Abu Dhabi Report H22012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Valustrat Dubai Real Estate Review Q1 2019

Real Estate Market 1st Quarter | 2019 Review Real VPI Residential VPI Residential VPI Office Estate Capital Values Rental Values Capital Values Performance -12.4% -9.0% -14.4% Q1 Y-o-Y Q1 Y-o-Y Q1 Y-o-Y Market Intelligence. VPI Simplified. ValuStrat Price Index Source: ValuStrat Source: ValuStrat Source: ValuStrat Key Indicators Source: REIDIN, DTCM, ValuStrat Residential Off-Plan Residential Off-Plan Residential Ready Residential Ready Residential Sales Ticket Size Sales Volume Sales Ticket Size Sales Volume Rents 1.59m 4,418 1.64m 2,677 94,929 AED Transactions AED Transactions AED p.a. 24.6% 4.8% 7.0% -0.9% -1.9% Q-o-Q Q-o-Q Q-o-Q Q-o-Q Q-o-Q Hotel Average Hotel Office Sales Office Sales Office Daily Rate Occupancy Ticket Size Volume Rents 465 78% 1.05m 387 968 AED Jan-Dec 2018 Jan-Dec 2018 AED Transactions AED/sq m p.a. -5.5% 2.0% -17.5% 64.0% -1.0% Y-o-Y Q-o-Q Q-o-Q Q-o-Q Q-o-Q Increase Stable Decline 1 | Dubai Real Estate Market 1st Quarter 2019 Review VPI ValuStrat Price Index Residential The valuation-based ValuStrat Price Index (VPI) for Dubai’s residential capital values, VPI - Dubai Residential Capital Values displayed an overall 12.4% annual fall in 16 Apartment and 10 Villa Locations [Base: Jan 2014=100] capital values, with quarterly declines of 3.2%. This downward trend resulted in 27.1% 110 citywide capital value loss since the peaks of 98.0 97.9 97.5 97.5 97.0 100 96.7 96.2 95.4 mid-2014. -

Sample 20. UAE: Abu Dhabi

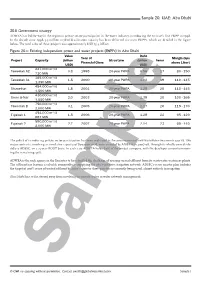

Sample 20. UAE: Abu Dhabi 20.11 Government strategy ADWEA has led the way in the region in private sector participation in the water industry, introducing the emirate’s first IWPP in 1998. In the decade since 1998, 3.3 million m3/d of desalination capacity has been delivered via seven IWPPs, which are detailed in the figure below. The total value of these projects was approximately USD 13.4 billion. Figure 20.x: Existing independent power and water projects (IWPPs) in Abu Dhabi Value Debt Year of Margin (bps Project Capacity (billion Structure (billion Tenor Financial Close above Libor) USD) USD) 227,000 m³/d Taweelah A2 0.8 1998 20-year PWPA 0.56 17 80 - 150 710 MW 385,000 m³/d Taweelah A1 1.5 2000 20-year PWPA 1.02 19 110 - 145 1,350 MW 454,000 m³/d Shuweihat 1.8 2001 20-year PWPA 1.28 20 110 - 145 1,500 MW 430,000 m³/d Umm al-Nar 2.0 2003 20-year PWPA 1.39 20 100 - 165 1,550 MW 750,000 m³/d Taweelah B 3.1 2005 20-year PWPA 2.17 20 115 - 170 2,000 MW 454,000 m³/d Fujairah 1 1.5 2006 20-year PWPA 1.28 22 65 - 120 887 MW 590,000 m³/d Fujairah 2 2.7 2007 20-year PWPA 2.14 23 65 - 110 2,000 MW The policy of introducing private sector participation has been replicated in the procurement of new wastewater-treatment capacity. Two major contracts, involving a cumulative capacity of 800,000 m3/d, were awarded by ADWEA in 2007-08, through its wholly owned sub- sidiary ADSSC, on a 25-year BOOT basis. -

List of References by Mbm

LIST OF REFERENCES BY MBM RAISED FLOOR RAISED FLOOR- REFERENCES PROJECT NAME CLIENT CONTRACTOR MANUFACTURER YEAR ABU DHABI WATER & ELECTRICITY AL AIN GAS TURBINE HOUSE TARGET ENGG. CONST. CO. UNIFLAIR 1993 DEPT ABU DHABI WATER & ELECTRICITY ABU DHABI GAS TURBINE HOUSE TARGET ENGG. CONST. CO. UNIFLAIR 1993 DEPT MUSSAFAH OFFSHORE ADDCAP COSTAIN ENGG. & CONST. UNIFLAIR 1994 LNG PLANT, DAS ISLAND ADGAS C.C.I.C. UNIFLAIR 1994 RENOVATION OF VILLA IN ABU DHABI PRIVATE POLENSKY & ZOELLINER UNIFLAIR 1994 BLDG. FOR MR. HATHBOUR AL RUMAITHI D.S.S.C.B. RANYA CONTG. CO. UNIFLAIR 1994 MIRFA GAS PIPELINE ADCO DODSAL PRIVATE LTD. UNIFLAIR 1995 ABU DHABI INT'L AIRPORT ABU DHABI DUTY FREE DECO EMIRATES UNIFLAIR 1995 ABU DHABI INT'L AIRPORT, EXT. TO TRANSIT ABU DHABI DUTY FREE DECO EMIRATES UNIFLAIR 1995 HOTEL GA MUBARRAZ ISLAND ADNOC TARGET ENGG. CONST. UNIFLAIR 1995 RAS AL KHAIMAH CEMENT FACTORY RAS AL KHAIMAH CEMENT COSTAIN ENGG. & CONST. UNIFLAIR 1995 RENOVATION OF COMPLEX IN ABU DHABI MINISTRY OF INTERIOR AL MANSOURI 3 B UNIFLAIR 1995 31 December 2020 2 RAISED FLOOR- REFERENCES PROJECT NAME CLIENT CONTRACTOR MANUFACTURER YEAR W.E.D. GAS TURBINE PACKAGE AT AUH & AL AIN MARUBENI CORPORATION U.T.S. KENT UNIFLAIR 1995 ETISALAT TELECOM. BLDG. AT BARAHA, DUBAI ETISALAT UNITY CONTG. CO. UNIFLAIR 1995 ETISALAT TELECOM. BLDG.AT SHJ. IND. AREA ETISALAT UNITY CONTG. CO. UNIFLAIR 1995 NATIONAL BANK OF ABU DHABI NATIONAL BANK OF ABU DHABI A.C.C. UNIFLAIR 1995 ETISALAT TELECOM. & ADMIN. BLDG. , FUJAIRAH ETISALAT COSTAIN ABU DHABI CO. UNIFLAIR 1995 ETISALAT TELECOM. & ADMIN .BLDG., RAK ETISALAT COSTAIN ABU DHABI CO. -

Technological Advances and Trends in Modern High-Rise Buildings

buildings Article Technological Advances and Trends in Modern High-Rise Buildings Jerzy Szolomicki 1,* and Hanna Golasz-Szolomicka 2 1 Faculty of Civil Engineering, Wroclaw University of Science and Technology, 50-370 Wroclaw, Poland 2 Faculty of Architecture, Wroclaw University of Science and Technology, 50-370 Wroclaw, Poland * Correspondence: [email protected]; Tel.: +48-505-995-008 Received: 29 July 2019; Accepted: 22 August 2019; Published: 26 August 2019 Abstract: The purpose of this paper is to provide structural and architectural technological solutions applied in the construction of high-rise buildings, and present the possibilities of technological evolution in this field. Tall buildings always have relied on technological innovations in engineering and scientific progress. New technological developments have been continuously taking place in the world. It is closely linked to the search for efficient construction materials that enable buildings to be constructed higher, faster and safer. This paper presents a survey of the main technological advancements on the example of selected tall buildings erected in the last decade, with an emphasis on geometrical form, the structural system, sophisticated damping systems, sustainability, etc. The famous architectural studios (e.g., for Skidmore, Owings and Merill, Nikhen Sekkei, RMJM, Atkins and WOHA) that specialize, among others, in the designing of skyscrapers have played a major role in the development of technological ideas and architectural forms for such extraordinary engineering structures. Among their completed projects, there are examples of high-rise buildings that set a precedent for future development. Keywords: high-rise buildings; development; geometrical forms; structural system; advanced materials; damping systems; sustainability 1. -

Valustrat Abu Dhabi Real Estate Review Q2 2021

Abu Dhabi Real Estate Market 2021 Quartely Review www.valustrat.com 2nd Quarter Market Intelligence. VPI Simplified. ValuStrat Price Index REAL ESTATE PERFORMANCE VPI Residential VPI Residential Capital Values Rental Values 67.3 77.7 Base: Q1 2016=100 Base: Q1 2016=100 2.1% 4.3% Q-o-Q Q-o-Q Source: ValuStrat KEY INDICATORS Source: ValuStrat, REIDIN, STR Apartment Villa Apartment Villa Asking Sales Price Asking Sales Price Asking Rents Asking Rents 12,491 10,596 118,000 213,700 AED/sq m AED/sq m 2 Bedrooms (AED p.a.) 4 Bedrooms (AED p.a.) 3.5% 9.3% 4.9% 3.6% Q-o-Q Q-o-Q Q-o-Q Q-o-Q Hotel Hotel Office Office Average Daily Rate Occupancy Asking Sales Price Asking Rents 481.5 62% 10,370 860 (AED) Mar 2021 Mar 2021 AED/sq m AED/sq m p.a. 18.6% 4.2% -10.1% 1.9% Y-o-Y Y-o-Y Q-o-Q Q-o-Q Increase Stable Decline 1 | Abu Dhabi Real Estate Market 2nd Quarter 2021 Review Market Intelligence. VPI Simplified. ValuStrat Price Index RESIDENTIAL The valuation based ValuStrat Price VPI - ABU DHABI RESIDENTIAL CAPITAL VALUES Index (VPI) for capital values in 5 Villa and 5 Apartment Locations Abu Dhabi’s residential investment [Base: Q1 2016=100] zones for the second quarter 2021, increased 2.1% quarterly to 65.8 points. This was the first time the 4.1% VPI has witnessed three consecutive 92.4 90.3 88.5 87.1 85.5 83.8 quarters of growth since 2016, 81.1 2.1% 77.6 75.1 72.7 70.9 69.1 aggregating 7.2% since Q4 2020. -

List of Pharmaceutical Providers Within UAE for Daman's Health Insurance Plans

List of Pharmaceutical Providers within UAE for Daman ’s Health Insurance Plans (InsertDaman TitleProvider Here) Network - List of Pharmaceutical Providers within UAE for Daman’s Health Insurance Plans This document lists out the Pharmacies and Hospitals available in Daman’s Network, dispensing prescribed medicines, for Daman’s Health Insurance Plan (including Essential Benefits Plan, Classic, Care, Secure, Core, Select, Enhanced, Premier and CoGenio Plan) members. Daman also covers its members for other inpatient and outpatient services in its network of Health Service Providers (including hospitals, polyclinics, diagnostic centers, etc.). For more details on the other health service providers, please refer to the Provider Network Directory of your plan on our website www.damanhealth.ae or call us on the toll free number mentioned on your Daman Card. Edition: October 01, 2015 Exclusive 1 covers CoGenio, Premier, Premier DNE, Enhanced Platinum Plus, Select Platinum Plus, Enhanced Platinum, Select Platinum, Care Platinum DNE, Enhanced Gold Plus, Select Gold Plus, Enhanced Gold, Select Gold, Care Gold DNE Plans Comprehensive 2 covers Enhanced Silver Plus, Select Silver Plus, Enhanced Silver, Select Silver Plans Comprehensive 3 covers Enhanced Bronze, Select Bronze Plans Standard 2 covers Care Silver DNE Plan Standard 3 covers Care Bronze DNE Plan Essential 5 covers Core Silver, Secure Silver, Core Silver R, Secure Silver R, Core Bronze, Secure Bronze, Care Chrome DNE, Classic Chrome, Classic Bronze Plans 06 covers Classic Bronze -

Case Study: Gate Towers, Abu Dhabi

ctbuh.org/papers Title: Case Study: Gate Towers, Abu Dhabi Authors: Gurjit Singh, Chief Development Officer, Aldar Properties Hossam Eldin Elsouefi, Senior Project Manager, Aldar Properties Peter Brannan, Managing Director, Arquitectonica Subjects: Architectural/Design Building Case Study Keywords: Construction Design Process Façade Skybridges Publication Date: 2013 Original Publication: CTBUH Journal, 2013 Issue IV Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Gurjit Singh; Hossam Eldin Elsouefi; Peter Brannan About the Council The Council on Tall Buildings and Urban Habitat, based at the Illinois Institute of CTBUH Journal Technology in Chicago, is an international International Journal on Tall Buildings and Urban Habitat not-for-profi t organization supported by architecture, engineering, planning, development, and construction professionals. Founded in 1969, the Council’s mission is to disseminate multi-disciplinary information on Tall buildings: design, construction, and operation | 2013 Issue IV tall buildings and sustainable urban environments, to maximize the international interaction of professionals involved in creating Case Study: Gate Towers, Abu Dhabi the built environment, and to make the latest knowledge available to professionals in a useful Designing Tall to Promote Physical Activity in China form. The Monadnock Building, Technically Reconsidered The CTBUH disseminates -

Of Abu Dhabi Emirate, United Arab Emirates MARINE and COASTAL ENVIRONMENTS of ABU DHABI EMIRATE, UNITED ARAB EMIRATES

of Abu Dhabi Emirate, United Arab Emirates MARINE AND COASTAL ENVIRONMENTS OF ABU DHABI EMIRATE, UNITED ARAB EMIRATES Page . II of Abu Dhabi Emirate, United Arab Emirates Page . III MARINE AND COASTAL ENVIRONMENTS OF ABU DHABI EMIRATE, UNITED ARAB EMIRATES Page . IV MARINE AND COASTAL ENVIRONMENTS OF ABU DHABI EMIRATE, UNITED ARAB EMIRATES H. H. Sheikh Khalifa bin Zayed Al Nahyan President of the United Arab Emirates Page . V MARINE AND COASTAL ENVIRONMENTS OF ABU DHABI EMIRATE, UNITED ARAB EMIRATES Page . VI MARINE AND COASTAL ENVIRONMENTS OF ABU DHABI EMIRATE, UNITED ARAB EMIRATES H. H. Sheikh Mohammed bin Zayed Al Nahyan Crown Prince of Abu Dhabi, Deputy Supreme Commander of the UAE Armed Forces Page . VII MARINE AND COASTAL ENVIRONMENTS OF ABU DHABI EMIRATE, UNITED ARAB EMIRATES Page . VIII MARINE AND COASTAL ENVIRONMENTS OF ABU DHABI EMIRATE, UNITED ARAB EMIRATES H. H. Sheikh Hamdan bin Zayed Al Nahyan Deputy Prime Minister Page . IX MARINE AND COASTAL ENVIRONMENTS OF ABU DHABI EMIRATE, UNITED ARAB EMIRATES s\*?*c*i]j6.%;M"%&9+~)#"$*&ENL`\&]j6. =';78G=%1?%&'12= !"##$" 9<8*TPEg-782#,On%O)6=]KL %&'( )*+,-. 2#,On#X%3G=FON&$4#*.%&9+~)#"$*&XNL %?)#$*&E, &]1TL%&9+%?)':5=&4O`(.#`g-78 %!/ اﻷوراق اﻟﻘﻄﺎﻋﻴﺔ fJT=V-=>?#Fk9+*#$'&= /%*?%=*<(/8>OhT7.F 012(.%34#56.%-78&9+:;(<=>=?%@8'-/ABC $L#01i%;1&&!580.9,q@EN(c D)=EF%3G&H#I7='J=:KL)'MD*7.%&'-(8=';78G=NO D)$8P#"%;QI8ABCRI7S;<#D*T(8%.I7)=U%#$#VW'.X JG&Bls`ItuefJ%27=PE%u%;QI8)aEFD)$8%7iI=H*L YZZ[\&F]17^)#G=%;/;!N_-LNL`%3;%87VW'.X NL]17~Is%1=fq-L4"#%;M"~)#"G=,|2OJ*c*TLNLV(ItuG= )aE0@##`%;Kb&9+*c*T(`d_-8efJG=g-78012 -

Valustrat Abu Dhabi Real Estate Review Q4 2019

Real Estate Market 4th Quarter | 2019 Review VPI Residential VPI Residential Real Capital Values Rental Values Estate 69.1 71.5 Performance (Base Q1 2016=100) (Base Q1 2016=100) -11.0% -9.3% Y-o-Y Y-o-Y Market Intelligence. VPI Simplified. ValuStrat Price Index Source: ValuStrat Key Indicators Source: ValuStrat, REIDIN, DCTAD Apartment Asking Villa Asking Apartment Villa Sales Price Sales Price Asking Rents Asking Rents 13,005 9,943 112,500 187,734 AED/sq m AED/sq m 2 Bedrooms (AED p.a.) 4 Bedrooms (AED p.a.) -1.6% -3.4% -2.8% -3.6% Q-o-Q Q-o-Q Q-o-Q Q-o-Q Hotel Average Hotel Office Asking Office Asking Room Rate Occupancy Sales Price Rents 343 73% 10,889 827 (AED) Jan-Sep Jan-Sep AED/sq m AED/sq m p.a. 10.9% 1.1% 2.5% -1.1% Y-o-Y Y-o-Y Q-o-Q Q-o-Q Increase Stable Decline 1 | Abu Dhabi Real Estate Market 4th Quarter 2019 Review VPI ValuStrat Price Index Residential The valuation based ValuStrat Price VPI - Abu Dhabi Residential Capital Values Index (VPI) for capital values in Abu 5 Villa and 5 Apartment Locations Dhabi’s residential investment zones [Base: Q1 2016=100] for the fourth quarter 2019, declined 2.6% quarterly to 69.1 points. Annually, capital values were 11% 120 100.0 lower than the fourth quarter 2018. 96.4 95.4 94.1 100 92.4 90.3 88.5 87.1 85.5 83.8 81.1 The weighted average residential 77.6 80 75.1 72.7 value this quarter was AED 9,246 per 70.9 69.1 sq m (AED 859 per sq ft), apartments stood at AED 10,236 per sq m (AED 60 951 per sq ft), and villas at AED 6,910 per sq m (AED 642 per sq ft). -

GENESYS 20 Service Manual Table of Contents

GENESYS™ 20 SPECTROPHOTOMETER SERVICE MANUAL GENESYS™ 20 SPECTROPHOTOMETER SERVICE MANUAL Copyright © 1998-2002, Thermo Spectronic All rights reserved. NOTE This service manual contains information, instructions, and specifications for the GENESYS™ 20 spectrophotometer that were believed accurate at the time this manual was written. However, as part of Thermo Spectronic’s on-going program of product development, the specifications and operating instructions may be changed from time to time. Thermo Spectronic reserves the right to change such operating instructions and specifications. Under no circumstances shall Thermo Spectronic be obligated to notify purchasers of any future changes in either this or any other instructions or specifications relating to Thermo Spectronic products, nor shall Thermo Spectronic be liable in any way for its failure to notify purchasers of such changes. FCC COMPLIANCE STATEMENT FOR U.S.A. USERS This equipment generates, uses, and can radiate radio frequency energy, and if not installed and used in accordance with the reference guide, may cause interference to radio communications. It has been tested and found to comply with the limits in effect at the time of manufacture for a Class A computing device pursuant to Subpart J of Part 15 of FCC Rules, which are designed to provide reasonable protection against such interference when operated in a commercial environment. Operation of this equipment in a residential area is likely to cause interference in which case the user at his own expense will be required to take whatever measures may be required to correct the interference. i NEW PRODUCT WARRANTY Thermo Spectronic instrumentation and related accessories are warranted against defects in material and workmanship for a period of three (3) years from the date of delivery. -

List of World's Tallest Buildings in the World

Height Height Rank Building City Country Floors Built (m) (ft) 1 Burj Khalifa Dubai UAE 828 m 2,717 ft 163 2010 2 Shanghai Tower Shanghai China 632 m 2,073 ft 121 2014 Saudi 3 Makkah Royal Clock Tower Hotel Mecca 601 m 1,971 ft 120 2012 Arabia 4 One World Trade Center New York City USA 541.3 m 1,776 ft 104 2013 5 Taipei 101 Taipei Taiwan 509 m 1,670 ft 101 2004 6 Shanghai World Financial Center Shanghai China 492 m 1,614 ft 101 2008 7 International Commerce Centre Hong Kong Hong Kong 484 m 1,588 ft 118 2010 8 Petronas Tower 1 Kuala Lumpur Malaysia 452 m 1,483 ft 88 1998 8 Petronas Tower 2 Kuala Lumpur Malaysia 452 m 1,483 ft 88 1998 10 Zifeng Tower Nanjing China 450 m 1,476 ft 89 2010 11 Willis Tower (Formerly Sears Tower) Chicago USA 442 m 1,450 ft 108 1973 12 Kingkey 100 Shenzhen China 442 m 1,449 ft 100 2011 13 Guangzhou International Finance Center Guangzhou China 440 m 1,440 ft 103 2010 14 Dream Dubai Marina Dubai UAE 432 m 1,417 ft 101 2014 15 Trump International Hotel and Tower Chicago USA 423 m 1,389 ft 98 2009 16 Jin Mao Tower Shanghai China 421 m 1,380 ft 88 1999 17 Princess Tower Dubai UAE 414 m 1,358 ft 101 2012 18 Al Hamra Firdous Tower Kuwait City Kuwait 413 m 1,354 ft 77 2011 19 2 International Finance Centre Hong Kong Hong Kong 412 m 1,352 ft 88 2003 20 23 Marina Dubai UAE 395 m 1,296 ft 89 2012 21 CITIC Plaza Guangzhou China 391 m 1,283 ft 80 1997 22 Shun Hing Square Shenzhen China 384 m 1,260 ft 69 1996 23 Central Market Project Abu Dhabi UAE 381 m 1,251 ft 88 2012 24 Empire State Building New York City USA 381 m 1,250 -

Allen & Overy in the Middle East

Allen & Overy in the Middle East 2019 allenovery.com 2 Allen & Overy in the Middle East | 2019 Clients praise the firm as “really cutting-edge in their approach. The quality of their work in many respects is unparalleled. It’s very good to have them working with you.” Chambers Global 2019 (Middle East Projects & Energy) “Allen & Overy LLP provides ‘excellent advice, combining technical expertise and commerciality’ .” Legal 500 2018 (UAE, Real Estate) “Allen & Overy LLP handles big-ticket deals across the UAE and the wider Middle East.” Legal 500 2017 (UAE) © Allen & Overy LLP 2019 3 Contents Covering your needs – Supporting you globally 4 Allen & Overy in the Middle East 6 Our regional presence 8 Independent market recognition 10 Awards 11 Sector expertise 13 Banking 14 Project finance 15 Financial services regulatory 17 Corporate and M&A 19 Telecommunications, Media and Technology 22 Equity capital markets 24 Debt capital markets 26 Industry recognition 28 Investment funds 32 Litigation and arbitration 34 Real estate and hospitality 36 Construction 39 Key contacts 41 allenovery.com 4 Allen & Overy in the Middle East | 2019 Covering your needs – Supporting you globally GLOBAL KEY FACTS 5,400 2,800 People Lawyers over firm Single global 40 over 550 Partners 1profit pool Offices of the top 100 public 83% companies assisted 30 worldwide in FY17 Countries (Forbes, May 2017) On average we advise our Top 50 clients in 74% 19% 19 of our work involved of AO’s work comes countries 2 or more offices from high growth markets Our lawyers were ranked