ronald Dougherty 422 N. -

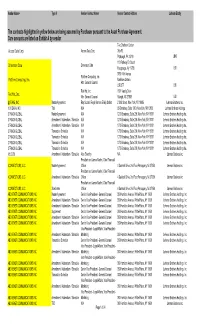

The Contracts Highlighted in Yellow Below Are Being Assumed by Purchaser Pursuant to the Asset Purchase Agreement. Cure Amounts Are Listed on Exhibit a by Vendor

Vendor Name+ Type II Vendor Contact Name Vendor Contact Address Lehman Entity The contracts highlighted in yellow below are being assumed by Purchaser pursuant to the Asset Purchase Agreement. Cure amounts are listed on Exhibit A by vendor. Two Chatham Center Access Data Corp. Access Data Corp. 24th FL Pittsburgh, PA 15219 LBHI 110 Parkway Dr. South Dimension Data Dimension Data Hauppauge, Ny 11788 LBI 3760 14th Avenue Platform Computing, Inc. Platform Computing, Inc. Markham Ontario Attn: General Counsel L3R 3T7 LBI Red Hat, Inc. 1801 Varsity Drive Red Hat, Inc. Attn: General Counsel Raleigh, NC 27606 LBI @STAKE, INC Master Agreement Ray Scutari, Royal Hansen, Emily Sebert 2 Wall Street, New York, NY 10005 Lehman Brothers, Inc. 1010 DATA, INC Trial N/A 65 Broadway, Suite 1010, New York, NY 10006 Lehman Brothers Holdings 2 TRACK GLOBAL Master Agreement N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Amendment / Addendum / Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Amendment / Addendum / Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, DC 20549

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event reported): March 22, 2021 (March 19, 2021) REYNOLDS CONSUMER PRODUCTS INC. (Exact Name of Registrant as Specified in its Charter) Delaware 001-39205 45-3464426 (State or other jurisdiction (Commission (I.R.S. Employer of incorporation) File Number) Identification No.) 1900 W. Field Court Lake Forest, Illinois 60045 (Address of Principal Executive Offices) (Zip Code) Registrant’s telephone number, including area code: (800) 879-5067 Not Applicable (Former name or former address, if changed since last report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below): ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Securities registered pursuant to Section 12(b) of the Act: Trading Title of each class symbol(s) Name of each exchange on which registered Common Stock, $0.001 Par Value REYN The Nasdaq Stock Market LLC Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter). -

Alphabetical Listing by Company Name

FOREIGN COMPANIES REGISTERED AND REPORTING WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION December 31, 2015 Alphabetical Listing by Company Name COMPANY COUNTRY MARKET 21 Vianet Group Inc. Cayman Islands Global Market 37 Capital Inc. Canada OTC 500.com Ltd. Cayman Islands NYSE 51Job, Inc. Cayman Islands Global Market 58.com Inc. Cayman Islands NYSE ABB Ltd. Switzerland NYSE Abbey National Treasury Services plc United Kingdom NYSE - Debt Abengoa S.A. Spain Global Market Abengoa Yield Ltd. United Kingdom Global Market Acasti Pharma Inc. Canada Capital Market Acorn International, Inc. Cayman Islands NYSE Actions Semiconductor Co. Ltd. Cayman Islands Global Market Adaptimmune Ltd. United Kingdom Global Market Adecoagro S.A. Luxembourg NYSE Adira Energy Ltd. Canada OTC Advanced Accelerator Applications SA France Global Market Advanced Semiconductor Engineering, Inc. Taiwan NYSE Advantage Oil & Gas Ltd. Canada NYSE Advantest Corp. Japan NYSE Aegean Marine Petroleum Network Inc. Marshall Islands NYSE AEGON N.V. Netherlands NYSE AerCap Holdings N.V. Netherlands NYSE Aeterna Zentaris Inc. Canada Capital Market Affimed N.V. Netherlands Global Market Agave Silver Corp. Canada OTC Agnico Eagle Mines Ltd. Canada NYSE Agria Corp. Cayman Islands NYSE Agrium Inc. Canada NYSE AirMedia Group Inc. Cayman Islands Global Market Aixtron SE Germany Global Market Alamos Gold Inc. Canada NYSE Alcatel-Lucent France NYSE Alcobra Ltd. Israel Global Market Alexandra Capital Corp. Canada OTC Alexco Resource Corp. Canada NYSE MKT Algae Dynamics Corp. Canada OTC Algonquin Power & Utilities Corp. Canada OTC Alianza Minerals Ltd. Canada OTC Alibaba Group Holding Ltd. Cayman Islands NYSE Allot Communications Ltd. Israel Global Market Almaden Minerals Ltd. -

NASD Notice to Members 99-46

Executive Summary $250, and two or more Market NASD Effective July 1, 1999, the maximum Ma k e r s . Small Order Execution SystemSM (S O E S SM ) order sizes for 336 Nasdaq In accordance with Rule 4710, Nas- Notice to National Market® (NNM) securities daq periodically reviews the maxi- will be revised in accordance with mum SOES order size applicable to National Association of Securities each NNM security to determine if Members Dealers, Inc. (NASD®) Rule 4710(g). the trading characteristics of the issue have changed so as to warrant For more information, please contact an adjustment. Such a review was 99-46 ® Na s d a q Market Operations at conducted using data as of March (203) 378-0284. 31, 1999, pursuant to the aforemen- Maximum SOES Order tioned standards. The maximum Sizes Set To Change SOES order-size changes called for Description by this review are being implemented July 1, 1999 Under Rule 4710, the maximum with three exceptions. SOES order size for an NNM security is 1,000, 500, or 200 shares, • First, issues were not permitted to depending on the trading characteris- move more than one size level. For Suggested Routing tics of the security. The Nasdaq example, if an issue was previously ® Senior Management Workstation II (NWII) indicates the categorized in the 1,000-share maximum SOES order size for each level, it would not be permitted to Ad v e r t i s i n g NNM security. The indicator “NM10,” move to the 200-share level, even if Continuing Education “NM5,” or “NM2” displayed in NWII the formula calculated that such a corresponds to a maximum SOES move was warranted. -

2010 IMRF Addendum to the 2010 Comprehensive Annual Financial

Illinois Municipal Retirement Fund Addendum to the 2010 Comprehensive Annual Financial Report For the year ending December 31, 2010 Illinois Municipal Retirement Fund Investment Portfolio as of December 31, 2010 Interest Asset Description Rate Maturity Date Par Value Cost Value Market Value FIXED INCOME U.S. Securities Corporate Bonds 1st Horizon Natl 5.38% 12/15/2015 $ 500,000 $ 498,345 $ 504,710 Abbott Labs 5.13% 4/1/2019 2,830,000 2,817,746 3,116,011 Acco Brands Corp 10.63% 3/15/2015 90,000 88,652 101,250 Ace Cash Express 10.25% 10/1/2014 330,000 330,000 290,400 Actuant Corp 6.88% 6/15/2017 990,000 991,138 1,012,275 Adobe Sys Inc 4.75% 2/1/2020 2,365,000 2,319,805 2,419,182 AEP Inds Inc Sr Nt 7.88% 3/15/2013 180,000 180,000 179,325 AES Corp 7.75% 3/1/2014 350,000 373,988 373,625 AES Corp 7.75% 10/15/2015 580,000 580,000 619,150 AES Corp 8.00% 10/15/2017 140,000 141,075 148,050 Affiliated 5.20% 6/1/2015 650,000 675,340 689,794 Affinia Group Inc 9.00% 11/30/2014 720,000 668,494 739,800 AFLAC Inc 8.50% 5/15/2019 2,745,000 3,255,410 3,394,173 AFLAC Inc 6.45% 8/15/2040 3,000,000 2,984,970 3,072,534 Air Med Group 9.25% 11/1/2018 980,000 980,000 1,029,000 Ak Stl Corp Sr Nt 7.63% 5/15/2020 100,000 99,000 100,250 Albertsons Inc 7.50% 2/15/2011 1,500,000 1,523,385 1,501,875 Alcoa Inc 6.15% 8/15/2020 3,000,000 2,996,130 3,080,703 Alere Inc 8.63% 10/1/2018 1,045,000 1,046,575 1,060,675 Aleris International Inc Dip 10.46% 12/19/2013 139,837 61,794 143,858 Aleris Intl Inc B-1 Ru 4.25% 12/19/2013 325,784 286,376 146,603 Aleris Intl Inc Sr 9.00% 12/15/2014