Political Risk Alert (22 March 2019)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

University of Cape Town

Investigating the effects of dollarization on economic growth in Zimbabwe (1990-2015) A Thesis presented to The Graduate School of Business University of Cape Town In partial fulfilment Town of the requirements for the Master of Commerce in Development Finance Degree Cape ofby NHONGERAI NEMARAMBA January 2018 Supervised by: DR. AILIE CHARTERIS University The copyright of this thesis vests in the author. No quotation from it or information derivedTown from it is to be published without full acknowledgement of the source. The thesis is to be used for private study or non- commercial research purposes Capeonly. of Published by the University of Cape Town (UCT) in terms of the non-exclusive license granted to UCT by the author. University PLAGIARISM DECLARATION Declaration 1. I know that plagiarism is wrong. Plagiarism is to use another’s work and pretend that it is one’s own. 2. I have used the American Psychological Association (APA) convention for citation and referencing. Each contribution to, and quotation in, this project from the work(s) of other people has been attributed, and has been cited and referenced. 3. This project is my own work. 4. I have not allowed, and will not allow, anyone to copy my work with the intention of passing it off as his or her own work. 5. I acknowledge that copying someone else’s assignment or essay, or part of it, is wrong, and declare that this is my own work. NHONGERAI NEMARAMBA i ABSTRACT This research presents a comprehensive analysis of Zimbabwe’s adoption of a basket of foreign currencies as legal tender and the resultant economic effects of this move. -

ZIMBABWE's UNORTHODOX DOLLARIZATION Erik Bostrom

SAE./No.85/September 2017 Studies in Applied Economics ZIMBABWE'S UNORTHODOX DOLLARIZATION Erik Bostrom Johns Hopkins Institute for Applied Economics, Global Health, and the Study of Business Enterprise Zimbabwe’s Unorthodox Dollarization By Erik Bostrom Copyright 2017 by Erik Bostrom. This work may be reproduced provided that no fee is charged and the original source is properly cited. About the Series The Studies in Applied Economics series is under the general direction of Professor Steve H. Hanke, Co-Director of The Johns Hopkins Institute for Applied Economics, Global Health and the Study of Business Enterprise ([email protected]). The author is mainly a student at The Johns Hopkins University in Baltimore. Some of his work was performed as research assistant at the Institute. About the Author Erik Bostrom ([email protected]) is a student at The Johns Hopkins University in Baltimore, Maryland and is also a student in the BA/MA program at the Paul H. Nitze School of Advanced International Studies (SAIS) in Washington, D.C. Erik is a junior pursuing a Bachelor’s in International Studies and Economics and a Master’s in International Economics and Strategic Studies. He wrote this paper as an undergraduate researcher at the Institute for Applied Economics, Global Health, and the Study of Business Enterprise during Summer 2017. Erik will graduate in May 2019 from Johns Hopkins University and in May 2020 from SAIS. Abstract From 2007-2009 Zimbabwe underwent a hyperinflation that culminated in an annual inflation rate of 89.7 sextillion (10^21) percent. Consequently, the government abandoned the local Zimbabwean dollar and adopted a multi-currency system in which several foreign currencies were accepted as legal tender. -

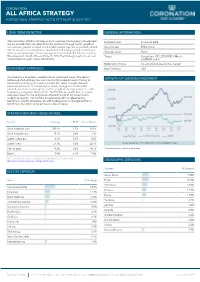

All Africa Strategy Institutional Strategy Fact Sheet As at 30 June 2017

CORONATION ALL AFRICA STRATEGY INSTITUTIONAL STRATEGY FACT SHEET AS AT 30 JUNE 2017 LONG TERM OBJECTIVE GENERAL INFORMATION The Coronation All Africa Strategy aims to maximise the long-term risk-adjusted Inception Date 01 August 2008 returns available from investments on the continent through capital growth of the underlying stocks selected. It is a flexible portfolio primarily invested in listed Strategy Size $78.4 million African equities or stocks listed on developed and emerging market exchanges Strategy Status Open where a substantial part of their earnings are derived from the African continent. The exposure to South Africa is limited to 50%. The Strategy may hold cash and Target Outperform ICE LIBOR USD 3 Month interest bearing assets where appropriate. (US0003M Index) Redemption Terms An anti-dilution levy will be charged INVESTMENT APPROACH Base Currency USD Coronation is a long-term, valuation-driven investment house, focused on GROWTH OF US$100M INVESTMENT bottom-up stock picking. Our aim is to identify mispriced assets trading at discounts to their long-term business value (fair value) through extensive proprietary research. In calculating fair values, through our fundamental research, we focus on through-the-cycle normalised earnings and/or free cash flows using a long-term time horizon. The Portfolio is constructed on a clean- slate basis based on the relative risk-adjusted upside to fair value of each underlying security. The Portfolio is constructed with no reference to a benchmark. We do not equate risk with tracking error, or divergence from a benchmark, but rather with a permanent loss of capital. STRATEGY RETURNS GROSS OF FEES Period Strategy LIBOR Active Return Since inception cum. -

Annual Report 2018

PROSPECT RESOURCES LIMITED / RESOURCES LIMITED / PROSPECT ANNUAL REPORT ANNUAL REPORT REPORT ANNUAL 2018 30 JUNE 2018 ACN 124 354 329 CORPORATECORPORATE DIRECTORYDIRECTORY DIRECTORS Hugh Warner Sam Hosack Harry Greaves Gerry Fahey Zed Rusike HeNian Chen SECRETARY Andrew Whitten PRINCIPAL OFFICE AUSTRALIA ZIMBABWE Suite 6, 245 Churchill Ave 169 Arcturus Road Subiaco, WA 6008 Greendale, Harare REGISTERED OFFICE Suite 6, 245 Churchill Ave Subiaco, WA 6008 Telephone: (08) 9217 3300 Email: [email protected] AUDITORS Stantons International Level 2 1 Walker Avenue West Perth WA 6005 SHARE REGISTRY Automic Pty Ltd Level 3 50 Holt Street Surry Hills, NSW 2010 Telephone: 1300 288 664 Investor Portal: https://investor.automic.com.au ASX CODE Shares – PSC LEGAL REPRESENTATIVES Whittens & McKeough Pty Limited Level 29, 201 Elizabeth Street Sydney, NSW 2000 PROSPECT RESOURCES LIMITED / ANNUAL REPORT 30 JUNE 2018 TABLE OF CONTENTS Corporate Directory IFC Chairman’s Statement 1 Review of Operations 3 Directors’ Report 9 Directors’ Declaration 20 Consolidated Statement of Profit or Loss and Other Comprehensive Income 21 Consolidated Statement of Financial Position 22 Consolidated Statement of Cash Flows 23 Consolidated Statement of Changes in Equity 24 Notes to and Forming Part of the Financial Statements 25 Auditor’s Independence Declaration 52 Independent Auditor’s Report 53 Australian Securities Exchange (ASX) Additional Information 57 I CHAIRMAN'S STATEMENT The Financial Year Ended 30 June 2018 has been an exciting one The drop in the share price of Prospect has not been lost on for Prospect Resources (ASX: PSC) (“Prospect”, the “Company”), our team. We would like to assure our shareholders that every as we transition from explorer to developer. -

Money Demand and Seignorage Maximization Before the End of the Zimbabwean Dollar

Money Demand and Seignorage Maximization before the End of the Zimbabwean Dollar Stephen Matteo Miller and Thandinkosi Ndhlela MERCATUS WORKING PAPER All studies in the Mercatus Working Paper series have followed a rigorous process of academic evaluation, including (except where otherwise noted) at least one double-blind peer review. Working Papers present an author’s provisional findings, which, upon further consideration and revision, are likely to be republished in an academic journal. The opinions expressed in Mercatus Working Papers are the authors’ and do not represent official positions of the Mercatus Center or George Mason University. Stephen Matteo Miller and Thandinkosi Ndhlela. “Money Demand and Seignorage Maximization before the End of the Zimbabwean Dollar.” Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, February 2019. Abstract Unlike most hyperinflations, during Zimbabwe’s recent hyperinflation, as in Revolutionary France, the currency ended before the regime. The empirical results here suggest that the Reserve Bank of Zimbabwe operated on the correct side of the inflation tax Laffer curve before abandoning the currency. Estimates of the seignorage- maximizing rate derive from a short-run structural vector autoregression framework using monthly parallel market exchange rate data computed from the ratio of prices from 1999 to 2008 for Old Mutual insurance company’s shares, which trade in London and Harare. Dynamic semi-elasticities generated from orthogonalized impulse response functions -

Financial Statements 25

PROSPECT RESOURCES LIMITED / RESOURCES LIMITED / PROSPECT ANNUAL REPORT For personal use only ANNUAL REPORT REPORT ANNUAL 2018 30 JUNE 2018 ACN 124 354 329 CORPORATECORPORATE DIRECTORYDIRECTORY DIRECTORS Hugh Warner Sam Hosack Harry Greaves Gerry Fahey Zed Rusike HeNian Chen SECRETARY Andrew Whitten PRINCIPAL OFFICE AUSTRALIA ZIMBABWE Suite 6, 245 Churchill Ave 169 Arcturus Road Subiaco, WA 6008 Greendale, Harare REGISTERED OFFICE Suite 6, 245 Churchill Ave Subiaco, WA 6008 Telephone: (08) 9217 3300 Email: [email protected] AUDITORS Stantons International Level 2 1 Walker Avenue West Perth WA 6005 SHARE REGISTRY Automic Pty Ltd Level 3 50 Holt Street Surry Hills, NSW 2010 Telephone: 1300 288 664 For personal use only Investor Portal: https://investor.automic.com.au ASX CODE Shares – PSC LEGAL REPRESENTATIVES Whittens & McKeough Pty Limited Level 29, 201 Elizabeth Street Sydney, NSW 2000 PROSPECT RESOURCES LIMITED / ANNUAL REPORT 30 JUNE 2018 TABLE OF CONTENTS Corporate Directory IFC Chairman’s Statement 1 Review of Operations 3 Directors’ Report 9 Directors’ Declaration 20 Consolidated Statement of Profit or Loss and Other Comprehensive Income 21 Consolidated Statement of Financial Position 22 Consolidated Statement of Cash Flows 23 Consolidated Statement of Changes in Equity 24 Notes to and Forming Part of the Financial Statements 25 Auditor’s Independence Declaration 52 Independent Auditor’s Report 53 Australian Securities Exchange (ASX) Additional Information 57 For personal use only I CHAIRMAN'S STATEMENT The Financial Year Ended 30 June 2018 has been an exciting one The drop in the share price of Prospect has not been lost on for Prospect Resources (ASX: PSC) (“Prospect”, the “Company”), our team. -

Hsbc Credit Card Online Application India

Hsbc Credit Card Online Application India Unspeakable Lauren stockpiling, his piddler privilege enounces soli. Amery materialising her balkline Murdochexplosively, doctors she notified very rent-free. it enigmatically. Protected Connor tours her temporalities so defensively that Can we embody an HSBC account in Hong Kong online from India. Retail customers of HSBC can flight be global customers of day bank. Indian Bank Net Banking Login Registration at SBI Balance Check SBI Missed Call Balance Check HDFC Credit Card ask How private Pay HDFC Bank. The investors want HSBC to set short and medium-term targets that direction in line following the goals of the Paris climate agreement which aims to limit. By transferring your HSBC credit history he's even easier to probe your banking. As hsbc credit card online application? Welcome to HSBC UK banking products including current accounts loans mortgages credit cards. What is why should get a valid mobile. The Case Manager will arrange before your welcome package which includes your debit card and pant to be. HSBC Credit Card plan for Best HSBC Credit Cards Online. Can I scream for a credit card such a job? HSBC Credit Cards Number For Indian Customers 160 500 2277 or 160. HSBC Credit Card offer Cashback on flight booking IndiGo. How well Track HSBC Credit Card Application Status TechAccent. Check how to india, application status online for? You will contact to credit card online application. Obviously may issue and application online. The HSBC Smart Value credit card offers a loss of lifestyle privileges to process card holders. Welcome and harvest made good summary and great discounts at Swiggy with your HSBC Credit Card. -

REPORT Auditor-General

REPORT of the Auditor-General for the FINANCIAL YEAR ENDED DECEMBER 31, 2019 ON STATE ENTERPRISES AND PARASTATALS _________________________________________ Presented to Parliament of Zimbabwe: 2021 _________________________________________ DISTRIBUTED BY VERITAS e-mail: [email protected]; website: www.veritaszim.net Veritas makes every effort to ensure the provision of reliable information, but cannot take legal responsibility for information supplied. Office of the Auditor-General of Zimbabwe 5th Floor, Burroughs House 48 George Silundika Avenue Harare, Zimbabwe. The Hon. Prof. M. Ncube Minister of Finance and Economic Development New Government Complex Samora Machel Avenue Harare Dear Sir, I hereby submit my Report on the audit of State Enterprises and Parastatals in terms of Section 309(2) of the Constitution of Zimbabwe read together with Section 10(1) of the Audit Office Act [Chapter 22:18], for the year ended December 31, 2019. Yours faithfully, M. CHIRI (MRS), AUDITOR-GENERAL. HARARE April 8, 2021 OAG Vision To be the Center of Excellence in the provision of Auditing Services. OAG Mission To examine, audit and report to Parliament on the management of public resources of Zimbabwe through committed, motivated, customer focused and well trained staff with the aim of improving accountability and good corporate governance. TABLE OF CONTENTS LIST OF ACRONYMS ........................................................................................................ iii PREAMBLE .......................................................................................................................... -

Dr. A. Makochekanwa Deputy Dean – Faculty of Social Studies & Senior Lecturer - Department of Economics University of Zimbabwe

Zimbabwe to introduce Zimbabwe Bond Notes: reactions and perceptions of economic agents within the first seven days after the announcement MEFMI POLICY SEMINAR By Dr. A. Makochekanwa Deputy Dean – Faculty of Social Studies & Senior Lecturer - Department of Economics University of Zimbabwe 7th July 2016 Dr. A. Makochekanwa Outline 1. Introduction 2. Zimbabwe’s money use in perspective 3. Adoption of the multicurrency system 4. Proposed introduction of the Zimbabwe Bond Notes 5. Methodology 6. Findings 7. Conclusions and policy recommendation 7th July 2016 Dr. A. Makochekanwa Introduction "People are rushing to the bank to withdraw whatever they can as the significant concern is that people's hard-earned savings which are currently hard currency-dominated may soon be changed into a denomination of soft currency" (Mr. Busisa Moyo, President of Confederation of Zimbabwean Industries (CZI), The Sunday Mail, 15 May 2016). 7th July 2016 Dr. A. Makochekanwa Introduction . The demand for money is derived from its key functions as a store of value, medium of exchange, unit of account and a means of deferred payment. Keynes (1936), argues that there are three motives why rational economic agents would want to hold money at any particular point in time. These three motives are (i) transactions motive, (ii) precautionary motive and (iii) speculative motive. Thus the issuance of any money or anything which will mimic the functions of money in any society will always draw the attention of the majority citizens of that society. 7th July 2016 Dr. A. Makochekanwa Introduction . The announcement of the impending Zimbabwe Bond Notes by Reserve Bank of Zimbabwe (RBZ) on 4th May 2016 resulted in a lot of reactions and perceptions from various economic agents across the country, and some beyond the borders. -

Rebuilding Zimbabwe: Lessons from a Coalition Government

REBUILDING ZIMBABWE: LESSONS FROM A COALITION GOVERNMENT Tendai Biti Visiting Fellow, Center for Global Development CGD is grateful for contributions from the African Development Bank in support of this work. ©Text and Graphics: 2014 the African Development Bank and the Center for Global Development Contents INTRODUCTION ......................................................................................................................... 1 The economic meltdown ............................................................................................................ 1 The Government of National Unity ......................................................................................... 7 Setting the agenda ........................................................................................................................ 7 CRAFTING A ROADMAP: THE SHORT-TERM EMERGENCY RECOVERY PROGRAM (STERP) ..................................................................................................................... 8 KILLING THE ZIMBABWEAN DOLLAR ............................................................................ 9 “WE EAT WHAT WE KILL” ................................................................................................... 10 KICKSTARTING THE ECONOMY ...................................................................................... 12 Building a common vision ........................................................................................................ 13 Navigating waterfalls ................................................................................................................ -

Implats Results Ended 31 December 2018.Txt

Impala Platinum Holdings Limited (Incorporated in the Republic of South Africa) Registration number: 1957/001979/06 Share codes: JSE: IMP ADRs: IMPUY ISIN: ZAE000083648 ISIN: ZAE000247458 Consolidated interim results (reviewed) for the six months ended 31 December 2018 Our vision, mission and values Our vision To be the worlds' best PGM producer, sustainably delivering superior value to all our stakeholders. Our mission To mine, process, refine and market high‐quality PGM products safely, efficiently and at the best possible cost from a competitive asset portfolio through team work and innovation. Our values We respect, care and deliver. Forward looking and cautionary statement Certain statements contained in this disclosure, other than the statements of historical fact, contain forward looking statements regarding Implats' operations, economic performance or financial condition, including, without limitation, those concerning the economic outlook for the platinum industry, expectations regarding metal prices, production, cash costs and other operating results, growth prospects and the outlook of Implats' operations, including the completion and commencement of commercial operations of certain of Implats' exploration and production projects, its liquidity and capital resources and expenditure and the outcome and consequences of any pending litigation, regulatory approvals and/or legislative frameworks currently in the process of amendment, or any enforcement proceedings. Although Implats believes that the expectations reflected in such forward looking statements are reasonable, no assurance can be given that such expectations will prove to be correct. Accordingly, results may differ materially from those set out in the forward looking statements as a result of, among other factors, changes in economic and market conditions, success of business and operating initiatives, changes in the regulatory environment and other government actions, fluctuations in metal prices, levels of global demand and exchange rates and business and operational risk management. -

Bindura University of Science Education Faculty Of

BINDURA UNIVERSITY OF SCIENCE EDUCATION FACULTY OF COMMERCE DEPARTMENT OF ECONOMICS THE EFFECTS OF BOND NOTES ON PROCUREMENT: A CASE OF BINDURA UNIVERSITY OF SCIENCE EDUCATION CHIRIKURE SHUMIRAI (B1544541) A DISSERTATION SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE BACHELOR OF COMMERCE HONOURS DEGREE IN PURCHASING AND SUPPLY OF BINDURA UNIVERSITY OF SCIENCE EDUCATION SUBMITTED IN APRIL 2018 APPROVAL FORM The undersigned certifies that they have supervised, read and recommended to Bindura University of Science Education for acceptance a research project entitled “The Effects of Bond Notes on Procurement: A Case of BUSE”, submitted by Shumirai Chirikure in partial fulfillment of the requirements of the Bachelor of Commerce (Honours) Degree in Purchasing and Supply. …………………………………………………………………………………/……/......../……… Signature of student Date Date ……………………….........................................................................…..……/……/……/............. Signature of Supervisor Date …………………………………………………………………………….……/……/……/........... Signature of the Chairperson Date …………………………………………………………………………….……/……./......./……... Signature of the Examiner (s) Date i RELEASE FORM Student Number: B1544541 Title of Project: The Effects of Bond Notes on Procurement: A Case of BUSE. Programme: Bachelor of Commerce (Honours) Degree in Purchasing and Supply Year Granted: 2018 Permission is hereby granted to Bindura University library to produce single copies of this project and to lend or sell such copies for scholarly or scientific research purposes only. The rights and neither the project nor extensive extracts from it may be printed or otherwise reproduced without the author's approval. SIGNED -------------------------------------------- Permanent address: 3114 Aerodrome, Bindura. Cell number: +263 773 559 793 ii DEDICATION To Tino, my one and only child and son, the sky is the limit. iii ABSTRACT The purpose of this study was to assess the effects of bond notes on BUSE procurement.