Currency Redenomination in Developing Nations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Euro and Currency Unions October 2011 2 the Euro and Currency Unions | October 2011

GLOBAL LAW INTELLIGENCE UNIT The euro and currency unions October 2011 www.allenovery.com 2 The euro and currency unions | October 2011 Key map of jurisdictions © Allen & Overy LLP 2011 3 Contents Introduction 4 Map of world currencies 4 Currency unions 5 Break-up of currency unions 6 Break-up of federations 6 How could the eurozone break up? 6 Rights of withdrawal from the eurozone 7 Legal rights against a member withdrawing from the eurozone unilaterally 7 What would a currency law say? 8 Currency of debtors' obligations to creditors 8 Role of the lex monetae if the old currency (euro) is still in existence 9 Creditors' rights of action against debtors for currency depreciation 10 Why would a eurozone member want to leave? - the advantages 10 Why would a eurozone member want to leave? - the disadvantages 11 History of expulsions 12 What do you need for a currency union? 12 Bailing out bankrupt member states 13 European fire-power 14 Are new clauses needed to deal with a change of currency? 14 Related contractual terms 18 Neutering of protective clauses by currency law 18 Other impacts of a currency change 18 Reaction of markets 19 Conclusion 20 Contacts 21 www.allenovery.com 4 The euro and currency unions | October 2011 Allen & Overy Global Law Intelligence Unit The euro and currency unions October 2011 Introduction The views of the executive of the Intelligence Unit as to whether or not breakup of the eurozone currency union This paper reviews the role of the euro in the context of would be a bad idea will appear in the course of this paper. -

ASIFMA RMB Roadmap

RMB ROADMAP May 2014 CO AUTHORS ASIFMA is an independent, regional trade association with over 80 member firms comprising a diverse range of leading financial institutions fromboththebuyandsellsideincludingbanks,assetmanagers,lawfirms andmarketinfrastructureserviceproviders.Together,weharnesstheshared interests of the financial industry to promote the development of liquid, deep and broad capital markets in Asia. ASIFMA advocates stable, innovative and competitive Asian capital markets that are necessary to support the region’s economic growth. We drive consensus, advocate solutionsandeffectchangearoundkeyissuesthroughthecollectivestrength andclarityofoneindustryvoice.Ourmanyinitiativesincludeconsultations withregulatorsandexchanges,developmentofuniformindustrystandards, advocacyforenhancedmarketsthroughpolicypapers,andloweringthecost ofdoingbusinessintheregion.ThroughtheGFMAalliancewithSIFMAinthe US and AFME in Europe,ASIFMA also provides insights on global best practicesandstandardstobenefittheregion. ASIFMAwouldliketoextenditsgratitudetoallofthememberfirmsandassociationswho contributedtothedevelopmentofthisroadmap Table of Contents List of Charts .........................................................................................................................................................ii List of Break-Out Boxes ....................................................................................................................................... iii Introduction ........................................................................................................................................................ -

University of Cape Town

Investigating the effects of dollarization on economic growth in Zimbabwe (1990-2015) A Thesis presented to The Graduate School of Business University of Cape Town In partial fulfilment Town of the requirements for the Master of Commerce in Development Finance Degree Cape ofby NHONGERAI NEMARAMBA January 2018 Supervised by: DR. AILIE CHARTERIS University The copyright of this thesis vests in the author. No quotation from it or information derivedTown from it is to be published without full acknowledgement of the source. The thesis is to be used for private study or non- commercial research purposes Capeonly. of Published by the University of Cape Town (UCT) in terms of the non-exclusive license granted to UCT by the author. University PLAGIARISM DECLARATION Declaration 1. I know that plagiarism is wrong. Plagiarism is to use another’s work and pretend that it is one’s own. 2. I have used the American Psychological Association (APA) convention for citation and referencing. Each contribution to, and quotation in, this project from the work(s) of other people has been attributed, and has been cited and referenced. 3. This project is my own work. 4. I have not allowed, and will not allow, anyone to copy my work with the intention of passing it off as his or her own work. 5. I acknowledge that copying someone else’s assignment or essay, or part of it, is wrong, and declare that this is my own work. NHONGERAI NEMARAMBA i ABSTRACT This research presents a comprehensive analysis of Zimbabwe’s adoption of a basket of foreign currencies as legal tender and the resultant economic effects of this move. -

Redenomination of Naira: a Strategy for Inflationary Reduction

International Journal of Academic Research in Business and Social Sciences Vol. 1 1 , No. 2, 2021, E-ISSN: 2222-6990 © 2021 HRMARS Redenomination of Naira: A Strategy for Inflationary Reduction Osakwe Charity Ifunanya, Nduka, Afamefuna Joseph, Obi-nwosu Victoria Ogochukwu To Link this Article: http://dx.doi.org/10.6007/IJARBSS/v11-i2/8860 DOI:10.6007/IJARBSS/v11-i2/8860 Received: 02 January 2021, Revised: 29 January 2021, Accepted: 15 February 2021 Published Online: 25 February 2021 In-Text Citation: (Ifunanya et al., 2021) To Cite this Article: Ifunanya, O. C., Nduka, A. J., & Ogochukwu, O. V. (2021). Redenomination of Naira: A Strategy for Inflationary Reduction. International Journal of Academic Research in Business and Social Sciences, 11(2), 472–481. Copyright: © 2021 The Author(s) Published by Human Resource Management Academic Research Society (www.hrmars.com) This article is published under the Creative Commons Attribution (CC BY 4.0) license. Anyone may reproduce, distribute, translate and create derivative works of this article (for both commercial and non-commercial purposes), subject to full attribution to the original publication and authors. The full terms of this license may be seen at: http://creativecommons.org/licences/by/4.0/legalcode Vol. 11, No. 2, 2021, Pg. 472 - 481 http://hrmars.com/index.php/pages/detail/IJARBSS JOURNAL HOMEPAGE Full Terms & Conditions of access and use can be found at http://hrmars.com/index.php/pages/detail/publication-ethics 472 International Journal of Academic Research in Business and Social Sciences Vol. 1 1 , No. 2, 2021, E-ISSN: 2222-6990 © 2021 HRMARS Redenomination of Naira: A Strategy for Inflationary Reduction Osakwe Charity Ifunanya (PhD) Department of Banking and Finance, Nnamdi Azikiwe University, Anambra State, PMB 5025, Awka, Nigeria. -

Redenomination of Naira: a Critical Analysis of Its Problems and Prospects

EUROPEAN ACADEMIC RESEARCH Vol. VII, Issue 12/ March 2020 Impact Factor: 3.4546 (UIF) ISSN 2286-4822 DRJI Value: 5.9 (B+) www.euacademic.org Redenomination of Naira: A Critical Analysis of Its Problems and Prospects OSAKWE CHARITY IFUNANYA (Ph.D)1 Department of Banking and Finance Faculty of Management Sciences Nnamdi Azikiwe University, Awka, Nigeria Abstract The study examines the problems and prospects of redenominating the naira currency. The economic consequences of the devaluation of Naira currency in the eighties are still being felt in the low value of naira. To ascertain Nigerians view on redenominating the naira, a total number of 153 respondents were studied and the data extracted from them was analyzed with simple percentage method. The study found that redenomination of naira will lead to the economic recovery of Nigeria and that redenomination can increase the prices of Nigeria export. The study recommends that for the redenomination exercise to be successful, it should be complemented with strict and disciplined fiscal policy so as to strengthen the economy and sustain the value of the redenominated currency and that the redenomination exercise should be timed in such a way that it will not create uncertainty and instability that will make investors to be risk averse. Key words: Redenomination, Prospects, Currency, Decimalization, and evaluation. 1 The author Osakwe Charity Ifunanya is a Financial Management Lecturer in Banking and Finance Department of Nnamdi Azikiwe University, Awka, Nigeria. Her research interests cover diverse areas of Investment Banking and finance. Her recent publications include: stock market capitalization and economic growth of Nigeria and South Africa (2000-2018), Credit Risk Management and Efficiency in the Banking Industry of an Emerging Economy in Africa: Evidence from Nigeria and stock market development and economic growth in Nigeria: A camaraderie Reconnaissance amongst others. -

ZIMBABWE's UNORTHODOX DOLLARIZATION Erik Bostrom

SAE./No.85/September 2017 Studies in Applied Economics ZIMBABWE'S UNORTHODOX DOLLARIZATION Erik Bostrom Johns Hopkins Institute for Applied Economics, Global Health, and the Study of Business Enterprise Zimbabwe’s Unorthodox Dollarization By Erik Bostrom Copyright 2017 by Erik Bostrom. This work may be reproduced provided that no fee is charged and the original source is properly cited. About the Series The Studies in Applied Economics series is under the general direction of Professor Steve H. Hanke, Co-Director of The Johns Hopkins Institute for Applied Economics, Global Health and the Study of Business Enterprise ([email protected]). The author is mainly a student at The Johns Hopkins University in Baltimore. Some of his work was performed as research assistant at the Institute. About the Author Erik Bostrom ([email protected]) is a student at The Johns Hopkins University in Baltimore, Maryland and is also a student in the BA/MA program at the Paul H. Nitze School of Advanced International Studies (SAIS) in Washington, D.C. Erik is a junior pursuing a Bachelor’s in International Studies and Economics and a Master’s in International Economics and Strategic Studies. He wrote this paper as an undergraduate researcher at the Institute for Applied Economics, Global Health, and the Study of Business Enterprise during Summer 2017. Erik will graduate in May 2019 from Johns Hopkins University and in May 2020 from SAIS. Abstract From 2007-2009 Zimbabwe underwent a hyperinflation that culminated in an annual inflation rate of 89.7 sextillion (10^21) percent. Consequently, the government abandoned the local Zimbabwean dollar and adopted a multi-currency system in which several foreign currencies were accepted as legal tender. -

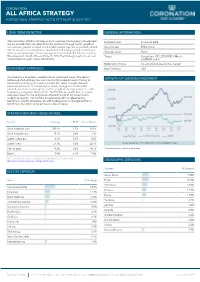

All Africa Strategy Institutional Strategy Fact Sheet As at 30 June 2017

CORONATION ALL AFRICA STRATEGY INSTITUTIONAL STRATEGY FACT SHEET AS AT 30 JUNE 2017 LONG TERM OBJECTIVE GENERAL INFORMATION The Coronation All Africa Strategy aims to maximise the long-term risk-adjusted Inception Date 01 August 2008 returns available from investments on the continent through capital growth of the underlying stocks selected. It is a flexible portfolio primarily invested in listed Strategy Size $78.4 million African equities or stocks listed on developed and emerging market exchanges Strategy Status Open where a substantial part of their earnings are derived from the African continent. The exposure to South Africa is limited to 50%. The Strategy may hold cash and Target Outperform ICE LIBOR USD 3 Month interest bearing assets where appropriate. (US0003M Index) Redemption Terms An anti-dilution levy will be charged INVESTMENT APPROACH Base Currency USD Coronation is a long-term, valuation-driven investment house, focused on GROWTH OF US$100M INVESTMENT bottom-up stock picking. Our aim is to identify mispriced assets trading at discounts to their long-term business value (fair value) through extensive proprietary research. In calculating fair values, through our fundamental research, we focus on through-the-cycle normalised earnings and/or free cash flows using a long-term time horizon. The Portfolio is constructed on a clean- slate basis based on the relative risk-adjusted upside to fair value of each underlying security. The Portfolio is constructed with no reference to a benchmark. We do not equate risk with tracking error, or divergence from a benchmark, but rather with a permanent loss of capital. STRATEGY RETURNS GROSS OF FEES Period Strategy LIBOR Active Return Since inception cum. -

Annual Report 2018

PROSPECT RESOURCES LIMITED / RESOURCES LIMITED / PROSPECT ANNUAL REPORT ANNUAL REPORT REPORT ANNUAL 2018 30 JUNE 2018 ACN 124 354 329 CORPORATECORPORATE DIRECTORYDIRECTORY DIRECTORS Hugh Warner Sam Hosack Harry Greaves Gerry Fahey Zed Rusike HeNian Chen SECRETARY Andrew Whitten PRINCIPAL OFFICE AUSTRALIA ZIMBABWE Suite 6, 245 Churchill Ave 169 Arcturus Road Subiaco, WA 6008 Greendale, Harare REGISTERED OFFICE Suite 6, 245 Churchill Ave Subiaco, WA 6008 Telephone: (08) 9217 3300 Email: [email protected] AUDITORS Stantons International Level 2 1 Walker Avenue West Perth WA 6005 SHARE REGISTRY Automic Pty Ltd Level 3 50 Holt Street Surry Hills, NSW 2010 Telephone: 1300 288 664 Investor Portal: https://investor.automic.com.au ASX CODE Shares – PSC LEGAL REPRESENTATIVES Whittens & McKeough Pty Limited Level 29, 201 Elizabeth Street Sydney, NSW 2000 PROSPECT RESOURCES LIMITED / ANNUAL REPORT 30 JUNE 2018 TABLE OF CONTENTS Corporate Directory IFC Chairman’s Statement 1 Review of Operations 3 Directors’ Report 9 Directors’ Declaration 20 Consolidated Statement of Profit or Loss and Other Comprehensive Income 21 Consolidated Statement of Financial Position 22 Consolidated Statement of Cash Flows 23 Consolidated Statement of Changes in Equity 24 Notes to and Forming Part of the Financial Statements 25 Auditor’s Independence Declaration 52 Independent Auditor’s Report 53 Australian Securities Exchange (ASX) Additional Information 57 I CHAIRMAN'S STATEMENT The Financial Year Ended 30 June 2018 has been an exciting one The drop in the share price of Prospect has not been lost on for Prospect Resources (ASX: PSC) (“Prospect”, the “Company”), our team. We would like to assure our shareholders that every as we transition from explorer to developer. -

Money Demand and Seignorage Maximization Before the End of the Zimbabwean Dollar

Money Demand and Seignorage Maximization before the End of the Zimbabwean Dollar Stephen Matteo Miller and Thandinkosi Ndhlela MERCATUS WORKING PAPER All studies in the Mercatus Working Paper series have followed a rigorous process of academic evaluation, including (except where otherwise noted) at least one double-blind peer review. Working Papers present an author’s provisional findings, which, upon further consideration and revision, are likely to be republished in an academic journal. The opinions expressed in Mercatus Working Papers are the authors’ and do not represent official positions of the Mercatus Center or George Mason University. Stephen Matteo Miller and Thandinkosi Ndhlela. “Money Demand and Seignorage Maximization before the End of the Zimbabwean Dollar.” Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, February 2019. Abstract Unlike most hyperinflations, during Zimbabwe’s recent hyperinflation, as in Revolutionary France, the currency ended before the regime. The empirical results here suggest that the Reserve Bank of Zimbabwe operated on the correct side of the inflation tax Laffer curve before abandoning the currency. Estimates of the seignorage- maximizing rate derive from a short-run structural vector autoregression framework using monthly parallel market exchange rate data computed from the ratio of prices from 1999 to 2008 for Old Mutual insurance company’s shares, which trade in London and Harare. Dynamic semi-elasticities generated from orthogonalized impulse response functions -

Impact of Currency Redenomination on an Economy: an Evidence of Ghana

International Business Research; Vol. 13, No. 2; 2020 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Impact of Currency Redenomination on an Economy: An Evidence of Ghana Bright Obuobi1, Emmanuel Nketiah1, Faustina Awuah2, Fredrick Oteng Agyeman1, Deborah Ofosu1, Gibbson Adu-Gyamfi1, Mavis Adjei1 & Adelaide Gyanwah Amadi1 1 School of Business, Nanjing University of Information Science & Technology, Nanjing 210044, China 2 University of Education, Winneba, Ghana Correspondence: Bright Obuobi, School of Business, Nanjing University of Information Science & Technology, Nanjing 210044, China. Received: December 6, 2019 Accepted: January 14, 2020 Online Published: January 16, 2020 doi:10.5539/ibr.v13n2p62 URL: https://doi.org/10.5539/ibr.v13n2p62 Abstract The main objective of this study is to ascertain the impact of currency redenomination on the Ghanaian economy. Since independence in 1957, Ghana has had series of redenomination exercises but the recent one which became a debatable topic happened in 2007. As a result, the study is conducted to determine the pre and post-performance of the country using 2007 as the benchmark. This research takes into consideration the quantitative research technique based on ex-post factor design. Secondary data of the research variables (GDP, Economic growth, Balance of trade, inflation, FDI and Globalization index) were used over a 20-year period between 1997 and 2017. Analytical techniques of both descriptive statistics and independent sample test were used for the research. The t-test for equality of means adopted was to determine the statistically significant difference on the economic variables. The study also used the Levene’s test of equality of variance assumed. -

Working Paper Series Roberto A

Working Paper Series Roberto A. De Santis A measure of redenomination risk 1785 / April 2015 Note: This Working Paper should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB Abstract Euro redenomination risk is the risk that a euro asset will be redenominated into a devalued legacy currency. We propose a time-varying, country-specific market perception of intra-euro area redenomination risk measure, defined as the quanto CDS of a member country relative to the quanto CDS of a benchmark member country. Focusing on Italy, Spain and France and using Germany as benchmark, we show that the redenomination risk shocks, defined as the unexplained component of the market perception of redenomination risk orthogonal to exchange rate, global, regional and liquidity risks, significantly affect sovereign yield spreads, with Italy and Spain being the countries most adversely affected, followed by France. Finally, foreign redenomination risk shocks spill over and above local redenomination risk shocks, corroborating the fact that this risk is systemic. Keywords: Redenomination risk, sovereign credit spreads, systemic risk, euro. JEL classification: C32, F36, G12, G15 ECB Working Paper 1785, April 2015 1 Non-Technical Executive Summary On 24 July 2012, the sovereign yield spreads of Italian and Spanish sovereign bonds - as measured by sovereign yield relative to the overnight index swap (OIS) rate - a risk-free rate proxy - reached record highs. The same spreads had been about 200 basis points lower only few months earlier in March 2012. -

The Currency Conversion in Postwar Taiwan: Gold Standard from 1949 to 1950 Shih-Hui Li1

The Kyoto Economic Review 74(2): 191–203 (December 2005) The Currency Conversion in Postwar Taiwan: Gold Standard from 1949 to 1950 Shih-hui Li1 1Graduate School of Economics, Kyoto University. E-mail: [email protected] The discourses on Taiwanese successful currency reform in postwar period usually put emphasis on the actors of the U.S. economic aids. However, the objective of this research is to re-examine Taiwanese currency reform experiences from the vantage- point of the gold standard during 1949–50. When Kuomintang (KMT) government decided to undertake the currency conversion on June 15, 1949, it was unaided. The inflation was so severe that the KMT government must have used all the resources to finish the inflation immediately and to restore the public confidence in new currency as well as in the government itself. Under such circumstances, the KMT government established a full gold standard based on the gold reserve which the KMT government brought from mainland China in 1949. This research would like to investigate what role the gold standard played during the process of the currency conversion. Where this gold reserve was from? And how much the gold reserve possessed by the KMT government during this period of time? Trying to answer these questions, the research investigates three sources of data: achieves of the KMT government in the period of mainland China, the official re- ports of the KMT government in Taiwan, and the statistics gathered from international organizations. Although the success of Taiwanese currency reform was mostly from the help of U.S.