DTC Participant Alphabetical Listing June 2019.Xlsx

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ADV Part 2A: Firm Brochure

Firm Brochure Part 2A Natixis Advisors, LLC (“Natixis Advisors”) Natixis Investment Managers Solutions, a division of Natixis Advisors (“Solutions”) Boston Office San Francisco Office 888 Boylston Street 101 Second Street, Suite 1600 Boston, MA 02199 San Francisco, CA 94105 Phone: 617-449-2835 Phone: 617-449-2838 Fax: 617-369-9794 Fax: 617-369-9794 www.im.natixis.com This brochure provides information about the qualifications and business practices of Natixis Advisors. If you have any questions about the contents of this brochure, please contact us at 617-449-2838 or by email at [email protected]. The information in this brochure has not been approved or verified by the United States Securities and Exchange Commission (“SEC”) or by any state securities authority. Additional information about Natixis Advisors is available on the SEC’s website at www.adviserinfo.sec.gov. Registration does not imply that any particular level of skill or training has been met by Natixis Advisors or its personnel. August 4, 2021 1 Important Note about this Brochure This Brochure is not: • an offer or agreement to provide advisory services to any person; • an offer to sell interests (or a solicitation of an offer to purchase interests) in any fund that we advise; or • a complete discussion of the features, risks, or conflicts associated with any advisory service or fund. As required by the Investment Advisers Act of 1940, as amended (the “Advisers Act”), we provide this Brochure to current and prospective clients. We also, in our discretion, will provide this Brochure to current or prospective investors in a fund, together with other relevant offering, governing, or disclosure documents. -

The Layman's Guide to Passive Investing

Technology and Investment, 2021, 12, 129-135 https://www.scirp.org/journal/ti ISSN Online: 2150-4067 ISSN Print: 2150-4059 The Layman’s Guide to Passive Investing Daniel Jonathan Ramos School of Management and Innovation, Colorado State University-Global Campus, Aurora, USA How to cite this paper: Ramos, D. J. Abstract (2021). The Layman’s Guide to Passive Investing. Technology and Investment, 12, Passive investing is a long-term method of investing that utilizes the time 129-135. value of money and compounding interest. Passive investing allows the in- https://doi.org/10.4236/ti.2021.123007 vestor to compete with professional investors without active trading. Once Received: March 5, 2021 the index fund is activated, the investor can walk away without having to Accepted: July 24, 2021 manage it on a day-to-day basis. The risk of an index fund is practically elimi- Published: July 27, 2021 nated by spreading the investment across a basket of instruments that allows the investor to minimize diversifiable risk. According to Kathryn Vasel of Copyright © 2021 by author(s) and CNN Money (Vasel, 2020: CNN.com), only 39% of Americans could raise Scientific Research Publishing Inc. This work is licensed under the Creative $1000 in an emergency. Think about that! Only 4 in 10 working Americans Commons Attribution International could come up with $1000 in an emergency. Could you raise $1000 right now License (CC BY 4.0). if you needed to? The secret to passive investing is “Little and often fills the http://creativecommons.org/licenses/by/4.0/ purse!” Left to one’s own management, a savings account will soon go dry. -

June 1, 2018 PUBLIC

June 1, 2018 COMMODITY FUTURES TRADING COMMISSION RULE 1.55(K): FCM-SPECIFIC DISCLOSURE DOCUMENT The Commodity Futures Trading Commission (Commission) requires each futures commission merchant (FCM), including HSBC Securities (USA) Inc. (“HSI”), to provide the following information to a customer prior to the time the customer first enters into an account agreement or deposits money or securities (funds) with HSI. Except as otherwise noted below, the information set out is as of June 30, 2017. HSI will update this information annually and as necessary to take account of any material change to its business operations, financial condition or other factors that HSI believes may be material to a customer’s decision to do business with HSI. Nonetheless, HSI’s business activities and financial data are not static and will change in non-material ways frequently throughout any 12-month period. HSBC Securities (USA) Inc. is a subsidiary of HSBC North America Holdings. Information that may be material with respect to HSI for purposes of the Commission’s disclosure requirements may not be material to HSBC North America Holdings for purposes of applicable securities laws. Firm Name and Address: HSBC Securities (USA) Inc., 452 5th Avenue New York N.Y. 10018, (212) 525-5000. Principals: Thierry Roland Thierry Roland is Group General Manager and Chief Executive Officer, HSBC Global Banking and Markets for the U.S, Canada and Latin America. Previous to his current role, Roland was Group Treasurer of HSBC Holdings plc from 2010 to April 2015. He has worked for HSBC and Crédit Commercial de France (which HSBC acquired in 2000) since 1988. -

18 February 2019 Solvency and Diversification in Insurance Remain Key Strengths Despite Change in Structure

FINANCIAL INSTITUTIONS ISSUER IN-DEPTH Lloyds Banking Group plc 18 February 2019 Solvency and diversification in insurance remain key strengths despite change in structure Summary RATINGS In 2018, Lloyds Banking Group plc (LBG) altered its structure to comply with the UK's ring- Lloyds Banking Group plc Baseline Credit a3 fencing legislation, which requires large banks to separate their retail and SME operations, Assessment (BCA) and deposit taking in the European Economic Area (EEA) from their other activities, including Senior unsecured A3 Stable the riskier capital markets and trading business. As part of the change, LBG designated Lloyds Bank plc as the“ring-fenced” entity housing its retail, SME and corporate banking operations. Lloyds Bank plc It also assumed direct ownership of insurer Scottish Widows Limited, previously a subsidiary Baseline Credit A3 Assessment (BCA) of Lloyds Bank. The changes had little impact on the creditworthiness of LBG and Lloyds Adjusted BCA A3 Bank, leading us to affirm the deposit and senior unsecured ratings of both entities. Scottish Deposits Aa3 Stable/Prime-1 Widows' ratings were unaffected. Senior unsecured Aa3 Stable » LBG's reorganisation was less complex than that of most UK peers. The Lloyds Lloyds Bank Corporate Markets plc Banking Group is predominantly focused on retail and corporate banking, and the Baseline Credit baa3 required structural changes were therefore relatively minor. The group created a small Assessment (BCA) separate legal entity, Lloyds Bank Corporate Markets plc (LBCM), to manage its limited Adjusted BCA baa1 Deposits A1 Stable/Prime-1 capital markets and trading operations, and it transferred its offshore subsidiary, Lloyds Issuer rating A1 Stable Bank International Limited (LBIL), to LBCM from Lloyds Bank. -

LPL Financial LLC Form 13F-HR Filed 2021-08-13

SECURITIES AND EXCHANGE COMMISSION FORM 13F-HR Initial quarterly Form 13F holdings report filed by institutional managers Filing Date: 2021-08-13 | Period of Report: 2021-06-30 SEC Accession No. 0001403438-21-000004 (HTML Version on secdatabase.com) FILER LPL Financial LLC Mailing Address Business Address 1055 LPL WAY 4707 EXECUTIVE DRIVE CIK:1403438| IRS No.: 952834236 | State of Incorp.:CA | Fiscal Year End: 1231 FORT MILL SC 29715 SAN DIEGO CA 92121 Type: 13F-HR | Act: 34 | File No.: 028-12526 | Film No.: 211170492 704-733-3300 Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE OMB Number: 3235-0006 COMMISSION Expires: July 31, 2015 Washington, D.C. 20549 Estimated average burden hours per response: 23.8 FORM 13F FORM 13F COVER PAGE Report for the Calendar Year or Quarter Ended: 06-30-2021 Check here if Amendment: ☐ Amendment Number: This Amendment (Check only one.): ☐ is a restatement. ☐ adds new holdings entries. Institutional Investment Manager Filing this Report: Name: LPL Financial LLC Address: 1055 LPL WAY FORT MILL, SC 29715 Form 13F File Number: 028-12526 The institutional investment manager filing this report and the person by whom it is signed hereby represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete, and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: Dean Phillips Title: Vice President Phone: 980-264-8377 Signature, Place, and Date of Signing: Dean Phillips Fort Mill, SOUTH CAROLINA 08-12-2021 [Signature] [City, State] [Date] Report Type (Check only one.): ☒ 13F HOLDINGS REPORT. -

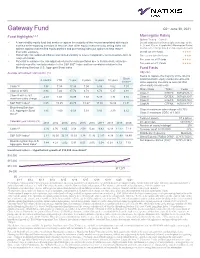

Gateway Fund

Gateway Fund Q2 • June 30, 2021 Fund Highlights1,2,3 Morningstar Rating Options Trading – Class Y • A low-volatility equity fund that seeks to capture the majority of the returns associated with equity Overall rating derived from weighted average of the markets while exposing investors to less risk than other equity investments by selling index call 3-, 5- and 10-year (if applicable) Morningstar Rating options against a diversified equity portfolio and purchasing index put options to help reduce metrics; other ratings based on risk-adjusted returns downside exposure Overall out of 81 funds ★★★★ • Historically has outpaced inflation and limited volatility to a level comparable to intermediate-term to Three years out of 81 funds ★★★ long term bonds Five years out of 57 funds • Potential to enhance the risk-adjusted returns for many portfolios due to its historically attractive ★★★★ risk/return profile, low beta relative to the S&P 500® Index and low correlation relative to the Ten years out of 11 funds ★★★★ Bloomberg Barclays U.S. Aggregate Bond Index Fund Facts Average annualized total returns† (%) Objective Seeks to capture the majority of the returns Since 3 months YTD 1 year 3 years 5 years 10 years associated with equity market investments, 1/1/88** while exposing investors to less risk than Class Y5 3.98 7.34 17.98 7.04 6.98 5.62 7.01 other equity investments Share Class Ticker Cusip Class A at NAV 3.94 7.24 17.72 6.78 6.72 5.37 6.91 Class Y GTEYX 367829-88-4 Class A with 5.75% -2.04 1.08 10.95 4.69 5.47 4.74 6.72 Class A GATEX 367829-20-7 maximum sales charge Class C GTECX 367829-70-2 ® 8 S&P 500 Index 8.55 15.25 40.79 18.67 17.65 14.84 11.31 Class N GTENX 367829-77-7 Bloomberg Barclays U.S. -

Golden Capital Large Cap Core Select UMA Wells Fargo Funds Management

Golden Capital Large Cap Core Product Placed on Watch Select UMA Wells Fargo Funds Management, LLC Style: US Large Cap Year Founded: 1971 Sub-Style: Blend GIMA Status: Approved 525 Market Street, 12th Floor Firm AUM: $512.5 billion Firm Ownership: Wells Fargo & Co. San Francisco, California 94105 Firm Strategy AUM: $368.6 million Professional-Staff: 1468 PRODUCT OVERVIEW TARGET PORTFOLIO CHARACTERISTICS PORTFOLIO STATISTICS Wells Fargo Asset Management's large cap core equity investment Number of stock holdings: 45 to 50 ---------------06/21------ 12/20 strategy's primary objective is long-term capital appreciation. Wells ---------- P/E ratio: Below the S&P 500 Wells Index*** Wells Fargo's goal is to produce excess returns above the S&P 500 Index. Fargo Fargo Golden's large cap core investment philosophy is to construct an actively Cash level over market cycle: 0 to 3% Number of stock holdings 52 505 52 managed, core portfolio of companies that exhibit the likelihood to meet Risk (standard deviation): Similar to/Below the S&P 500 or exceed earnings expectations. Golden uses proprietary, multifactor Dividend Yield 1.3% 1.4% 1.4% models that combine valuation, earnings and momentum factors to Average turnover rate: 30 to 60% identify the characteristics within each company that make it Distribution Rate — — — Use ADRs: No unsustainably cheap. Risk is managed through diversification by 19.79x 25.40x 23.00x avoiding concentration in any one security or industry while generally Capitalization: Mega, Large and Medium Wtd avg P/E ratio ¹ adhering to sector weights of +/- 5% to those of the S&P 500 Index. -

10 Year Capital Market Assumptions for 2021

10-Year Capital Market Assumptions Calendar Year 2021 2 10-Year Capital Market Assumptions Overview On an annual basis, BNY Mellon Investor Solutions, LLC develops capital market return assumptions for approximately 50 asset classes around the world. The assumptions are based on a 10-year investment time horizon and are intended to guide investors in developing their long-term strategic asset allocations. Historically, the initial baseline assumptions were derived using consensus views, adjusted to reflect insights regarding global market imbalances based on research from across BNY Mellon. This year we have incorporated the macroeconomic forecasts generated by BNY Mellon Investment Management Global Economic and Investment Analysis Group, led by Chief Economist Shamik Dhar. Given the global pandemic and unprecedented amount of global monetary and fiscal stimulus deployed to support the economic recovery, we believe the incorporation of these probability-weighted forecasts will prove particularly useful given the high degree of coronavirus-related economic uncertainty. Overall, the results of our 2021 10-year capital market assumptions are mixed depending on the asset class when compared to last year’s assumptions (see Exhibit 1). We see stronger equity market returns due to higher growth rates as the economy recovers from the pandemic. Fixed income asset class returns will be extremely limited given how low global bond yields are today. Alternative asset class returns are mixed, with generally lower returns in absolute return or hedged strategies and amplified returns in private markets. Exhibit 1: Snapshot of Risk and Return for the 2021 Capital Market Assumptions 9% U.S. Private Equity US Private Equity EM Equity Equity 2021 Equity 2020 EM Equity 8% Fixed Income 2021 Fixed Income 2020 Alternatives 2021 Alternatives 2020 Int'lIntl Developed Equity Equity USU.S. -

Hsbc to Acquire Lloyds Banking Group Onshore Assets in the Uae

Ab c 29 March 2012 HSBC TO ACQUIRE LLOYDS BANKING GROUP ONSHORE ASSETS IN THE UAE HSBC Bank Middle East Ltd (‘HSBC’), an indirect wholly-owned subsidiary of HSBC Holdings plc, has entered into an agreement to acquire the onshore retail and commercial banking business of Lloyds Banking Group (‘Lloyds’) in the United Arab Emirates (‘UAE’). The value of the gross assets being acquired is US$769m as at 31 December 2011. The transaction, which is subject to regulatory approvals, is expected to complete in 2012. HSBC’s largest operations in the MENA region are based in the UAE where HSBC enjoys a market-leading trade and commercial banking presence, in addition to the largest international retail banking and wealth management business. The business being acquired from Lloyds has approximately 8,800 personal and commercial customers and a loan book of approximately US$573m as at 31 December 2011. Commenting on the acquisition, Simon Cooper, Deputy Chairman and Chief Executive Officer of HSBC in MENA, said: “HSBC is the leading international bank in the UAE and the addition of Lloyds’ strong presence in retail and commercial banking is highly complementary to our business. The acquisition underscores the strategic importance of the UAE, and of the MENA region as a whole, to HSBC.” Media enquiries to: Tim Harrison + 971 4 4235632 [email protected] Brendan McNamara +44 (0) 20 7991 0655 [email protected] ends/more Registered Office and Group Head Office: This news release is issued by 8 Canada Square, London E14 5HQ, United Kingdom Web: www.hsbc.com HSBC Holdings plc Incorporated in England with limited liability. -

J.P. Morgan's Expression of Interest to Act As Global Co-Ordinator And

CONFIDENTIAL J.P. Morgan’s expression of interest to act as Global Co-ordinator and Bookrunner in connection with the Íslandsbanki IPO J.P. Morgan is pleased to express its interest to act as Global Co-ordinator and Bookrunner in connection with the sale process of the Icelandic State Financial Investments’ holdings in Íslandsbanki. J.P. Morgan is a leading global investment bank with a market capitalisation of $427bn and total assets of $3.4trn (December 2020). J.P. Morgan’s global headquarters are in New York, while our European headquarters are in London. We have a strong presence and track record in the Nordic region and our commitment to the region is evidenced by our local offices across the region. J.P. Morgan offers ISFI a full range of investment banking services and will provide first class advice in connection with the sale process of its holdings in Íslandsbanki. We are a global leader in areas such as equity and equity linked capital markets, debt capital markets, M&A advisory, ratings advisory and equity and debt sales, research and trading. J.P. Morgan team for Íslandsbanki Senior project leadership and sponsorship Andreas Lindh, Co-Head of EMEA FIG Stefan Weiner, Head of Northern Europe ECM Kari Hallgrimsson, Senior Country Sponsorship Nordic FIG Advisory European ECM Christian Kornhoff, Executive Director Vittorio Rivaroli, Executive Director Filiph Nilsson, Analyst Emese Pavlik, Associate Kim-Jonas Pellikka, Analyst Vincent Collan, Analyst FIG DCM Ratings Advisory Kiran D. Karia, Executive Director Jens Rasmussen, Executive Director J.P. Morgan contact details Andreas Lindh Registered address: Full legal name: Taunustor 1 J.P. -

Svenska Handelsbanken AB

OFFERING CIRCULAR Svenska Handelsbanken AB (publ) (Incorporated as a public limited liability banking company in The Kingdom of Sweden) U.S.$50,000,000,000 Euro Medium Term Note Programme for the issue of Notes with a minimum maturity of one month On 26th June, 1992 Svenska Handelsbanken AB (publ) (the “Issuer” or the “Bank”) entered into a U.S.$1,500,000,000 Euro Medium Term Note Programme (the “Programme”) and issued an offering circular on that date describing the Programme. This Offering Circular supersedes any previous offering circular and supplements therein prepared in connection with the Programme. Any Notes (as defined below) issued under the Programme on or after the date of this Offering Circular are issued subject to the provisions described herein. This does not affect any Notes already in issue. Under the Programme, the Bank may from time to time issue Notes (the “Notes”), which expression shall include Notes (i) issued on a senior preferred basis as described in Condition 3 (“Senior Preferred Notes”), (ii) issued on a senior non-preferred basis as described in Condition 4 (“Senior Non-Preferred Notes”), (iii) issued on a subordinated basis and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 5 (“Subordinated Notes”) and (iv) issued on a subordinated basis with no fixed maturity and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 6 (“Additional Tier 1 Notes”). The Outstanding Principal Amount (as defined in Condition 2) of each Series (as defined below) of Additional Tier 1 Notes will be subject to Write Down (as defined in Condition 2) if the Common Equity Tier 1 Capital Ratio (as defined in Condition 2) of the Bank and/or the Handelsbanken Group (as defined Condition 2) is less than the relevant Trigger Level (as defined in Condition 2). -

Brokerage Transfer

Brokerage Transfer ✓ Use this form to: Mail to: Express delivery only: • Transfer assets to T. Rowe Price Brokerage from another T. Rowe Price T. Rowe Price Mail Code 17150 institution. P.O. Box 17150 4515 Painters Mill Road ✗ Do not use this form to: Baltimore, MD 21297-1150 Owings Mills, MD 21117-4903 • Exchange between T. Rowe Price funds. This stamp indicates a signature guarantee is required. • Change ownership. Use the Change Ownership form. This paper clip indicates you may need to attach documentation. Trust, Estate, Corporation, or Other Entity Name (if applicable) TIN 1 T. Rowe Price Account A separate form is required for each account type or delivering institution. Delivering Firm Name Phone Check One Account Type: ¨ Individual ¨ Traditional or Rollover IRA ¨ Profit Sharing Plan (PSP) ¨ Joint ¨ Roth or Roth Rollover IRA ¨ Money Purchase Delivering Firm Address ¨ Trust ¨ Inherited IRA Pension Plan (MPP) ¨ Estate ¨ Roth Inherited IRA ¨ Individual 401(k) ¨ UGMA/UTMA ¨ SIMPLE IRA ¨ SEP-IRA City State ZIP Code ¨ Corporate or Other Entity For a new account, visit troweprice.com/newaccount to get an account ¨ For more owners, check this box and attach a separate page. number or write “new” and enclose one of these forms: • Brokerage New Account • Brokerage IRA New Account 3 Transfer Instructions • Brokerage Employer-Sponsored Retirement Plan New Account T. Rowe Price Brokerage Account Number Phone NOTE: Your current firm may charge a fee for transferring assets. Check one: ¨ Full transfer. Transfer all identically registered assets in kind. Owner Name (as it appears on statement) Social Security Number (SSN) Assets are moved as is and not sold.