Fiscal 2018 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Starbucks Corp. (SBUX) Annual General Meeting

Corrected Transcript 18-Mar-2020 Starbucks Corp. (SBUX) Annual General Meeting Total Pages: 14 1-877-FACTSET www.callstreet.com Copyright © 2001-2020 FactSet CallStreet, LLC Starbucks Corp. (SBUX) Corrected Transcript Annual General Meeting 18-Mar-2020 CORPORATE PARTICIPANTS Kevin Johnson John Culver President, Chief Executive Officer & Director, Starbucks Corp. Group President-International, Channel Development and Global Coffee & Tea, Starbucks Corp. Rachel A. Gonzalez Executive Vice President, General Counsel & Secretary, Starbucks Corp. Rosalind Gates Brewer Chief Operating Officer, Group President & Director, Starbucks Corp. Justin Danhof General Counsel & Director-Free Enterprise Project, The National Patrick J. Grismer Center for Public Policy Research Executive Vice President & Chief Financial Officer, Starbucks Corp. Rossann Williams Executive Vice President & President-U.S. company-operated business and Canada, Starbucks Corp. ..................................................................................................................................................................................................................................................................... MANAGEMENT DISCUSSION SECTION Kevin Johnson President, Chief Executive Officer & Director, Starbucks Corp. Well, good morning from Seattle, Washington, and welcome to Starbucks' 28th Annual Meeting of Shareholders. I'm so pleased to have you join this webcast and I want to open by thanking the Starbucks Board of Directors, all of whom are joining -

Embracing Our Heritage and Values While Aiming Higher

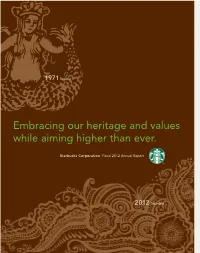

Fiscal 2012 Financial Highlights Net Revenues (in Billions) Comparable Store Sales Growth $13.3 (Company-Operated Stores Open 13 Months or Longer) $11.7 $10.7 8% $10.4 7%* 7% $9.8 –3% 1971 Seattle –6% 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 Operating Income (in Millions) Operating Margin GAAP Non-GAAP GAAP Non-GAAP 14.8% 15.0% $1,997 14.5%** 13.3% 13.5%** $1,728 $1,698** The artwork on the cover is inspired by the Siren from $1,419 $1,414** 9.2%** our original store's logo in Seattle's Pike Place Market. Embracing our heritage and values 8.1%** ** $894** The second illustration comes from the interior of our $843 5.7% 4.9% $562 first store in Mumbai, India. These drawings evoke the while aiming higher than ever. $504 Starbucks Experience, treasured in Seattle since 1971 and now around the world. Starbucks Corporation Fiscal 2012 Annual Report 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 Earnings per Diluted Share Operating Cash Flow & Capital Expenditures (in Millions) GAAP EPS Non-GAAP EPS Cash from Operations Capital Expenditures $1.79 $1,705 $1,750 $1,612 $1.62 $1.52*** $1,389 $1,259 $1.24 $1.23** $985 $856 $0.80** 2012 Mumbai $0.71** $0.52 $532 $0.43 $446 $441 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 * 2010 comparable store sales growth was calculated excluding the additional week in September 2010. ** Non-GAAP measure. Excludes $339, $332 and $53 million in pretax restructuring and transformation charges in 2008, 2009 and 2010, respectively. -

Leverage Our Buying Power with These Great Brands!

Leverage our buying power with these great brands! Dining Alliance has negotiated rebates with over 350 manufacturers on 165,000+ items & negotiated deviated pricing with manufacturers & cost-plus supplier contracts. Purchase from Manufacturers like these... ...and hundreds more. www.diningalliance.com | 307 Waverley Oaks Road, Suite 401, Waltham MA, 02452 | 617.275.8430 SELECT TOP MANUFACTURERS 3M Products Inc Niagara™ Scotch-Brite™ Scotchgard™ Aryzta LLC La Brea Bakery® La Francaise Bakery Otis Spunkmeyer® Pennant Campbell Foodservice Pepperidge Farm® Prego® Swanson® V8® Conagra Foodservice Angela Mia® Banquet Boom Chicka Pop Chef Boyardee® Gulden’s® Healthy Choice® Hebrew National® Hunt’s® Krusteaz® La Choy® Marie Callender’s Orville Pam® Peter Pan Reddi-Wip® Redenbacher’s® Slim Jim® Swiss Miss® Dart Container Corp Solo® General Mills Betty Crocker® Bisquick® Cheerios® Chex Mix® Gold Medal® Foodservice Nature Valley® Old El Paso® Pillsbury® Progresso® Yoplait Georgia Pacific Angel Soft Brawny® Dixie® Professional Series® Hormel Foods Applegate Naturals® Austin Blues® Dinty Moore® Fontanini Skippy® Corporation Spam Huhtamaki Americas Chinet® Keurig Dr Pepper 7-Up Big Red Canada Dry Clamato Crush Hawaiian Punch IBC Mott’s Mr & Mrs T’s ReaLemon Rose’s Schweppe’s Snapple Squirt Sunkist Yoo-Hoo Kraft Heinz Company Cheez Whiz Claussen Jell-O Jet Puffed Maxwell House Oscar Mayer Philadelphia Planters Shake ‘n Bake Velveeta McCormick & Company Old Bay Zatarain’s Mondelez International Chips Ahoy Fig Newton Honey Maid Nabisco Oreo Ritz Sour -

Unilever Annual Report & Accounts

DISCLAIMER This is a PDF version of the Annual Report on Form 20-F 2018 and is an exact copy of the document filed with the SEC at www.sec.gov. Certain sections of the Annual Report on Form 20-F 2018 have been audited. These are on pages 75 to 127 and the Guarantor Statements on pages 158 to 162. The maintenance and integrity of the Unilever website is the responsibility of the Directors; the work carried out by the auditors does not involve consideration of these matters. Accordingly, the auditors accept no responsibility for any changes that may have occurred to the financial statements since they were initially placed on the website. Legislation in the United Kingdom and the Netherlands governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions. Except where you are a shareholder, this material is provided for information purposes only and is not, in particular, intended to confer any legal rights on you. This Annual Report on Form 20-F does not constitute an invitation to invest in Unilever shares. Any decisions you make in reliance on this information are solely your responsibility. The information is given as of the dates specified, is not updated, and any forward-looking statements are made subject to the reservations specified in the cautionary statement on the inside back cover of the Annual Report on Form 20-F 2018. Unilever accepts no responsibility for any information on other websites that may be accessed from this site by hyperlinks. MAKING SUSTAINABLE LIVING COMMONPLACE ANNUAL REPORT ON FORM 20-F 2018 ANNUAL REPORT ON CONTENTS FORM 20-F 2018 Strategic Report .............................................................................. -

Menu Descriptions Packet

Moby Dicks Restaurant Menu & Descriptions Edited: March 2020 (prices not accurate for 2021) 11:30 AM to 9:30 PM late June through Labor Day (Closing earlier in off-season) 508.349.9795 3225 Rt. 6 Wellfleet, MA 02667 Mobys.com Soups Fried Platters Ask about quarts of soup to go! Served with French fries and cole slaw Cape Cod Clam ‘Chowdah’ Moby’s Fried Seafood Special Cup 5.75 Bowl 8.75 A heaping combination of Codfish, Scallops, Whole Belly Clams and Shrimp - MKT Lobster Bisque Cup 6.25 Bowl 9.25 Fish & Chips Absolutely the best! Hooked Atlantic cod - 19 Seafood Gumbo Lobster Cup 6.25 Bowl 9.25 We proudly serve premium hardshell Shrimp Platter lobsters coming from the cold Atlantic Wild white shrimp from the Gulf of Mexico - 19 waters. Starters Clam Strip Platter from local hard-shelled sea clams - 17 1.5 lb. or 2 lb. Lobster - MKT Moby’s Famous Outer Cape Onion Larger sizes when available or by special order A sweet Spanish onion, cut, battered and Scallop Platter deep-fried - 9 All lobsters steamed to order served with Day boat Cape Scallops - 25 drawn butter and corn on the cob. Nantucket Bucket Oyster Platter - 22 1lb. of steamers, 1lb. of mussels and corn Make it a New England Clambake Add Chatham Steamers and Potato - MKT on the cob - MKT Calamari Platter Rings & tentacles lightly fried - 16 Steamers Local Chatham steamers. Served with drawn Whole-Belly Clams butter and clam broth. 1lb. or 2lbs. - MKT Grilled & Broiled The perfect taste of Cape Cod - MKT Dinners Local Atlantic Mussels Fresh mussels steamed and served with Grilled Crab Cake Platter All served with potato & corn on cob. -

Empire of Tea

Empire of Tea Empire of Tea The Asian Leaf that Conquered the Wor ld Markman Ellis, Richard Coulton, Matthew Mauger reaktion books For Ceri, Bey, Chelle Published by Reaktion Books Ltd 33 Great Sutton Street London ec1v 0dx, uk www.reaktionbooks.co.uk First published 2015 Copyright © Markman Ellis, Richard Coulton, Matthew Mauger 2015 All rights reserved No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the publishers Printed and bound in China by 1010 Printing International Ltd A catalogue record for this book is available from the British Library isbn 978 1 78023 440 3 Contents Introduction 7 one: Early European Encounters with Tea 14 two: Establishing the Taste for Tea in Britain 31 three: The Tea Trade with China 53 four: The Elevation of Tea 73 five: The Natural Philosophy of Tea 93 six: The Market for Tea in Britain 115 seven: The British Way of Tea 139 eight: Smuggling and Taxation 161 nine: The Democratization of Tea Drinking 179 ten: Tea in the Politics of Empire 202 eleven: The National Drink of Victorian Britain 221 twelve: Twentieth-century Tea 247 Epilogue: Global Tea 267 References 277 Bibliography 307 Acknowledgements 315 Photo Acknowledgements 317 Index 319 ‘A Sort of Tea from China’, c. 1700, a material survival of Britain’s encounter with tea in the late seventeenth century. e specimen was acquired by James Cuninghame, a physician and ship’s surgeon who visited Amoy (Xiamen) in 1698–9 and Chusan (Zhoushan) in 1700–1703. -

Board of Directors

STARBUCKS CORPORATION BOARD OF DIRECTORS HOWARD SCHULTZ, 59, is the founder of Starbucks Corporation and serves as our chairman, president and chief executive officer. Mr. Schultz has served as chairman of the board of directors since our inception in 1985, and in January 2008, he reassumed the role of president and chief executive officer. From June 2000 to February 2005, Mr. Schultz also held the title of chief global strategist. From November 1985 to June 2000, he served as chairman of the board and chief executive officer. From November 1985 to June 1994, Mr. Schultz also served as president. From January 1986 to July 1987, Mr. Schultz was the chairman of the board, chief executive officer and president of Il Giornale Coffee Company, a predecessor to the Company. From September 1982 to December 1985, Mr. Schultz was the director of retail operations and marketing for Starbucks Coffee Company, a predecessor to the Company. WILLIAM W. BRADLEY, 69, has been a Starbucks director since June 2003. Since 2000, Senator Bradley has been a managing director of Allen & Company LLC, an investment banking firm. From 2001 until 2004, he acted as chief outside advisor to McKinsey & Company’s non-profit practice. In 2000, Sen. Bradley was a candidate for the Democratic nomination for President of the United States. He served as a senior advisor and vice chairman of the International Council of JP Morgan & Co. from 1997 through 1999. During that time, Sen. Bradley also worked as an essayist for CBS Evening News, and as a visiting professor at Stanford University, the University of Notre Dame and the University of Maryland. -

Seattle's Seafaring Siren: a Cultural Approach to the Branding Of

Running Head: SEATTLE’S SEAFARING SIREN 1 Seattle’s Seafaring Siren: A Cultural Approach to the Branding of Starbucks Briana L. Kauffman Master of Arts in Media Communications March 24, 2013 SEATTLE’S SEAFARING SIREN 2 Thesis Committee Starbucks Starbucks Angela Widgeon, Ph.D, Chair Date Starbucks Starbucks Stuart Schwartz, Ph.D, Date Starbucks Starbucks Todd Smith, M.F.A, Date SEATTLE’S SEAFARING SIREN 3 Copyright © 2013 Briana L. Kauffman All Rights Reserved SEATTLE’S SEAFARING SIREN 4 Abstract Many corporate brands tend to be built on a strong foundation of culture, but very minimal research seems to indicate a thorough analysis of the role of an organizational’s culture in its entirety pertaining to large corporations. This study analyzed various facets of Starbucks Coffee Company through use of the cultural approach to organizations theory in order to determine if the founding principles of Starbucks are evident in their organizational culture. Howard Schultz’ book “Onward” was analyzed and documented as the key textual artifact in which these principles originated. Along with these principles, Starbucks’ Website, Facebook, Twitter and YouTube page were analyzed to determine how Starbucks’ culture was portrayed on these sites. The rhetorical analysis of Schultz’ book “Onward” conveyed that Starbucks’ culture is broken up into a professional portion and a personal portion, each overlapping one another in its principles. After sifting through various tweets, posts and videos, this study found that Starbucks has created a perfect balance of culture, which is fundamentally driven by their values and initiatives in coffee, ethics, relationships and storytelling. This study ultimately found that Starbucks’ organizational culture is not only carrying out their initiatives that they principally set out to perform, but they are also doing so across all platforms while engaging others to do the same. -

Starbucks Corporation

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 Form 10-K ¥ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended October 2, 2005 OR n TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to . Commission File Number: 0-20322 Starbucks Corporation (Exact name of registrant as specified in its charter) Washington 91-1325671 (State or other jurisdiction of (IRS Employer incorporation or organization) Identification No.) 2401 Utah Avenue South 98134 Seattle, Washington 98134 (Zip Code) (Address of principal executive offices) (Registrant's telephone number, including area code): (206) 447-1575 Securities Registered Pursuant to Section 12(b) of the Act: None Securities Registered Pursuant to Section 12(g) of the Act: Common Stock, $0.001 Par Value Per Share Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¥ No n Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes n No ¥ Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¥ No n Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation of S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. -

Starbucks in 2018: Striving for Operational Excellence and Innovation Agility

Rev. ConfirmingRevisedDesignFirstTest Pages File CASE 29 Starbucks in 2018: Striving for Operational Excellence and Innovation Agility Arthur A. Thompson, The University of Alabama ince its founding in 1987 as a modest nine-store friends either at community tables or in lounge operation in Seattle, Washington, Starbucks areas around two fireplaces. Shad become the premier roaster, marketer, • Open 1,000 Starbucks Reserve stores worldwide and retailer of specialty coffees in the world, with to bring premium experiences to customers and over 28,200 store locations in 76 countries as of promote the company’s recently-introduced April 2018 and annual sales that were expected Starbucks Reserve coffees; these locations offered to exceed $24 billion in fiscal year 2018, ending a more intimate small-lot coffee experience and September 30. In addition to its flagship Starbucks gave customers a chance to chat with a barista brand coffees and coffee beverages, Starbucks’ other about all things coffee. The menu at Starbucks brands included Tazo and Teavana teas, Seattle’s Reserve stores included handcrafted hot and cold Best Coffee, Evolution Fresh juices and smoothies, Starbucks Reserve coffee beverages, hot and cold and Ethos bottled waters. Starbucks stores also sold teas, ice cream and coffee beverages, packages of snack foods, pastries, and sandwiches purchased Starbucks Reserve whole bean coffees, and an from a variety of local, regional, and national suppli- assortment of small plates, sandwiches and wraps, ers. In January 2107, Starbucks officially announced desserts, wines, and beer. There were four types of it would: brewing methods for the coffees and teas. • Open 20 to 30 Starbucks Reserve™ Roasteries and • Transform about 20 percent of the compa- Tasting Rooms, which would bring to life the the- ny’s existing portfolio of Starbucks stores into ater of coffee roasting, brewing, and packaging for Starbucks Reserve coffee bars. -

Demand Mounts for Directors with Digital Smarts

www.AgendaWeek.com 1 of 2 Demand Mounts for Directors With Digital Smarts By Amanda Gerut ore companies are seeking As these recent examples show, boards are Supplies Are Limited Express envisioned Leonsis as a special boardroom. And the recruits can help a experienced new directors, that’s all to directors with digital and social raiding the executive ranks of America’s assistant to CEO Kenneth Chenault to board mirror more closely the background the good, Leonsis says. “Being open to M media expertise, and the urgent top technology brands to recruit new When search rm Spencer Stuart help the company usher in a host of of its company’s customers. various types of board members, demand is prompting boards to consider directors with backgrounds in social surveyed corporate secretaries for its digital strategies. But he was soon encouraging diering ideas and some people who at rst glance would media. Why? “Social media is a 2011 Board Index, it found that appointed as a director and asked to chair At some companies, the search for social accepting those who challenge appear to be unlikely candidates. conversation and interacts with consumers demand for directors with digital the board’s new innovation and media savvy is even making the boards conventional thinking is what pumps and stakeholders,” writes eodore expertise — experience in social media, technology committee. more diverse. For instance, last March, life into a board of directors and e Starbucks board in December made Leonsis, who serves on the boards of technology and e-commerce — had AutoNation’s board appointed another ultimately the company,” he writes. -

Starbucks Corporation (Exact Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 Form 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended September 27, 2020 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to . Commission File Number: 0-20322 Starbucks Corporation (Exact Name of Registrant as Specified in its Charter) Washington 91-1325671 (State of Incorporation) (IRS Employer ID) 2401 Utah Avenue South, Seattle, Washington 98134 (206) 447-1575 (Address of principal executive office, zip code, telephone number) Securities Registered Pursuant to Section 12(b) of the Act: Title of Each Class Trading Symbol Name of Each Exchange on Which Registered Common Stock, $0.001 par value per share SBUX Nasdaq Global Select Market Securities Registered Pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.