Q4 2020: the Slow Path Back to Recovery

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

In Focusthe Barcelona Centre for International Affairs Brief

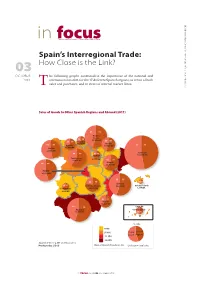

CIDOB • Barcelona Centre for International 2012 for September Affairs. Centre CIDOB • Barcelona in focusThe Barcelona Centre for International Affairs Brief Spain’s Interregional Trade: 03 How Close is the Link? OCTOBER he following graphs contextualise the importance of the national and 2012 international market for the 17 dif ferent Spanish regions, in terms of both T sales and purchases, and in terms of internal market flows. Sales of Goods to Other Spanish Regions and Abroad (2011) 46 54 Basque County 36 64 45,768 M€ 33 67 Cantabria 45 55 7,231 M€ Navarre 54 46 Asturias 17,856 M€ 53 47 Galicia 11,058 M€ 32,386 M€ 40 60 31 69 Catalonia La Rioja 104,914 M€ Castile-Leon 4,777 M€ 30,846 M€ 39 61 Aragon 54 46 23,795 M€ Madrid 45,132 M€ 45 55 22 78 5050 Valencia 29 71 Castile-La Mancha 44,405 M€ Balearic Islands Extremaura 18,692 M€ 1,694 M€ 4,896 M€ 39 61 Murcia 14,541 M€ 44 56 4,890 M€ Andalusia Canary Islands 52,199 M€ 49 51 % Sales 0-4% 5-10% To the Spanish World Regions 11-15% 16-20% Source: C-Intereg, INE and Datacomex Produced by: CIDOB Share of Spanish Population (%) Circle Size = Total Sales in focus CIDOB 03 . OCTOBER 2012 CIDOB • Barcelona Centre for International 2012 for September Affairs. Centre CIDOB • Barcelona Purchase of Goods From Other Spanish Regions and Abroad (2011) Basque County 28 72 36 64 35,107 M€ 35 65 Asturias Cantabria Navarre 11,580 M€ 55 45 6,918 M€ 14,914 M€ 73 27 Galicia 29 71 25,429 M€ 17 83 Catalonia Castile-Leon La Rioja 97,555 M€ 34,955 M€ 29 71 6,498 M€ Aragon 67 33 26,238 M€ Madrid 79,749 M€ 44 56 2 78 Castile-La Mancha Valencia 19 81 12 88 23,540 M€ Extremaura 49 51 45,891 M€ Balearic Islands 8,132 M€ 8,086 M€ 54 46 Murcia 18,952 M€ 56 44 Andalusia 52,482 M€ Canary Islands 35 65 13,474 M€ Purchases from 27,000 to 31,000 € 23,000 to 27,000 € Rest of Spain 19,000 to 23,000 € the world 15,000 to 19,000 € GDP per capita Circle Size = Total Purchase Source: C-Intereg, Expansión and Datacomex Produced by: CIDOB 2 in focus CIDOB 03 . -

Practical Guide of Zaragoza for Immigrants

INDEX INTRODUCTION 5 DISCOVER YOUR COMMUNITY: ARAGON 6 LOCATION 6 A BRIEF HISTORY OF ARAGON 7 MULTICULTURAL ARAGON 7 DISCOVER YOUR CITY: ZARAGOZA 8 LOCATION 8 A BRIEF HISTORY OF ZARAGOZA 8 MULTICULTURAL ZARAGOZA 10 PRINCIPAL MUNICIPAL BODIES 10 TOURIST INFORMATION AND MAPS 11 BASIC INFORMATION ABOUT THE CITY 11 Where to call in case of emergency 11 – Moving around the city 11 – Principal authorities 13 – City council at home 13 – Websites of interest about Zaragoza 13 BASIC RESOURCES FOR NEW RESIDENTS 14 INFORMATION AND FOREIGN RELATED PROCEDURES 14 CONSULATES IN ZARAGOZA 15 LEGAL ADVICE 16 REGISTRATION AT THE CITY COUNCIL 16 ¿HOW TO GET THE SANITARY CARD? 19 FOOD SERVICE 19 HYGIENE SERVICE 20 WARDROBE SERVICE 20 TRANSLATION, INTERPRETATION AND MEDIATION SERVICES 20 DRIVING LICENCE 21 SENDING LETTERS AND / OR MONEY 21 MICROCREDITS 21 HOUSING 22 ADVISING 22 PROTECTED HOUSING 22 STOCK HOUSING 23 HOUSING PROJECTS FOR IMMIGRANTS 23 FREE ACCOMMODATION 24 TRANSPORT 25 THE CAR 25 REGULAR BUS LINES 25 THE TRAIN 26 THE AEROPLANE 26 2 PRACTICAL GUIDE OF ZARAGOZA FOR IMMIGRANTS Information Resources point HEALTH 27 GENERAL INFORMATION 27 ASSISTANCE TO ILLEGAL PEOPLE 28 HEALTH CENTRES 28 PUBLIC HOSPITALS 30 CLINICS AND PRIVATE HOSPITALS 30 MEDICAL CENTRES OF SPECIALITIES 31 DRUG DEPENDENCY 32 AIDS 33 EMOTIONAL HEALTH 33 SOCIAL CARE 34 MUNICIPAL CENTRES OF SOCIAL SERVICES (CMSS) 34 WOMEN 34 Emergency cases 34 – Interesting organizations for women 35 FAMILY 36 YOUNG PEOPLE 37 Youth Houses 37 – Other resources for young people 37 DISABLED PEOPLE 38 OTHER -

The Beginning of the Neolithic in Andalusia

Quaternary International xxx (2017) 1e21 Contents lists available at ScienceDirect Quaternary International journal homepage: www.elsevier.com/locate/quaint The beginning of the Neolithic in Andalusia * Dimas Martín-Socas a, , María Dolores Camalich Massieu a, Jose Luis Caro Herrero b, F. Javier Rodríguez-Santos c a U.D.I. de Prehistoria, Arqueología e Historia Antigua (Dpto. Geografía e Historia), Universidad de La Laguna, Campus Guajara, 38071 Tenerife, Spain b Dpto. Lenguajes y Ciencias de la Computacion, Universidad de Malaga, Complejo Tecnologico, Campus de Teatinos, 29071 Malaga, Spain c Instituto Internacional de Investigaciones Prehistoricas de Cantabria (IIIPC), Universidad de Cantabria. Edificio Interfacultativo, Avda. Los Castros, 52. 39005 Santander, Spain article info abstract Article history: The Early Neolithic in Andalusia shows great complexity in the implantation of the new socioeconomic Received 31 January 2017 structures. Both the wide geophysical diversity of this territory and the nature of the empirical evidence Received in revised form available hinder providing a general overview of when and how the Mesolithic substrate populations 6 June 2017 influenced this process of transformation, and exactly what role they played. The absolute datings Accepted 22 June 2017 available and the studies on the archaeological materials are evaluated, so as to understand the diversity Available online xxx of the different zones undergoing the neolithisation process on a regional scale. The results indicate that its development, initiated in the middle of the 6th millennium BC and consolidated between 5500 and Keywords: Iberian Peninsula 4700 cal. BC, is parallel and related to the same changes documented in North Africa and the different Andalusia areas of the Central-Western Mediterranean. -

Cantabria Y Asturias Seniors 2016·17

Cantabria y Asturias Seniors 2016·17 7 días / 6 noches Hotel Zabala 3* (Santillana del Mar) € Hotel Norte 3* (Gijón) desde 399 Salida: 11 de junio Precio por persona en habitación doble Suplemento Hab. individual: 150€ ¡TODO INCLUIDO! 13 comidas + agua/vino + excursiones + entradas + guías ¿Por qué reservar este viaje? ¿Quiere conocer Cantabria y Asturias? En nuestro circuito Reserve por sólo combinamos lo mejor de estas dos comunidades para que durante 7 días / 6 noches conozcas a fondo los mejores rincones de la geografía. 50 € Itinerario: Incluimos: DÍA 1º. BARCELONA – CANTABRIA • Asistencia por personal de Viajes Tejedor en el punto de salida. Salida desde Barcelona. Breves paradas en ruta (almuerzo en restaurante incluido). • Autocar y guía desde Barcelona y durante todo el recorrido. Llegada al hotel en Cantabria. Cena y alojamiento. • 3 noches de alojamiento en el hotel Zabala 3* de Santillana del Mar y 2 noches en el hotel Norte 3* de Gijón. DÍA 2º. VISITA DE SANTILLANA DEL MAR y COMILLAS – VISITA DE • 13 comidas con agua/vino incluido, según itinerario. SANTANDER • Almuerzos en ruta a la ida y regreso. Desayuno. Seguidamente nos dirigiremos a la localidad de Santilla del Mar. Histórica • Visitas a: Santillana del Mar, Comillas, Santander, Santoña, Picos de Europa, Potes, población de gran belleza, donde destaca la Colegiata románica del S.XII, declarada Oviedo, Villaviciosa, Lastres, Tazones, Avilés, Luarca y Cudillero. Monumento Nacional. Las calles empedradas y las casas blasonadas, configuran un paisaje • Pasaje de barco de Santander a Somo. urbano de extraordinaria belleza. Continuaremos viaje a la cercana localidad de Comillas, • Guías locales en: Santander, Oviedo y Avilés. -

Commission V Italian Republic

C 256/16 EN Official Journal of the European Union 24.10.2009 Forms of order sought 273/2004 ( 1), by failing to communicate those measures pursuant to Article 16 of that Regulation and by failing — Declare that the Kingdom of Spain has failed to fulfil its to adopt the national measures necessary to implement obligations under Article 4(2), (3), (4) and (5) of Council Articles 26(3) and 31 of Regulation (EC) No 111/2005 ( 2 ), Directive 1999/22/EC of 29 March 1999 relating to the Ireland has failed to fulfil its obligations under Regulation 1 keeping of wild animals in zoos, ( ) in respect of certain (EC) No 273/2004 on drug precursors and Regulation (EC) zoos in the Autonomous Communities of Aragon, No 111/2005 laying down the rules for the monitoring of Asturias, the Balearic Islands, the Canary Islands, Cantabria, trade between the Community and third countries in drug Castile and Leon, Valencia, Extremadura and Galicia: precursors; — by failing to ensure that, by the date laid down in the Directive, all the zoos in its territory were licensed in accordance with paragraphs 2, 3 and, in the cases of — order Ireland to pay the costs. Aragon, Asturias, the Canary Islands, Cantabria and Castile and Leon, 4 of Article 4 of the Directive; and — by failing to order the closure of zoos, in accordance with Article 4(5) of the Directive, where they were not Pleas in law and main arguments licensed; Member States are required to adopt the measures necessary to comply with the provisions of Regulations, within the time — order the Kingdom of Spain to pay the costs. -

To the West of Spanish Cantabria. the Palaeolithic Settlement of Galicia

To the West of Spanish Cantabria. The Palaeolithic Settlement of Galicia Arturo de Lombera Hermida and Ramón Fábregas Valcarce (eds.) Oxford: Archaeopress, 2011, 143 pp. (paperback), £29.00. ISBN-13: 97891407308609. Reviewed by JOÃO CASCALHEIRA DNAP—Núcleo de Arqueologia e Paleoecologia, Faculdade de Ciências Humanas e Sociais, Universidade do Algarve, Campus Gambelas, 8005- 138 Faro, PORTUGAL; [email protected] ompared with the rest of the Iberian Peninsula, Galicia investigation, stressing the important role of investigators C(NW Iberia) has always been one of the most indigent such as H. Obermaier and K. Butzer, and ending with a regions regarding Paleolithic research, contrasting pro- brief presentation of the projects that are currently taking nouncedly with the neighboring Cantabrian rim where a place, their goals, and auspiciousness. high number of very relevant Paleolithic key sequences are Chapter 2 is a contribution of Pérez Alberti that, from known and have been excavated for some time. a geomorphological perspective, presents a very broad Up- This discrepancy has been explained, over time, by the per Pleistocene paleoenvironmental evolution of Galicia. unfavorable geological conditions (e.g., highly acidic soils, The first half of the paper is constructed almost like a meth- little extension of karstic formations) of the Galician ter- odological textbook that through the definition of several ritory for the preservation of Paleolithic sites, and by the concepts and their applicability to the Galician landscape late institutionalization of the archaeological studies in supports the interpretations outlined for the regional inter- the region, resulting in an unsystematic research history. land and coastal sedimentary sequences. As a conclusion, This scenario seems, however, to have been dramatically at least three stadial phases were identified in the deposits, changed in the course of the last decade. -

Ferdinand of Aragon

Contents Lorenzo the Magnifi cent ....................................................................................................... 5 Christopher Columbus .......................................................................................................... 9 Ferdinand of Aragon ............................................................................................................ 17 Vasco da Gama ..................................................................................................................... 21 Chevalier Bayard .................................................................................................................. 27 Cardinal Wolsey ................................................................................................................... 31 Charles V of Germany ......................................................................................................... 35 Suleiman the Magnifi cent ................................................................................................... 41 Sir Francis Drake .................................................................................................................. 45 Sir Walter Raleigh ................................................................................................................. 51 Henry of Navarre ................................................................................................................. 57 Wallenstein ........................................................................................................................... -

Chapter 24. the BAY of BISCAY: the ENCOUNTERING of the OCEAN and the SHELF (18B,E)

Chapter 24. THE BAY OF BISCAY: THE ENCOUNTERING OF THE OCEAN AND THE SHELF (18b,E) ALICIA LAVIN, LUIS VALDES, FRANCISCO SANCHEZ, PABLO ABAUNZA Instituto Español de Oceanografía (IEO) ANDRE FOREST, JEAN BOUCHER, PASCAL LAZURE, ANNE-MARIE JEGOU Institut Français de Recherche pour l’Exploitation de la MER (IFREMER) Contents 1. Introduction 2. Geography of the Bay of Biscay 3. Hydrography 4. Biology of the Pelagic Ecosystem 5. Biology of Fishes and Main Fisheries 6. Changes and risks to the Bay of Biscay Marine Ecosystem 7. Concluding remarks Bibliography 1. Introduction The Bay of Biscay is an arm of the Atlantic Ocean, indenting the coast of W Europe from NW France (Offshore of Brittany) to NW Spain (Galicia). Tradition- ally the southern limit is considered to be Cape Ortegal in NW Spain, but in this contribution we follow the criterion of other authors (i.e. Sánchez and Olaso, 2004) that extends the southern limit up to Cape Finisterre, at 43∞ N latitude, in order to get a more consistent analysis of oceanographic, geomorphological and biological characteristics observed in the bay. The Bay of Biscay forms a fairly regular curve, broken on the French coast by the estuaries of the rivers (i.e. Loire and Gironde). The southeastern shore is straight and sandy whereas the Spanish coast is rugged and its northwest part is characterized by many large V-shaped coastal inlets (rias) (Evans and Prego, 2003). The area has been identified as a unit since Roman times, when it was called Sinus Aquitanicus, Sinus Cantabricus or Cantaber Oceanus. The coast has been inhabited since prehistoric times and nowadays the region supports an important population (Valdés and Lavín, 2002) with various noteworthy commercial and fishing ports (i.e. -

Aragon and Catalunya, Spain Steve M R Young 28/3-1/4 2003 in March

Aragon and Catalunya, Spain Steve M R Young 28/3-1/4 2003 In March 1999 Ian Reid conducted a reconnaissance birding trip in Extremadura at the end of an academic visit to Madrid. In May he and I then followed up with a blinding four day clean- up operation that produced a key trip report and the bench-mark itinerary for a short May visit. Clearly hooked on Spain, Ian conducted another reccy in November 2002. This time he’d gone to the pre-Pyrenees region of Aragon in NE Spain after Lammergeier, Wallcreeper and Black Woodpecker. With the assistance of local guide Josele Saiz he’d succeeded with the first two, gripping me off with Lammergeier which I’d always believed was very hard in the Pyrenees. While Wallcreepers were still at low altitude wintering sites, March seemed a good time to follow up, just five months after my last birding in Spain. Ian and I planned another 3-4 day weekend based at Josele’s B&B in the province of Huesca on the southern edge of the Sierra de Guara, part of the pre-Pyrenees mountains. In addition to the impressive Black Woodpecker and the rare and fantastically charismatic Lammergeier other potential lifers for me were Rock Thrush and Lesser Short-toed Lark; the latter in the plains to the south. My one superb Wallcreeper in Switzerland (see 19/6/90) was well overdue for an update, especially if I could use the Coolpix and Televid successfully. Catalonia March 28th Ian met me at airport arrivals having already collected the Ford Focus and found his way to and from the first birding site just beyond the airport perimeter. -

Working Papers in Economic History the Roots of Land Inequality in Spain

The roots of land inequality in Spain Francisco J. Beltrán Tapia, Alfonso Díez-Minguela, Julio Martinez-Galarraga, Daniel A. Tirado-Fabregat (Universitat de València) Working Papers in Economic History 2021-01 ISSN: 2341-2542 Serie disponible en http://hdl.handle.net/10016/19600 Web: http://portal.uc3m.es/portal/page/portal/instituto_figuerola Correo electrónico: [email protected] Creative Commons Reconocimiento- NoComercial- SinObraDerivada 3.0 España (CC BY-NC-ND 3.0 ES) The roots of land inequality in Spain Francisco J. Beltrán Tapia (Norwegian University of Science and Technology, NTNU) Alfonso Díez-Minguela (Universitat de València) Julio Martinez-Galarraga (Universitat de València) Daniel A. Tirado-Fabregat (Universitat de València) Abstract There is a high degree of inequality in land access across Spain. In the South, and in contrast to other areas of the Iberian Peninsula, economic and political power there has traditionally been highly concentrated in the hands of large landowners. Indeed, an unequal land ownership structure has been linked to social conflict, the presence of revolutionary ideas and a desire for agrarian reform. But what are the origins of such inequality? In this paper we quantitatively examine whether geography and/or history can explain the regional differences in land access in Spain. While marked regional differences in climate, topography and location would have determined farm size, the timing of the Reconquest, the expansion of the Christian kingdoms across the Iberian Peninsula between the 9th and the 15th centuries at the expense of the Moors, influenced the type of institutions that were set up in each region and, in turn, the way land was appropriated and distributed among the Christian settlers. -

33 the Radiocarbon Chronology of El Mirón Cave

RADIOCARBON, Vol 52, Nr 1, 2010, p 33–39 © 2010 by the Arizona Board of Regents on behalf of the University of Arizona THE RADIOCARBON CHRONOLOGY OF EL MIRÓN CAVE (CANTABRIA, SPAIN): NEW DATES FOR THE INITIAL MAGDALENIAN OCCUPATIONS Lawrence Guy Straus1,2 • Manuel R González Morales2 ABSTRACT. Three additional radiocarbon assays were run on samples from 3 levels lying below the classic (±15,500 BP) Lower Cantabrian Magdalenian horizon in the outer vestibule excavation area of El Mirón Cave in the Cantabrian Cordillera of northern Spain. Although the central tendencies of the new dates are out of stratigraphic order, they are consonant with the post-Solutrean, Initial Magdalenian period both in El Mirón and in the Cantabrian region, indicating a technological transition in preferred weaponry from foliate and shouldered points to microliths and antler sagaies between about 17,000–16,000 BP (uncalibrated), during the early part of the Oldest Dryas pollen zone. Now with 65 14C dates, El Mirón is one of the most thor- oughly dated prehistoric sites in western Europe. The until-now poorly dated, but very distinctive Initial Cantabrian Magdale- nian lithic artifact assemblages are briefly summarized. INTRODUCTION El Mirón Cave is located in the upper valley of the Asón River in eastern Cantabria Province in northern Spain, about 100 m up from the valley floor on the steep western face of a mountain in the second foothill range of the Cantabrian Cordillera, about halfway between the cities of Santander and Bilbao. The site location in the town of Ramales de la Victoria (431448N, 3275W) is 260 m above present sea level, and about 20 km from the present shore of the Bay of Biscay (and about 25–30 km from the Tardiglacial shore). -

An Overview of Rice Cultivation in Spain and the Management of Herbicide-Resistant Weeds

agronomy Review An Overview of Rice Cultivation in Spain and the Management of Herbicide-Resistant Weeds Diego Gómez de Barreda 1, Gabriel Pardo 2, José María Osca 1 , Mar Catala-Forner 3 , Silvia Consola 4, Irache Garnica 5, Nuria López-Martínez 6, José Antonio Palmerín 7 and Maria Dolores Osuna 8,* 1 Plant Protection Department, Universitat Politècnica de València, Camino de Vera s/n, 46022 Valencia, Spain; [email protected] (D.G.d.B.); [email protected] (J.M.O.) 2 Plant Protection Department, Agrifood Research and Technology Centre of Aragon (CITA), AgriFood Institute of Aragon—IA2 (CITA-University of Zaragoza), Avenida Montañana 930, 50059 Zaragoza, Spain; [email protected] 3 Institute of Agrifood Research and Technology (IRTA), Estació Experimental de l’Ebre, Ctra. de Balada, km 1, 43870 Amposta, Spain; [email protected] 4 Plant Health Service (DARP), Generalitat de Catalunya, Ctra. de Valencia, 108, 43520 Roquetes, Spain; [email protected] 5 Institute for Agrifood Technology and Infrastructures of Navarra (INTIA), Edificio Peritos, Avda. Serapio Huici 22, Navarre, 31610 Villava, Spain; [email protected] 6 Agronomy Department, High Technical School of Agronomic Engineering (ETSIA), University of Sevilla, Ctra. de Utrera, 41013 Sevilla, Spain; [email protected] 7 Plant Health Service, Government of Extremadura, Ctra. de Miajadas, km 2,5, Don Benito, 06400 Badajoz, Spain; [email protected] 8 Plant Protection Department, Extremadura Scientific and Technological Research Center (CICYTEX), Ctra. de Citation: Gómez de Barreda, D.; AV, km 372, Badajoz, 06187 Guadajira, Spain Pardo, G.; Osca, J.M.; * Correspondence: [email protected] Catala-Forner, M.; Consola, S.; Garnica, I.; López-Martínez, N.; Abstract: Spain is the second highest rice-producing country in the European Union, with approxi- Palmerín, J.A.; Osuna, M.D.