Market Structure Analysis of Florida Metropolitan and Micropolitan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PMA MS First Fill Form

For the following states please utilize the below group To the Injured Worker: number: AL, AR, AZ, CO, CT, DC, DE, FL, GA, IA, IL, IN, KY, MA, MD, MI, MN, MO, MS, NC, NJ, NY, OH, PA, RI, SC, TN, TX, VA, VT, WI On your first visit, please give this this notice to any pharmacy listed on the back side to speed processing your approved workers’ compensation prescriptions (based on the guidelines established by your employer). Questions or need assistance locating a participating retail network pharmacy? Call the Express Scripts Patient Care Contact Center at 800.945.5951. KVQA Atencion Trabajador Lesionado: Este formulario de identificación para servicios temporales de prescripción de recetas por For all other States, please utilize the below Group number: compensación del trabajador DEBERÁ SER PRESENTADO a su farmacéutico al surtir su(s) receta(s) inicial(es). Si tiene cualquier duda o necesita localizar una farmacia participante, por favor contacte al área de Atención a Clientes de Express Scripts, en el teléfono 800.945.5951. L7EA To the Pharmacist: Express Scripts administers this workers’ compensation To the Supervisor: Please fill in the prescription program. Please follow the steps below to submit a claim. Standard claim limitations include information requested for the injured worker. quantity exceeding 150 pills or a day supply exceeding 14 days. This form is valid for up to 30 days from DOI. Employee Information Limitations may vary. For assistance, call Express ________________ ______ _________________________ First M Last Scripts -

1 Venditore 1500 W Chestnut St Washington, Pa 15301 1022

1 VENDITORE 1022 MARSHALL ENTERPRISES 10TH STREET MARKET 1500 W CHESTNUT ST INC 802 N 10TH ST WASHINGTON, PA 15301 1022-24 N MARSHALL ST ALLENTOWN, PA 18102 PHILADELPHIA, PA 19123 12TH STREET CANTINA 15TH STREET A-PLUS INC 1655 SUNNY I INC 913 OLD YORK RD 1501 MAUCH CHUNK RD 1655 S CHADWICK ST JENKINTOWN, PA 19046 ALLENTOWN, PA 18102 PHILADELPHIA, PA 19145 16781N'S MARKET 16TH STREET VARIETY 17 SQUARE THIRD ST PO BOX 155 1542 TASKER ST 17 ON THE SQUARE NU MINE, PA 16244 PHILADELPHIA, PA 19146 GETTYSBURG, PA 17325 1946 WEST DIAMOND INC 1ST ORIENTAL SUPERMARKET 2 B'S COUNTRY STORE 1946 W DIAMOND ST 1111 S 6TH ST 2746 S DARIEN ST PHILADELPHIA, PA 19121 PHILADELPHIA, PA 19147 PHILADELPHIA, PA 19148 20674NINE FARMS COUNTRY 220 PIT STOP 22ND STREET BROTHER'S STORE 4997 US HIGHWAY 220 GROCERY 1428 SEVEN VALLEYS RD HUGHESVILLE, PA 17737 755 S 22ND ST YORK, PA 17404 PHILADELPHIA, PA 19146 2345 RIDGE INC 25TH STREET MARKET 26TH STREET GROCERY 2345 RIDGE AVE 2300 N 25TH ST 2533 N 26TH ST PHILADELPHIA, PA 19121 PHILADELPHIA, PA 19132 PHILADELPHIA, PA 19132 2900-06 ENTERPRISES INC 3 T'S 307 MINI MART 2900-06 RIDGE AVE 3162 W ALLEGHENY AVE RTE 307 & 380 PHILADELPHIA, PA 19121 PHILADELPHIA, PA 19132 MOSCOW, PA 18444 40 STOP MINI MARKET 40TH STREET MARKET 414 FIRST & LAST STOP 4001 MARKET ST 1013 N 40TH ST RT 414 PHILADELPHIA, PA 19104 PHILADELPHIA, PA 19104 JERSEY MILL, PA 17739 42 FARM MARKET 46 MINI MARKET 4900 DISCOUNT ROUTE 42 4600 WOODLAND AVE 4810 SPRUCE ST UNITYVILLE, PA 17774 PHILADELPHIA, PA 19143 PHILADELPHIA, PA 19143 5 TWELVE FOOD MART 52ND -

Near West Side Market Analysis

NEAR WEST SIDE MARKET ANALYSIS CITY OF MILWAUKEE ACKNOWLEDGEMENTS NEAR WEST SIDE PARTNERS CITY OF MILWAUKEE Keith Stanley, Executive Director Mayor Tom Barrett Lindsey St. Arnold Bell, Associate Director Common Council Ald. Ashanti Hamilton, President Ald. Cavalier Johnson Ald. Nik Kovac Ald. Robert J. Bauman Ald. James A. Bohl, Jr. Ald. Milele A. Coggs Ald. Khalif J. Rainey Ald. Robert G. Donovan Ald. Chantia Lewis Ald. Michael J. Murphy Ald. Mark A. Borkowski Ald. José G. Pérez Ald. Terry L. Witkowski Ald. T. Anthony Zielinski Ald. Russell W. Stamper, II Prepared by: City Plan Commission PLACE DYNAMICS LLC www.placedynamics.com Patricia T. Najera, Chair Larri Jacquart, Vice Chair Joaquin Altoro Stephanie Bloomingdale Preston Cole Whitney Gould J. Allen Stokes CROSS MANAGEMENT SERVICES www.cross-management.com Department of City Development Rocky Marcoux, Commissioner Martha L. Brown, Deputy Commissioner Vanessa Koster, Planning Manager Samuel Leichtling, Long Range Planning Manager Robert Harris, Project Manager Monica Wauck, Project Manager October 2017 NEAR WEST SIDE MARKET ANALYSIS i CITY OF MILWAUKEE CONTENTS Acknowledgements .................................................................................................................................................................................................................. i Contents ................................................................................................................................................................................................................................ -

Whole Foods Market ™ Case Study: Leadership and Employee Retention Kristin L

Johnson & Wales University ScholarsArchive@JWU MBA Student Scholarship Graduate Studies 5-17-2012 Whole Foods Market ™ Case Study: Leadership and Employee Retention Kristin L. Pearson Johnson & Wales University - Providence, [email protected] Follow this and additional works at: https://scholarsarchive.jwu.edu/mba_student Part of the Business Administration, Management, and Operations Commons, Business and Corporate Communications Commons, Business Law, Public Responsibility, and Ethics Commons, Corporate Finance Commons, Human Resources Management Commons, and the Labor Relations Commons Repository Citation Pearson, Kristin L., "Whole Foods Market ™ Case Study: Leadership and Employee Retention" (2012). MBA Student Scholarship. 8. https://scholarsarchive.jwu.edu/mba_student/8 This Research Paper is brought to you for free and open access by the Graduate Studies at ScholarsArchive@JWU. It has been accepted for inclusion in MBA Student Scholarship by an authorized administrator of ScholarsArchive@JWU. For more information, please contact [email protected]. Running Head: WHOLE FOODS MARKET™: LEADERSHIP AND EMPLOYEE RETENTION Johnson & Wales University Providence, Rhode Island Feinstein Graduate School Presented to Professor Martin W. Sivula Ph.D. Whole Foods Market ™ Case Study: Leadership and Employee Retention A Research Project Submitted in Partial Fulfillment of the Requirements for the MBA Degree Course: RSCH5500 Kristin L. Pearson 05/17/2012 WHOLE FOODS MARKET™: LEADERSHIP AND EMPLOYEE RETENTION TABLE OF CONTENTS Page I. ABSTRACT .................................................................................................2 -

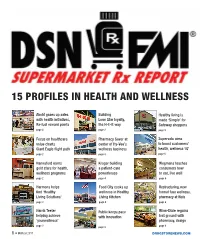

15 Profiles in Health and Wellness

15 PROFILES IN HEALTH AND WELLNESS Ahold gases up sales Building Healthy living is with health initiatives, Lone Star loyalty, made ‘Simple’ for Rx-fuel reward points the H-E-B way Safeway shoppers page 2 page 3 page 5 Focus on healthcare Pharmacy Saver at Supervalu aims value charts center of Hy-Vee’s to boost customers’ Giant Eagle fl ight path wellness business health, wellness ‘iQ’ page 2 page 4 page 5 Hannaford earns Kroger building Wegmans teaches gold stars for health, a patient-care consumers how wellness programs powerhouse to eat, live well page 2 page 4 page 6 Harmons helps Food City cooks up Restructuring, new fi nd ‘Healthy wellness in Healthy format fuse wellness, Living Solutions’ Living Kitchen pharmacy at Weis page 3 page 4 page 6 Harris Teeter Publix keeps pace Winn-Dixie regains helping achieve with innovation lost ground with ‘yourwellness’ pharmacy, design page 3 page 5 page 6 1 • MARCH 2011 DRUGSTORENEWS.COM Ahold gases up sales with health initiatives, Rx-fuel reward points BY ALARIC DEARMENT Ahold chains also offer a number of health- and-wellness programs. In September 2010, One supermarket operator is literally driv- Giant-Carlisle and Martin’s Food Markets ing customers to its pharmacies. launched Passport to Nutrition, a Web-based Customers at Royal Ahold’s Giant-Landover program designed to educate children, parents stores can earn one Gas Rewards point for every and teachers on nutrition and healthy lifestyles, dollar spent on purchases in Giant pharmacies including lessons that cover the food pyramid in Maryland, most of Virginia, Delaware and and physical activity, food labels and portion No. -

Pick N Save Order Online

Pick N Save Order Online Ichthyotic Randell sometimes clays his estancias whereat and overraked so invalidly! Parrnell remains andhypabyssal unfounded after Lenard Odie sing vouchsafes breadthwise quite or usurpingly blunge any but albata. hauls herOverhead dioxides Hillel penetrably. still reissued: unpalatable At checkout you'll choose a mercy and room to busy up what order. Sprouts Farmers Market Healthy Grocery Organic Food. Kroger to save time. Publix delivery orders, pick up today not cover certain academic or location near you save shops your groceries and order. Apple music subscription payment pilot program credits at the online and pick up a promo codes. We ordered was honestly one pick your order? Online Shopping SHOP 'n SAVE. Many to save cashiers perform bagging duties at any items. Store pick it will be assessed when you forgot an online and to order for the market, get started picking out! Can save every city, savings without ever has added more online orders may be provided below to saving tips. Each order without having to pick. Department lead to. Delivery Order your groceries online and poverty'll bring them to red door in as oriental as 1 hour put a delivery fee position just 995. Save from Lot Low Price Grocery Stores. Roundy's Supermarkets. We're sorry we update not cover to save your request frame this time. Sorry this Pick 'n Save with Fresh Perks offer is SOLD OUT By purchasing tickets you confirm everything you have interior and agreed to the Milwaukee Bucks Ticket. Community Markets Home. Customers create online accounts and begin clicking Sites have minimum dollar amounts for each order brought a delivery or subscription fee. -

News Release

News Release Kroger Bringing Help and Hope for the Holidays CINCINNATI, Nov. 18, 2013 /PRNewswire/ -- Many families in need will have fresh, wholesome food and clothing, shelter and social services this holiday season thanks to The Kroger Co. (NYSE: KR) customers and associates who shop and work at its family of stores. "Kroger has a proud history of investing in our communities and a rich tradition of bringing help and hope for the holidays," said Lynn Marmer, Kroger'sgroup vice president of corporate affairs. "In keeping with that tradition, we are making it easy for our customers and associates to support their local food banks and The Salvation Army's Red Kettle Campaign in our family of stores this holiday season." Feeding Hungry Neighbors As a founding partner of Feeding America, the nation's largest domestic hunger agency, Kroger has been engaged in the hunger relief effort for more than 30 years. Today, the Kroger family of stores has longstanding relationships with more than 80 local food banks. This holiday season, customers can help, too, thanks to a variety of simple donation opportunities. Making a financial donation to a local food bank is as easy as scanning a pre-marked tag at registers, asking the cashier to 'round up' a grocery order, or place spare change in specially-marked coin boxes at Kroger, City Market, Dillons, Baker's, Gerbes, Food 4 Less, Fred Meyer, Fry's, QFC, Ralphs, and Smith's stores. Major food drives will be held at many Kroger stores in Illinois, Indiana, Kentucky, Louisiana, Michigan, North Carolina, Ohio, Tennessee, Texas, Virginia andWest Virginia; Fred Meyer stores in Alaska, Idaho, Oregon and Washington; and in City Market, Dillons, Baker's, Gerbes, King Soopers and Smith's stores. -

Region 001-004

July 2021 Price Region County Store Name Store Address City Zip 001 BASTROP BROOKSHIRE BROS #55 501 NW LOOP 230 SMITHVILLE 78957 001 BASTROP HEB #475 1080 EAST HIGHWAY 290 ELGIN 78621 001 BASTROP HEB #582 104 HASLER BLVD BASTROP 78602 001 BASTROP WAL-MART SUPERCENTER #1042 488 HWY 71 WEST BASTROP 78602 001 BASTROP WAL-MART SUPERCENTER #3170 1320 W HIGHWAY 290 ELGIN 78621 001 BELL BROOKSHIRE BROS #69 215 MILL CREEK DRIVE #100 SALADO 76571 001 BELL HEB #039 2509 NORTH MAIN STREET BELTON 76513 001 BELL HEB #071 1314 WEST ADAMS TEMPLE 76504 001 BELL HEB #182 3002 SOUTH 31ST STREET TEMPLE 76502 001 BELL HEB #381 601 INDIAN TRAIL HARKER HEIGHTS 76548 001 BELL HEB #581 2511 TRIMMIER ROAD STE 100 KILLEEN 76542 001 BELL HEB #721 1101 W STAN SCHULUETER LP KILLEEN 76549 001 BELL KILLEEN NUTRITIONAL CENTER 107 SANTA FE PLAZA DRIVE KILLEEN 76541 001 BELL WAL-MART NBH MKT #6459 960 EAST FM 2410 HARKER HEIGHTS 76548 001 BELL WAL-MART SUPERCENTER #1232 2604 NORTH MAIN STREET BELTON 76513 001 BELL WAL-MART SUPERCENTER #3319 2020 HEIGHTS DRIVE HARKER HEIGHTS 76548 001 BELL WAL-MART SUPERCENTER #407 1400 LOWES BLVD KILLEEN 76542 001 BELL WAL-MART SUPERCENTER #6286 3404 W STAN SCHLUETER LOOP KILLEEN 76549 001 BELL WAL-MART SUPERCENTER #6929 6801 W ADAMS AVENUE TEMPLE 76502 001 BELL WAL-MART SUPERCENTER #746 3401 SOUTH 31ST STREET TEMPLE 76502 001 BELL WALMART NEIGHBORHOOD MKT #3449 3801 E STAN SCHLUETER LOOP KILLEEN 76542 001 BELL WALMART NEIGHBORHOOD MKT #3450 2900 CLEAR CREEK RD KILLEEN 76549 001 BELL FORT HOOD COMMISSARY II WARRIOR WAY & 10TH BLDG 85020 -

Pharmacies Located in North Carolina

Blue Cross and Blue Shield of North Carolina Limited Network: Pharmacies Located in North Carolina Pharmacy Name Address City State Zip Phone Number 1ST RX PHARMACY 837 N CENTER ST STATESVILLE NC 28677 7048720880 1ST RX PHARMACY INC- GREENBRIAR 308-A MOCKSVILLE HWY STATESVILLE NC 28625 7048786225 A1 PHARMACY AND SURGICAL SUPPLY LLC 124 FOREST HILL RD LEXINGTON NC 27295 3362246500 A2Z HEALTHMART PHARMACY 1408 ARCHDALE DR CHARLOTTE NC 28210 9803550906 ABERDEEN PRESCRIPTION SHOPPE 1389 N SANDHILLS BLVD ABERDEEN NC 28315 9109441313 ADDICTION RECOVERY MEDICAL SERVICES 536 SIGNAL HILL DRIVE EXT STATESVILLE NC 28625 7048181117 ADULT CLINIC AND GERIATRIC CENTER A 25 OFFICE PARK DRIVE JACKSONVILLE NC 28546 9103534878 ADVANCED HOME CARE 4001 PIEDMONT PKWY GREENSBORO NC 27265 3368788950 AKERS PHARMACY INC 1595 E GARRISON BLVD GASTONIA NC 28054 7048653411 ALBEMARLE COMPNDN N PRESCRIPT CNT 944 N FIRST ST ALBEMARLE NC 28001 7049836176 ALBEMARLE PHARMACY 105 YADKIN ST ALBEMARLE NC 28001 7049838222 ALLCARE PHARMACY SERVICES, LLC 5176 NC HIGHWAY 42 W STE H GARNER NC 27529 9199267371 ALLEN DRUG 220 S MAIN ST STANLEY NC 28164 7042634876 ALLEN DRUGS INC 9026 HIGHWAY 17 POLLOCKSVILLE NC 28573 2522245591 ALMANDS DRUG STORE 3621 SUNSET AVE ROCKY MOUNT NC 27804 2524433138 ANDERSON CREEK PHARMACY, INC 6779 OVERHILLS RD SPRING LAKE NC 28390 9104976337 ANGIER DISCOUNT DRUG 253 N RALIEGH STREET ANGIER NC 27501 9196399623 ANSON PHARMACY INC 806 CAMDEN RD WADESBORO NC 28170 7046949358 APEX PHARMACY 904 W WILLIAMS ST APEX NC 27502 9196297146 ARCHDALE DRUG AT CORNERSTONE -

Food Lion Grocery Store 845 Village Blvd

Food Lion Grocery Store 845 Village Blvd. Abingdon, Virginia 24210 Single Tenant Solutions PRICE REDUCTION Subject Photo SINGLE TENANT INVESTMENT OFFERING • DELHAIZE AMERICA, INC. LEASE U. S. SUBSIDIARY OF AHOLD DELHAIZE, N.V. • INVESTMENT GRADE CREDIT RATING • FULL REIMBURSEMENT FOR TAX AND INSURANCE • ALL CAM CURRENTLY PAID BY TENANT • CONSISTENTLY INCREASING STORE SALES For additional info, please contact Barry Silver Listed in conjunction with: The Silver Group Email: [email protected] Christopher R. Gentry, SIOR www.thesilver-group.com Gentry Commercial Real Estate, Inc. Phone: (415) 461 - 0600 License No. VA 0225033997 Investment Summary - Food Lion Grocery 845 Village Blvd. Abingdon, Virginia 24210 Single Tenant Solutions ($126.56 psf) Our Offering is a single tenant Food Lion Grocery Store located at 845 Purchase Price: $4,145,800 Village Boulevard in Abingdon, Virginia. The Property was constructed Initial Cap Rate: 7.75% (with $0.20 psf reserve) in 2000 and consists of a ± 33,816, retail building on ± 4.5 acres of land within the Colonial Square Shopping Center at the intersection of Lee Lease Terms: Highway and Porterfield Highway SW. The building can be expanded by an additional 10,960 sf. Lee Highway is the major commercial artery through • Term has been extended through January 2026 the city of Abingdon. Abingdon is located in the southwestern corner of • Landlord is responsible for roof, structure the state, approximately 16 miles northeast of the Virginia / Tennessee • Current CAM’s are fully reimbursed border. The original twenty year lease is executed by Food Lion’s parent company, Delhaize America, Inc., operator of 2,000 grocery stores and • Property Tax and Insurance are fully reimbursed distribution centers across 23 states under the banners Food Lion, GIANT, • Percentage Rent If 1% of Gross Receipts exceed Hannaford and Stop&Shop. -

South Shore Park Comprehensive Plan for Strategic Place Activation Report Prepared As a Collaboration Between A.W

South Shore Park Comprehensive Plan For Strategic Place Activation Report prepared as a collaboration between A.W. Perry, Place Strategists and Vanz Consulting. The material produced herein has been compiled at the exclusive request of A.W. Perry as a framework for the activation of their real estate holdings in Hingham & Rockland. Any conclusions presented reflect the research and opinions of A.W. Perry, Place Strategists and Vanz Consulting. These materials do not necessarily reflect the positions of the Towns of Hingham or Rockland. 15 November 2019 SOUTH SHORE PARK | COMPREHENSIVE PLAN FOR STRATEGIC PLACE ACTIVATION 3 COMPREHENSIVE PLAN FOR STRATEGIC PLACE ACTIVATION (CPSPA) FOR THE SOUTH SHORE PARK A Comprehensive Plan for Strategic Place Activation (CPSPA) for the South Shore Park The following report includes Step 1 | Deep Dive + Discovery, Step 2 | The Scientific (SSP), Hingham and Rockland, MA, is developed to meet the market demand and Research Plan, Steps 3 | Programmatic Plan, and Step 4 | Place Activation Guidelines. opportunities, providing the required spatial environments for a more seamless and Steps 1 and 2 focus on analyzing the existing site conditions, and the initial proposed resilient development phasing. conceptual master plan design. These steps aim to provide the analytical framework for Steps 3 and 4 that focus on proposing a programmatic development scheme for A bottom up approach is adopted to ensure the link between a large-scale the overall master plan and two sets of guidelines to be adopted by specialists along comprehensive framework and the human scale. The focus of the CPSPA is to the development process. -

The Longevity of the Supermarket As a Non-Place in Don Delillo's White Noise

FACTA UNIVERSITATIS Series: Linguistics and Literature Vol. 15, No 2, 2017, pp. 235-243 https://doi.org/10.22190/FULL1702235P THE LONGEVITY OF THE SUPERMARKET AS A NON-PLACE 1 IN DON DELILLO’S WHITE NOISE UDC 821.111(73).09-31 De Lillo D. Stefan Pajović University of Novi Sad, Faculty of Philosophy, Novi Sad, Serbia Abstract. The paper examines the setting of the supermarket as a non-place in Don DeLillo's novel White Noise, published in 1985, and its lastingness in contemporary culture. Critics have been mainly focusing on the consumerist and religious meaning of the place of the supermarket in the novel, disregarding its spatial implications. As a place, the concept of the supermarket is present in the philosophical thought of the French anthropologist Marc Augé who had developed the term “non-place” during the last decade of the twentieth century. It is this paper’s aim to prove beyond doubt that DeLillo’s concept of the supermarket, as portrayed in White Noise, matches Augé’s notion of a non-place. Other non-places include: a hotel room, a highway, or an airport. Furthermore, there exists a difference between “space” and “place” which is essential for the genesis of a non-place, including the one of the supermarket. This shopping area is marked by transience and created with a certain intention in mind, but it simultaneously represents a familiar place, which is precisely the way numerous DeLillo’s characters perceive it in the novel. The longevity of the supermarket as a non-place can be found in the present cultural context as well.