2021 Clergy Tax Return Preparation Guide for 2020 Returns

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Creating Market Incentives for Greener Products Policy Manual for Eastern Partnership Countries

Creating Market Incentives for Greener Products Policy Manual for Eastern Partnership Countries Creating Incentives for Greener Products Policy Manual for Eastern Partnership Countries 2014 About the OECD The OECD is a unique forum where governments work together to address the economic, social and environmental challenges of globalisation. The OECD is also at the forefront of efforts to understand and to help governments respond to new developments and concerns, such as corporate governance, the information economy and the challenges of an ageing population. The Organisation provides a setting where governments can compare policy experiences, seek answers to common problems, identify good practice and work to co-ordinate domestic and international policies. The OECD member countries are: Australia, Austria, Belgium, Canada, Chile, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Israel, Italy, Japan, Korea, Luxembourg, Mexico, the Netherlands, New Zealand, Norway, Poland, Portugal, the Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States. The European Union takes part in the work of the OECD. Since the 1990s, the OECD Task Force for the Implementation of the Environmental Action Programme (the EAP Task Force) has been supporting countries of Eastern Europe, Caucasus and Central Asia to reconcile their environment and economic goals. About the EaP GREEN programme The “Greening Economies in the European Union’s Eastern Neighbourhood” (EaP GREEN) programme aims to support the six Eastern Partnership countries to move towards green economy by decoupling economic growth from environmental degradation and resource depletion. The six EaP countries are: Armenia, Azerbaijan, Belarus, Georgia, Republic of Moldova and Ukraine. -

The New Ministers Manual

The New Ministers Manual Paul W. Powell Unless otherwise identified, scripture quotations are from the Holy Bible, King James Version. Scripture identified from the New American Standard Bible, Copyright the Lockman Foundation 1960, 1962, 1968, 1971, 1972, 1973,1975,1977. Copyright 1994 Paul W. Powell All Rights Reserved ii Dedicated to The Students of Truett Seminary and all other young people on whom the mantle of ministry will fall iii iv PREFACE Thomas Jefferson once described the presidency as “a splendid misery.” I think that is an apt description of the ministry. I know of no calling that is more rewarding, and at the same time, more demanding than being a minister. The modern minister faces a multitude of tasks that are both exciting and exacting. He must conduct funerals and weddings, often on the same day. He must be a scholar, a public speaker, an educator, a financier, a CEO, a personnel manager, a shepherd and a personal counselor. While still a student at Baylor University I became pastor of an open country church. I soon found myself confronted with many things I had seen and even been a part of in my home church, but to which I paid little attention until I was called on to do them myself. In the next 34 years I pastored churches of all sizes, my last church having more than 7,000 members. As I became pastor of larger churches I would ask young ministers to assist me in funerals, weddings, baptisms, so they could learn firsthand what to do. What I have recorded in this book are some of the things I tried to teach them. -

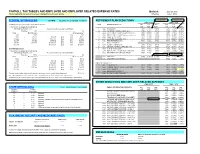

PAYROLL TAX TABLES and EMPLOYEE and EMPLOYER RELATED EXPENSE RATES Updated: June 27, 2012 *Items Highlighted in Yellow Have Been Changed Since the Last Update

PAYROLL TAX TABLES AND EMPLOYEE AND EMPLOYER RELATED EXPENSE RATES Updated: June 27, 2012 *items highlighted in yellow have been changed since the last update. Effective: July 1, 2012 FEDERAL WITHHOLDING 26 PAYS FEDERAL TAX ID NUMBER 86-6004791 RETIREMENT PLAN DEDUCTIONS 10.5% AT 50/50 10.5% AT 50/50 EMPLOYEE EMPLOYER (a) SINGLE person (including head of household) - CODE RETIREMENT PLAN DED OLD NEW DED OLD NEW If the amount of wages (after subtracting CODE RATE RATE CODE RATE RATE withholding allowances) is: The amount of income tax to withhold is: 1 ASRS PLAN-ASRS 7903 11.13% 10.90% 7904 9.87% 10.90% Not Over $83 ............................................................................................. $0 2 CORP JUVENILE CORRECTIONS (501) 7905 8.41% 8.41% 7906 9.92% 12.30% Over But not over - of excess over - 3 EORP ELECTED OFFICIALS & JUDGES (415) 7907 10.00% 11.50% 7908 17.96% 20.87% $83 - $417 10% $83 4 PSRS PUBLIC SAFETY (007) (ER pays 5% EE share) 7909 3.65% 4.55% 7910 38.30% 48.71% $417 - $1,442 $33.40 plus 15% $417 5 PSRS GAME & FISH (035) 7911 8.65% 9.55% 7912 43.35% 50.54% $1,442 - $3,377 $187.15 plus 25% $1,442 6 PSRS AG INVESTIGATORS (151) 7913 8.65% 9.55% 7914 90.08% 136.04% $3,377 - $6,954 $670.90 plus 28% $3,377 7 PSRS FIRE FIGHTERS (119) 7915 8.65% 9.55% 7916 17.76% 20.54% $6,954 - $15,019 $1,672.46 plus 33% $6,954 9 N/A NO RETIREMENT $15,019 ………………………………………………………$4,333.91 plus 35% $15,019 0 CORP CORRECTIONS (500) 7901 8.41% 8.41% 7902 9.15% 11.14% B PSRS LIQUOR CONTROL OFFICER (164) 7923 8.65% 9.55% 7924 38.77% 46.99% (b) MARRIED person F PSRS STATE PARKS (204) 7931 8.65% 9.55% 7932 18.50% 25.16% If the amount of wages (after subtracting G CORP PUBLIC SAFETY DISPATCHERS (563) 7933 7.96% 7.96% 7934 7.50% 7.90% withholding allowances) is: The amount of income tax to withhold is: H PSRS DEFERRED RET OPTION (DROP) 7957 8.65% 9.55% 0.24% AT 50/50 Not Over $312 ............................................................................................ -

412 Stephen Spencer, Anglicanism

412 Book Reviews / Ecclesiology 8 (2012) 389–420 Stephen Spencer, Anglicanism (SCM Study Guide Series, London: SCM, 2010). ix + 229 pp. £16.99. ISBN 978-0-334-04337-9 (pbk). When I was an English Anglican ordinand (late 1980s), I received four and a half hours explicit teaching on Anglicanism in three years full time train- ing. When I returned to teach at a theological college five years later, I was (I think) the first person appointed to an English Anglican theological col- lege with an explicit brief to teach Anglicanism. Since then there has been a modest explosion in the teaching of Anglicanism and in teaching resources. This latest resource, in the SCM study guide series, is a sign that teaching Anglicanism is now a mainstream commitment. There was once a deep reluctance to teach ‘Anglicanism’, partly because of significant scepticism that such a thing really existed – a scepticism which is still very much alive in England even if most of the rest of the Communion regards this scepticism as nonsensical – and perhaps also because we were anxious that actually trying to teach Anglicanism would expose its divisions and contradictions. However, certainly in England, we can no longer assume that students of Anglicanism are cradle Anglicans; we cannot assume that people will carry ‘proper’ Anglicanism in their DNA. If they are to live and minister fruitfully within the Anglican context, they must have an opportunity to study Anglicanism rigorously. Some of the ten- sions in the Anglican Communion and the Church of England are simply a result of unreflective assumptions about the content and methods of Anglicanism. -

Form W-4, Employee's Withholding Certificate

Employee’s Withholding Certificate OMB No. 1545-0074 Form W-4 ▶ (Rev. December 2020) Complete Form W-4 so that your employer can withhold the correct federal income tax from your pay. ▶ Department of the Treasury Give Form W-4 to your employer. 2021 Internal Revenue Service ▶ Your withholding is subject to review by the IRS. Step 1: (a) First name and middle initial Last name (b) Social security number Enter Address ▶ Does your name match the Personal name on your social security card? If not, to ensure you get Information City or town, state, and ZIP code credit for your earnings, contact SSA at 800-772-1213 or go to www.ssa.gov. (c) Single or Married filing separately Married filing jointly or Qualifying widow(er) Head of household (Check only if you’re unmarried and pay more than half the costs of keeping up a home for yourself and a qualifying individual.) Complete Steps 2–4 ONLY if they apply to you; otherwise, skip to Step 5. See page 2 for more information on each step, who can claim exemption from withholding, when to use the estimator at www.irs.gov/W4App, and privacy. Step 2: Complete this step if you (1) hold more than one job at a time, or (2) are married filing jointly and your spouse Multiple Jobs also works. The correct amount of withholding depends on income earned from all of these jobs. or Spouse Do only one of the following. Works (a) Use the estimator at www.irs.gov/W4App for most accurate withholding for this step (and Steps 3–4); or (b) Use the Multiple Jobs Worksheet on page 3 and enter the result in Step 4(c) below for roughly accurate withholding; or (c) If there are only two jobs total, you may check this box. -

Publication 509, Tax Calendars

Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 8 Draft Ok to Print AH XSL/XML Fileid: … tions/P509/2021/A/XML/Cycle13/source (Init. & Date) _______ Page 1 of 13 10:55 - 31-Dec-2020 The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing. Publication 509 Cat. No. 15013X Contents Introduction .................. 2 Department of the Tax Calendars Background Information for Using Treasury the Tax Calendars ........... 2 Internal Revenue General Tax Calendar ............ 3 Service First Quarter ............... 3 For use in Second Quarter ............. 4 2021 Third Quarter ............... 4 Fourth Quarter .............. 5 Employer's Tax Calendar .......... 5 First Quarter ............... 6 Second Quarter ............. 7 Third Quarter ............... 7 Fourth Quarter .............. 8 Excise Tax Calendar ............. 8 First Quarter ............... 8 Second Quarter ............. 9 Third Quarter ............... 9 Fourth Quarter ............. 10 How To Get Tax Help ........... 12 Future Developments For the latest information about developments related to Pub. 509, such as legislation enacted after it was published, go to IRS.gov/Pub509. What’s New Payment of deferred employer share of so- cial security tax from 2020. If the employer deferred paying the employer share of social security tax in 2020, pay 50% of the employer share of social security tax by January 3, 2022 and the remainder by January 3, 2023. Any payments or deposits you make before January 3, 2022, are first applied against the first 50% of the deferred employer share of social security tax, and then applied against the remainder of your deferred payments. Payment of deferred employee share of so- cial security tax from 2020. -

Tax Us If You Can 2012 FINAL.Pdf

City Research Online City, University of London Institutional Repository Citation: Murphy, R. and Christensen, J.F. (2012). Tax us if you can. Chesham, UK: Tax Justice Network. This is the published version of the paper. This version of the publication may differ from the final published version. Permanent repository link: https://openaccess.city.ac.uk/id/eprint/16543/ Link to published version: Copyright: City Research Online aims to make research outputs of City, University of London available to a wider audience. Copyright and Moral Rights remain with the author(s) and/or copyright holders. URLs from City Research Online may be freely distributed and linked to. Reuse: Copies of full items can be used for personal research or study, educational, or not-for-profit purposes without prior permission or charge. Provided that the authors, title and full bibliographic details are credited, a hyperlink and/or URL is given for the original metadata page and the content is not changed in any way. City Research Online: http://openaccess.city.ac.uk/ [email protected] tax us nd if you can 2Edition INTRODUCTION TO THE TAX JUSTICE NETWORK The Tax Justice Network (TJN) brings together charities, non-governmental organisations, trade unions, social movements, churches and individuals with common interest in working for international tax co-operation and against tax avoidance, tax evasion and tax competition. What we share is our commitment to reducing poverty and inequality and enhancing the well being of the least well off around the world. In an era of globalisation, TJN is committed to a socially just, democratic and progressive system of taxation. -

Handbook for Christian Ministries

Handbook for Christian Ministries Called to Ministry A Journey of Service Course of Study Advisory Committee-USA Clergy Development September 2005 Table of Contents Welcome to the Journey ............................................................... v Looking Ahead ........................................................................... v Stage One: The Call .................................................................... v Stage Two: Educational Preparation .............................................. v Stage Three: The Road to Ordination............................................ vi Stage Four: Lifelong Learning...................................................... vi Stage One: The Call ....................................................................... 1 A Call from God.......................................................................... 1 How Do I Know for Sure?............................................................. 1 Two Arrows, Four Quadrants ........................................................ 1 How to Pray about Your Call ......................................................... 3 Owning Your Call to Ministry......................................................... 4 Registration ............................................................................... 4 Exploring Your Call...................................................................... 4 Finding Your Place in Ministry ....................................................... 5 Discovering Your Gifts and Graces................................................ -

Can My Church Benefit from a CARES Act Forgivable Loan?

I hope this finds you well and living confidently into the times. Congress passed and the President signed the CARES Act this past Friday, March 27, 2020. I write to share specific information from the CARES Act that answers some of the questions that I have heard being asked. Can my church benefit from a CARES Act forgivable loan? This question is on the minds of most pastors and church leaders since the passage of the $2 trillion relief package. As I continue to participate in some and receive information from other webcasts and conference calls across the connection, there are some things you can begin to do to prepare to apply for the loan program. While I do not encourage you to borrow funds for normal operating expenses, it appears that this loan has the potential to become a grant that you would not need to repay. Attorneys and accountants are studying the bill and awaiting guidelines from the Small Business Administration (SBA) and the U.S. Treasury on how the CARES Act will be administered. However, it appears that churches and non-profits may be able to borrow money that could be completely forgiven if they maintain their previous 12-month staffing levels through June of 2020. Key Provisions: • Paycheck Protection Program (“PPP”) - Eligible churches and non-profits will be able to borrow up to 2.5 times their average monthly payroll and benefits up to $100,000. While this appears to cap the amount to approximately $40,000 of monthly current costs, it is not yet known if that is for all employees in the salary-paying entity or per person. -

Guidelines for Extraordinary Ministers of Holy Communion

GUIDELINES FOR EXTRAORDINARY MINISTERS OF HOLY COMMUNION The ministry of distributing Holy Communion is the responsibility of priests and deacons. It is understood that at regularly scheduled parish Masses, concelebrating priests and the deacons present and assisting at that Mass (unless impeded by physical reasons or other sufficient cause) will participate in the distribution of Holy Communion. If these ordinary ministers are not sufficient to distribute the Sacrament within a reasonable amount of time, then extraordinary ministers of Holy Communion may be invited to assist them. Canon 910.2: The extraordinary minister of Holy Communion is an acolyte or other member of the Christian faithful deputed in accord with Canon 230.3. Canon 230.3: When the need of the Church warrants it and ministers are lacking, lay persons, even if they are not lectors or acolytes, can also supply certain of their duties, namely, to exercise the ministry of the word, to preside over liturgical prayers, to confer baptism, and to distribute Holy Communion in accord with the prescripts of the law. The following policies are to be followed in the Archdiocese of New Orleans in regard to these extraordinary ministers of Holy Communion in parish celebrations. In instances other than parochial settings, the Office of Worship will be consulted. 1. Only adults (18 years and older) are to serve as extraordinary ministers of Holy Communion. Special permission has been granted by Archbishop Gregory M. Aymond which permits High School seniors to serve as extraordinary ministers of Holy Communion after completing specialized training. This special permission expires upon graduation. -

Publication 517, Social Security

Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 8 Draft Ok to Print AH XSL/XML Fileid: … tions/P517/2020/A/XML/Cycle03/source (Init. & Date) _______ Page 1 of 18 11:42 - 2-Mar-2021 The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing. Publication 517 Cat. No. 15021X Contents Future Developments ............ 1 Department of the Social Security What's New .................. 1 Treasury Internal Reminders ................... 2 Revenue and Other Service Introduction .................. 2 Information for Social Security Coverage .......... 3 Members of the Ministerial Services ............. 4 Exemption From Self-Employment Clergy and (SE) Tax ................. 6 Self-Employment Tax: Figuring Net Religious Earnings ................. 7 Income Tax: Income and Expenses .... 9 Workers Filing Your Return ............. 11 Retirement Savings Arrangements ... 11 For use in preparing Earned Income Credit (EIC) ....... 12 Worksheets ................. 14 2020 Returns How To Get Tax Help ........... 15 Index ..................... 18 Future Developments For the latest information about developments related to Pub. 517, such as legislation enacted after this publication was published, go to IRS.gov/Pub517. What's New Tax relief legislation. Recent legislation pro- vided certain tax-related benefits, including the election to use your 2019 earned income to fig- ure your 2020 earned income credit. See Elec- tion to use prior-year earned income for more information. Credits for self-employed individuals. New refundable credits are available to certain self-employed individuals impacted by the coro- navirus. See the Instructions for Form 7202 for more information. Deferral of self-employment tax payments under the CARES Act. The CARES Act al- lows certain self-employed individuals who were affected by the coronavirus and file Schedule SE (Form 1040), to defer a portion of their 2020 self-employment tax payments until 2021 and 2022. -

Curacao Highlights 2020

International Tax Curaçao Highlights 2020 Updated January 2020 Recent developments: For the latest tax developments relating to Curaçao, see Deloitte tax@hand. Investment basics: Currency – Netherlands Antilles Guilder (ANG) Foreign exchange control – A 1% license fee will be calculated as a percentage of the gross outflow of money on transfers from residents to nonresidents, and on foreign currency cash transactions. Holding companies may obtain an exemption from the fee. Accounting principles/financial statements – IAS/IFRS applies. Financial statements must be prepared annually. Principal business entities – These are the public and private company (NV and BV), general partnership, (private) foundation, Curaçao trust, limited partnership, and branch of a foreign corporation. Corporate taxation: Rates Corporate income tax rate 22%/3%/0% Branch tax rate 22%/3%/0% Capital gains tax rate 22%/3%/0% Residence – A corporation is resident if it is incorporated under the laws of Curaçao or managed and controlled in Curaçao. Basis – In principle, residents are taxed on worldwide income. Exemptions may apply for profits derived by permanent establishments located abroad. In addition, as from 1 July 2018, foreign-source income is excluded from the profit tax base (although there is an exception for certain services, including insurance and reinsurance activities; trust activities; the services of notaries, lawyers, public accountants and tax consultants; related services; income derived from the exploitation of intellectual property (IP); and shipping activities). Page 1 of 7 Curaçao Highlights 2020 Nonresidents are taxed only on Curaçao-source income. Foreign-source income derived by residents that is not excluded from the profit tax base is subject to corporation tax in the same way as Curaçao-source income.