Valustrat Dubai Real Estate Review Q1 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

GENESYS 20 Service Manual Table of Contents

GENESYS™ 20 SPECTROPHOTOMETER SERVICE MANUAL GENESYS™ 20 SPECTROPHOTOMETER SERVICE MANUAL Copyright © 1998-2002, Thermo Spectronic All rights reserved. NOTE This service manual contains information, instructions, and specifications for the GENESYS™ 20 spectrophotometer that were believed accurate at the time this manual was written. However, as part of Thermo Spectronic’s on-going program of product development, the specifications and operating instructions may be changed from time to time. Thermo Spectronic reserves the right to change such operating instructions and specifications. Under no circumstances shall Thermo Spectronic be obligated to notify purchasers of any future changes in either this or any other instructions or specifications relating to Thermo Spectronic products, nor shall Thermo Spectronic be liable in any way for its failure to notify purchasers of such changes. FCC COMPLIANCE STATEMENT FOR U.S.A. USERS This equipment generates, uses, and can radiate radio frequency energy, and if not installed and used in accordance with the reference guide, may cause interference to radio communications. It has been tested and found to comply with the limits in effect at the time of manufacture for a Class A computing device pursuant to Subpart J of Part 15 of FCC Rules, which are designed to provide reasonable protection against such interference when operated in a commercial environment. Operation of this equipment in a residential area is likely to cause interference in which case the user at his own expense will be required to take whatever measures may be required to correct the interference. i NEW PRODUCT WARRANTY Thermo Spectronic instrumentation and related accessories are warranted against defects in material and workmanship for a period of three (3) years from the date of delivery. -

Tall Buildings in 2020: COVID-19 Contributes to Dip in Year-On-Year Completions

CTBUH Year in Review: Tall Trends of 2020 Tall Buildings in 2020: COVID-19 Contributes To Dip in Year-On-Year Completions Abstract In 2020, the tall building industry constructed 106 buildings of 200 meters’ height or greater, a 20 percent decline from 2019, when 133 such buildings were completed.* The decline can be partly attributed to work stoppages and other impacts of the COVID-19 pandemic. This report provides analysis and commentary on global and regional trends underway during an eventful year. Research Project Kindly Sponsored by: Note: Please refer to Tall Buildings in Numbers—The Global Tall Building Picture: Impact of 2020 in conjunction with this Schindler paper, pages 48–49. *The study sets a minimum threshold of 200 meters’ height because of the completeness of data available on buildings of that height. Keywords: Construction, COVID-19, Development, Height, Hotel, Megatall, Mixed-Use, Office, Residential, Supertall Introduction This is the second year in a row in which Center (New York City) completed, that the the completion figure declined. In 2019, tallest building of the year was in the For many people, 2020 will be remembered the reasons for this were varied, though United States. as the year that nothing went to plan. The the change in the tall building climate in same can be said for the tall building China, with public policy statements This is also the first year since 2014 in which industry. As a global pandemic took hold in against needless production of there has not been at least one building the first quarter, numerous projects around exceedingly tall buildings, constituted a taller than 500 meters completed. -

Tall Can Be Beautiful

The Financial Express January 10, 2010 7 INDIA’S VERTICAL QUEST TALLCANBEBEAUTIFUL SCRAPINGTHE PreetiParashar 301m)—willbecompleted. FSI allowed is 1.50-2.75 in all metros and meansprojectswillbecheaperonaunit-to- ronment-friendly. ” KaizerRangwala mid-risebuildings.ThisisbecauseIndian TalltowersshouldbedesignedfortheIndi- SKY, FORWHAT? Of the newer constructions,the APIIC ground coverage is 30-40%. It is insuffi- unit basis and also more plentiful in prof- “There is a need for more service pro- cities have the lowest floor space index an context. They should take advantage of S THE WORLD’S Tower (Andhra Pradesh Industrial Infra- cient to build skyscrapers here.”He adds, itable areas,which is good news for viders of eco-friendly construction mate- Winston Churchill said, (FSI), in the world. Government regula- thelocalclimate—rainfall,light,ventilation, tallest building, the structure Corporation Tower) being built “The maximum height that can be built investors and the buyers.However, allow- rials toreducecosts,”saysPeriwal. “We make our buildings tions thatallowspecific number of build- solar orientation without sacrificing the KiranYadav theleadafterWorldWarI—again,aperiod 828-metreBurjKhalifa, at Hyderabadisexpectedtobea100-storey (basedonperacrescalculation)isapproxi- ing high-rises indiscriminately in certain However Sandhir thinks of high-rises and afterwards they make ing floors based on the land area, thus street-levelorientationof buildings;history; marked by economic growth and techno- alters the skyline of buildingwithaheightof -

Abu Dhabi Report H22012

Abu Dhabi Report H2 2012 “2012 was a pivotal year for the Abu Dhabi real estate market with the delivery of significant new developments which have raised the quality of living and working standards in the capital. The residential sub-sectors are now becoming more clearly defined by qualitative factors with tenants seeking value for money. In 2013 we expect to see a widening segregation in rental rates between the popular new developments, which, with occupancy levels rising, will be able to sustain rental levels and in some cases achieve growth, and the less popular older stock, that will continue to see rents come under downward pressure as landlords compete to maintain occupancy.“ Paul Maisfield, Associate Director & General Manager Abu Dhabi, Asteco Property Management Abu Dhabi Supply Estimates 2012 New Supply 2013 Scheduled New Supply Average Apartment Rental Rates (AED’000/pa) Apartments (in units) 9,000 12,000 Studio 1 BR 2 BR 3 BR Villas (in units) 6,000 5,000 From To From To From To From To Offices (in m2) 312,000 290,000 Marasy -- 87 110 135 170 185 237 Marina Square 55 65 75 85 110 130 140 180 Nation Towers - - 95 100 145 170 165 300 Reef Downtown - - 55 65 70 75 85 95 Residential Market Overview Rihan Heights -- 95 122 130 150 155 190 We estimate that approximately 15,000 new homes have been delivered to the Abu Dhabi market Saadiyat Beach Apartments -- 81 128 130 163 165 206 over the course of 2012, with a further 17,000 scheduled for completion in 2013. -

Cities of the Future

CITIES OF THE FUTURE CITIES OF THE FUTURE Chris Johnson, CEO of Urban Taskforce Australia, discussed the Cities of the Future at the recent API National Conference. VANESSA MITCHELL reports. 019 CITIES OF THE FUTURE SYDNEY NEEDS TO DOUBLE ITS AMOUNT OF HOMES FROM THE CURRENT 1.66 MILLION OVER THE NEXT 40 YEARS he cities of the locate growth around city centres, of tall buildings across the world. future are going to corridors and public transport nodes “Seventy-five stories is the be more urbanised, for a new way of living. We will see tallest building in Sydney currently, with higher density high-rise developments around due to aircraft restrictions, but this living—particularly railway stations and a spreading is changing. Taround public transport hubs. out to areas within walking distance “In New York we are seeing a These sometimes contentious of railway stations. trend towards tall, thin, elegant issues were discussed by Chris “This is already happening; we are buildings, such as 111 West 57th Street Johnson, Chief Executive Officer of seeing towers popping up in various (see image on previous page), which Urban Taskforce Australia, on the final areas that include a mix of residential features one apartment per floor and day of the API National Conference. and commercial offerings. What stands at over 1,400 feet. The top Chris, who is a former NSW needs to happen in the future is a apartment of this development sold Government Architect and former strong integration between transport for US$90 million recently. Executive Director at the NSW networks and the planning system, “Australia 108, featuring 100 Department of Planning, said we will and dialogue between these two areas. -

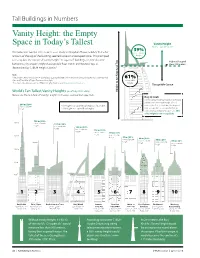

Vanity Height: the Empty Space in Today's Tallest

Tall Buildings in Numbers Vanity Height: the Empty Space in Today’s Tallest Vanity Height Non-occupiable Space 39% We noticed in Journal 2013 Issue I’s case study on Kingdom Tower, Jeddah, that a fair non-occupiable amount of the top of the building seemed to be an unoccupied spire. This prompted height us to explore the notion of “vanity height ” in supertall1 buildings, i.e., the distance Highest Occupied between a skyscraper’s highest occupiable fl oor and its architectural top, as Floor: 198 meters determined by CTBUH Height Criteria.2 Note: 1Historically there have been 74 completed supertalls (300+ m) in the world, including the now-demolished 61% One and Two World Trade Center in New York. occupiable 2 For more information on the CTBUH Height Criteria, visit http://criteria.ctbuh.org height Occupiable Space World’s Ten Tallest Vanity Heights (as of July 2013 data) Top Architectural to Height Below are the ten tallest “Vanity Heights” in today’s completed supertalls. Burj Al Arab With a vanity height of nearly 124 meters within its architectural height of 321 244 m | 29% meters, the Burj Al Arab has the highest non-occupiable * The highest occupied fl oor height as datum line. height ** The highest occupied fl oor height. non-occupiable-to-occupiable height ratio among completed supertalls. 39% of its height is non-occupiable. 133 m | 30% 200 m non-occupiable 131 m | 36% height non-occupiable 124 m | 39% height non-occupiable 113 m | 32% height non-occupiable 99 m | 31% height 150 m non-occupiable height 97 m | 31% 96 m | 29% non-occupiable -

Dubai Marina Market Report Q2 2019 Publication This Document Was Produced in 2019

Dubai Marina Market Report Q2 2019 Publication This document was produced in 2019. The data used in the tables and charts is the latest available at the time of publishing. Data sources are included for all the charts. We have detailed what we believe to be an accurate snapshot of the current market. CONTENT 04 05 06 07 Location Supply Rental Sales Overview Analysis Rates Prices 08 09 10 11 Rental Rates Sales Prices Studio Apartment One Bedroom Apartment Analysis Analysis Analysis Analysis 12 13 14 Two Bedroom Two Bedroom Two Bedroom Analysis Analysis Analysis Q2- Dubai Marina - Market Report 3 DUBAI MARINA LOCATION OVERVIEW This report analyses studio, one, and two-bedroom unit typologies within the secondary residential market, through this publication we assess the sales and rental performance and aim to highlight any key trends. With miminal rental compression, Dubai Marina remains consistent comparative to Q1, with an average area softening of only 1.33 percent. Studios were the most stable with a gradual increase 0.10 percent. One-bedrooms saw a softening of only 0.74% on Q1, two bedrooms witnessed the most compression comparing to the previous quarter of 3.36 percent. In comparison to the same quarter last year Dubai Marina remains one of the least volatile areas with rental rates only declining 10 percent. In the sales market the three typologies continued their downward projectory, with an decline 4.59 percent on Q1. Studio apartments witnessed the highest compression of 7.64 percent after a promising start to the year, one-bedrooms softened the least maintaining momentum from a relatively stable first quarter. -

The Skyscraper Surge Continues in 2015, the “Year of 100 Supertalls” Report by Jason Gabel, CTBUH; Research by Marty Carver and Marshall Gerometta, CTBUH

CTBUH Year in Review: Tall Trends All building data, images and drawings can be found at end of 2015, and Forecasts for 2016 Click on building names to be taken to the Skyscraper Center The Skyscraper Surge Continues in 2015, The “Year of 100 Supertalls” Report by Jason Gabel, CTBUH; Research by Marty Carver and Marshall Gerometta, CTBUH Note: Please refer to “Tall Buildings in Numbers – 2015: A Tall Building Review” in conjunction with this paper, pages 9–10 The Council on Tall Buildings and Urban the previous record high of 99 completions 2010, the number of supertalls in the world Habitat (CTBUH) has determined that 106 in 2014. This brings the total number of has exactly doubled, from 50 at the end of buildings of 200 meters’ height or greater 200-meter-plus buildings in the world to 2010 to 100 at the end of 2015. were completed around the world in 2015 – 1,040, exceeding 1,000 for the first time in setting a new record for annual tall building history and marking a 392% increase from The tallest building to complete in 2015 completions (see Figure 3). the year 2000, when only 265 existed. was Shanghai Tower, now the tallest building in China and the second-tallest in Further Highlights: A total of 13 supertalls (buildings of 300 the world at 632 meters. This had notable The 106 buildings completed in 2015 beat meters or higher) were completed in 2015, effects on the list of the 10 tallest buildings, every previous year on record, including the highest annual total on record. -

Development News Highlights MANHATTAN - MID 2ND QUARTER 2016 Looking Ahead

Development News Highlights MANHATTAN - MID 2ND QUARTER 2016 Looking Ahead Midtown East Rezoning Proposal – Progress Update The massive up-zoning initiative initially proposed back in 2012 during the Bloomberg administration is slowly moving closer to being put into effect. Created in an effort to spark revitalization of the area anchored by Grand Central Terminal, as well as preserve historic landmarks, the proposal had been rejected by City Council members in November 2013; and ultimately withdrawn prior to former Mayor Bloomberg stepping down. Since the changeover of administrations, efforts were reinitiated by Mayor de Blasio. Recent news brought the welcomed announcement that the city administration is hoping to fi nalize their proposal and enter it into the Uniform Land Use Review Process (ULURP) before the end of the year. July 2014 a group called the East Midtown Steering Committee was created. Members of the group represented a wide range of interests including community members, elected offi cials, real estate executives and preservationists. The committee was assigned the task of spearheading the Greater Midtown East rezoning identifi ed as the 2nd Phase that will affect 73-blocks within the Midtown East neighborhood. By getting input upfront from the community and stakeholders prior to the ULURP public review process, it was hoped that the proposal would gain stronger support upon coming up for a vote. A detailed report presenting the committee’s draft plan with recommendations for the up-zoning initiative of the corridor roughly bound by East 57th- and East 39th Streets to the north and south, and 3rd- and 5th Avenues to the east and west was released in October 2015. -

Are Australia's Cities Outgrowing Its

ARE AUSTRALIA’S CITIES OUTGROWING ITS CONSTRUCTION LEGISLATION? MATTHEW BELL* This article examines the way in which legislative regulation seeks to enhance consumer protection in relation to the procurement of residential construction work. Its focus is upon reforms to the statutory regime for such protection in Victoria which were enacted during 2016–17. These reforms are primarily directed towards reducing the incidence of defective work through the tightening of ‘quality assurance’ provisions, such as ensuring that work is carried out by qualified practitioners, and of ‘safety net’ measures such as conciliation processes to avoid the escalation of disputes. The article analyses these reforms by reference to identified problems relating to defective residential construction work. These range from high-profile incidents such as the 2014 cladding-related fire at the Lacrosse Apartments in Melbourne (and the fire, with similar causes yet tragically more disastrous consequences, at the Grenfell Tower in London in 2017), through to more mundane — yet, frequently occurring — problems such as poor workmanship and behaviours. The article concludes that the Victorian reforms are clearly directed towards many of these identified problems. It cautions, however, that the success of the reforms in contributing to an effective consumer protection regime may be limited because other factors contributing to the widespread incidence of defects remain unaddressed. These factors include gaps such as the non-prescriptive nature of many of the regulatory requirements, and the limited capacity of project participants to assimilate the detailed requirements of the regime, and for regulators to enforce it. I INTRODUCTION AND OUTLINE Australia has, according to its national anthem, ‘boundless plains to share’. -

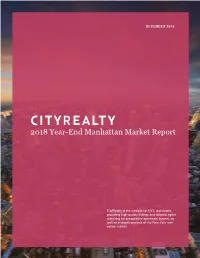

2018 Year-End Manhattan Market Report Here

THE CITYREALTY YEAR-END REPORT DECEMBER 2018 DECEMBER 2018 2018 Year-End Manhattan Market Report CityRealty is the website for NYC real estate, providing high-quality listings and tailored agent matching for prospective apartment buyers, as well as in-depth analysis of the New York real estate market. 1 THE CITYREALTY YEAR-END REPORT DECEMBER 2018 Summary After years of soaring prices, Manhattan residential real estate contiues to cool off with condos showing slight declines and transaction volume substantially down. Total apartment sales over $10 million are projected to reach $4.4 billion by the end of 2018, down from $4.6 billion in 2017. AVERAGE SALES PRICE 2018: $2.06 Million CONDOS AND CO-OPS 2017: $2.16 Million MEDIAN SALES PRICE CONDOS CO-OPS 2018: $1.72 Million 2018: $855,000 2017: $1.84 Million 2017: $845,000 The median sales price of all apartments in 2018 was $1.2 million, down from $1.25 million in 2017. There was a slight decrease in the median price of condos, which fell to $1.72 million from $1.84 million in 2017. Co-ops, however, rose to a median price of $855,000 from $845,000 in 2017. CONDO AVERAGE PRICE/FT2 2018 2017 $1,802/ft2 $1,861/ft2 The average price of a condo in 2018, $2.88 million, was down from $3.05 million the year prior. The average price per square foot dipped slightly to $1,802, down from $1,861 in 2017. 2018 2017 $2.88M $3.05M AVERAGE SALES PRICE AVERAGE SALES PRICE CONDO CONDO $1.4M $1.37M AVERAGE SALES PRICE AVERAGE SALES PRICE CO-OP CO-OP Note: 2018 statistics are based on closings recorded through Nov. -

Taipei 101 Striving to Be a Sustainable Skyscraper 3

ctbuh.org/papers Title: Taipei 101 Striving to be a Sustainable Skyscraper Authors: Harace Lin, Chairman , Taipei Financial Center Corporation Yvonne Lin, Executive Director, Hong Kuo Group Subjects: Architectural/Design Sustainability/Green/Energy Keywords: Economics Environment Office Social Interaction Sustainability Publication Date: 2012 Original Publication: CTBUH 2012 9th World Congress, Shanghai Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Harace Lin; Yvonne Lin Taipei 101 Striving to be a Sustainable Skyscraper 台北101: 一座永续发展的超高层建筑 Abstract Taipei Financial Corporation (TFCC), similar to most super high-rise developers, has gone through its share of challenges throughout the relatively short span of the building’s existence; from the early days of planning and design, through construction and subsequent management. But after only 13 years of successfully navigating numerous obstacles, the TAIPEI 101 project can already be considered to have achieved its original objective to be truly sustainable. Such sense of success could not be achieved without the integration and Harace Lin Hong-Ming Yvonne Lin accomplishment of three critical aspects – Economical, Environmental, and Social. Keywords: Sustainability; Tall Building; Skyscraper; Taipei; TAIPEI 101 Harace Lin Hong-Ming Taipei Financial Center Corporation 59F, TAIPEI 101, No.7 XinYi Rd. Sec.5 Taipei, 110 , Taiwan tel (电话): +886 (2) 8101 7777 fax (传真): +886 (2) 8101 8949 email (电子邮箱): [email protected] 摘要 www.taipei-101.com.tw 台北金融大楼公司(TFCC)从规划设计初期、实际兴建一直到后续展开营运,在整体建 Harace Lin Hong-Ming is the Chairman and President of Taipei Financial Center Corp., and is responsible for 物并不算长的存在时间中,与其他超高建筑物的开发者一样都经历了各种严峻的挑战。 the investment, construction and management of 不过,度过了13年克服万难的岁月,台北101大楼已经达成了各面向主要目标,成为永 TAIPEI 101.