Leading You to a Brighter Future

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FACTSHEET - AS of 30-Sep-2021 Solactive L&G ESG Japan PR Index

FACTSHEET - AS OF 30-Sep-2021 Solactive L&G ESG Japan PR Index HISTORICAL PERFORMANCE 240 220 200 180 160 140 120 100 Jan-2013 Jan-2014 Jan-2015 Jan-2016 Jan-2017 Jan-2018 Jan-2019 Jan-2020 Jan-2021 Solactive L&G ESG Japan PR Index CHARACTERISTICS ISIN / WKN DE000SLA5HR1 / SLA5HR Base Value / Base Date 100 Points / 02.05.2012 Bloomberg / Reuters SOESGJPP Index / .SOESGJPP Last Price 226.15 Index Calculator Solactive AG Dividends Not included (Price index) Index Type Japan Calculation 09:00am to 10:30pm (CET), every 15 seconds Index Currency GBP History Available daily back to 02.05.2012 Index Members 338 FACTSHEET - AS OF 30-Sep-2021 Solactive L&G ESG Japan PR Index STATISTICS 30D 90D 180D 360D YTD Since Inception Performance 4.66% 5.64% 4.78% 15.98% 6.31% 126.15% Performance (p.a.) - - - - - 9.06% Volatility (p.a.) 17.26% 14.41% 15.32% 15.41% 15.59% 18.53% High 234.30 234.30 234.30 234.30 234.30 234.30 Low 216.07 207.97 199.97 191.99 199.97 92.54 Sharpe Ratio 4.29 1.72 0.64 1.03 0.52 0.47 Max. Drawdown -3.49% -3.76% -8.43% -10.85% -10.85% -21.65% VaR 95 \ 99 -27.5% \ -40.9% -29.2% \ -51.0% CVaR 95 \ 99 -34.7% \ -45.8% -43.3% \ -65.6% COMPOSITION BY CURRENCIES COMPOSITION BY COUNTRIES JPY 100.0% JP 100.0% TOP COMPONENTS AS OF 30-Sep-2021 Company Ticker Country Currency Index Weight (%) TOYOTA MOTOR CORP 7203 JT Equity JP JPY 5.47% SONY GROUP CORP 6758 JT Equity JP JPY 4.86% RECRUIT HOLDINGS CO LTD 6098 JT Equity JP JPY 3.65% TOKYO ELECTRON LTD ORD 8035 JT Equity JP JPY 2.27% SOFTBANK GROUP CORP 9984 JT Equity JP JPY 2.12% TAKEDA PHARMACEUTICAL 4502 JT Equity JP JPY 2.03% MITSUBISHI UFJ FINANCIAL GRO 8306 JT Equity JP JPY 2.01% KEYENCE CORP ORD 6861 JT Equity JP JPY 1.92% NIDEC CORP ORD 6594 JT Equity JP JPY 1.86% NIPPON TELEGRAPH & TELEPHONE ORD 9432 JT Equity JP JPY 1.80% FACTSHEET - AS OF 30-Sep-2021 Solactive L&G ESG Japan PR Index DISCLAIMER © Solactive AG, 2021. -

First Quarterly Report 2019/20 2019.9.1–2019.11.30 Stock Code: 6288 858638 (Fast Retailing 210X297) 中英分開排 \ 08/01/2020 \ X11 \ IFC

FAST RETAILING CO., LTD. 迅銷有限公司 First Quarterly Report 2019/20 2019.9.1–2019.11.30 Stock Code: 6288 858638 (Fast Retailing_210x297) 中英分開排 \ 08/01/2020 \ X11 \ IFC Contents 1. Corporate Profile 2 2. Financial Highlights 3 3. Management Discussion and Analysis 5 4. Information about the Reporting Entity 9 5. Financial Section 15 1. Interim Condensed Consolidated Financial Statements (1) Interim Condensed Consolidated Statement of 16 Financial Position (2) Interim Condensed Consolidated Statement of 17 Profit or Loss and Interim Condensed Consolidated Statement of Comprehensive Income Interim Condensed Consolidated Statement of 17 Profit or Loss Interim Condensed Consolidated Statement of 18 Comprehensive Income (3) Interim Condensed Consolidated Statement of 19 Changes in Equity (4) Interim Condensed Consolidated Statement of 21 Cash Flows 2. Others 34 Independent Accountant’s Review Report 35 858638 (Fast Retailing_210x297) 中英分開排 \ 08/01/2020 \ X11 \ P.2 1. Corporate Profile Board of Directors Principal Place of Business in Japan Executive Director Midtown Tower 9-7-1 Tadashi Yanai (Chairman of the Board of Directors, Akasaka, Minato-ku President and Chief Executive Officer) Tokyo 107-6231 Japan Directors Takeshi Okazaki Principal Place of Business in Hong Kong Kazumi Yanai 702–706, 7th Floor, Mira Place Tower A Koji Yanai No. 132 Nathan Road Tsim Sha Tsui Independent Directors Kowloon Toru Hambayashi (External) Hong Kong Nobumichi Hattori (External) Masaaki Shintaku (External) HDR Registrar and HDR Transfer Office Takashi Nawa (External) -

Hiroshi Miura

Hiroshi Miura Bengoshi Asia Pacific Counsel, Skadden Arps Law Office, Tokyo (registered associated office of Skadden Arps Foreign Law Office) Corporate Finance; Mergers and Acquisitions Hiroshi Miura’s practice focuses on corporate finance, general corporate matters, mergers and acquisitions (including transactions involving bank and other regulated companies), and equity finance (including initial public offerings and offerings of preferred securities). Mr. Miura’s experience includes representing Mitsui Sumitomo Insurance Co., Ltd. in its £3.46 billion acquisition of Amlin PLC; Nikkei Inc. in its £844 million acquisition of the Financial Times Group from Pearson PLC; Digital Garage, Inc., in its US$114 million going-private acquisition of its subsidiary econtext Asia Limited (Hong Kong); Marubeni Corporation in its US$2.7 billion (excluding debt) acquisition of Gavilon Group LLC and related preferred equity investment by Japan Bank for International Cooperation; NTT DOCOMO, Inc. in its US$290 million all cash tender offer for Buongiorno S.p.A. (Italy); Advantest Corporation in its US$1.1 billion acquisition of Verigy Ltd. (Singapore); TOMY T: 81.3.3568.2819 Company, Ltd. in its US$860 million acquisition of RC2 Corporation through an all-cash F: 1.917.777.5522 tender offer and related financing; andAioi Insurance Company, Limited in its business [email protected] combination with Nissay Dowa General Insurance Company, Limited and Mitsui Sumitomo Insurance Group Holdings, Inc. to form the largest non-life insurance company group in Japan. Mr. Miura also has represented prominent companies such as Toshiba Corporation, Education Westinghouse Electric UK Limited, CSK Holdings Corporation, DBS Group Holdings Diploma of Completion, the Legal Research and Training Institute of Ltd., Sekisui Chemical Co., Ltd., Hoya Corporation, Sumitomo Mitsui Financial Group the Supreme Court of Japan, 2005 and its subsidiary Sumitomo Mitsui Banking Corporation, TPG Capital, Inc. -

Chicago Board Options Exchange Annual Report 2001

01 Chicago Board Options Exchange Annual Report 2001 cv2 CBOE ‘01 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010 CBOE is the largest and 01010101010101010most successful options 01010101010101010marketplace in the world. 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010 01010101010101010ifc1 CBOE ‘01 ONE HAS OPPORTUNITIES The NUMBER ONE Options Exchange provides customers with a wide selection of products to achieve their unique investment goals. ONE HAS RESPONSIBILITIES The NUMBER ONE Options Exchange is responsible for representing the interests of its members and customers. Whether testifying before Congress, commenting on proposed legislation or working with the Securities and Exchange Commission on finalizing regulations, the CBOE weighs in on behalf of options users everywhere. As an advocate for informed investing, CBOE offers a wide array of educational vehicles, all targeted at educating investors about the use of options as an effective risk management tool. ONE HAS RESOURCES The NUMBER ONE Options Exchange offers a wide variety of resources beginning with a large community of traders who are the most experienced, highly-skilled, well-capitalized liquidity providers in the options arena. In addition, CBOE has a unique, sophisticated hybrid trading floor that facilitates efficient trading. 01 CBOE ‘01 2 CBOE ‘01 “ TO BE THE LEADING MARKETPLACE FOR FINANCIAL DERIVATIVE PRODUCTS, WITH FAIR AND EFFICIENT MARKETS CHARACTERIZED BY DEPTH, LIQUIDITY AND BEST EXECUTION OF PARTICIPANT ORDERS.” CBOE MISSION LETTER FROM THE OFFICE OF THE CHAIRMAN Unprecedented challenges and a need for strategic agility characterized a positive but demanding year in the overall options marketplace. The Chicago Board Options Exchange ® (CBOE®) enjoyed a record-breaking fiscal year, with a 2.2% growth in contracts traded when compared to Fiscal Year 2000, also a record-breaker. -

Comércio Eletrônico

Comércio Eletrônico Aula 1 - Overview of Electronic Commerce Learning Objectives 1. Define electronic commerce (EC) and describe its various categories. 2. Describe and discuss the content and framework of EC. 3. Describe the major types of EC transactions. 4. Describe the drivers of EC. 5. Discuss the benefits of EC to individuals, organizations, and society. 6. Discuss social computing. 7. Describe social commerce and social software. 8. Understand the elements of the digital world. 9. Describe some EC business models. 10. List and describe the major limitations of EC. Case: Starbucks Electronic Commerce (EC) EC refers to using the Internet and other networks (e.g., intranets) to purchase, sell, transport, or trade data, goods, or services. e-Business • Narrow definition of EC: buying and selling transactions between business partners. • e-Business refers to a broader definition of EC: – buying and selling of goods and services – Servicing customers – collaborating with business partners, – delivering e-learning, – conducting electronic transactions within organizations. – Among others e-Business Note: some view e-business only as comprising those activities that do not involve buying or selling over the Internet, i.e., a complement of the narrowly defined EC. Major EC Concepts: Non-EC vs. Pure EC vs. Partial EC • EC three major activities: – ordering and payments, – order fulfilment, and – delivery to customers. • pure EC: all activities are digital, • non-EC: none are digital, • otherwise, we have partial EC. Major EC Concepts: Pure -

Supply Chain Management Strategy and Organization

springer.com Mikihisa Nakano Supply Chain Management Strategy and Organization Uses the well-known framework of strategic management and organizational design: strategy–structure–process–performance Shows both the static side of supply chain management (SCM) and the dynamic side such as supply chain process change Includes case studies on Toyota and Nissan, Fujitsu, Ricoh, Daikin, Japan Tobacco, Kao, Fast Retailing, and Inditex This book explains supply chain management (SCM) using the strategy–structure–process– performance (SSPP) framework. Utilizing this well-known framework of contingency theory in the areas of strategic management and organizational design, SCM is firmly positioned among management theories. The author specifically proposes a theoretical foundation of SCM that will be relevant to such areas as operations management, logistics management, purchasing management, and marketing. Both the static and dynamic sides of SCM are reported. On the static side, supply chain strategies are divided into three patterns: efficiency-oriented, 1st ed. 2020, XVII, 239 p. 90 illus., 9 illus. responsiveness-oriented, and the hybrid efficiency- and responsiveness-oriented pattern. For in color. each strategy, suitable internal and external supply chain structures and processes are proposed. On the dynamic side, the big issue is to overcome performance trade-offs. Based on Printed book theories of organizational change, process change, and dynamic capabilities, the book presents Hardcover a model of supply chain process change. On structure, -

Nikkei Indexes Monthly Report (October 2012)

Nikkei Indexes Monthly Report November 1, 2012 Nikkei 225 in October As of the end of October, the Nikkei Stock Average (Nikkei 225) stood at 8928.29, up 58.13 points, or 0.66%, from the end of September. In the first part of month, the index fell to around the 8500 level due to concern over China-related risk etc. Afterwards the index continued to rise for 7 consecutive days from Oct 15 up to above 9000 for the first time in a month, in positive response to weakening yen and expectation of BOJ’s further monetary easing. Nikkei 225 was down to around 8900 due to profit taking selling later. This month’s Topic:Nikkei Stock Average (Nikkei 225) SONY to UNIQLO, tracing changes in leading companies In 1950, the Nikkei Stock Average, Nikkei 225 was first calculated and published. Since then, as the flagship index comprising of representative Japanese stocks, the Nikkei 225 has been used worldwide for media and market participants in varied ways. Analyzing the historical changes in its constituents and sectors shows clearly which companies have led the economy and stock market in Japan since the Second World War. Constituent reshuffles reflect industrial structure changes The Nikkei 225 is a price-weighted equity index, which consists of 225 stocks in the 1st section of the Tokyo Stock Exchange. The components have been reviewed regularly based on liquidity and sector balance for the purpose of reflecting changes in industrial structures appropriately while replacing with high liquidity stocks. To know more the Nikkei 225, please visit here. -

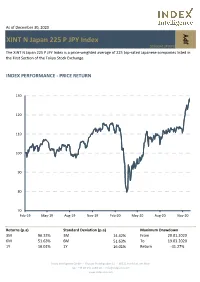

XINT N Japan 225 P JPY Index

As of December 30, 2020 XINT N Japan 225 P JPY Index JPY DE000A13PWP8 The XINT N Japan 225 P JPY Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. INDEX PERFORMANCE - PRICE RETURN 130 120 110 100 90 80 70 Feb-19 May-19 Aug-19 Nov-19 Feb-20 May-20 Aug-20 Nov-20 Returns (p.a) Standard Deviation (p.a) Maximum Drawdown 3M 96.33% 3M 14.42% From 20.01.2020 6M 51.63% 6M 51.63% To 19.03.2020 1Y 16.01% 1Y 16.01% Return -31.27% Index Intelligence GmbH - Grosser Hirschgraben 15 - 60311 Frankfurt am Main Tel.: +49 69 247 5583 50 - [email protected] www.index-int.com Top 10 Constituents FFMV (JPYm) Weight % Industry Sector Fast Retailing Co Ltd 5 12.13 Retail SoftBank Group Corp 2 6.34 Telecommunications Tokyo Electron Ltd 2 5.04 Technology FANUC Corp 1 3.33 Industrial Goods & Services M3 Inc 1 3.07 Health Care Daikin Industries Ltd 1 3.01 Construction & Materials KDDI Corp 1 2.41 Telecommunications Shin-Etsu Chemical Co Ltd 1 2.37 Chemicals Terumo Corp 1 2.26 Health Care Chugai Pharmaceutical Co Ltd 1 2.17 Health Care Total 16 42.13 This information has been prepared by Index Intelligence GmbH (“IIG”). All information is provided "as is" and IIG makes no express or implied warranties, and expressly disclaims all warranties of merchantability or fitness for a particular purpose or use with respect to any data included herein. -

Fast Retailing Policy on Wood-Derived Products and Forest

Fast Retailing Responsible Product Policy: Wood-based Products and Forest Materials Ancient and endangered forests regulate our planet – providing clean air, fresh water, a stable climate and biodiversity. Fast Retailing Co., Ltd. and our brands including UNIQLO, Theory, GU, PLST, Helmut Lang, Comptoir des Cotonniers, Princess tam.tam and J Brand are committed to protecting the world’s ancient and endangered forests including efforts toward zero deforestation through our approach to procurement of wood- based fabrics, materials derived from forests, and/or manmade cellulosic fabrics. Conservation of Ancient and Endangered Forests and Ecosystems While it is commonly known that paper and wood come from forests, it is a little known fact that trees are being made into clothing. Fabrics originating from forest sources are almost exclusively referring to viscose (also known as rayon), and other fabrics are also covered in this “man-made cellulosic fabric” family. Fast Retailing Co., Ltd. is committed to undertaking reasonable efforts in the following: 1. Assess and map our existing use of forest materials and eliminate sourcing identified as coming from endangered species habitat and ancient and endangered forests. 2. Work to eliminate sourcing from companies that are logging forests illegally or tree plantations established after 1994, from areas being logged in contravention of indigenous and local peoples’ rights, and/or from other suppliers identified by Fast Retailing as controversial. 3. Should we learn that any of our forest materials are being sourced from ancient and endangered forests, endangered species habitat or through illegal logging, we will investigate our supply chain, engage our suppliers to change practices, and/or re-evaluate our relationship with them. -

Items Stipulated for Internet Disclosure in Conjunction with the Notice of 2019 General Meeting of Shareholders

Items stipulated for internet disclosure in conjunction with the Notice of 2019 General Meeting of Shareholders ■ Business report Employees ………………………………………… 1 Principal Lenders ………………………………… 1 Items Relating to External Officers ………… 2 Independent Auditors …………………………… 3 Share Subscription Rights …………………… 5 Ensuring Proper Business Operations ……… 7 (Corporate Governance) ■ Consolidated Statement of …………………… 14 Changes in Equity ■ Notes to the Consolidated ……………………… 15 Financial Statements ■ Statement of Changes ………………………… 27 in Net Assets ■ Notes to Financial Statements………………… 28 These items are available for shareholders to view on our company website (https:// www.fastretailing.com/eng/ir) as stipulated by law and Fast Retailing’s Articles of Incorporation, No.15 FAST RETAILING CO., LTD Business report 1 Employees (as at 31 August 2019) (1)Employees of the Group Number of Employees Change from Previous Consolidated Fiscal Year 56,523 + 3,684 (Note) The number of employees does not include operating officers, junior employees, part-time workers or temporary staff seconded from other companies. (2)Employees of the Company Number of Change from Previous Average Years of Average Age Employees Fiscal Year Service 1,389 + 44 38 years and 4month 4 years and 7 months (Note) The number of employees does not include operating officers, junior employees, part-time workers or temporary staff seconded from other companies. 2 Principal Lenders (as at 31 August 2019) Lender Loan Balance Sumitomo Mitsui Financial Group, Inc. 3,759 million yen Mitsubishi UFJ Financial Group, Inc. 1,419 million yen Mizuho Financial Group, Inc. 315 million yen 1 3 Items Relating to External Officers (1)Relationship between the Company and companies where External Officers hold significant concurrent offices As stated in Section 2 2 (1)Directors and Statutory Auditors (as at 31 August 2019) of the Business Report included in the AGM Notice. -

NASD Notice to Members 99-46

Executive Summary $250, and two or more Market NASD Effective July 1, 1999, the maximum Ma k e r s . Small Order Execution SystemSM (S O E S SM ) order sizes for 336 Nasdaq In accordance with Rule 4710, Nas- Notice to National Market® (NNM) securities daq periodically reviews the maxi- will be revised in accordance with mum SOES order size applicable to National Association of Securities each NNM security to determine if Members Dealers, Inc. (NASD®) Rule 4710(g). the trading characteristics of the issue have changed so as to warrant For more information, please contact an adjustment. Such a review was 99-46 ® Na s d a q Market Operations at conducted using data as of March (203) 378-0284. 31, 1999, pursuant to the aforemen- Maximum SOES Order tioned standards. The maximum Sizes Set To Change SOES order-size changes called for Description by this review are being implemented July 1, 1999 Under Rule 4710, the maximum with three exceptions. SOES order size for an NNM security is 1,000, 500, or 200 shares, • First, issues were not permitted to depending on the trading characteris- move more than one size level. For Suggested Routing tics of the security. The Nasdaq example, if an issue was previously ® Senior Management Workstation II (NWII) indicates the categorized in the 1,000-share maximum SOES order size for each level, it would not be permitted to Ad v e r t i s i n g NNM security. The indicator “NM10,” move to the 200-share level, even if Continuing Education “NM5,” or “NM2” displayed in NWII the formula calculated that such a corresponds to a maximum SOES move was warranted. -

How Much Are Your Eyeballs Worth? Placing a Value on a Website's Customers May Be the Best Way to Judge a Net Stock

How Much Are Your Eyeballs Worth? Placing a value on a Website's customers may be the best way to judge a Net stock. It's not perfect, but on the Net, what is? By Erick Schonfeld February 21, 2000 (FORTUNE Magazine) – Internet CEOs crave many things: world domination, instant service in bistros, fawning media attention. But what they crave above all else is eyeballs. That's less ghoulish than it sounds. In Webspeak, you see, eyeballs mean customers. Since the typical dot- com lacks the one metric that Wall Street has traditionally used to evaluate companies (you remember--earnings) analysts and investors have contrived other ways to size up Net stocks. One now stands out: market capitalization per pair of eyeballs. It's a useful first step in explaining why a company garners a certain kind of valuation. For instance, a pair of eyeballs at Web portal Lycos, with a $7.4 billion market cap, has a value of just $244; at Schwab, which has a $30 billion market cap, a pair is worth $4,562 (ironically, this also happens to be around the price a pair of real human corneas reportedly commands on the black market). If the Internet market were rational, the market cap per eyeball would represent the total profit that you could reasonably expect a company to get from its average customer, adjusted for risk and the length of time before those profits are realized. Internet analysts are the first to admit that today's is not a rational market. So correlating the lifetime value of eyeballs to a fast-growing dot-com's stock price is not perfect science.