Fiscal 2014 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Starbucks Corp. (SBUX) Annual General Meeting

Corrected Transcript 18-Mar-2020 Starbucks Corp. (SBUX) Annual General Meeting Total Pages: 14 1-877-FACTSET www.callstreet.com Copyright © 2001-2020 FactSet CallStreet, LLC Starbucks Corp. (SBUX) Corrected Transcript Annual General Meeting 18-Mar-2020 CORPORATE PARTICIPANTS Kevin Johnson John Culver President, Chief Executive Officer & Director, Starbucks Corp. Group President-International, Channel Development and Global Coffee & Tea, Starbucks Corp. Rachel A. Gonzalez Executive Vice President, General Counsel & Secretary, Starbucks Corp. Rosalind Gates Brewer Chief Operating Officer, Group President & Director, Starbucks Corp. Justin Danhof General Counsel & Director-Free Enterprise Project, The National Patrick J. Grismer Center for Public Policy Research Executive Vice President & Chief Financial Officer, Starbucks Corp. Rossann Williams Executive Vice President & President-U.S. company-operated business and Canada, Starbucks Corp. ..................................................................................................................................................................................................................................................................... MANAGEMENT DISCUSSION SECTION Kevin Johnson President, Chief Executive Officer & Director, Starbucks Corp. Well, good morning from Seattle, Washington, and welcome to Starbucks' 28th Annual Meeting of Shareholders. I'm so pleased to have you join this webcast and I want to open by thanking the Starbucks Board of Directors, all of whom are joining -

National Retailer & Restaurant Expansion Guide Spring 2016

National Retailer & Restaurant Expansion Guide Spring 2016 Retailer Expansion Guide Spring 2016 National Retailer & Restaurant Expansion Guide Spring 2016 >> CLICK BELOW TO JUMP TO SECTION DISCOUNTER/ APPAREL BEAUTY SUPPLIES DOLLAR STORE OFFICE SUPPLIES SPORTING GOODS SUPERMARKET/ ACTIVE BEVERAGES DRUGSTORE PET/FARM GROCERY/ SPORTSWEAR HYPERMARKET CHILDREN’S BOOKS ENTERTAINMENT RESTAURANT BAKERY/BAGELS/ FINANCIAL FAMILY CARDS/GIFTS BREAKFAST/CAFE/ SERVICES DONUTS MEN’S CELLULAR HEALTH/ COFFEE/TEA FITNESS/NUTRITION SHOES CONSIGNMENT/ HOME RELATED FAST FOOD PAWN/THRIFT SPECIALTY CONSUMER FURNITURE/ FOOD/BEVERAGE ELECTRONICS FURNISHINGS SPECIALTY CONVENIENCE STORE/ FAMILY WOMEN’S GAS STATIONS HARDWARE CRAFTS/HOBBIES/ AUTOMOTIVE JEWELRY WITH LIQUOR TOYS BEAUTY SALONS/ DEPARTMENT MISCELLANEOUS SPAS STORE RETAIL 2 Retailer Expansion Guide Spring 2016 APPAREL: ACTIVE SPORTSWEAR 2016 2017 CURRENT PROJECTED PROJECTED MINMUM MAXIMUM RETAILER STORES STORES IN STORES IN SQUARE SQUARE SUMMARY OF EXPANSION 12 MONTHS 12 MONTHS FEET FEET Athleta 46 23 46 4,000 5,000 Nationally Bikini Village 51 2 4 1,400 1,600 Nationally Billabong 29 5 10 2,500 3,500 West Body & beach 10 1 2 1,300 1,800 Nationally Champs Sports 536 1 2 2,500 5,400 Nationally Change of Scandinavia 15 1 2 1,200 1,800 Nationally City Gear 130 15 15 4,000 5,000 Midwest, South D-TOX.com 7 2 4 1,200 1,700 Nationally Empire 8 2 4 8,000 10,000 Nationally Everything But Water 72 2 4 1,000 5,000 Nationally Free People 86 1 2 2,500 3,000 Nationally Fresh Produce Sportswear 37 5 10 2,000 3,000 CA -

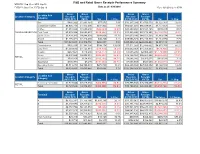

F&B and Retail Gross Receipts Performance Summary

F&B and Retail Gross Receipts Performance Summary MTD PFY: Sep 15 vs. MTD: Sep 16 FYTD PY: Sep 15 vs. FYTD: Sep 16 Data as of: 9/30/2016 Run: 12/1/2016 2:14:15 PM 12:00:00 AM Gross Gross Gross Gross Location Sub Location Category Receipts Receipts Receipts Receipts Category (MTD PFY) (MTD) Var % Chg (FYTD PFY) (FYTD) Var % Chg Bar $985,292 $1,063,164 $77,872 7.9% $10,237,209 $13,559,570 $3,322,361 32.5% Casual Dining/Bar $6,930,743 $7,472,696 $541,952 7.8% $83,051,037 $86,828,087 $3,777,051 4.5% Coffee $1,663,026 $1,620,456 ($42,569) (2.6%) $20,593,466 $21,123,745 $530,279 2.6% FOOD & BEVERAGE Fast Food $3,272,934 $2,653,679 ($619,254) (18.9%) $39,936,206 $37,772,391 ($2,163,816) (5.4%) Quick-Serve $3,439,385 $4,048,054 $608,669 17.7% $42,670,286 $44,553,560 $1,883,274 4.4% Snack $1,276,421 $1,316,689 $40,268 3.2% $15,056,923 $16,218,893 $1,161,970 7.7% Total $17,567,801 $18,174,738 $606,937 3.5% $211,545,128 $220,056,247 $8,511,119 4.0% Convenience $592,130 $1,341,304 $749,174 126.5% $7,511,263 $12,486,622 $4,975,359 66.2% Duty Free $1,203,685 $1,125,314 ($78,370) (6.5%) $15,632,363 $14,753,053 ($879,309) (5.6%) Kiosks $287,657 $118,240 ($169,417) (58.9%) $4,086,286 $2,906,298 ($1,179,988) (28.9%) News $2,597,882 $2,005,573 ($592,309) (22.8%) $32,124,769 $26,461,368 ($5,663,400) (17.6%) RETAIL News/Coffee $793,250 $678,050 ($115,199) (14.5%) $8,686,166 $9,305,677 $619,511 7.1% Spa/Salon $138,982 $7,429 ($131,553) (94.7%) $2,005,669 $541,657 ($1,464,012) (73.0%) Specialty Retail $3,711,278 $4,390,033 $678,755 18.3% $42,200,052 $47,368,052 -

Board of Directors

STARBUCKS CORPORATION BOARD OF DIRECTORS HOWARD SCHULTZ, 59, is the founder of Starbucks Corporation and serves as our chairman, president and chief executive officer. Mr. Schultz has served as chairman of the board of directors since our inception in 1985, and in January 2008, he reassumed the role of president and chief executive officer. From June 2000 to February 2005, Mr. Schultz also held the title of chief global strategist. From November 1985 to June 2000, he served as chairman of the board and chief executive officer. From November 1985 to June 1994, Mr. Schultz also served as president. From January 1986 to July 1987, Mr. Schultz was the chairman of the board, chief executive officer and president of Il Giornale Coffee Company, a predecessor to the Company. From September 1982 to December 1985, Mr. Schultz was the director of retail operations and marketing for Starbucks Coffee Company, a predecessor to the Company. WILLIAM W. BRADLEY, 69, has been a Starbucks director since June 2003. Since 2000, Senator Bradley has been a managing director of Allen & Company LLC, an investment banking firm. From 2001 until 2004, he acted as chief outside advisor to McKinsey & Company’s non-profit practice. In 2000, Sen. Bradley was a candidate for the Democratic nomination for President of the United States. He served as a senior advisor and vice chairman of the International Council of JP Morgan & Co. from 1997 through 1999. During that time, Sen. Bradley also worked as an essayist for CBS Evening News, and as a visiting professor at Stanford University, the University of Notre Dame and the University of Maryland. -

Tampa, Florida (The “Property”)

CHIPOTLE / STARBUCKS T A M P A, FLORIDA EXCLUSIVE OFFERING DISCLAIMER This Offering Memorandum has been prepared by Owner Representative Additional information and an opportunity to inspect the property will be made (“OREP”) for use by a limited number of parties to evaluate the potential available to interested and qualified prospective investors upon written request. acquisition of Chipotle / Starbucks, Tampa, Florida (the “Property”). All Owner and OREP each expressly reserve the right, at their sole discretion, to projections have been developed by OREP, Owner and designated sources, reject any or all expressions of interest or offers regarding the property and/or are based upon assumptions relating to the general economy, competition, and terminate discussions with any entity at any time with or without notice. Owner other factors beyond the control of OREP and Owner, and therefore are subject shall have no legal commitment or obligations to any entity reviewing this to variation. No representation is made by OREP or Owner as to the accuracy Offering Memorandum or making an offer to purchase the property unless and or completeness of the information contained herein, and nothing contained until such offer is approved by Owner, a written agreement for the purchase herein is or shall be relied on as a promise or representation as to the future of the property has been fully executed, delivered and approved by Owner performance of the Property. Although the information contained herein has and its legal counsel, and any obligations set by Owner thereunder have been been obtained from sources deemed to be reliable and believed to be correct, satisfied or waived. -

Seattle's Seafaring Siren: a Cultural Approach to the Branding Of

Running Head: SEATTLE’S SEAFARING SIREN 1 Seattle’s Seafaring Siren: A Cultural Approach to the Branding of Starbucks Briana L. Kauffman Master of Arts in Media Communications March 24, 2013 SEATTLE’S SEAFARING SIREN 2 Thesis Committee Starbucks Starbucks Angela Widgeon, Ph.D, Chair Date Starbucks Starbucks Stuart Schwartz, Ph.D, Date Starbucks Starbucks Todd Smith, M.F.A, Date SEATTLE’S SEAFARING SIREN 3 Copyright © 2013 Briana L. Kauffman All Rights Reserved SEATTLE’S SEAFARING SIREN 4 Abstract Many corporate brands tend to be built on a strong foundation of culture, but very minimal research seems to indicate a thorough analysis of the role of an organizational’s culture in its entirety pertaining to large corporations. This study analyzed various facets of Starbucks Coffee Company through use of the cultural approach to organizations theory in order to determine if the founding principles of Starbucks are evident in their organizational culture. Howard Schultz’ book “Onward” was analyzed and documented as the key textual artifact in which these principles originated. Along with these principles, Starbucks’ Website, Facebook, Twitter and YouTube page were analyzed to determine how Starbucks’ culture was portrayed on these sites. The rhetorical analysis of Schultz’ book “Onward” conveyed that Starbucks’ culture is broken up into a professional portion and a personal portion, each overlapping one another in its principles. After sifting through various tweets, posts and videos, this study found that Starbucks has created a perfect balance of culture, which is fundamentally driven by their values and initiatives in coffee, ethics, relationships and storytelling. This study ultimately found that Starbucks’ organizational culture is not only carrying out their initiatives that they principally set out to perform, but they are also doing so across all platforms while engaging others to do the same. -

Demand Mounts for Directors with Digital Smarts

www.AgendaWeek.com 1 of 2 Demand Mounts for Directors With Digital Smarts By Amanda Gerut ore companies are seeking As these recent examples show, boards are Supplies Are Limited Express envisioned Leonsis as a special boardroom. And the recruits can help a experienced new directors, that’s all to directors with digital and social raiding the executive ranks of America’s assistant to CEO Kenneth Chenault to board mirror more closely the background the good, Leonsis says. “Being open to M media expertise, and the urgent top technology brands to recruit new When search rm Spencer Stuart help the company usher in a host of of its company’s customers. various types of board members, demand is prompting boards to consider directors with backgrounds in social surveyed corporate secretaries for its digital strategies. But he was soon encouraging diering ideas and some people who at rst glance would media. Why? “Social media is a 2011 Board Index, it found that appointed as a director and asked to chair At some companies, the search for social accepting those who challenge appear to be unlikely candidates. conversation and interacts with consumers demand for directors with digital the board’s new innovation and media savvy is even making the boards conventional thinking is what pumps and stakeholders,” writes eodore expertise — experience in social media, technology committee. more diverse. For instance, last March, life into a board of directors and e Starbucks board in December made Leonsis, who serves on the boards of technology and e-commerce — had AutoNation’s board appointed another ultimately the company,” he writes. -

Starbucks Corporation (Exact Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 Form 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended September 27, 2020 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to . Commission File Number: 0-20322 Starbucks Corporation (Exact Name of Registrant as Specified in its Charter) Washington 91-1325671 (State of Incorporation) (IRS Employer ID) 2401 Utah Avenue South, Seattle, Washington 98134 (206) 447-1575 (Address of principal executive office, zip code, telephone number) Securities Registered Pursuant to Section 12(b) of the Act: Title of Each Class Trading Symbol Name of Each Exchange on Which Registered Common Stock, $0.001 par value per share SBUX Nasdaq Global Select Market Securities Registered Pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Retail Attraction Survey Results.Pdf

Retail Attraction Survey SurveyMonkey Q1 From what store and city was your last purchase from a retailer that exceeded $200? Answered: 232 Skipped: 11 # RESPONSES DATE 1 Best buy 9/10/2018 10:29 PM 2 Walmart - Jefferson City 8/14/2018 10:28 AM 3 Lowe’s in JC 8/10/2018 12:24 PM 4 Lowes. Jefferson City 8/10/2018 11:13 AM 5 Target - Jefferson City 8/10/2018 10:39 AM 6 multiple items: Walmart JC Stadium 8/10/2018 10:29 AM 7 Dicks 8/10/2018 7:34 AM 8 IKEA St. Louis 8/10/2018 12:48 AM 9 McKnight Tire, Jefferson City Wal-Mart, Jefferson City Sam's, Jefferson City 8/9/2018 11:05 PM 10 Wal-Mart 8/9/2018 4:10 PM 11 IKEA in st Louis 8/9/2018 3:45 PM 12 Best Buy, Jefferson City 8/9/2018 1:20 PM 13 Jefferson City, Lowe’s 8/9/2018 12:48 PM 14 Kohls, Columbia, MO 8/9/2018 11:48 AM 15 Walmart-school supplies and clothes 8/9/2018 10:19 AM 16 Lowe’s, Jefferson City 8/9/2018 10:14 AM 17 Jefferson City, Walmart 8/9/2018 8:59 AM 18 Nordstrom's, St Louis 8/9/2018 8:10 AM 19 Zales. Osage Beach 8/9/2018 6:37 AM 20 Children’s place, build a bear 8/9/2018 6:36 AM 21 Kirklands Branson 8/9/2018 6:31 AM 22 Sams 8/9/2018 5:38 AM 23 JC Mattress in Jefferson City 8/8/2018 11:46 PM 24 Walmart 8/8/2018 9:39 PM 25 Walmart, jefferson city 8/8/2018 8:22 PM 26 Scruggs, Jefferson City, MO 8/8/2018 7:33 PM 27 Lowes 8/8/2018 5:41 PM 28 Kohls, Jefferson City 8/8/2018 4:38 PM 29 Columbia, Soma 8/8/2018 3:51 PM 30 Will West Music & Sound, Lowe's 8/8/2018 11:35 AM 31 Walmart in Jefferson City 8/8/2018 10:28 AM 32 Staples jeff city 8/8/2018 6:08 AM 33 Probably car maintenance and service at Honda dealer in JC 8/7/2018 5:07 PM 34 Chico's Columbia, Missosuri 8/7/2018 3:00 PM 1 / 43 Retail Attraction Survey SurveyMonkey 35 Best Buy Columbia, MO 8/7/2018 2:49 PM 36 Walmart 8/7/2018 2:28 PM 37 Sunglass Hut 8/7/2018 1:00 PM 38 Homegoods 8/7/2018 12:49 PM 39 Walmart 8/7/2018 12:46 PM 40 Columbia Appliance Columbia MO. -

Starbucks Company Profile

Starbucks Company Profile September 2013 The Starbucks Story Our story began in 1971. Back then we were a roaster and retailer of whole bean and ground coffee, tea and spices with a single store in Seattle’s Pike Place Market. Today, we are privileged to connect with millions of customers every day with exceptional products and more than 19,000 retail stores in over 60 countries. Folklore Starbucks is named after the first mate in Herman Melville’s Moby Dick. Our logo is also inspired by the sea – featuring a twin‐tailed siren from Greek mythology. Starbucks Mission Our mission: to inspire and nurture the human spirit – one person, one cup and one neighborhood at a time. Our Coffee We’ve always believed in serving the best coffee possible. It's our goal for all of our coffee to be grown under the highest standards of quality, using ethical sourcing practices. Our coffee buyers personally travel to coffee farms in Latin America, Africa and Asia to select the highest quality beans. And our master roasters bring out the balance and rich flavor of the beans through the signature Starbucks Roast. Our Stores Our stores are a neighborhood gathering place for meeting friends and family. Our customers enjoy quality service, an inviting atmosphere and an exceptional beverage. Total stores: 19,209* (as of June 30, 2013) Argentina, Aruba, Australia, Austria, Bahamas, Bahrain, Belgium, Brazil, Bulgaria, Canada, Chile, China, Costa Rica, Curacao, Cyprus, Czech Republic, Denmark, Egypt, El Salvador, England, Finland, France, Germany, Greece, Guatemala, Hong Kong/Macau, Hungary, India, Indonesia, Ireland, Japan, Jordan, Kuwait, Lebanon, Malaysia, Mexico, Morocco, New Zealand, Netherlands, Northern Ireland, Oman, Peru, Philippines, Poland, Portugal, Qatar, Romania, Russia, Saudi Arabia, Scotland, Singapore, South Korea, Spain, Sweden, Switzerland, Taiwan, Thailand, Turkey, United Arab Emirates, United States, Vietnam and Wales. -

Brand Benchmark Analysis

COFFEE SHOP BRAND BENCHMARK BRANDS ANALYSIS LexisNexis® Media Intelligence Research and Analytics Methodology • This study examines traditional media attention of Starbucks and four competing major international coffee chains published from July 1 - August 31, 2017: • Coverage from major Canadian, U.S., U.K., and French media was examined for this study. This coverage was sourced from the LexisNexis Newsdesk® media monitoring and analytics solution, and included coverage with a Newsdesk Source Rank of 1. • This study includes quantitative and qualitative metrics and analysis, as well as results derived from LexisNexis Newsdesk® and human analysis of the coverage by LexisNexis analysts. The study’s overall volume and audience reach results and derivative metrics (share of voice) were determined through LexisNexis Newsdesk®, while the sentiment and messaging results were determined through human analysis by the LexisNexis team. • For the human analysis, LexisNexis analyzed a random sampling of 800 clips across all coffee chains included in the study. For each clip examined, LexisNexis determined how favorably the chain was depicted using a modified five-point scale: 1. Intensely Positive; 2. Positive; 3. Neutral; 4. Mixed / Balanced; 5. Negative; and 6. Intensely Negative. Also, LexisNexis tracked what the focus of the story was from the perspective of the coffee chain from among three options: 1. Corporate News; 2. Restaurant / Product News; and 3. Other News. Lastly, LexisNexis tracked a list of key positive and negative messages about corporate and restaurant/product matters for each chain. The names and logos of Dunkin’ Donuts, Tim Hortons, and Starbucks, Costa Coffee, and Caffe Nero are the trade names and logos of their respective owners. -

Fiscal 2018 Annual Report

Fiscal 2018 Annual Report UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 Form 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended September 30, 2018 or TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to . Commission File Number: 0-20322 Starbucks Corporation (Exact Name of Registrant as Specified in its Charter) Washington 91-1325671 (State of Incorporation) (IRS Employer ID) 2401 Utah Avenue South, Seattle, Washington 98134 (206) 447-1575 (Address of principal executive offices, zip code, telephone number) Securities Registered Pursuant to Section 12(b) of the Act: Title of Each Class Name of Each Exchangegg on Which Registered Common Stock, $0.001 par value per share Nasdaq Global Select Market Securities Registered Pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.