View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

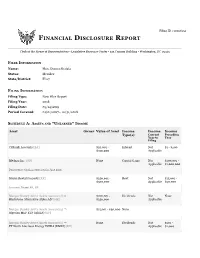

Financial Disclosure Report

Filing ID #10026155 financial DiScloSure report Clerk of the House of Representatives • Legislative Resource Center • 135 Cannon Building • Washington, DC 20515 filer information name: Hon. Donna Shalala Status: Member State/District: FL27 filing information filing type: New Filer Report filing year: 2018 filing Date: 05/14/2019 period covered: 01/01/2017– 12/31/2018 ScheDule a: aSSetS anD "unearneD" income asset owner Value of asset income income income type(s) current preceding year to year filing Citibank Accounts [BA] $50,001 - Interest Not $1 - $200 $100,000 Applicable Mednax Inc. [OP] None Capital Gains Not $100,001 - Applicable $1,000,000 DESCRIPTION: Options exercised in June 2018. Miami Rental Property [RP] $250,001 - Rent Not $15,001 - $500,000 Applicable $50,000 LOCATION: Miami, FL, US Morgan Stanley Active Assets Account (1) ⇒ $100,001 - Dividends Not None Blackstone Alternative Alpha Adv [HE] $250,000 Applicable Morgan Stanley Active Assets Account (2) ⇒ $15,001 - $50,000 None Algerian MLP ETF (AMLP) [EF] Morgan Stanley Active Assets Account (2) ⇒ None Dividends Not $201 - FT North American Energy INFRA (EMLP) [EF] Applicable $1,000 asset owner Value of asset income income income type(s) current preceding year to year filing Morgan Stanley Active Assets Account (2) ⇒ $50,001 - None ISHARES CORE MSCI EUROPE (IEUR) [EF] $100,000 Morgan Stanley Active Assets Account (2) ⇒ $15,001 - $50,000 Dividends Not $1,001 - ISHARES EDGE MSCI MIN VOL EAFE (EFAV) [EF] Applicable $2,500 Morgan Stanley Active Assets Account (2) ⇒ $15,001 - -

S P O T L I G H T Pa R T I C I Pa N

SPOTLIGHT PARTICIPANTS 12 Copyright © 2019 Mercer (US) Inc. All rights reserved. ORGANIZATION LISTING 3M (Minnesota Mining & Manufacturing) Atlas Energy Group LLC City of Overland Park, KS Cleveland Indians Baseball Co. A&E Television Networks Auburn University City of Winston-Salem, NC CliftonLarsonAllen, LLP A.O. Smith Corporation Automatic Data Processing California Health Care Foundation CMA CGM (America) LLC American Automobile Association, Inc., The Automobile Club of Southern California Cabot Oil & Gas Corporation CNH Industrial America LLC Accenture LLP AXA XL Cactus Feeders, Inc. CNO Financial Group Accudyne Industries, LLC Badger Meter, Inc. Cadmus Holding Company CNOOC Petroleum U.S.A. Inc. Advance Auto Parts Baltimore Orioles California Endowment, The CNX Resources ADVICS North America, Inc. Bank of the Ozarks, Inc. California ISO Colorado Rockies Baseball Club AECOM Building & Construction Bank of New York Mellon California Wellness Foundation Cobb Electric Membership Corporation AECOM Enterprise Baptist Health - FL Cambia Health Solutions (Regence Group) Coca-Cola Company, Inc., The AECOM Management Services Crestline Hotels & Resorts, LLC Canadian Imperial Bank of Commerce COG Operating, LLC Aera Energy Services Company Barnes & Noble, Inc. Canadian National Cognizant Technology Solutions Corporation Affinity Federal Credit Union BASF Corporation Canadian Pacific Railway CohnReznick LLP AgReserves Inc. Basin Electric Power Co-op Canadian Solar, Inc. Colby College Agri Beef Company Bates College Capital Group Companies, Inc., The Colonial Group, Inc. American International Group, Inc. (AIG) Battelle Memorial Institute Capital One Financial Corporation Columbia Sportswear Company Aimbridge Hospitality Baylor College of Medicine CarMax Auto Superstores, Inc. Columbia University American Institutes for Research BB&T Corporation Carilion Clinic Columbus McKinnon Corporation Air Liquide USA Blue Cross Blue Shield of Kansas Carrix, Inc. -

March 31, 2021

Units Cost Market Value US Equity Index Fund US Equities 95.82% Domestic Common Stocks 10X GENOMICS INC 126 10,868 24,673 1LIFE HEALTHCARE INC 145 6,151 4,794 2U INC 101 5,298 4,209 3D SYSTEMS CORP 230 5,461 9,193 3M CO 1,076 182,991 213,726 8X8 INC 156 2,204 4,331 A O SMITH CORP 401 17,703 28,896 A10 NETWORKS INC 58 350 653 AAON INC 82 3,107 5,132 AARON'S CO INC/THE 43 636 1,376 ABBOTT LABORATORIES 3,285 156,764 380,830 ABBVIE INC 3,463 250,453 390,072 ABERCROMBIE & FITCH CO 88 2,520 4,086 ABIOMED INC 81 6,829 25,281 ABM INDUSTRIES INC 90 2,579 3,992 ACACIA RESEARCH CORP 105 1,779 710 ACADIA HEALTHCARE CO INC 158 8,583 9,915 ACADIA PHARMACEUTICALS INC 194 6,132 4,732 ACADIA REALTY TRUST 47 1,418 1,032 ACCELERATE DIAGNOSTICS INC 80 1,788 645 ACCELERON PHARMA INC 70 2,571 8,784 ACCO BRANDS CORP 187 1,685 1,614 ACCURAY INC 64 483 289 ACI WORLDWIDE INC 166 3,338 6,165 ACTIVISION BLIZZARD INC 1,394 52,457 133,043 ACUITY BRANDS INC 77 13,124 14,401 ACUSHNET HOLDINGS CORP 130 2,487 6,422 ADAPTHEALTH CORP 394 14,628 10,800 ADAPTIVE BIOTECHNOLOGIES CORP 245 11,342 10,011 ADOBE INC 891 82,407 521,805 ADT INC 117 716 1,262 ADTALEM GLOBAL EDUCATION INC 99 4,475 3,528 ADTRAN INC 102 2,202 2,106 ADVANCE AUTO PARTS INC 36 6,442 7,385 ADVANCED DRAINAGE SYSTEMS INC 116 3,153 13,522 ADVANCED ENERGY INDUSTRIES INC 64 1,704 7,213 ADVANCED MICRO DEVICES INC 2,228 43,435 209,276 ADVERUM BIOTECHNOLOGIES INC 439 8,321 1,537 AECOM 283 12,113 17,920 AERIE PHARMACEUTICALS INC 78 2,709 1,249 AERSALE CORP 2,551 30,599 31,785 AES CORP/THE 1,294 17,534 33,735 AFFILIATED -

DTC Participant Alphabetical Listing June 2019.Xlsx

DTC PARTICPANT REPORT (Alphabetical Sort ) Month Ending - June 30, 2019 PARTICIPANT ACCOUNT NAME NUMBER ABN AMRO CLEARING CHICAGO LLC 0695 ABN AMRO SECURITIES (USA) LLC 0349 ABN AMRO SECURITIES (USA) LLC/A/C#2 7571 ABN AMRO SECURITIES (USA) LLC/REPO 7590 ABN AMRO SECURITIES (USA) LLC/ABN AMRO BANK NV REPO 7591 ALPINE SECURITIES CORPORATION 8072 AMALGAMATED BANK 2352 AMALGAMATED BANK OF CHICAGO 2567 AMHERST PIERPONT SECURITIES LLC 0413 AMERICAN ENTERPRISE INVESTMENT SERVICES INC. 0756 AMERICAN ENTERPRISE INVESTMENT SERVICES INC./CONDUIT 7260 APEX CLEARING CORPORATION 0158 APEX CLEARING CORPORATION/APEX CLEARING STOCK LOAN 8308 ARCHIPELAGO SECURITIES, L.L.C. 0436 ARCOLA SECURITIES, INC. 0166 ASCENSUS TRUST COMPANY 2563 ASSOCIATED BANK, N.A. 2257 ASSOCIATED BANK, N.A./ASSOCIATED TRUST COMPANY/IPA 1620 B. RILEY FBR, INC 9186 BANCA IMI SECURITIES CORP. 0136 BANK OF AMERICA, NATIONAL ASSOCIATION 2236 BANK OF AMERICA, NA/GWIM TRUST OPERATIONS 0955 BANK OF AMERICA/LASALLE BANK NA/IPA, DTC #1581 1581 BANK OF AMERICA NA/CLIENT ASSETS 2251 BANK OF CHINA, NEW YORK BRANCH 2555 BANK OF CHINA NEW YORK BRANCH/CLIENT CUSTODY 2656 BANK OF MONTREAL, CHICAGO BRANCH 2309 BANKERS' BANK 2557 BARCLAYS BANK PLC NEW YORK BRANCH 7263 BARCLAYS BANK PLC NEW YORK BRANCH/BARCLAYS BANK PLC-LNBR 8455 BARCLAYS CAPITAL INC. 5101 BARCLAYS CAPITAL INC./LE 0229 BB&T SECURITIES, LLC 0702 BBVA SECURITIES INC. 2786 BETHESDA SECURITIES, LLC 8860 # DTCC Confidential (Yellow) DTC PARTICPANT REPORT (Alphabetical Sort ) Month Ending - June 30, 2019 PARTICIPANT ACCOUNT NAME NUMBER BGC FINANCIAL, L.P. 0537 BGC FINANCIAL L.P./BGC BROKERS L.P. 5271 BLOOMBERG TRADEBOOK LLC 7001 BMO CAPITAL MARKETS CORP. -

NASDAQ Stock Market

Nasdaq Stock Market Friday, December 28, 2018 Name Symbol Close 1st Constitution Bancorp FCCY 19.75 1st Source SRCE 40.25 2U TWOU 48.31 21st Century Fox Cl A FOXA 47.97 21st Century Fox Cl B FOX 47.62 21Vianet Group ADR VNET 8.63 51job ADR JOBS 61.7 111 ADR YI 6.05 360 Finance ADR QFIN 15.74 1347 Property Insurance Holdings PIH 4.05 1-800-FLOWERS.COM Cl A FLWS 11.92 AAON AAON 34.85 Abiomed ABMD 318.17 Acacia Communications ACIA 37.69 Acacia Research - Acacia ACTG 3 Technologies Acadia Healthcare ACHC 25.56 ACADIA Pharmaceuticals ACAD 15.65 Acceleron Pharma XLRN 44.13 Access National ANCX 21.31 Accuray ARAY 3.45 AcelRx Pharmaceuticals ACRX 2.34 Aceto ACET 0.82 Achaogen AKAO 1.31 Achillion Pharmaceuticals ACHN 1.48 AC Immune ACIU 9.78 ACI Worldwide ACIW 27.25 Aclaris Therapeutics ACRS 7.31 ACM Research Cl A ACMR 10.47 Acorda Therapeutics ACOR 14.98 Activision Blizzard ATVI 46.8 Adamas Pharmaceuticals ADMS 8.45 Adaptimmune Therapeutics ADR ADAP 5.15 Addus HomeCare ADUS 67.27 ADDvantage Technologies Group AEY 1.43 Adobe ADBE 223.13 Adtran ADTN 10.82 Aduro Biotech ADRO 2.65 Advanced Emissions Solutions ADES 10.07 Advanced Energy Industries AEIS 42.71 Advanced Micro Devices AMD 17.82 Advaxis ADXS 0.19 Adverum Biotechnologies ADVM 3.2 Aegion AEGN 16.24 Aeglea BioTherapeutics AGLE 7.67 Aemetis AMTX 0.57 Aerie Pharmaceuticals AERI 35.52 AeroVironment AVAV 67.57 Aevi Genomic Medicine GNMX 0.67 Affimed AFMD 3.11 Agile Therapeutics AGRX 0.61 Agilysys AGYS 14.59 Agios Pharmaceuticals AGIO 45.3 AGNC Investment AGNC 17.73 AgroFresh Solutions AGFS 3.85 -

Announcement February 22, 2019

Announcement February 22, 2019 Indxx USA Regional Banking Index will be reconstituted after the close of trading hours on February 28, 2019. Listed below are the constituents that will be added to the existing index: S.No ISIN Company Name 1 US5116561003 Lakeland Financial Corporation 2 US42234Q1022 Heartland Financial USA, Inc. 3 US3369011032 1st Source Corporation 4 US89214P1093 TowneBank 5 US4461501045 Huntington Bancshares Incorporated 6 US1637311028 Chemical Financial Corporation 7 US2298991090 Cullen/Frost Bankers, Inc. 8 US1176651099 Bryn Mawr Bank Corporation 9 US72346Q1040 Pinnacle Financial Partners, Inc. 10 US90539J1097 Union Bankshares Corporation 11 US81768T1088 ServisFirst Bancshares Inc 12 US06652K1034 BankUnited, Inc. 13 US6952631033 PacWest Bancorp 14 US9897011071 Zions Bancorporation, N.A. 15 US05945F1030 BancFirst Corporation 16 US15201P1093 CenterState Bank Corporation Listed below are the constituents that will be deleted from the existing index: S.No ISIN Company Name 1 US03076K1088 Ameris Bancorp 2 US05561Q2012 BOK Financial Corporation 3 US1011191053 Boston Private Financial Holdings, Inc. 4 US1547604090 Central Pacific Financial Corp. 5 US1972361026 Columbia Banking System, Inc. 6 US2937121059 Enterprise Financial Services Corp 7 US3198291078 First Commonwealth Financial Corporation 8 US3202091092 First Financial Bancorp. 9 US3205171057 First Horizon National Corporation 10 US52471Y1064 LegacyTexas Financial Group, Inc. 11 US7838591011 S&T Bancorp, Inc. 12 US8404411097 South State Corporation 13 US84470P1093 Southside Bancshares, Inc. 14 US9027881088 UMB Financial Corporation 15 US9197941076 Valley National Bancorp Listed below are the new index constituents that will be effective at the close of trading hours on February 28, 2019. Weights as of S.No ISIN Company Name Feb 21, 2019 1 US1491501045 Cathay General Bancorp 2.00% 2 US8984021027 Trustmark Corporation 2.00% 3 US4590441030 International Bancshares Corporation 2.00% 4 US1266001056 CVB Financial Corp. -

Closed Merged and Renamed Bank Holding Company of Oklahoma 11

Closed Merged and Renamed Bank Holding Company Of Oklahoma 11-30-2004 Ada First Ada Bancshares Inc. Merged into Vision Bancshares Inc., Ada 02-10-1972 Ada Tommie Maines, C.C. Collier, Closed J. M. Carter 11-06-1999 Ada Oklahoma State Bancorporation Merged into First United Bank and Trust Company, Durant 12-28-1998 Adair Commerce Bancshares Relocated to Catoosa 09-30-1994 Alex First Alex Bancshares, Inc. Merged into First Independence Bancorp, Chickasha 05-01-2003 Allen Allen Bancshares Merged into Farmers State Bank, Allen 06-16-1997 Altus Altus NBC Corp Changed name to NBC Corp of Oklahoma, Oklahoma City 07-31-2009 Altus FSB Bancorporation Closed 03-18-2004 Altus NBC Corp of Oklahoma, OKC Relocated to Oklahoma City. 09-01-1994 Anadarko Anadarko Bancshares, Inc. Merged into Falcon Bancorp. Inc., Anadarko 08-01-2015 Anadarko Falcon Bancorp. Inc. On this day, deregistered as a bank holding company, as a result of the merger of its bank (Anadarko Bank & Trust Co).into Bank of Commerce, Duncan. 01-30-1989 Antlers First Antlers Closed 09-30-1992 Apache First Apache Bancshares, Inc. Merged into First Bank of Apache, Apache. See bank entry to find out what happen to this institution. 06-30-1992 Ardmore Exchange Financial Corporation Merged into Security Corporation, Duncan which on 10-01-1998 merged into BancFirst Corporation, Oklahoma City. 06-30-1992 Ardmore Exchange National Corporation Merged into Security Corporation, Duncan which on 10-01-1998 merged 11/13/2020 Page 1 of 29 Closed Merged and Renamed Bank Holding Company Of Oklahoma into BancFirst Corporation, Oklahoma City. -

BOK Financial Corporation 2021 Proxy Statement

March 25, 2021 To Our Shareholders: The Annual Meeting of Shareholders of BOK Financial Corporation will be held this year on Tuesday, May 4, 2021, at 2:30 p.m. Central Time as a virtual meeting of shareholders. You will be able to participate in the meeting, vote, and submit questions during the meeting via live webcast by visiting www.virtualshareholdermeeting.com/BOKF2021 and entering your secure control number, which can be found on the enclosed proxy card. Details of the business to be conducted at the annual meeting are given in the attached Notice of Annual Meeting and Proxy Statement. Also enclosed is our Annual Report to Shareholders, covering the fiscal year ended December 31, 2020. We hope that you will be able to attend this meeting via live webcast, but all shareholders, whether or not they expect to attend the meeting, are requested to complete, date and sign the enclosed proxy and return it in the enclosed envelope as promptly as possible. Sincerely, George B. Kaiser, Chairman of the Board of Directors Steven G. Bradshaw, President and Chief Executive Officer BOK Financial Corporation | 1 TABLE OF CONTENTS NOTICE OF ANNUAL MEETING OF SHAREHOLDERS 4 PROXY STATEMENT FOR ANNUAL MEETING OF SHAREHOLDERS 5 General 5 Voting by Proxy 5 Voting and Quorum Requirements at the Meeting 5 Solicitation of Proxies 6 Annual Report 6 Principal Shareholders of the Company 6 Security Ownership of Certain Beneficial Owners and Management 7 PROPOSAL ONE - ELECTION OF DIRECTORS 9 Nominees and Vote Required to Elect Nominees 9 Term of Office 9 -

SCHEDULE of INVESTMENTS MID-CAP 1.5X STRATEGY FUND

SCHEDULE OF INVESTMENTS December 31, 2020 MID-CAP 1.5x STRATEGY FUND SHARES VALUE SHARES VALUE COMMON STOCKS† - 39.5% United Bankshares, Inc. 118 $ 3,823 Kinsale Capital Group, Inc. 19 3,802 FINANCIAL - 9.3% Highwoods Properties, Inc. REIT 95 3,765 Medical Properties Trust, Inc. REIT 489 $ 10,655 RLI Corp. 36 3,749 Brown & Brown, Inc. 215 10,193 Park Hotels & Resorts, Inc. REIT 215 3,687 Camden Property Trust REIT 89 8,893 Selective Insurance Group, Inc. 55 3,684 CyrusOne, Inc. REIT 110 8,047 Rayonier, Inc. REIT 125 3,673 Alleghany Corp. 13 7,848 Healthcare Realty Trust, Inc. REIT 124 3,670 RenaissanceRe Holdings Ltd. 46 7,628 Valley National Bancorp 369 3,598 Omega Healthcare Investors, Inc. REIT 207 7,518 Webster Financial Corp. 82 3,456 STORE Capital Corp. REIT 216 7,340 Bank OZK 110 3,440 Reinsurance Group of Physicians Realty Trust REIT 190 3,382 America, Inc. — Class A 62 7,186 PROG Holdings, Inc. 62 3,340 Eaton Vance Corp. 104 7,065 Hudson Pacific Properties, Inc. REIT 139 3,339 Jones Lang LaSalle, Inc.* 47 6,973 Sabra Health Care REIT, Inc. 189 3,283 Signature Bank 49 6,629 Alliance Data Systems Corp. 44 3,260 Lamar Advertising Co. — Class A REIT 79 6,574 Wintrust Financial Corp. 53 3,238 East West Bancorp, Inc. 129 6,541 CIT Group, Inc. 90 3,231 National Retail Properties, Inc. REIT 159 6,506 JBG SMITH Properties REIT 102 3,190 First Horizon National Corp. 507 6,469 Sterling Bancorp 177 3,183 SEI Investments Co. -

TARP Capital Purchase Program Recipients

TARP Capital Purchase Program Recipients Date Name of Institution City State Investment Type Investment 2/6/2009 Alaska Pacific Bancshares, Inc. Juneau AK Preferred Stock w/Warrants 4,781,000 Alaska Total: 1 12/19/2008 BancTrust Financial Group, Inc. Mobile AL Preferred Stock w/Warrants $50,000,000 11/14/2008 Regions Financial Corp. Birmingham AL Preferred Stock w/Warrants $3,500,000,000 12/5/2008 Superior Bancorp Inc. Birmingham AL Preferred Stock w/Warrants $69,000,000 12/23/2008 United Bancorporation of Alabama, Inc. Atmore AL Preferred Stock w/ Warrants $10,300,000 Alabama Total: 4 12/12/2008 Bank of the Ozarks, Inc. Little Rock AR Preferred Stock w/Warrants $75,000,000 1/16/2009 Home Bancshares, Inc. Conway AR Preferred Stock w/ Warrants 50,000,000 2/ 1/23/2009 Liberty Bancshares, Inc. Jonesboro AR Preferred Stock w/ Exercised Warrants 57,500,000 2/ 1/30/2009 Rogers Bancshares, Inc. Little Rock AR Preferred Stock w/ Exercised Warrants 25,000,000 3/ 1/16/2009 Southern Bancorp, Inc. Arkadelphia AR Preferred Stock 11,000,000 Arkansas Total: 5 2/ 1/30/2009 Goldwater Bank, N.A. Scottsdale AZ Preferred Stock w/ Exercised Warrants 2,568,000 Arizona Total: 1 11/14/2008 Bank of Commerce Holdings Redding CA Preferred Stock w/Warrants $17,000,000 12/5/2008 Bank of Marin Bancorp Novato CA Preferred Stock w/Warrants $28,000,000 2/ 1/30/2009 Beach Business Bank Manhattan Beach CA Preferred Stock w/ Exercised Warrants 6,000,000 12/23/2008 Bridge Capital Holdings San Jose CA Preferred Stock w/ Warrants $23,864,000 11/14/2008 Broadway Financial Corporation -

Bankers' Bank of the West

1099 18th Street Suite 2700 BANKERS’ BANK OF THE WEST Denver, CO 80202 Tel: 303-291-3700 FEDERAL FUND AGENCY AGREEMENT – EXHIBIT A Fax: 303-291-3714 EFFECTIVE February 7, 2020 Based on December 31, 2019 call report data Associated Bank, NA First Horizon Bank People’s United Bank, NA Bank of Hawaii First National Bank of Pennsylvania Regions Bank Bank of the West First Republic Bank Signature Bank Bankers' Bank of the West Fulton Bank, NA Silicon Valley Bank Bank of Oklahoma (BOKF, NA) Hancock Whitney Bank Sterling National Bank BMW Bank of North America Huntington National Bank Texas Capital Bank, NA Capital One Bank (USA), NA JPMorgan Chase Bank, NA Truist Financial Corporation Citibank, NA Manufacturers & Traders Trust Company Trustmark National Bank Citizens Bank, NA MUFG Union Bank, National Association US Bank, NA Commerce Bank New York Community Bank Webster Bank, N.A Federal Reserve Bank of Kansas City [1] Northern Trust Company Zions Bancorporation, NA First Hawaiian Bank Old National Bank [1] Excess funds placed with the Federal Reserve Bank are subject to the terms and conditions established by the Federal Reserve Bank’s Excess Balance Account program. Prior approval of the Federal Reserve Bank is required. Bankers’ Bank of the West (“BBW”) may sell Respondent’s Agency Funds to any one or more of the approved purchasers listed above. Respondent may instruct BBW in writing that Agency Funds shall not be sold to certain approved purchasers. BBW may amend Exhibit A at any time by adding or deleting purchasers upon written or verbal notice as soon as practical to Respondent, and BBW may sell Agency Funds to such additional purchasers unless the Respondent shall have directed BBW prior to the sale not to sell Agency Funds to such additional purchasers. -

Mean Everything

2017 YEAR IN REVIEW MEAN EVERYTHING Front Cover: Hope Butler, Private Banking; Richard Hong, Branch Manager; Lila Colridge, Branch Manager; Veronica Wallace, Training Manager; Paula Fryland, Commercial Banking; Todd Baker, Branch Manager; Andrea Brimhall, Foreign Exchange Operations Specialist; Thomas Morgan, Executive Director Retail and Omni Channel Banking; Chris Penman, Commercial Relationship Manager; Nebiat Haile, Treasury Management Officer “Our Guiding Principles speak to the importance of creating value for our customers, our employees and our shareholders. In truth, value creation is possible only when you have great Employees. We have truly extraordinary bankers who develop strong and enduring relationships with Customers – the kinds of relationships that allow us to become long-term partners in helping our customers strengthen their financial foundations and build outstanding businesses. They’re also the kinds of bankers who are leaders in building their Communities. They understand that what we do as bankers is tantamount to providing the financial ‘oxygen’ that is critical in building strong local economies. Our bankers are also exemplary in giving of their time, talent and leadership, and delivering the Company’s financial resources, in solving pressing needs in their communities.” Harris H. Simmons, Chairman and CEO ZIONS BANCORPORATION 2017 YEAR IN REVIEW 1 OurOUR EMPLOYEES Mean Everything PEOPLE Angela Underwood Jacobs, Marcos Garay, Executive Vice Luz Escamilla, Vice President Senior Vice President, California President, Director of Strategic Community Development, Bank & Trust: Angela has been Business Development, National Zions Bank: Luz is responsible instrumental in the development Bank of Arizona: Marcos is an for establishing, cultivating and success of the Greater accomplished senior executive and maintaining business Southern California North with extensive international relationships across Utah Region through her ability to experience in financial services and Idaho.