The Future of the Drone Economy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rns Over the Long Term and Critical to Enabling This Is Continued Investment in Our Technology and People, a Capital Allocation Priority

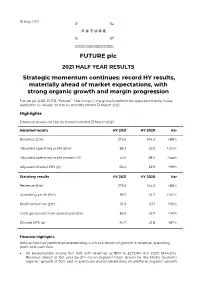

19 May 2021 FUTURE plc 2021 HALF YEAR RESULTS Strategic momentum continues: record HY results, materially ahead of market expectations, with strong organic growth and margin progression Future plc (LSE: FUTR, “Future”, “the Group”), the global platform for specialist media, today publishes its results for the six months ended 31 March 2021. Highlights Financial results for the six months ended 31 March 2021 Adjusted results HY 2021 HY 2020 Var Revenue (£m) 272.6 144.3 +89% Adjusted operating profit (£m)1 89.2 39.9 +124% Adjusted operating profit margin (%) 33% 28% +5ppt Adjusted diluted EPS (p) 65.4 32.9 +99% Statutory results HY 2021 HY 2020 Var Revenue (£m) 272.6 144.3 +89% Operating profit (£m) 59.7 24.7 +142% Profit before tax (£m) 56.9 27.1 +110% Cash generated from operations (£m) 85.9 35.7 +141% Diluted EPS (p) 40.7 21.8 +87% Financial highlights Robust first-half performance extending our track record of growth in revenue, operating profit and cash flow: An exceptionally strong first half, with revenue up 89% to £272.6m (HY 2020: £144.3m). Revenue ahead of last year by 21% on an organic2 basis, driven by the Media division’s organic2 growth of 30% and in particular digital advertising on-platform organic2 growth of 30% and eCommerce affiliates’ organic2 growth of 56%. US achieved revenue growth of 31% on an organic2 basis and UK revenues grew by 5% organically (UK has a higher mix of events and magazines revenues which were impacted more materially by the pandemic). -

Assessing Feasibility of the Delivery Drone

Assessing Feasibility of the Delivery Drone By: Blane Butcher and Kok Weng Lim Topic Areas: Strategy, Transportation, Last Mile Advisor: Dr. Justin Boutilier Summary: Blane is from Cleveland, Weng is from Kuala Lumpur, Ohio. He graduated from Malaysia. He holds a Master’s Cornell University with a in Engineering Management Bachelor of Science in from University Putra Mechanical Engineering in Malaysia. His background is 2012. He is a helicopter pilot in risk management, internal in the United States Navy auditing, and quality with experience in aviation management with Sime Darby maintenance and quality (Malaysian Conglomerate) in assurance. China and Southeast Asia. Background KEY INSIGHTS Getting into the delivery drone industry requires careful alignment of business and strategy for a company. Examining the important aspects of the 1. Constraints are a critical component to drone industry to align them with the company understand and consider when exploring strategy is the first step. delivery drones in a transportation network. Drone flight range, payload, and Amazon, Boeing, UPS, FedEX, and DHL are just a cost of operation are currently the most few of the companies that have been experimenting difficult constraints to address. with delivery drones. Most of the momentum in drones seems to be in the medical industry. There 2. Applications in the medical industry are also a number of emerging delivery drone constitute most of the current delivery companies such as Matternet and Flirtey. drone applications. Major transportation companies like UPS, Amazon, and DHL Given the activity in the drone industry, it is important have all shown active participation in to understand their technological capabilities and delivery drone research. -

Design Perspectives on Delivery Drones

C O R P O R A T I O N Design Perspectives on Delivery Drones Jia Xu For more information on this publication, visit www.rand.org/t/RR1718z2 Published by the RAND Corporation, Santa Monica, Calif. © Copyright 2017 RAND Corporation R® is a registered trademark. Limited Print and Electronic Distribution Rights This document and trademark(s) contained herein are protected by law. This representation of RAND intellectual property is provided for noncommercial use only. Unauthorized posting of this publication online is prohibited. Permission is given to duplicate this document for personal use only, as long as it is unaltered and complete. Permission is required from RAND to reproduce, or reuse in another form, any of its research documents for commercial use. For information on reprint and linking permissions, please visit www.rand.org/pubs/permissions. The RAND Corporation is a research organization that develops solutions to public policy challenges to help make communities throughout the world safer and more secure, healthier and more prosperous. RAND is nonprofit, nonpartisan, and committed to the public interest. RAND’s publications do not necessarily reflect the opinions of its research clients and sponsors. Support RAND Make a tax-deductible charitable contribution at www.rand.org/giving/contribute www.rand.org Preface Delivery drones may become widespread over the next five to ten years, particularly for what is known as the “last-mile” logistics of small, light items. Companies such as Amazon, Google, the United Parcel Service (UPS), DHL, and Alibaba have been running high-profile experiments testing drone delivery systems, and the development of such systems reached a milestone when the first commercial drone delivery approved by the Federal Aviation Administration took place on July 17, 2015. -

Comitato Salviamo Genova E La Liguria ABSTRACT Stima Della

Comitato Salviamo Genova e la Liguria ABSTRACT Stima della perdita di marginalità subita dalle imprese liguri a seguito dei lavori sulla rete autostradale regionale Disclaimer: In questo rapporto sono contenuti i dati che i rappresentanti delle categorie economiche hanno predisposto per la stima della perdita di fatturato e dei maggiori costi sostenuti a seguito della caduta dei livelli di servizio sulle autostrade liguri. Il Dipartimento di Economia dell’Università di Genova e la Camera di Commercio di Genova si sono occupati solo delle elaborazioni successive. Obiettivo del lavoro Il presente lavoro ha come obiettivo la stima dei danni subiti dalle imprese liguri a seguito dei lavori che hanno interessato la rete autostradale – in particolare nei mesi da giugno ad agosto 2020 – che si sono tradotti in una perdita di marginalità, quindi maggiori costi di produzione che non sono stati ribaltati sui prezzi di vendita, e perdita di fatturato conseguente al maggior tempo di produzione o alla riduzione della domanda (in particolare per le attività di servizi). Metodologia del lavoro Il lavoro si propone di giungere ad una stima del danno complessivo come sommatoria delle stime relative alle singole categorie economiche o settori di attività. Tale metodo di lavoro si rende necessario per tenere conto delle specificità dei singoli settori, oltre che della necessità di dover ricorrere a proxy differenti per le singole stime. Va inoltre sottolineato che i danni oggetto di stima sono intervenuti in un periodo del tutto particolare, caratterizzato dall’emergenza sanitaria legata al virus Covid-19, pertanto si è dovuto preliminarmente depurare i dati dagli effetti legati all’emergenza sanitaria; infine va tenuto presente che le stime si basano su dati che in alcuni casi sono ancora provvisori (es. -

A Virtual Train Journey Along the Mare Ligure from Ventimiglia to Rome

Italian Culture Newsletter Number 22 A Virtual Train Journey along the Mare Ligure from Ventimiglia to Rome. Marie and I have made this journey on a number of occasions. In doing so we have either made the journey in a single day albeit with a change of train, usually at Genova. On other occasions, we have spent an evening or even a few days at Genova and/or at Livorno or Pisa. The journey described will involve more stops on the way but could be more interesting on that account. The trip begins in Ventimiglia where we stayed overnight on our last day of our last holiday in Italy. This had been occasioned by the French railway strike which prevented any trains from running from Ventimiglia to Nice on the day of our arrival from Rome into the city at the Italian- French border in Liguria. Our first visit to Ventimiglia was in 2006 when some Italian friends from Cuneo, due north of Ventimiglia, in Piemonte, met us at the rail station in Ventimiglia to take us for a short stay at their apartment in Nice. On that occasion we didn’t see much of the city except for part of the old medieval town, which now mostly is the home of many of the southerners from Naples, Calabria and Sicily who moved north seeking employment after WWII. The old town is perched high above the new city with its long sea-front promenade and railway station. Ventimiglia is the ancient Albium Intemelium, the capital of the Intemelii, a Ligurian tribe which long resisted the Romans, until in 115 BC it was forced to submit to Marcus Aemilius Scaurus. -

PONTE MORANDI, Genova Un Anno Fa Crollava Il Viadotto Sul Polcevera

1 PONTE MORANDI, Genova un anno fa crollava il viadotto sul Polcevera di Alice Spagnolo – 14 Agosto 2019 – 6:30 Genova. L’orologio segna le 11.36. E’ il 14 agosto 2018 e sta piovendo. La città è viva come non lo sarà mai più. Un boato e poi la polvere che copre Genova, la Superba. Il viadotto sul Polcevera del Ponte Morandi si spezza e si sgretola, trascinando nel baratro 43 vite. Con il ponte si spacca in due una città, una regione, la Liguria, l’Italia intera. E’ passato un anno, ma le immagini del crollo del viadotto restano negli occhi dei genovesi, dei liguri e non solo. Il ponte ora non esiste più, completamente demolito alle 9,37 del 28 giugno scorso con una ‘bomba’ di 680 chili di esplosivo, tra dinamite e plastico. Un simbolo di Genova cancellato dalla vista, ma che resta impresso nella mente e nell’animo come una ferita che non si rimargina. Come quel furgoncino verde della Basko rimasto a un metro dal precipizio, e il cui conducente si è salvato per un miracolo, così i liguri sono rimasti, aggrappati alla vita guardando negli occhi la morte. A un anno dalla strage autostradale di Genova, restano le famiglie e gli amici di quelle 43 vite spezzate. Restano i 566 sfollati. Restano la rabbia e il dolore, ma anche la voglia di rinascere e ricominciare. C’è chi ha perso un figlio, un padre, un fratello. Chi ha perso la casa e chi ha perso il lavoro. C’è chi convive, ancora oggi, con i disagi, con le polveri sollevate dall’enorme cantiere che ha dapprima messo in sicurezza e poi demolito ciò che restava del ponte Morandi e ora si prepara a ricostruire un viadotto che unisca di nuovo la Riviera24 - 1 / 2 - 27.09.2021 2 Liguria, da Ponente a Levante. -

Strategic Network Design for Parcel Delivery with Drones Under Competition

Strategic Network Design for Parcel Delivery with Drones under Competition Gohram Baloch, Fatma Gzara Department of Management Sciences, University of Waterloo, ON Canada N2L 3G1 [email protected] [email protected] This paper studies the economic desirability of UAV parcel delivery and its effect on e-retailer distribution network while taking into account technological limitations, government regulations, and customer behavior. We consider an e-retailer offering multiple same day delivery services including a fast UAV service and develop a distribution network design formulation under service based competition where the services offered by the e-retailer not only compete with the stores (convenience, grocery, etc.), but also with each other. Competition is incorporated using the Multinomial Logit market share model. To solve the resulting nonlinear mathematical formulation, we develop a novel logic-based Benders decomposition approach. We build a case based on NYC, carry out extensive numerical testing, and perform sensitivity analyses over delivery charge, delivery time, government regulations, technological limitations, customer behavior, and market size. The results show that government regulations, technological limitations, and service charge decisions play a vital role in the future of UAV delivery. Key words : UAV; drone; market share models; facility location; logic-based benders decomposition 1. Introduction Unmanned aerial vehicles (UAVs) or drones have been used in military applications as early as 1916 (Cook 2007). As the technology improved, their applications extended to surveillance and moni- toring (Maza et al. 2010, Krishnamoorthy et al. 2012), weather research (Darack 2012), delivery of medical supplies (Wang 2016, Thiels et al. 2015), and emergency response (Adams and Friedland 2011). -

IVT Annual Report 2019 with Review 2012–2018

Research Collection Report IVT Annual Report 2019 With Review 2012–2018 Author(s): Institute for Transport Planning and Systems, ETH Zurich Publication Date: 2020-04 Permanent Link: https://doi.org/10.3929/ethz-b-000410787 Rights / License: In Copyright - Non-Commercial Use Permitted This page was generated automatically upon download from the ETH Zurich Research Collection. For more information please consult the Terms of use. ETH Library Institute for Transport Planning and Systems Annual Report 2019 review 2012–2018 01-rubrik-pagina-rechts | 01-rubrik-pagina-rechtsThe IVT in the +year medium 2019 Ioannis Agalliadis, MSc Felix Becker, MSc 2015 Aristotle University of Thessaloniki (BSc); 2014 Freie Universität Berlin (BSc); 2018 RWTH Aachen University (MSc) 2016 (MSc) Dr. sc. Henrik Becker Lukas Ambühl, MSc 2012 ETH Zürich (BSc); 2014 (MSc); 2013 ETH Zürich (BSc); 2015 (MSc) 2018 (Dr. sc.) Illahi Anugrah, MSc 2011 Gadjah Mada University (BSc); Harald Bollinger 2013 (MSc) Labor Prof. Dr.-Ing. Kay W. Axhausen 1984 University of Wisconsin, Madison (MSc); 1988 Universität Karlsruhe (Dr.-Ing.); Axel Bomhauer-Beins, MSc Since 1999 full Professor for Transport planning 2014 ETH Zürich (BSc); 2016 (MSc) Dr. sc. Milos Balac 2010 University of Belgrade (BSc); 2012 EPFL (MSc); Beda Büchel, MSc 2019 ETH Zürich (Dr. Sc.) 2014 ETH Zürich (BSc); 2016 (MSc) IVT Annual Report 2019 The IVT in the year 2019 Dr. Jérémy Decerle Jenny Burri 2013 University of Technology of Belfort- Secretary Montbéliard (MSc); 2018 (PhD) Prof. Dr. Francesco Corman 2006 Università Roma Tre (MSc); Dr. sc. 2010 Delft University of Technology (Dr) ; Ilka Dubernet since 2017 assistant professor 2008 Freie Universität Berlin (Diplom); for Transport Systems 2019 ETH Zürich (Dr. -

Trends in U.S. Oil and Natural Gas Upstream Costs

Trends in U.S. Oil and Natural Gas Upstream Costs March 2016 Independent Statistics & Analysis U.S. Department of Energy www.eia.gov Washington, DC 20585 This report was prepared by the U.S. Energy Information Administration (EIA), the statistical and analytical agency within the U.S. Department of Energy. By law, EIA’s data, analyses, and forecasts are independent of approval by any other officer or employee of the United States Government. The views in this report therefore should not be construed as representing those of the Department of Energy or other federal agencies. U.S. Energy Information Administration | Trends in U.S. Oil and Natural Gas Upstream Costs i March 2016 Contents Summary .................................................................................................................................................. 1 Onshore costs .......................................................................................................................................... 2 Offshore costs .......................................................................................................................................... 5 Approach .................................................................................................................................................. 6 Appendix ‐ IHS Oil and Gas Upstream Cost Study (Commission by EIA) ................................................. 7 I. Introduction……………..………………….……………………….…………………..……………………….. IHS‐3 II. Summary of Results and Conclusions – Onshore Basins/Plays…..………………..…….… -

Demolizione Ponte Morandi, Salvini: “Operazione Unica Al Mondo”. Toti: “Giornata Storica” Di Redazione 28 Giugno 2019 – 11:53

1 Demolizione Ponte Morandi, Salvini: “Operazione unica al mondo”. Toti: “Giornata storica” di Redazione 28 Giugno 2019 – 11:53 Genova. “Sono totalmente fiducioso sulla ricostruzione del ponte di Genova”. Lo ha detto il vicepremier Matteo Salvini dopo la demolizione delle pile. “Oggi è la giornata in cui ringraziare ingegneri, tecnici operai e forze dell’ordine, oggi si è compiuta un’operazione unica al mondo”. “È una giornata bellissima per la nostra città, la nostra regione, per tutta l’Italia. Siamo di fronte a un intervento di alta ingegneria, un’eccellenza del nostro paese. La demolizione è il risultato di capacità tecniche straordinarie e di una straordinaria unione di intenti dal punto di vista politico e amministrativo. Tutti hanno remato nella stessa direzione, dal 14 agosto Governo, Regione, Comune e istituzioni periferiche dello Stato hanno lavorato con abnegazione e serietà, ma anche con generosità, per rispettare le promesse fatte ai cittadini”. Il presidente di Regione Liguria Giovanni Toti ha seguito la demolizione delle pile 10 e 11, con l’assessore alla Protezione civile Giacomo Giampedrone, il sindaco di Genova Marco Bucci, il ministro dell’Interno Matteo Salvini e quello allo Sviluppo economico Luigi di Maio. “Credo che quello di oggi – aggiunge Toti – sia un evento che riavvicina la politica al Paese perché si è dimostrato che, quando si vuole, le cose si possono fare. Tutti i tempi sono stati rispettati, anche anticipando di qualche giorno, quando possibile, ad esempio con la consegna delle case agli sfollati. Avevamo promesso viabilità alternativa, risarcimenti alle Il Vostro Giornale - 1 / 3 - 26.09.2021 2 imprese, investimenti per rendere competitivo il nostro porto: siamo riusciti, grazie alla collaborazione e all’impegno di tutti, a dare strade, compensare chi era stato danneggiato e portare investimenti infrastrutturali importanti che sono già in corso d’appalto”. -

14 AGOSTO '18 - CROLLO DEL PONTE MORANDI LA RISPOSTA DEL GALLIERA Galliera News 4 2018 Ok.Qxp Layout 1 03/10/18 14:19 Pagina 2

Galliera_news_4_2018_ok.qxp_Layout 1 03/10/18 14:19 Pagina 1 N. 4 ANNO IX 2018 – TRIMESTRALE DI INFORMAZIONE SANITARIA E AZIENDALE 14 AGOSTO '18 - CROLLO DEL PONTE MORANDI LA RISPOSTA DEL GALLIERA Galliera_news_4_2018_ok.qxp_Layout 1 03/10/18 14:19 Pagina 2 SOMMARIO EDITORIALE 3 14 AGOSTO 2018 - ORE 11.36, CROLLO DEL PONTE MORANDI IN OSPEDALE 4 CROLLO DEL PONTE MORANDI LA RISPOSTA DEL GALLIERA 6 LETTERA DEL DOTT. MARVIN MENINI 7 ICTUS? FAI P.R.E.S.T.O.! 8 IL GALLIERA E LE SFIDE DELLA MEDICINA SULL’INVECCHIAMENTO SALUTE E BENESSERE 10 ALLATTAMENTO MATERNO NELLE EMERGENZE E.O. Ospedali Galliera 11 INFEZIONI E PREVENZIONE SPAZIO ASSOCIAZIONI 12 ASSOCIAZIONE LIGURE THALASSEMICI n. 4 anno 9 – settembre 2018 10 NEWS Galliera News - Pubblicazione trimestrale di informazione sanitaria e aziendale L'ANGOLO DELLA MEDITAZIONE dell’E.O. Ospedali Galliera di Genova 14 OMELIA DEL CARDINALE ANGELO BAGNASCO DURANTE I FUNERALI DI STATO Proprietario ed Editore: DELLE VITTIME DEL CROLLO DI PONTE MORANDI E.O. Ospedali Galliera Mura delle Cappuccine, 14 - 16128 - Genova 15 RASSEGNA STAMPA Tel. 010 56321 - www.galliera.it Direttore responsabile: Adriano Lagostena Comitato di redazione: Adriano Lagostena, Roberto Viale, Giuliano Lo Pinto, Gian Andrea Rollandi, Marco Esposto, LEGENDA INTERATTIVA Simone Canepa, Roberta Perdelli Bottino Scopri l’interattività del giornale digitale Ideazione, pianificazione e gestione dei contenuti digitali; su http://magazine.galliera.it/gallieranews2018n4/ coordinamento editoriale e redazione: Clicca in corrispondenza delle icone per consultare Roberta Perdelli Bottino i contenuti extra relativi agli articoli. Consulenza tecnica per la versione digitale: S.C. Informatica e Telecomunicazioni Direttore Carlo Berutti Bergotto PILLOLE DI SALUTE LO SPECIALISTA RISPONDE Fotografie e riprese video: Servizio Fotografico – Ufficio del Coordinatore Scientifico Impaginazione, archivio iconografico, stampa e realizzazione digitale: VIDEO Giuseppe Lang - Arti Grafiche S.r.l. -

SESAR European Drones Outlook Study / 1

European Drones Outlook Study Unlocking the value for Europe November 2016 SESAR European Drones Outlook Study / 1 / Contents Note to the Reader ............................................................................................. 2 Executive Summary ............................................................................................ 3 1 | Snapshot of the Evolving 'Drone' Landscape .................................................. 8 1.1 'Drone' Industry Races Forward – Types of Use Expanding Rapidly ............................. 8 1.2 Today's Evolution depends on Technology, ATM, Regulation and Societal Acceptance .......................................................................................................................... 9 1.3 Scaling Operations & Further Investment Critical to Fortify Europe's Position in a Global Marketplace ........................................................................................................... 11 2 | How the Market Will Unfold – A View to 2050 ............................................ 14 2.1 Setting the Stage – Framework to Assess Benefits in Numerous Sectors .................. 14 2.2 Meeting the Hype – Growth Expected Across Leisure, Military, Government and Commercial ....................................................................................................................... 15 2.3 Closer View of Civil Missions Highlights Use in All Classes of Airspace ...................... 20 2.4 Significant Societal Benefits for Europe Justify Further Action .................................