U.S. END MARKET ANALYSIS for KENYAN TEA December 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

National Retailer & Restaurant Expansion Guide Spring 2016

National Retailer & Restaurant Expansion Guide Spring 2016 Retailer Expansion Guide Spring 2016 National Retailer & Restaurant Expansion Guide Spring 2016 >> CLICK BELOW TO JUMP TO SECTION DISCOUNTER/ APPAREL BEAUTY SUPPLIES DOLLAR STORE OFFICE SUPPLIES SPORTING GOODS SUPERMARKET/ ACTIVE BEVERAGES DRUGSTORE PET/FARM GROCERY/ SPORTSWEAR HYPERMARKET CHILDREN’S BOOKS ENTERTAINMENT RESTAURANT BAKERY/BAGELS/ FINANCIAL FAMILY CARDS/GIFTS BREAKFAST/CAFE/ SERVICES DONUTS MEN’S CELLULAR HEALTH/ COFFEE/TEA FITNESS/NUTRITION SHOES CONSIGNMENT/ HOME RELATED FAST FOOD PAWN/THRIFT SPECIALTY CONSUMER FURNITURE/ FOOD/BEVERAGE ELECTRONICS FURNISHINGS SPECIALTY CONVENIENCE STORE/ FAMILY WOMEN’S GAS STATIONS HARDWARE CRAFTS/HOBBIES/ AUTOMOTIVE JEWELRY WITH LIQUOR TOYS BEAUTY SALONS/ DEPARTMENT MISCELLANEOUS SPAS STORE RETAIL 2 Retailer Expansion Guide Spring 2016 APPAREL: ACTIVE SPORTSWEAR 2016 2017 CURRENT PROJECTED PROJECTED MINMUM MAXIMUM RETAILER STORES STORES IN STORES IN SQUARE SQUARE SUMMARY OF EXPANSION 12 MONTHS 12 MONTHS FEET FEET Athleta 46 23 46 4,000 5,000 Nationally Bikini Village 51 2 4 1,400 1,600 Nationally Billabong 29 5 10 2,500 3,500 West Body & beach 10 1 2 1,300 1,800 Nationally Champs Sports 536 1 2 2,500 5,400 Nationally Change of Scandinavia 15 1 2 1,200 1,800 Nationally City Gear 130 15 15 4,000 5,000 Midwest, South D-TOX.com 7 2 4 1,200 1,700 Nationally Empire 8 2 4 8,000 10,000 Nationally Everything But Water 72 2 4 1,000 5,000 Nationally Free People 86 1 2 2,500 3,000 Nationally Fresh Produce Sportswear 37 5 10 2,000 3,000 CA -

Tea Industry

Tea Industry Introduction The Indian tea industry is nearly 200 years old. Robert Bruce, a British national discovered tea plants growing in the upper Brahmaputra valley in Assam and adjoining areas. In 1838, Indian tea that was grown in Assam was sent to the UK for the first time, for public sale. Tea in India is grown primarily in Assam, West Bengal, Tamil Nadu and Kerala. Apart from this, it is also grown in small quantities in Karnataka, HP, Tripura, Uttaranchal, Arunachal Pradesh, Manipur, Sikkim and Meghalaya. India has a dual tea base, unlike most other tea exporting countries. Both CTC and Orthodox tea is produced in India. The tea industry is agro‐based and labour intensive. It provides direct employment to over 1 million persons. Through its forward and backward linkages another 10 million persons derive their livelihood from tea. In Northeast India alone, the tea industry employs around 900,000 persons on permanent rolls. It is one of the largest employers of women amonst organized industries in India. Women constitute nearly 51% of the total workforce. The tea estates in the North Eastern India are located in industrially backward areas. Tea being the only organised industry in the private sector in this region, people outside the tea estates have high expectations from the industry. The three most distinct known varieties of tea in India are: a) Assam tea (grown in Assam and other parts of NE India) b) Darjeeling tea (grown in Darjeeling and other parts of West Bengal) c) Nilgiri tea (grown in the Nilgiri hills of Tamil Nadu) Objective Through this dissertation project, I intend to study, with respect to the CIS nations and the United Kingdom that serve as the foremost export markets, the Indian tea industry in detail, the trends observed in the past, the highs and lows of export volumes to these countries and the reasons behind them, as well as future prospects on where Indian would stand in the global arena. -

Tea Time with the Cozy Chicks Pdf Free Download

TEA TIME WITH THE COZY CHICKS PDF, EPUB, EBOOK Ellery Adams | 230 pages | 05 Oct 2015 | Createspace Independent Publishing Platform | 9781517385781 | English | none Tea Time With The Cozy Chicks PDF Book Grab your calendar. About Publish Join Sign In. Collins Paperbacks Books. So when I think of a cozy girl, I see a woman who's personal sense of style is all about staying comfortable. Tuesday, December 1, Join us on Facebook! Pork rib roast with cranberry-apricot stuffing Prep Time. And once we had the idea, we were off and running, thanks, in part, to many a full cup of Irish Breakfast Tea. Madewell madewell. See all 5 - All listings for this product. Riwi the Kiwi: Goes Looking for his Tea. The first, The Cozy Chicks Kitchen , allowed readers to enter the heart of our cozy mystery worlds, with stories about our characters and about us — all told through food. If you don't have a sifter, use a mesh strainer and tap it. Sprinkle the 2 tablespoons of sugar on the top. Type keyword s to search. Catalogue Number: To register, visit Pine Needles online here. Thank goodness times have changed and tea is now offered many places and in many forms! Unmasked by Andy Ngo , Hardcover No ratings or reviews yet. For a better shopping experience, please upgrade now. About this product. Tea is such simple pleasure, you think as you pull the bag from the steaming mug, with limitless and unique meanings to each and every person who enjoys it. Search Search Search Browse menu. Sometimes friendships that served us well in the past no longer provide the nurturance and support we need right now. -

Wikipedia, the Free Encyclopedia 03-11-09 12:04

Tea - Wikipedia, the free encyclopedia 03-11-09 12:04 Tea From Wikipedia, the free encyclopedia Tea is the agricultural product of the leaves, leaf buds, and internodes of the Camellia sinensis plant, prepared and cured by various methods. "Tea" also refers to the aromatic beverage prepared from the cured leaves by combination with hot or boiling water,[1] and is the common name for the Camellia sinensis plant itself. After water, tea is the most widely-consumed beverage in the world.[2] It has a cooling, slightly bitter, astringent flavour which many enjoy.[3] The four types of tea most commonly found on the market are black tea, oolong tea, green tea and white tea,[4] all of which can be made from the same bushes, processed differently, and in the case of fine white tea grown differently. Pu-erh tea, a post-fermented tea, is also often classified as amongst the most popular types of tea.[5] Green Tea leaves in a Chinese The term "herbal tea" usually refers to an infusion or tisane of gaiwan. leaves, flowers, fruit, herbs or other plant material that contains no Camellia sinensis.[6] The term "red tea" either refers to an infusion made from the South African rooibos plant, also containing no Camellia sinensis, or, in Chinese, Korean, Japanese and other East Asian languages, refers to black tea. Contents 1 Traditional Chinese Tea Cultivation and Technologies 2 Processing and classification A tea bush. 3 Blending and additives 4 Content 5 Origin and history 5.1 Origin myths 5.2 China 5.3 Japan 5.4 Korea 5.5 Taiwan 5.6 Thailand 5.7 Vietnam 5.8 Tea spreads to the world 5.9 United Kingdom Plantation workers picking tea in 5.10 United States of America Tanzania. -

Trustea Brochure

INDIA SUSTAINABLE TEA PROGRAM trustea THE INDIA SUSTAINABLE TEA PROGRAMA. WHAT IS trustea THE INDIA SUSTAINABLE TEA PROGRAM? is an ambitious initiative to develop and implement a The India Sustainable Tea Program is a locally-developed and sustainability Code for the Indian domestic tea market. owned Indian sustainability tea Code. This meaningful, cost- effective and practical Code does not compromise globally This initiative to transform the Indian tea industry is based on accepted core sustainability standards. industry realities and globally accepted sustainability principles. It is envisioned that compliance with the Code will not only improve competitiveness for tea farms but also make it The program, led by the Tea Board of India is currently jointly possible for them to comply with national regulations and in funded by The Sustainable Trade Initiative (IDH), Hindustan future international sustainability standards. The applicable Unilever Limited (HUL) and Tata Global Beverages Limited control points under 11 chapters need to be adhered to (TGBL). within a four-year period, resulting in complete compliance. The verification under the Code provides consumers with the Solidaridad and Ethical Tea Partnership (ETP) are the assurance of responsible production and provides producers implementing partners. the opportunity to credibly demonstrate this to their customers. Rainforest Alliance (RA) is the technical advisor. B WHY DO WE NEED trustea? It is hoped that other organizations will soon join the program. Increasing number of consumers around the world are insisting that the products they buy are made from Tea Board of India strongly believes that the effective sustainable raw material. The effective delivery of the India implementation of the trustea program will significantly Sustainable Tea program will: improve the social and economic conditions of the tea industry whilst protecting the environment. -

Of Counsel: Alden L

IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLUMBIA FEDERAL TRADE COMMISSION, ) ) Plaintiff, ) ) v. ) Civ. No. 1:07-cv-01021-PLF ) WHOLE FOODS MARKET, INC., ) REDACTED - PUBLIC VERSION ) And ) ) WILD OATS MARKETS, INC., ) ) Defendants. ) ~~~~~~~~~~~~) JOINT MEMORANDUM OF POINTS AND AUTHORITIES OF WHOLE FOODS MARKET, INC., AND WILD OATS MARKETS, INC. IN OPPOSITION TO MOTION FOR A PRELIMINARY INJUNCTION Paul T. Denis (DC Bar No. 437040) Paul H. Friedman (DC Bar No. 290635) Jeffrey W. Brennan (DC Bar No. 447438) James A. Fishkin (DC Bar No. 478958) Michael Farber (DC Bar No. 449215) Rebecca Dick (DC Bar No. 463197) DECHERTLLP 1775 I Street, N.W. Washington, DC 20006 Telephone: (202) 261-3430 Facsimile: (202) 261-3333 Of Counsel: Alden L. Atkins (DC Bar No. 393922) Neil W. Imus (DC Bar No. 394544) Roberta Lang John D. Taurman (DC Bar No. 133942) Vice-President of Legal Affairs and General Counsel VINSON & ELKINS L.L.P. Whole Foods Market, Inc. The Willard Office Building 550 Bowie Street 1455 Pennsylvania Avenue, N.W., Suite 600 Austin, TX Washington, DC 20004-1008 Telephone (202) 639-6500 Facsimile (202) 639-6604 Attorneys for Whole Foods Market, Inc. Clifford H. Aronson (DC Bar No. 335182) Thomas Pak (Pro Hae Vice) Matthew P. Hendrickson (Pro Hae Vice) SKADDEN, ARPS, SLATE, MEAGHER &FLOMLLP Four Times Square NewYork,NY 10036 Telephone: (212) 735-3000 [email protected] Gary A. MacDonald (DC Bar No. 418378) SKADDEN, ARPS, SLATE, MEAGHER &FlomLLP 1440 New York Avenue, N.W. Washington, DC 20005 Telephone: (202) 371-7000 [email protected] Terrence J. Walleck (Pro Hae Vice) 2224 Pacific Dr. -

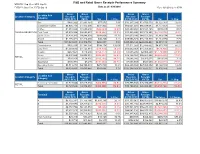

F&B and Retail Gross Receipts Performance Summary

F&B and Retail Gross Receipts Performance Summary MTD PFY: Sep 15 vs. MTD: Sep 16 FYTD PY: Sep 15 vs. FYTD: Sep 16 Data as of: 9/30/2016 Run: 12/1/2016 2:14:15 PM 12:00:00 AM Gross Gross Gross Gross Location Sub Location Category Receipts Receipts Receipts Receipts Category (MTD PFY) (MTD) Var % Chg (FYTD PFY) (FYTD) Var % Chg Bar $985,292 $1,063,164 $77,872 7.9% $10,237,209 $13,559,570 $3,322,361 32.5% Casual Dining/Bar $6,930,743 $7,472,696 $541,952 7.8% $83,051,037 $86,828,087 $3,777,051 4.5% Coffee $1,663,026 $1,620,456 ($42,569) (2.6%) $20,593,466 $21,123,745 $530,279 2.6% FOOD & BEVERAGE Fast Food $3,272,934 $2,653,679 ($619,254) (18.9%) $39,936,206 $37,772,391 ($2,163,816) (5.4%) Quick-Serve $3,439,385 $4,048,054 $608,669 17.7% $42,670,286 $44,553,560 $1,883,274 4.4% Snack $1,276,421 $1,316,689 $40,268 3.2% $15,056,923 $16,218,893 $1,161,970 7.7% Total $17,567,801 $18,174,738 $606,937 3.5% $211,545,128 $220,056,247 $8,511,119 4.0% Convenience $592,130 $1,341,304 $749,174 126.5% $7,511,263 $12,486,622 $4,975,359 66.2% Duty Free $1,203,685 $1,125,314 ($78,370) (6.5%) $15,632,363 $14,753,053 ($879,309) (5.6%) Kiosks $287,657 $118,240 ($169,417) (58.9%) $4,086,286 $2,906,298 ($1,179,988) (28.9%) News $2,597,882 $2,005,573 ($592,309) (22.8%) $32,124,769 $26,461,368 ($5,663,400) (17.6%) RETAIL News/Coffee $793,250 $678,050 ($115,199) (14.5%) $8,686,166 $9,305,677 $619,511 7.1% Spa/Salon $138,982 $7,429 ($131,553) (94.7%) $2,005,669 $541,657 ($1,464,012) (73.0%) Specialty Retail $3,711,278 $4,390,033 $678,755 18.3% $42,200,052 $47,368,052 -

Economics of Change in Market Structure, Conduct, and Performance the Baking Industry 1947-1958

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Papers from the University Studies series (The University of Nebraska) University Studies of the University of Nebraska 12-1963 Economics of Change in Market Structure, Conduct, and Performance The Baking Industry 1947-1958 Richard G. Walsh University of Nebraska - Lincoln Bert M. Evans University of Nebraska- Lincoln Follow this and additional works at: https://digitalcommons.unl.edu/univstudiespapers Part of the Arts and Humanities Commons Walsh, Richard G. and Evans, Bert M., "Economics of Change in Market Structure, Conduct, and Performance The Baking Industry 1947-1958" (1963). Papers from the University Studies series (The University of Nebraska). 48. https://digitalcommons.unl.edu/univstudiespapers/48 This Article is brought to you for free and open access by the University Studies of the University of Nebraska at DigitalCommons@University of Nebraska - Lincoln. It has been accepted for inclusion in Papers from the University Studies series (The University of Nebraska) by an authorized administrator of DigitalCommons@University of Nebraska - Lincoln. new series no. 28 University of Nebraska Studies december 1963 Richard G. Walsh Bert M. Evans Economics of Change in Market Structure, Conduct, and Performance The Baking Industry 1947-1958 university of nebraska studies : new series no. 28 published by the university at lincoln: december 1963 The University of Nebraska The £lard of Regents RICHARD E. ADKINS B. N. GREENBERG, M.D., president J. G. ELLIOTI JOSEPH SOSHNIK, corporation secretary VAL PETERSON CLARENCE E. SWANSON J. LEROY WELSH The Chancellor CLIFFORD M. HARDIN Richard G. Walsh Bert M. Evans Economics of Change in Market Structure, Conduct, and Performance The Baking Industry 1947-1958 university of nebraska studies : new series no. -

F All & Winter 2

Fall & winter 2009 MILOTM LOOSE TEA INFUSER DEAR VALUED CUSTOMER, Welcome to Fall/Holiday 2009! With consumer uncertainty settling, on shelf. I have also created the festive and functional Milo tea infuser, we are anticipating a strong and healthy second half of the year. Tea a truly innovative design. Say goodbye to the tea ball and chain!! Forté is uniquely poised— offering elegant and purposeful gift options at accessible price points. We truly are an affordable luxury that And finally, back by popular demand, the 2009 pre-assorted Holiday continues to sell well beyond expectations. Collection! We are appreciative of your enthusiastic feedback regarding the ease of last year’s program and its successful sell through. milo loose tea infuser NEW This season’s design has focused on enhanced merchandising. We And this year’s Collection is even better! Inspired by the simple beauty MEASURES : 6 X 2.75 X 2” have replaced many of our gift boxes with distinguished bands that of natural birch bark, we have developed a line of products that are An easy to use loose tea infuser that is showcase the unique, clean lines of our products. We have redesigned elegant in their simplicity and offer very accessible price points. In the perfect for brewing a cup, mug or small teapot. Just add loose tea to the stainless the interior of our best selling gift sets so that shoppers can easily spirit of the season, we are offering you a financial incentive to purchase steel base, twist on the colorful ceramic see the contents. These changes make dramatic, eye-=catching by the Assortment. -

Q Products: a CUP of TEA ANYONE? Aussiesencha Tea Australia’S Only Locally-Grown & Certified Organic Greem Sencha Tea Blends

q products: A CUP OF TEA ANYONE? AussieSencha Tea Australia’s only locally-grown & certified organic greem sencha tea blends Asian cultures have been drinking green tea for more than 2000 years and it is now well known that green tea improves cardiovascular health, reduces the risk of cancer and is a natural aid in weight loss regimes. Green tea, as with oolong and black tea comes from the same plant species, camellia sinensis, but green tea is steamed and fired straight after harvesting to stop the fermentation process, the oxidation of the leaf which gives oolong and black tea their distinct colour and flavour. This treatment of green tea therefore allows for better retention of more nutrients and a higher yield of antioxidants than fermented teas. Since the development of green tea production in Victoria in 1994, there are five growers of which one is certified organic. Harvested in Victoria’s high country and processed in Australia’s only green tea processing plant in Wangaratta, Yarra Valley Tea Co. is the largest buyer of locally grown organic green tea in Australia. It is used exclusively for their unique green tea blends, Uncle Vic & Aunt Myrtle. UNCLE VIC: Packed full of antioxidants and restorative properties, Uncle vic pays homage to the traditional Japanese sencha tea with its vibrant green hue, cleaning aromatic taste and sweet tongue glosses. Benefits: Weight Loss - The polyphenols found in green teas work to increase our metabolism by burning more kilojoules throughout the day and increasing the body’s ability to burn fat. Boosts Energy - The rich blend of vitamins, minerals, caffeine, and antioxidants found in this green tea variety, along with an ample amount of caffeine, make it very effective as an energy-booster. -

Japanese Green Tea

Market Alternatives for Japanese Green Tea A report for the Rural Industries Research and Development Corporation by Angela Monks November 2000 RIRDC Publication No 00/169 RIRDC Project No DAT-38A © 2000 Rural Industries Research and Development Corporation. All rights reserved. ISBN 0 642 58200 9 ISSN 1440-6845 Market Alternatives for Japanese Green Tea Publication No. 00/169 Project No.DAT-38A. The views expressed and the conclusions reached in this publication are those of the author and not necessarily those of persons consulted. RIRDC shall not be responsible in any way whatsoever to any person who relies in whole or in part on the contents of this report. This publication is copyright. However, RIRDC encourages wide dissemination of its research, providing the Corporation is clearly acknowledged. For any other enquiries concerning reproduction, contact the Publications Manager on phone 02 6272 3186. Researcher Contact Details Ms Angela Monks Department of Primary Industry Water and Environment St. Johns Avenue New Town Tasmania 7050 Phone: 03 6233 6813 Fax: 03 6228 5936 Email: [email protected] RIRDC Contact Details: Rural Industries Research and Development Corporation Level 1, AMA House 42 Macquarie Street BARTON ACT 2600 PO Box 4776 KINGSTON ACT 2604 Phone: 06 272 4539 Fax: 06 272 5877 Email: [email protected] Internet: http://www.rirdc.gov.au Published in November 2000 Printed on environmentally friendly paper by Canprint ii Foreword There is increasing interest world wide in the use of green tea in beverages, cosmetics, nutriceuticals, medicinals and as flavours and fragrances. The medical research industry is increasing its focus on potential disease cures and preventatives. -

Download March 2018 Issue

ASIAN HOTEL & CATERING TIMES ASIAN HOTEL & CATERING PUBLISHED SINCE 1976 Volume 43 • Issue 03 • March 2018 DESIGN Urban resorts TEA TIME Growing market MARKET REPORT Booming Dubai TECHNOLOGY Cloud-based solutions Volume 43 Volume • Issue Hong Kong SAR HK$50 03 China RMB50 • March 2018 March Singapore S$15 BREAKING BREAD Malaysia RM30 Thailand Bt300 Rest of Asia US$10 Asia wants more EDITOR’S NOTE MANAGING EDITOR he Year of the Dog celebrations underlined once again the Neetinder Dhillon [email protected] far reaching impact of Chinese travellers who celebrated the New Year in diverse locations across the globe in Art DIRECtor staggering numbers: from Thailand to Australia, from Hatsada Tirawutsakul Cuba to London, with London even hosting one of the COORDINAtor biggest Lunar Year celebrations ever. Everybody cashed in on China’s Wajiraprakan Punyajai nationalT holiday. Dubai too rolled out the red carpet for the estimated CONTRIBUtorS 120,000 Chinese tourists; Dubai and UAE are on the list of the top 20 Donald Gasper, Zara Horner, most popular destinations for Chinese tourists. This influx is thanks to Rebecca Lo, Jane Ram, Michael Taylor, Mischa Moselle, the recent introduction of visa-on-arrival for Chinese travellers combined Victoria Burrows, Vicki Williams with high-quality hotels and high-end shopping. UAE as a whole expects ADVertISING SALES MANAGER to welcome 500,000 Chinese nationals each year by 2021, this according Virat Schlumberger to Colliers International. The same report predicts that Gulf countries will [email protected] welcome 2.5 million additional Chinese visitors by 2021. This influx of PRODUCTION MANAGER tourists to the region (not just from China) has lead to an expansion in Kanda Thanakornwongskul the hotel market with over six thousand branded hotel keys added to the CIRCULATION room inventory in UAE alone.