NASD Notice to Members 99-46

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NASDAQ MLNK 2003.Pdf

Dear Fellow Stockholder: Our fiscal year 2003 has seen the completion of an eighteen-month period of restructuring, and the focus of management’s efforts on expansion of select core businesses. CMGI has made great strides in building its long- term liquidity and improving its operating results. The focus of management’s attention continues to be on building the global supply chain management business and expanding the literature fulfillment business in the United States, both of which are operated by CMGI’s wholly owned subsidiary, SalesLink, and realizing value and liquidity from the venture capital portfolio of our venture capital affiliate, @Ventures. The restructuring of CMGI into a more focused operating company was achieved in several steps during the year: • Non-core or under performing businesses were divested. This included CMGI’s divestitures of its interests in Engage, Inc., NaviSite, Inc., Equilibrium Technologies, Inc., Signatures SNI, Inc., Tallan, Inc. and Yesmail, Inc. • uBid, Inc. sold its assets to a global leader in sourcing, selling and financing of consumer goods. • AltaVista Company, operating in the rapidly consolidating internet search industry, sold its assets to Overture Services, Inc., which was acquired by Yahoo! Inc. shortly thereafter. The divestiture of these businesses has allowed CMGI to focus its management resources on its global supply chain management and fulfillment businesses. CMGI ended fiscal year 2003 with $276 million in cash, cash equivalents, and marketable securities. Cash used for operating activities from continuing operations in fiscal 2003 improved markedly from fiscal 2002. The cash balances available at year end permit CMGI to strive toward accomplishing three objectives: maintaining a liquidity reserve to protect the long-term future of the company, investing in expansion of its supply chain management and fulfillment businesses, and making selective acquisitions, either of new accounts or of companies, to expand these businesses. -

Internet Distribution, E-Commerce and Other Computer Related Issues

Internet Distribution, E-Commerce and Other Computer Related Issues: Current Developments in Liability On-Line, Business Methods Patents and Software Distribution, Licensing and Copyright Protection Questions Table of Contents Contents I. Liability On-Line: Copyright and Tort Risks of Providing Content, or Who’s In Charge Here? ......................................................................................................1 A. The Applicability of Multiple Laws ..........................................................................1 B. Jurisdictional Questions ..........................................................................................2 C. Determining Applicable Law .................................................................................16 D. Copyright Infringement ..........................................................................................21 E. Defamation & the Communications Decency Act ..................................................31 F. Trademark Infringement ........................................................................................36 G. Regulation of Spam ................................................................................................47 H. Spyware ..................................................................................................................54 I. Trespass .................................................................................................................55 J. Privacy ...................................................................................................................57 -

Chicago Board Options Exchange Annual Report 2001

01 Chicago Board Options Exchange Annual Report 2001 cv2 CBOE ‘01 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010 CBOE is the largest and 01010101010101010most successful options 01010101010101010marketplace in the world. 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010ifc1 CBOE ‘01 ONE HAS OPPORTUNITIES The NUMBER ONE Options Exchange provides customers with a wide selection of products to achieve their unique investment goals. ONE HAS RESPONSIBILITIES The NUMBER ONE Options Exchange is responsible for representing the interests of its members and customers. Whether testifying before Congress, commenting on proposed legislation or working with the Securities and Exchange Commission on finalizing regulations, the CBOE weighs in on behalf of options users everywhere. As an advocate for informed investing, CBOE offers a wide array of educational vehicles, all targeted at educating investors about the use of options as an effective risk management tool. ONE HAS RESOURCES The NUMBER ONE Options Exchange offers a wide variety of resources beginning with a large community of traders who are the most experienced, highly-skilled, well-capitalized liquidity providers in the options arena. In addition, CBOE has a unique, sophisticated hybrid trading floor that facilitates efficient trading. 01 CBOE ‘01 2 CBOE ‘01 “ TO BE THE LEADING MARKETPLACE FOR FINANCIAL DERIVATIVE PRODUCTS, WITH FAIR AND EFFICIENT MARKETS CHARACTERIZED BY DEPTH, LIQUIDITY AND BEST EXECUTION OF PARTICIPANT ORDERS.” CBOE MISSION LETTER FROM THE OFFICE OF THE CHAIRMAN Unprecedented challenges and a need for strategic agility characterized a positive but demanding year in the overall options marketplace. The Chicago Board Options Exchange ® (CBOE®) enjoyed a record-breaking fiscal year, with a 2.2% growth in contracts traded when compared to Fiscal Year 2000, also a record-breaker. -

Comércio Eletrônico

Comércio Eletrônico Aula 1 - Overview of Electronic Commerce Learning Objectives 1. Define electronic commerce (EC) and describe its various categories. 2. Describe and discuss the content and framework of EC. 3. Describe the major types of EC transactions. 4. Describe the drivers of EC. 5. Discuss the benefits of EC to individuals, organizations, and society. 6. Discuss social computing. 7. Describe social commerce and social software. 8. Understand the elements of the digital world. 9. Describe some EC business models. 10. List and describe the major limitations of EC. Case: Starbucks Electronic Commerce (EC) EC refers to using the Internet and other networks (e.g., intranets) to purchase, sell, transport, or trade data, goods, or services. e-Business • Narrow definition of EC: buying and selling transactions between business partners. • e-Business refers to a broader definition of EC: – buying and selling of goods and services – Servicing customers – collaborating with business partners, – delivering e-learning, – conducting electronic transactions within organizations. – Among others e-Business Note: some view e-business only as comprising those activities that do not involve buying or selling over the Internet, i.e., a complement of the narrowly defined EC. Major EC Concepts: Non-EC vs. Pure EC vs. Partial EC • EC three major activities: – ordering and payments, – order fulfilment, and – delivery to customers. • pure EC: all activities are digital, • non-EC: none are digital, • otherwise, we have partial EC. Major EC Concepts: Pure -

Growth of the Internet

Growth of the Internet K. G. Coffman and A. M. Odlyzko AT&T Labs - Research [email protected], [email protected] Preliminary version, July 6, 2001 Abstract The Internet is the main cause of the recent explosion of activity in optical fiber telecommunica- tions. The high growth rates observed on the Internet, and the popular perception that growth rates were even higher, led to an upsurge in research, development, and investment in telecommunications. The telecom crash of 2000 occurred when investors realized that transmission capacity in place and under construction greatly exceeded actual traffic demand. This chapter discusses the growth of the Internet and compares it with that of other communication services. Internet traffic is growing, approximately doubling each year. There are reasonable arguments that it will continue to grow at this rate for the rest of this decade. If this happens, then in a few years, we may have a rough balance between supply and demand. Growth of the Internet K. G. Coffman and A. M. Odlyzko AT&T Labs - Research [email protected], [email protected] 1. Introduction Optical fiber communications was initially developed for the voice phone system. The feverish level of activity that we have experienced since the late 1990s, though, was caused primarily by the rapidly rising demand for Internet connectivity. The Internet has been growing at unprecedented rates. Moreover, because it is versatile and penetrates deeply into the economy, it is affecting all of society, and therefore has attracted inordinate amounts of public attention. The aim of this chapter is to summarize the current state of knowledge about the growth rates of the Internet, with special attention paid to the implications for fiber optic transmission. -

Leading You to a Brighter Future

ANNUAL REPORT 2001 西 日 本ANNUAL REPORT 旅 客 鉄 道 株 式 会 社 一 九 九 九2001 年 三 月 期 年 次 報 告 書 Leading you to a brighter future http://www.softbank.co.jp SOFTBANK 2001 1 C1 QX/Softbank (E) 後半 01.9.12 3:25 PM ページ 60 Directors and Corporate Auditors As of June 21, 2001 President & Chief Executive Officer MASAYOSHI SON Directors YOSHITAKA KITAO KEN MIYAUCHI KAZUHIKO KASAI MASAHIRO INOUE President & CEO, President & CEO, President & CEO, SOFTBANK FINANCE SOFTBANK EC HOLDINGS Yahoo Japan Corporation CORPORATION CORP. RONALD D. FISHER JUN MURAI, PH.D. TOSHIFUMI SUZUKI TADASHI YANAI MARK SCHWARTZ Vice Chairman, Professor, Faculty of President & CEO, President & CEO, Chairman, SOFTBANK Holdings Inc. Environmental Information, Ito-Yokado Co., Ltd., FAST RETAILING CO., LTD. Goldman Sachs (Asia) KEIO University and Chairman & CEO, Seven-Eleven Japan Co., Ltd. Corporate Auditors MITSUO YASUHARU SABURO HIDEKAZU SANO NAGASHIMA KOBAYASHI KUBOKAWA Full-time Corporate Auditor, Attorney Full-time Corporate Auditor, Certified Public Accountant, SOFTBANK CORP. HEIWA Corporation Certified Tax Accountant Note: Corporate auditors Yasuharu Nagashima, Saburo Kobayashi, and Hidekazu Kubokawa are outside corporate auditors appointed under Article 18, Section 1, of the Commercial Code of Japan. 60 60 QX/Softbank (E) 後半pdf修正 01.10.11 10:39 AM ページ 61 SOFTBANK Corporate Directory Domestic Overseas SOFTBANK CORP. SOFTBANK Broadmedia Corporation SOFTBANK Inc. http://www.softbank.co.jp/ http://www.broadmedia.co.jp/ http://www.softbank.com/ 24-1, Nihonbashi-Hakozakicho, Chuo-ku, 24-1, Nihonbashi-Hakozakicho, Chuo-ku, 1188 Centre Street, Tokyo 103-8501, Japan Tokyo 103-0015, Japan Newton Center, MA 02459, U.S.A. -

Oc-Gl-Etv-Og-V02-091223

OpenCable™ Guidelines Enhanced TV Operational Guidelines OC-GL-ETV-OG-V02-091223 RELEASED Notice This document is the result of a cooperative effort undertaken at the direction of Cable Television Laboratories, Inc. for the benefit of the cable industry and its customers. This document may contain references to other documents not owned or controlled by CableLabs. Use and understanding of this document may require access to such other documents. Designing, manufacturing, distributing, using, selling, or servicing products, or providing services, based on this document may require intellectual property licenses from third parties for technology referenced in the document. Neither CableLabs nor any member company is responsible to any party for any liability of any nature whatsoever resulting from or arising out of use or reliance upon this document, or any document referenced herein. This document is furnished on an "AS IS" basis and neither CableLabs nor its members provides any representation or warranty, express or implied, regarding the accuracy, completeness, or fitness for a particular purpose of this document, or any document referenced herein. © Copyright 2006 - 2009 Cable Television Laboratories, Inc. All rights reserved. OC-GL-ETV-OG-V02-091223 OpenCable™ Guidelines Document Status Sheet Document Control Number: OC-GL-ETV-OG-V02-091223 Document Title: Enhanced TV Operational Guidelines Revision History: V01 - released 7/14/06 V02 - released 12/23/09 Date: December 23, 2009 Status: Work in Draft Released Closed Progress Distribution Restrictions: Author Only CL/Member CL/ Member/ Public Vendor Trademarks CableLabs®, DOCSIS®, EuroDOCSIS™, eDOCSIS™, M-CMTS™, PacketCable™, EuroPacketCable™, PCMM™, CableHome®, CableOffice™, OpenCable™, OCAP™, CableCARD™, M-Card™, DCAS™, tru2way™, and CablePC™ are trademarks of Cable Television Laboratories, Inc. -

The Great Telecom Meltdown for a Listing of Recent Titles in the Artech House Telecommunications Library, Turn to the Back of This Book

The Great Telecom Meltdown For a listing of recent titles in the Artech House Telecommunications Library, turn to the back of this book. The Great Telecom Meltdown Fred R. Goldstein a r techhouse. com Library of Congress Cataloging-in-Publication Data A catalog record for this book is available from the U.S. Library of Congress. British Library Cataloguing in Publication Data Goldstein, Fred R. The great telecom meltdown.—(Artech House telecommunications Library) 1. Telecommunication—History 2. Telecommunciation—Technological innovations— History 3. Telecommunication—Finance—History I. Title 384’.09 ISBN 1-58053-939-4 Cover design by Leslie Genser © 2005 ARTECH HOUSE, INC. 685 Canton Street Norwood, MA 02062 All rights reserved. Printed and bound in the United States of America. No part of this book may be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without permission in writing from the publisher. All terms mentioned in this book that are known to be trademarks or service marks have been appropriately capitalized. Artech House cannot attest to the accuracy of this information. Use of a term in this book should not be regarded as affecting the validity of any trademark or service mark. International Standard Book Number: 1-58053-939-4 10987654321 Contents ix Hybrid Fiber-Coax (HFC) Gave Cable Providers an Advantage on “Triple Play” 122 RBOCs Took the Threat Seriously 123 Hybrid Fiber-Coax Is Developed 123 Cable Modems -

Designated Agents for Local Exchange Carriers

Designated Agents for Local Exchange Carriers Document Processor Document Processor 321 Communications, Inc. Access Point, Inc. InCorp Services, Inc. Illinois Corporation Service Company 2501 Chatham Rd., Ste. 110 801 Adlai Stevenson Dr. Springfield IL 62704-7100 Springfield IL 62703-4261 Lisa Brown John Petrakis 321 Communications, Inc. Access2Go, Inc. Regulatory and Tax Consultants 4700 N. Prospect Rd. 3483 Satellite Blvd., Ste. 202 Peoria Heights IL 61616 Duluth GA 30096-5800 Document Processor Document Processor ACN Communication Services, Inc. 360networks (USA) inc. C T Corporation System C T Corporation System 208 S. LaSalle St. 208 S. LaSalle St. Chicago IL 60604 Chicago IL 60604 Doug Forster Document Processor ACN Communication Services, Inc. AboveNet Communications, Inc. Technologies Management, Inc. d/b/a AboveNet Media Networks PO Drawer 200 Illinois Corporation Service Company Winter Park FL 32790-0200 801 Adlai Stevenson Dr. Springfield IL 62703-4261 James W. Broemmer Jr Adams Telephone Co-Operative Robert Sokota PO Box 217 AboveNet Communications, Inc. Golden IL 62339 d/b/a AboveNet Media Networks 360 Hamilton Blvd. James W. Broemmer Jr White Plains NY 10601 Adams TelSystems, Inc. PO Box 217 Robert Neumann Golden IL 62339 Access Media 3, Inc. 900 Commerce Dr., Ste. 200 Gary Pieper Oak Brook IL 60523 Advanced Integrated Technologies Inc. PO Box 51 Brian McDermott Columbia IL 62236 Access Media 3, Inc. Synergies Law Group, PLLC Mark Lammert 1002 Parker St. Advanced Integrated Technologies Inc. Falls Church VA 22046 Compliance Solutions Inc. 740 Florida Central Pkwy., Ste. 2028 Document Processor Longwood FL 32750 Access One, Inc. Corporation Service Company Ronald Dougherty 422 N. -

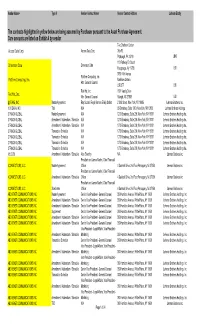

The Contracts Highlighted in Yellow Below Are Being Assumed by Purchaser Pursuant to the Asset Purchase Agreement. Cure Amounts Are Listed on Exhibit a by Vendor

Vendor Name+ Type II Vendor Contact Name Vendor Contact Address Lehman Entity The contracts highlighted in yellow below are being assumed by Purchaser pursuant to the Asset Purchase Agreement. Cure amounts are listed on Exhibit A by vendor. Two Chatham Center Access Data Corp. Access Data Corp. 24th FL Pittsburgh, PA 15219 LBHI 110 Parkway Dr. South Dimension Data Dimension Data Hauppauge, Ny 11788 LBI 3760 14th Avenue Platform Computing, Inc. Platform Computing, Inc. Markham Ontario Attn: General Counsel L3R 3T7 LBI Red Hat, Inc. 1801 Varsity Drive Red Hat, Inc. Attn: General Counsel Raleigh, NC 27606 LBI @STAKE, INC Master Agreement Ray Scutari, Royal Hansen, Emily Sebert 2 Wall Street, New York, NY 10005 Lehman Brothers, Inc. 1010 DATA, INC Trial N/A 65 Broadway, Suite 1010, New York, NY 10006 Lehman Brothers Holdings 2 TRACK GLOBAL Master Agreement N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Amendment / Addendum / Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Amendment / Addendum / Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. 2 TRACK GLOBAL Transaction Schedule N/A 1270 Broadway, Suite 208, New York, NY 10001 Lehman Brothers Holdings Inc. -

13-0399 JBM Journal Special Issue Vol 19.Indd

Jeffrey A. Sonnenfeld 59 Steve Jobs’ Immortal Quest and the Heroic Persona Jeffrey A. Sonnenfeld Yale University October 2011 was a month of historic milestones for Apple. At the end of the prior month, on Tuesday, September 27, Apple sent media invitations for a press event to be held October 4, 2011 at 10:00 am at the Cupertino Headquarters for a major announcement. Several prominent industry analysts proclaimed with hopeful optimism that the firm would announce the return of Apple founder Steve Jobs. Sadly, Steve Jobs did not appear for what turned out to be a product announcement of the iPhone 4S. In fact, Jobs had stepped down as CEO on January 17, 2011, a year and a half after returning from medical leave. He stated that Tim Cook, Apple’s Chief Operating Officer, would run day-to-day operations as he had previously done during Jobs’ 2009 medical leave. The analysts’ wishful thinking had some basis in more than cult like denial of Steve Jobs’ mortality. In fact, despite that medical leave, Jobs had returned for the iPad 2 launch on March 2 and the iCloud introduction on June 6. The analysts were among many constituents around the world who were to be tragically disappointed. Jobs actually had resigned as CEO on August 22, 2011 saying, “I have always said if there ever came a day when I could no longer meet my duties and expectations as Apple’s CEO, I would be the first to let you know. Unfortunately, that day has come” (Isaacson, 2011). Six weeks later, a day after the new iPhone press conference, he died (Isaacson, 2011). -

How Much Are Your Eyeballs Worth? Placing a Value on a Website's Customers May Be the Best Way to Judge a Net Stock

How Much Are Your Eyeballs Worth? Placing a value on a Website's customers may be the best way to judge a Net stock. It's not perfect, but on the Net, what is? By Erick Schonfeld February 21, 2000 (FORTUNE Magazine) – Internet CEOs crave many things: world domination, instant service in bistros, fawning media attention. But what they crave above all else is eyeballs. That's less ghoulish than it sounds. In Webspeak, you see, eyeballs mean customers. Since the typical dot- com lacks the one metric that Wall Street has traditionally used to evaluate companies (you remember--earnings) analysts and investors have contrived other ways to size up Net stocks. One now stands out: market capitalization per pair of eyeballs. It's a useful first step in explaining why a company garners a certain kind of valuation. For instance, a pair of eyeballs at Web portal Lycos, with a $7.4 billion market cap, has a value of just $244; at Schwab, which has a $30 billion market cap, a pair is worth $4,562 (ironically, this also happens to be around the price a pair of real human corneas reportedly commands on the black market). If the Internet market were rational, the market cap per eyeball would represent the total profit that you could reasonably expect a company to get from its average customer, adjusted for risk and the length of time before those profits are realized. Internet analysts are the first to admit that today's is not a rational market. So correlating the lifetime value of eyeballs to a fast-growing dot-com's stock price is not perfect science.