Form 1065, U.S. Return of Partnership Income

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Partnership Management & Project Portfolio Management

Partnership Management & Project Portfolio Management Partnerships and strategic management for projects, programs, quasi- projects, and operational activities In the digital age – we need appropriate socio-technical approaches, tools, and methods for: • Maintainability • Sustainability • Integration • Maturing our work activities At the conclusion of this one-hour session, participants will: • Be able to define partnership management and project portfolio management. • Be able to identify examples of governance models to support partnerships. • Be able to share examples of document/resource types for defining and managing partnerships within project portfolio management. • Be able to describe how equity relates to partnerships and partnership management. Provider, Partner, Pioneer Digital Scholarship and Research Libraries Provider, Partner, Pilgrim (those who journey, who wander and wonder) https://www.rluk.ac.uk/provider-partner-pioneer-digital-scholarship-and-the-role-of-the-research-library-symposium/ Partners and Partnership Management Partner: any individual, group or institution including governments and donors whose active participation and support are essential for the successful implementation of a project or program. Partnership Management: the process of following up on and maintaining effective, productive, and harmonious relationships with partners. It can be informal (phone, email, visits) or formal (written, signed agreements, with periodic review). What is most important is to: invest the time and resources needed to -

Partnership Agreement Example

Partnership Agreement Example THIS PARTNERSHIP AGREEMENT is made this __________ day of ___________, 20__, by and between the following individuals: Address: __________________________ ___________________________ City/State/ZIP:______________________ Address: __________________________ ___________________________ City/State/ZIP:______________________ 1. Nature of Business. The partners listed above hereby agree that they shall be considered partners in business for the following purpose: ______________________________________________________________________________ ______________________________________________________________________________ 2. Name. The partnership shall be conducted under the name of ________________ and shall maintain offices at [STREET ADDRESS], [CITY, STATE, ZIP]. 3. Day-To-Day Operation. The partners shall provide their full-time services and best efforts on behalf of the partnership. No partner shall receive a salary for services rendered to the partnership. Each partner shall have equal rights to manage and control the partnership and its business. Should there be differences between the partners concerning ordinary business matters, a decision shall be made by unanimous vote. It is understood that the partners may elect one of the partners to conduct the day-to-day business of the partnership; however, no partner shall be able to bind the partnership by act or contract to any liability exceeding $_________ without the prior written consent of each partner. 4. Capital Contribution. The capital contribution of -

8Th Metro World Summit 201317-18 April

30th Nov.Register to save before 8th Metro World $800 17-18 April Summit 2013 Shanghai, China Learning What Are The Series Speaker Operators Thinking About? Faculty Asia’s Premier Urban Rail Transit Conference, 8 Years Proven Track He Huawu Chief Engineer Record: A Comprehensive Understanding of the Planning, Ministry of Railways, PRC Operation and Construction of the Major Metro Projects. Li Guoyong Deputy Director-general of Conference Highlights: Department of Basic Industries National Development and + + + Reform Commission, PRC 15 30 50 Yu Guangyao Metro operators Industry speakers Networking hours President Shanghai Shentong Metro Corporation Ltd + ++ Zhang Shuren General Manager 80 100 One-on-One 300 Beijing Subway Corporation Metro projects meetings CXOs Zhang Xingyan Chairman Tianjin Metro Group Co., Ltd Tan Jibin Chairman Dalian Metro Pak Nin David Yam Head of International Business MTR C. C CHANG President Taoyuan Metro Corp. Sunder Jethwani Chief Executive Property Development Department, Delhi Metro Rail Corporation Ltd. Rachmadi Chief Engineering and Project Officer PT Mass Rapid Transit Jakarta Khoo Hean Siang Executive Vice President SMRT Train N. Sivasailam Managing Director Bangalore Metro Rail Corporation Ltd. Endorser Register Today! Contact us Via E: [email protected] T: +86 21 6840 7631 W: http://www.cdmc.org.cn/mws F: +86 21 6840 7633 8th Metro World Summit 2013 17-18 April | Shanghai, China China Urban Rail Plan 2012 Dear Colleagues, During the "12th Five-Year Plan" period (2011-2015), China's national railway operation of total mileage will increase from the current 91,000 km to 120,000 km. Among them, the domestic urban rail construction showing unprecedented hot situation, a new round of metro construction will gradually develop throughout the country. -

Limited Liability Partnerships

inbrief Limited Liability Partnerships Inside Key features Incorporation and administration Members’ Agreements Taxation inbrief Introduction Key features • any members’ agreement is a confidential Introduction document; and It first became possible to incorporate limited Originally conceived as a vehicle liability partnerships (“LLPs”) in the UK in 2001 • the accounting and filing requirements are for use by professional practices to after the Limited Liability Partnerships Act 2000 essentially the same as those for a company. obtain the benefit of limited liability came into force. LLPs have an interesting An LLP can be incorporated with two or more background. In the late 1990s some of the major while retaining the tax advantages of members. A company can be a member of an UK accountancy firms faced big negligence claims a partnership, LLPs have a far wider LLP. As noted, it is a distinct legal entity from its and were experiencing a difficult market for use as is evidenced by their increasing members and, accordingly, can contract and own professional indemnity insurance. Their lobbying property in its own right. In this respect, as in popularity as an alternative business of the Government led to the introduction of many others, an LLP is more akin to a company vehicle in a wide range of sectors. the Limited Liability Partnerships Act 2000 which than a partnership. The members of an LLP, like gave birth to the LLP as a new business vehicle in the shareholders of a company, have limited the UK. LLPs were originally seen as vehicles for liability. As he is an agent, when a member professional services partnerships as demonstrated contracts on behalf of the LLP, he binds the LLP as by the almost immediate conversion of the major a director would bind a company. -

Basic Concepts Page 1 PARTNERSHIP ACCOUNTING

Dr. M. D. Chase Long Beach State University Advanced Accounting 1305-87B Partnership Accounting: Basic Concepts Page 1 PARTNERSHIP ACCOUNTING I. Basic Concepts of Partnership Accounting A. What is A Partnership?: An association of two or more persons to carry on as co-owners of a business for a profit; the basic rules of partnerships were defined by Congress: 1. Uniform Partnership Act of 1914 (general partnerships) 2. Uniform Limited Partnership Act of 1916 (limited partnerships) B. Characteristics of a Partnership: 1. Limited Life--dissolved by death, retirement, incapacity, bankruptcy etc 2. Mutual agency--partners are bound by each others’ acts 3. Unlimited Liability of the partners--the partnership is not a legal or taxable entity and therefore all debts and legal matters are the responsibility of the partners. 4. Co-ownership of partnership assets--all assets contributed to the partnership are owned by the individual partners in accordance with the terms of the partnership agreement; or equally if no agreement exists. C. The Partnership Agreement: A contract (oral or written) which can be used to modify the general partnership rules; partnership agreements at a minimum should cover the following: 1. Names or Partners and Partnership; 2. Effective date of the partnership contract and date of termination if applicable; 3. Nature of the business; 4. Place of business operations; 5. Amount of each partners capital and the valuation of each asset contributed and date the valuation was made; 6. Rights and responsibilities of each partner; 7. Dates of partnership accounting period; minimum capital investments for each partner and methods of determining equity balances (average, weighted average, year-end etc.) 8. -

Limited Partnerships

INTELLECTUAL PROPERTY AND TRANSACTIONAL LAW CLINIC LIMITED PARTNERSHIPS INTRODUCTORY OVERVIEW A limited partnership is a business entity comprised of two or more persons, with one or more general partners and one or more limited partners. A limited partnership differs from a general partnership in the amount of control and liability each partner has. Limited partnerships are governed by the Virginia Revised Uniform Partnership Act,1 which is an adaptation of the 1976 Revised Uniform Limited Partnership Act, or RULPA, and its subsequent amendments. HOW A LIMITED PARTNERSHIP IS FORMED To form a limited partnership in Virginia, a certificate of limited partnership must be filed with the Virginia State Corporation Commission. This is different from general partnerships which require no formal recording with the Commonwealth. The certificate must state the name of the partnership,2 and, the name must contain the designation “limited partnership,” “a limited partnership,” “L.P.,” or “LP;” which puts third parties on notice of the limited liability of one or more partners. 3 Additionally, the certificate must name a registered agent for service of process, state the Post Office mailing address of the company, and state the name and address of every general partner. The limited partnership is formed on the date of filing of the certificate unless a later date is specified in the certificate.4 1 VA. CODE ANN. § 50, Ch. 2.2. 2 VA. CODE ANN. § 50-73.11(A)(1). 3 VA. CODE ANN. § 50-73.2. 4 VA. CODE ANN. § 50-73.11(C)0). GENERAL PARTNERS General partners run the company's day-to-day operations and hold management control. -

China Railway Signal & Communication Corporation

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. China Railway Signal & Communication Corporation Limited* 中國鐵路通信信號股份有限公司 (A joint stock limited liability company incorporated in the People’s Republic of China) (Stock Code: 3969) ANNOUNCEMENT ON BID-WINNING OF IMPORTANT PROJECTS IN THE RAIL TRANSIT MARKET This announcement is made by China Railway Signal & Communication Corporation Limited* (the “Company”) pursuant to Rules 13.09 and 13.10B of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited (the “Listing Rules”) and the Inside Information Provisions (as defined in the Listing Rules) under Part XIVA of the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong). From July to August 2020, the Company has won the bidding for a total of ten important projects in the rail transit market, among which, three are acquired from the railway market, namely four power integration and the related works for the CJLLXZH-2 tender section of the newly built Langfang East-New Airport intercity link (the “Phase-I Project for the Newly-built Intercity Link”) with a tender amount of RMB113 million, four power integration and the related works for the XJSD tender section of the newly built -

Anonymous Referee #1

Anonymous Referee #1 This manuscript is well written. I recommend it be published with a few minor edits. We thank the reviewer for their positive comments and suggestions. Please find below our replies and the related modifications to the manuscript. The page and line numbers refer to the version of the manuscript published on 5 ACPD. Section 2.2: Go into more depth how the footprints and the emissions inventory are combined to obtain atmospheric concentrations of CO. The text below has been added to the section 2.2 (P5, l3): “To do this, first we derive the sensitivities of the measured air masses to emissions occurring within a grid cell 10 (units [gm−3] / [gm−2s−1], i.e. sm−1) and then by multiplying the sensitivities with the emissions from the emission inventories we are able to calculate the modelled CO concentration (dimensionally, sm−1 × gm−2s−1 = gm−3). To convert the concertation to a volume mixing ratio we divide the modelled concentrations by the molar mass, divide again by the air density and multiply by 1 x 109.” Figure 4: Black box referred to in caption is not visible. 15 Figure 4 “black box” – that was a mistake in the caption. Caption for Figure 4 (P5) corrected to say: “Figure 4: The blue box represents the regional contributions from outside Beijing and the red box is the Beijing region. The map also shows the 2010 population census (people per pixel – WorldPop data)” Page 6, line 10: change the time resolution of 1 Hz to an actual time resolution (in hours, minutes, or seconds). -

Effects of Partner Characteristic, Partnership Quality, and Partnership Closeness on Cooperative Performance: a Study of Supply Chains in High-Tech Industry

Management Review: An International Journal Volume 4 Number 2 Winter 2009 Effects of Partner Characteristic, Partnership Quality, and Partnership Closeness on Cooperative Performance: A Study of Supply Chains in High-tech Industry Mei-Ying Wu Department of Information Management Chung-Hua University Hsin-Chu Taiwan, Republic of China Email: [email protected] Yun-Ju Chang Department of Information Management Chung-Hua University Hsin-Chu Taiwan, Republic of China Email: [email protected] Yung-Chien Weng Department of Information Management Chung-Hua University Hsin-Chu Taiwan, Republic of China Email: [email protected] Received May 28, 2009; Revised Aug. 14, 2009; Accepted Oct. 21, 2009 ABSTRACT Owing to the rapid development of information technology, change of supply chain structures, trend of globalization, and intense competition 29 Management Review: An International Journal Volume 4 Number 2 Winter 2009 in the business environment, almost all enterprises have been confronted with unprecedented challenges in recent years. As a coping strategy, many of them have gradually viewed suppliers as “cooperative partners”. They drop the conventional strategy of cooperating with numerous suppliers and build close partnerships with only a small number of selected suppliers. This paper aims to explore partnerships between manufacturers and suppliers in Taiwan’s high- tech industry. Through a review of literature, four constructs, including partner characteristic, partnership quality, partnership closeness, and cooperative performance are extracted to be the basis of the research framework, hypotheses, and questionnaire. The questionnaire is administered to staff of the purchasing and quality control departments in some high-tech companies in Taiwan. The proposed hypotheses are later empirically validated using confirmatory factor analysis (CFA) and structural equation modeling (SEM). -

ACCOUNTING for PARTNERSHIPS and LIMITED LIABILITY CORPORATIONS Objectives

13 ACCOUNTING FOR PARTNERSHIPS AND LIMITED LIABILITY CORPORATIONS objectives After studying this chapter, you should be able to: Describe the basic characteristics of 1 proprietorships, corporations, partner- ships, and limited liability corpora- tions. Describe and illustrate the equity re- 2 porting for proprietorships, corpora- tions, partnerships, and limited liability corporations. Describe and illustrate the accounting 3 for forming a partnership. Describe and illustrate the accounting 4 for dividing the net income and net loss of a partnership. Describe and illustrate the accounting 5 for the dissolution of a partnership. Describe and illustrate the accounting 6 for liquidating a partnership. Describe the life cycle of a business, 7 including the role of venture capital- ists, initial public offerings, and under- writers. PHOTO: © EBBY MAY/STONE/GETTY IMAGES IIf you were to start up any type of business, you would want to separate the busi- ness’s affairs from your personal affairs. Keeping business transactions separate from personal transactions aids business analysis and simplifies tax reporting. For example, if you provided freelance photography services, you would want to keep a business checking account for depositing receipts for services rendered and writing checks for expenses. At the end of the year, you would have a basis for determining the earn- ings from your business and the information necessary for completing your tax re- turn. In this case, forming the business would be as simple as establishing a name and a separate checking account. As a business becomes more complex, the form of the business entity becomes an important consideration. The entity form has an im- pact on the owners’ legal liability, taxation, and the ability to raise capital. -

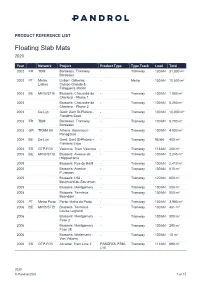

Floating Slab Mats 2020

PRODUCT REFERENCE LIST Floating Slab Mats 2020 Year Network Project Product Type Type Track Load Total 2002 FR TBM Bordeaux: Tramway - Tramway 100 kN 31,000 m² Bordeaux 2002 PT Metro Lisbon: Odivelas, - Metro 100 kN 10,000 m² Lisboa Campo Grande & Falagueira station 2003 BE MIVB/STIB Brussels: Chaussée de - Tramway 100 kN 1,800 m² Charleroi - Phase 1 2003 Brussels: Chaussée de - Tramway 100 kN 5,250 m² Charleroi - Phase 2 2003 De Lijn Gent: Gent St-Pieters - - Tramway 100 kN 10,000 m² Flanders Expo 2003 FR TBM Bordeaux: Tramway - Tramway 130 kN 9,700 m² Bordeaux 2003 GR TRAM SA Athens: Kasamouli - - Tramway 100 kN 4,000 m² Panagitsas 2004 BE De Lijn Gent: Gent St-Pieters - - Tramway 95 kN 400 m² Flanders Expo 2004 ES GTP-FGV Valencia: Tram Valencia - Tramway 113 kN 200 m² 2005 BE MIVB/STIB Brussels: Avenue de - Tramway 100 kN 2,245 m² l'Hippodrome 2005 Brussels: Rue du Bailli - Tramway 100 kN 2,410 m² 2005 Brussels: Avenue - Tramway 100 kN 610 m² P.Janson 2005 Brussels: L94 - - Tramway 120 kN 600 m² Boulevard du Souverain 2005 Brussels: Montgomery - Tramway 100 kN 250 m² 2005 Brussels: Terminus - Tramway 100 kN 550 m² Boondael 2005 PT Metro Porto Porto: Metro do Porto - Tramway 100 kN 3,900 m² 2006 BE MIVB/STIB Brussels: Terminus - Tramway 130 kN 481 m² Louise Legrand 2006 Brussels: Montgomery - Tramway 100 kN 300 m² Fase 2 2006 Brussels: Montgomery - Tramway 100 kN 290 m² Fase 2E 2006 Brussels: Wielemans - - Tramway 100 kN 15 m² Van Volxem 2006 ES GTP-FGV Alicante: Tram Line 2 PANDROL FSM- Tramway 113 kN 690 m² L10 2020 © Pandrol 2020 -

Appendix a Monorail Database Formatted 1.13.2020.Xlsx

Appendix A Global Scan Summary Number and Type Location Year Open Length # Stations Ridership (Daily Average) Ridership (Annual) Speed Travel Time Design/Construction Cost Infrastructure Technology/Guidence System of Vehicles Australia, 1989 (Closed 2017) Straddle-beam Steel box beam Broadbeach Australia, Queensland, Sea 1986 1.2 miles 2 17 mph $3M (Australian) 3, 9-car trains Straddle-beam Von Roll Mk II World 500 V AV power, generator provided to clear trains in emergencies. Built to operate 12 minutes (entire Von Roll Type III, 6, Australia, Sydney 1988 (Closed 2013) 2.24 miles 8 70 million (lifetime) 21 mph (average) $55 million USD Straddle-beam autonomously, breakdowns loop) 7-car trains (construction) soon after opening led to $10-15 million USD decision to retain drivers for (demolish) each train Approx. $550,000 dollars Belgium, Lichtaart 1975 1.15 miles 3 4.7 mph 15 minutes Straddle-beam Schwarzkopf (1978) 2021 (proposed Capacity of 150,000 $650 million Brazil, Salvador 12.4 miles 22 Straddle-beam BYD Skyrail estimate) passengers a day (approximately) 54 seven-car trains 500,000 (estimated once fully $1.6 billion (estimated for Brazil, Sao Paulo, 12 min (50 minutes (total once Phase 1: 2016 4.7 miles (out of 17 6 (out of 18 completed) entire project, not clear CITYFLO 650 automatic train Line 15 (Expresso 50 mph (average) end to end once completed), Straddle-beam Phase 2: 2018 miles planned) planned) 40,000 passengers per hour what is included in this control Tiradentes) fully completed) Bombardier Innova per direction amount)