Quarter 1 Appendix a , Item 13. PDF 301 KB

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BERKSHIRE PROSPECTUS AMBITION, COLLABORATION and GROWTH Thames Valley Berkshire LEP Berkshire Prospectus Local Authorities As Well As Other Key Stakeholders

BERKSHIRE PROSPECTUS AMBITION, COLLABORATION AND GROWTH 02 THE BERKSHIRE Berkshire Prospectus Berkshire PROSPECTUS THE OPPORTUNITIES IN THIS PROSPECTUS It is no coincidence that this prospectus for Berkshire has been released in tandem with the Thames Valley Berkshire Local Enterprise Partnership (LEP) Recovery and REPRESENT A CHANCE Renewal Plan. The two documents sit alongside each other, evidencing the formidable collaborative nature of how TO RESET POST COVID the LEP is working in partnership with the six Berkshire Local Authorities as well as other key stakeholders. AND MAKE BERKSHIRE This prospectus clearly identifies several key schemes and projects which, when delivered, will greatly enhance Berkshire’s appeal as a place to live and EVEN BETTER work in the years ahead. The projects highlighted in this prospectus represent unique opportunities for new investment that will appeal to a wide range of partners, locally, regionally and nationally. The LEP and Local Authorities will work alongside private and public sector colleagues to facilitate the development and successful delivery of these great opportunities. COLLABORATIVE WORKING We should highlight the constructive partnership between the Local Authorities and the LEP, who together have forged a great working relationship with One Public Estate (OPE). Established in 2013, OPE now works nationally with more than 300 councils.These projects are transforming local communities and public services right across the country. They provide technical support and funding to councils to deliver ambitious property and place-focused programmes in collaboration with central government and other public sector partners. Thames Valley Berkshire LEP Berkshire Thames Valley 03 As highlighted in the Recovery and Renewal Plan, Thames Valley Berkshire is more than the sum of its parts. -

List of Councils in England by Type

List of councils in England by type There are a total of 353 councils in England: Metropolitan districts (36) London boroughs (32) plus the City of London Unitary authorities (55) plus the Isles of Scilly County councils (27) District councils (201) Metropolitan districts (36) 1. Barnsley Borough Council 19. Rochdale Borough Council 2. Birmingham City Council 20. Rotherham Borough Council 3. Bolton Borough Council 21. South Tyneside Borough Council 4. Bradford City Council 22. Salford City Council 5. Bury Borough Council 23. Sandwell Borough Council 6. Calderdale Borough Council 24. Sefton Borough Council 7. Coventry City Council 25. Sheffield City Council 8. Doncaster Borough Council 26. Solihull Borough Council 9. Dudley Borough Council 27. St Helens Borough Council 10. Gateshead Borough Council 28. Stockport Borough Council 11. Kirklees Borough Council 29. Sunderland City Council 12. Knowsley Borough Council 30. Tameside Borough Council 13. Leeds City Council 31. Trafford Borough Council 14. Liverpool City Council 32. Wakefield City Council 15. Manchester City Council 33. Walsall Borough Council 16. North Tyneside Borough Council 34. Wigan Borough Council 17. Newcastle Upon Tyne City Council 35. Wirral Borough Council 18. Oldham Borough Council 36. Wolverhampton City Council London boroughs (32) 1. Barking and Dagenham 17. Hounslow 2. Barnet 18. Islington 3. Bexley 19. Kensington and Chelsea 4. Brent 20. Kingston upon Thames 5. Bromley 21. Lambeth 6. Camden 22. Lewisham 7. Croydon 23. Merton 8. Ealing 24. Newham 9. Enfield 25. Redbridge 10. Greenwich 26. Richmond upon Thames 11. Hackney 27. Southwark 12. Hammersmith and Fulham 28. Sutton 13. Haringey 29. Tower Hamlets 14. -

Foi 6711 Q & A

FOI’s received and answered – October 2014 FOI 6711 Q I request a list of Business Rate accounts that meet the following criteria: 1. Current overpayment/credit shown if credit balance hasn’t been carried forward 2. Accounts where a ‘write on’ has been used since 1st April 2000 to cancel an overpayment which has not since been reversed FOI 6711 A If you would like a copy of the attachment sent in response to this request please email [email protected] and quote the above reference. FOI 6712 Q Please can you provide me with the information in relation to business rates accounts in your area. (a) Addresses of all commercial properties that currently have a credit on their account above £1,000. (b) The names and addresses of the ratepayer of the property referred to in (a) if they are NOT a sole trader or individual. (c) The amount by which the account is in credit (d) The rating year that the credit arose (e) The date the information was generated. FOI 6712 A If you would like a copy of the attachment sent in response to this request please email [email protected] and quote the above reference. FOI 6713 Q Please would the Council, firstly, confirm that the department known as "Children's Social Services/Care" comply - at all times - with the Children Act 1989? Please would the Council also confirm that it uses "Risk Assessments" when complying with the Children Act 1989? Please would the Council provide me with one blank copy of all of the various Risk Assessment forms used by the Council "prior" to approaching the Courts in respect of applications -

Future Libraries: Change, Options and How to Get There

Culture, tourism and sport Future libraries Change, options and how to get there Learning from the Future Libraries Programme Phase 1 Contents Preface 2 Executive summary 4 Introduction 5 The reform and change model 6 Part One: Four models of reform 9 Service location and distribution 9 New provider models 10 Shared services across council boundaries 12 Empowering communities to do things their way 13 Part Two: The ingredients for generating change 16 Political and managerial leadership 16 Governance arrangements 17 Positioning library service to priority outcomes 19 Internal capacity to support change 20 Digital opportunities 22 External support and challenge 23 Analysis of need 24 Understanding current and cost performance 25 User and community engagement 26 Partner and stakeholder engagement 27 Future libraries 31 Further information 32 Appendix: The pilot change projects 33 Preface When we launched the Future Libraries We have been hugely encouraged by the Programme in August last year, it was progress so far and with the partnerships that in recognition of our shared belief that have developed. The ten phase one projects innovation, led by the energy and experience have commissioned practical support and of local authorities themselves, was going advice to develop a wide range of options to provide the best recipe for modernising and ideas to save money while minimising libraries. the need for cuts to front line services and meeting communities’ needs. These include There was an exceptional level of interest new collaborations across council and in the programme – 51 projects submitted organisational boundaries, the use of digital expressions of interest with the participation opportunities and closer engagement with of over 100 local authorities. -

(Public Pack)Minutes Document for Thames Valley Berkshire City Deal

THAMES VALLEY BERKSHIRE CITY DEAL (ELEVATE BERKSHIRE) JOINT COMMITTEE 17 JULY 2015 11.30 AM - 12.30 PM Present: Councillor Stuart Munro, Wokingham Borough Council Councillor Alan Law, West Berkshire Council Councillor Phillip Bicknell, Royal Borough of Windsor & Maidenhead Councillor Marc Brunel-Walker, Bracknell Forest Council Councillor Sohail Munawar, Slough Borough Council Councillor Tony Page, Reading Borough Council Co-opted Members: Tim Smith, Thames Valley Berkshire Local Enterprise Partnership Also Present: Sue Brackley, Reading Borough Council Mark Browne, West Berkshire Council Shanzeeda Chowdhury, Slough Borough Council Rhian Hayes, Wokingham Borough Council Joanne Horton, Royal Borough of Windsor & Maidenhead Emelye Janes, Reading Borough Council Rohit Paul, Reading Borough Council Anneken Priesack, Bracknell Forest Council Grant Thornton, Reading Borough Council Philip Wright, Slough Borough Council Apologies for absence were received from: Councillor Rob Anderson, Slough Borough Council Councillor Jo Lovelock, Reading Borough Council 25. Apologies for Absence and Substitute Members The Committee noted that apologies had been received from Councillors Anderson and Lovelock. In addition Councillor Bicknell had replaced Councillor Kellaway as the representative of the Royal Borough of Windsor & Maidenhead. Katharine Horler was to replace Steve Lamb as one of the Thames Valley Berkshire LEP’s representatives. 26. Election of Chairman RESOLVED that Councillor Munro be re-elected Chairman of the Joint Committee for the ensuing municipal year. 27. Appointment of Vice-Chairman RESOLVED that Councillor Bicknell be elected Vice-Chairman of the Joint Committee for the ensuing municipal year. 28. Minutes RESOLVED that the minutes of the meeting of the Committee held on 23 January 2015 be approved as a correct record and signed by the Chairman. -

Local Authority / Combined Authority / STB Members (July 2021)

Local Authority / Combined Authority / STB members (July 2021) 1. Barnet (London Borough) 24. Durham County Council 50. E Northants Council 73. Sunderland City Council 2. Bath & NE Somerset Council 25. East Riding of Yorkshire 51. N. Northants Council 74. Surrey County Council 3. Bedford Borough Council Council 52. Northumberland County 75. Swindon Borough Council 4. Birmingham City Council 26. East Sussex County Council Council 76. Telford & Wrekin Council 5. Bolton Council 27. Essex County Council 53. Nottinghamshire County 77. Torbay Council 6. Bournemouth Christchurch & 28. Gloucestershire County Council 78. Wakefield Metropolitan Poole Council Council 54. Oxfordshire County Council District Council 7. Bracknell Forest Council 29. Hampshire County Council 55. Peterborough City Council 79. Walsall Council 8. Brighton & Hove City Council 30. Herefordshire Council 56. Plymouth City Council 80. Warrington Borough Council 9. Buckinghamshire Council 31. Hertfordshire County Council 57. Portsmouth City Council 81. Warwickshire County Council 10. Cambridgeshire County 32. Hull City Council 58. Reading Borough Council 82. West Berkshire Council Council 33. Isle of Man 59. Rochdale Borough Council 83. West Sussex County Council 11. Central Bedfordshire Council 34. Kent County Council 60. Rutland County Council 84. Wigan Council 12. Cheshire East Council 35. Kirklees Council 61. Salford City Council 85. Wiltshire Council 13. Cheshire West & Chester 36. Lancashire County Council 62. Sandwell Borough Council 86. Wokingham Borough Council Council 37. Leeds City Council 63. Sheffield City Council 14. City of Wolverhampton 38. Leicestershire County Council 64. Shropshire Council Combined Authorities Council 39. Lincolnshire County Council 65. Slough Borough Council • West of England Combined 15. City of York Council 40. -

Valuing the Benefits from Trees in Slough

Valuing the benefits from trees in Slough • • • Thames Valley Environmental Records Centre Sharing environmental information in Berkshire and Oxfordshire 01865 815 451 [email protected] www.tverc.org VALUING THE BENEFITS FROM TREES IN SLOUGH MARCH 2019 Follow us on Twitter @TVERC1 Dan Carpenter, TVERC Projects Manager March 2019 Page| 1 TVERC is hosted by Oxfordshire County Council Valuing the benefits from trees in Slough • • • VALUING THE BENEFITS FROM TREES IN SLOUGH SUMMARY Trees and woodland provide a number of benefits to society, which are termed ecosystem services. These benefits include the storage and capture of carbon, rainfall interception, shading and many others. These services are provided for free by nature to society. It is possible to value some of these services in economic terms by calculating the cost of society providing these services in another way without the benefit of nature. TVERC used the i‐Tree Canopy tool to estimate tree cover and the benefits that these trees provide. Based on this study, Slough has an estimated tree canopy cover of 16.8%. This tree cover provides annual benefits of approximately £380,000 to the residents and businesses of Slough. Tree canopy cover in Slough is below the recommended target for urban tree cover of 20%. Dan Carpenter, TVERC Projects Manager March 2019 Page| 2 TVERC is hosted by Oxfordshire County Council Valuing the benefits from trees in Slough • • • CONTENTS Valuing the benefits from trees in Slough 2 Summary 2 Contents 3 1. Introduction 4 2. Method 4 3. Results 6 4. Discussion 8 5. Summary and Recommendations 8 Recommendations for further work 8 6. -

Q2 1617 LA Referrals

Referrals to Local Authority Adoption Agencies from First4Adoption by region Q2 July-September 2016 Yorkshire & The Humber LA Adoption Agencies North East LA Adoption Agencies Durham County Council 13 North Yorkshire County Council* 30 1 Northumberland County Council 8 Barnsley Adoption Fostering Unit 11 South Tyneside Council 8 Rotherham Metropolitan Borough Council 11 2 North Tyneside Council 5 Bradford Metropolitan Borough Council 10 Redcar Cleveland Borough Council 5 Hull City Council 10 1 Web Referrals Phone Referrals Middlesbrough Council 3 East Riding Of Yorkshire Council 9 City Of Sunderland 2 Cumbria County Council 7 Gateshead Council 2 Calderdale Metropolitan Borough Council 6 1 Newcastle Upon Tyne City Council 2 0 3.5 7 10.5 14 Leeds City Council 6 1 Web Referrals Phone Referrals Doncaster Metropolitan Borough Council 5 Hartlepool Borough Council 4 North Lincolnshire Adoption Service 4 1 City Of York Council 3 North East Lincolnshire Adoption Service 3 1 Darlington Borough Council 2 Kirklees Metropolitan Council 2 1 Sheffield Metropolitan City Council 2 Wakefield Metropolitan District Council 2 * Denotes agencies with more than one office entry on the agency finder 0 10 20 30 40 North West LA Adoption Agencies Liverpool City Council 30 Cheshire West And Chester County Council 16 Bolton Metropolitan Borough Council 11 1 Manchester City Council 9 WWISH 9 Lancashire County Council 8 Oldham Council 8 1 Sefton Metropolitan Borough Council 8 2 Web Referrals Phone Referrals Wirral Adoption Team 8 Salford City Council 7 3 Bury Metropolitan -

Public Notices Public Notices: All You Need To

10 The Express, March 12, 2021 Public notices Public notices: all you need to Each week, the Express publishes public notices containing important All areas: From road closures to planning applications information affecting the community you live in. These statutory By David Lee place it with 61 apart- cost across the borough, notices help keep the wider public informed about key issues, from d av i d l @ b a y l i s m e d i a . co . u k m e n t s. including the precepts is- @ D av i d Le e _ B M plans to develop a block of flats in your neighbourhood to an Applicant Slough Propin- sued by the Police and application by your local bar or pub to serve alcohol for longer. You vest Ltd is seeking to re- Crime Commissioner for can find out about traffic orders and road closures affecting your This week’s public notices include develop Automotive House, the Thames Valley, Royal a planning application for 61 in Grays Place, into a resid- Berkshire Fire and Rescue travel plans, and keep up to date with the latest changes proposed by apartments near Slough Railway ential block with basement Authority, and, where rel- your local council. As part of the local newspaper industry’s Station and notice of an increase car parking and cycle evant, parish councils. commitment to highlighting the important role of public notices, we in council tax in Slough for the s t o r ag e. Annual council tax for have launched a new feature in print and online which will make it next financial year. -

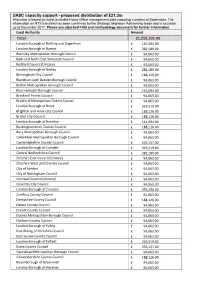

UASC Capacity Support - Proposed Distribution of £21.3M Allocation Is Based on Latest Available Home Office Management Data Capturing Numbers at September

UASC capacity support - proposed distribution of £21.3m Allocation is based on latest available Home Office management data capturing numbers at September. The information on NTS transfers has been confirmed by the Strategic Migration Partnership leads and is accurate up to December 2017. Please see attached FAQ and methodology document for further information. Local Authority Amount Total 21,258,203.00 London Borough of Barking and Dagenham £ 141,094.00 London Borough of Barnet £ 282,189.00 Barnsley Metropolitan Borough Council £ 94,063.00 Bath and North East Somerset Council £ 94,063.00 Bedford Council (Unitary) £ 94,063.00 London Borough of Bexley £ 282,189.00 Birmingham City Council £ 188,126.00 Blackburn with Darwen Borough Council £ 94,063.00 Bolton Metropolitan Borough Council £ 94,063.00 Bournemouth Borough Council £ 141,094.00 Bracknell Forest Council £ 94,063.00 Bradford Metropolitan District Council £ 94,063.00 London Borough of Brent £ 329,219.00 Brighton and Hove City Council £ 188,126.00 Bristol City Council £ 188,126.00 London Borough of Bromley £ 141,094.00 Buckinghamshire County Council £ 188,126.00 Bury Metropolitan Borough Council £ 94,063.00 Calderdale Metropolitan Borough Council £ 94,063.00 Cambridgeshire County Council £ 235,157.00 London Borough of Camden £ 329,219.00 Central Bedfordshire Council £ 282,189.00 Cheshire East Council (Unitary) £ 94,063.00 Cheshire West and Chester Council £ 94,063.00 City of London £ 94,063.00 City of Nottingham Council £ 94,063.00 Cornwall Council (Unitary) £ 94,063.00 Coventry City -

Slough-Borough-Council-Proposed

Slough Borough Council’s Please see attached Consultation for Slough Borough Council’s Proposed Admission Arrangements for Community Schools for 2021-2022. The consultation can be also be found at http://www.slough.gov.uk/schools-and-learning/school- admissions.aspx. Please email any comments to [email protected] and [email protected]. The consultation will close on Friday 31st January 2020. SLOUGH COMMUNITY SCHOOLS PROPOSED ADMISSION ARRANGEMENTS FOR 2021 -2022 Contents 1. Published Admission numbers for Slough Community Primary and Secondary Schools for 2021- 2022. (Appendix A) 2. Proposed admission arrangements for Slough Borough Council’s Community Primary Schools for 2021-2022. (Appendix B) 3. Proposed admission arrangements for Wexham School for 2021-2022. (Appendix C) 4. Proposed admission arrangements for In-Year entry to Slough Borough Council’s Community Schools for 2021-2022. (Appendix D) 5. Guidance for Admission Arrangements for Reception transfer and Year 7 for 2021-2022. (Appendix E) 6. Slough Scheme for Co-ordination of Admissions for 2021-2022 (Appendix F) 1 Appendix A Published Admission Numbers (PAN) for Slough Borough Council’s Community Primary and Secondary Schools for 2021 -2022 This document sets out the published admission numbers (PAN) for Slough community primary schools for September 2021. SCHOOL PAN 2021 Claycots Primary (Britwell) 120 Claycots Primary (Town Hall) 120 Penn Wood Primary 90 St Mary’s CE Primary ( Sabi this is a Vol Controlled school) 90 Wexham Court Primary 90 Published Admission Number (PAN) for Slough Borough Council’s Community Secondary Schools for 2021-2022 This document sets out the published admission number (PAN) for the Slough community secondary school for September 2021. -

Electric Chargepoint Analysis 2017: Local Authority Rapids

Statistical Release 13 December 2018 Electric Chargepoint Analysis 2017: Local Authority Rapids About this release This publication has been revised for the following reasons: This statistical release • The original release omitted data from Cornwall Council, approximately 2,500 presents experimental charging events. This has now been added to the underlying data and analysis statistics on local authority presented in this release. rapid plug-in vehicle • Some of the chargepoints reported to DfT as rapids were actually fast chargers. chargepoints in England in Charging events from fast chargers have been removed and added to our separate 2017. Data from the 27 local publication on Public Sector Fasts. This removed approximately 25,000 events from authorities that received the dataset and resulted in slightly higher average energy supplied per event and grants from the Local shorter average durations. Most of the figures in the release have been revised. Authority Grant Fund (LAGF) was provided as a condition • Further analysis has revealed that several local authorities received funding for of the grants. Complete data chargepoints outside their geographical boundaries, for example via joint bids. is only available for 2017. Therefore the local authority name does not indicate where the chargepoint is located. Consequently this report Less than half of the chargepoints had an identifiable location, so geographical focuses on that year alone. analysis is not possible and the local authority map has been removed. The Local Authority Grant Fund was set up in 2013 by the Office for Low Emission Vehicles (OLEV) to deliver recharging infrastructure in the UK. This analysis has been produced to help support and inform Key findings: the strategy for ultra low emission vehicles in the • Energy supplied The median average energy supplied by rapid UK.