Connecting Global Fintech: Hub Review 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Mastercard Compliant Service Provider List

The Mastercard Compliant Service Provider List A company’s name appears on this Compliant Service Provider List if (i) MasterCard has received a copy of an Attestation of Compliance (AOC) by a Qualified Security Assessor (QSA) reflecting validation of the company being PCI DSS compliant and (ii) MasterCard records reflect the company is registered as a Service Provider by one or more MasterCard Customers. The date of the AOC and the name of the QSA are also provided. Each AOC is valid for one year. MasterCard receives copies of AOCs from various sources. This Compliant Service Provider List is provided solely for the convenience of MasterCard Customers and any Customer that relies upon or otherwise uses this Compliant Service Provider list does so at the Customer’s sole risk. While MasterCard endeavors to keep the list current as of the date set forth in the footer, MasterCard disclaims any and all warranties of any kind, including any warranty of accuracy or completeness or fitness for any particular purpose. MasterCard disclaims any and all liability of any nature relating to or arising in connection with the use of or reliance on the Compliant Service Provider List or any part thereof. Each MasterCard Customer is obligated to comply with MasterCard Rules and other Standards pertaining to use of a Service Provider. As a reminder, an AOC by a QSA provides a “snapshot” of security controls in place at a point in time. Service Provider Name Region AOC Date Assessor DESV 1&1 Internet SE (1&1, 1&1 ipayment, Europe 05/09/2016 Security Research & Consulting GmbH ipayment.de) 1Link (Guarantee) Limited SAMEA 11/17/2015 Trustwave 1Shoppingcart.com (Web.com Group, lnc.) US 04/13/2016 SecurityMetrics 1stPayGateWay, LLC US 05/27/2016 IBM Internet Security Systems (ISS) 2138617 Ontario Inc. -

See Important Disclosures and Disclaimers at the End of This Report

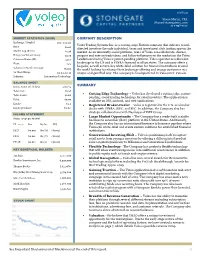

1/28/20 Shane Martin, CFA [email protected] 214-987-4121 MARKET STATISTICS ($CAD) COMPANY DESCRIPTION Exchange / Symbol OTC: VLEOF Voleo Trading Systems Inc. is a cutting-edge Fintech company that delivers to self- Price: $0.05 directed investors the only individual, team and investment club trading app on the Market Cap ($mm): $5.38 market. As an inherently social platform, users of Voleo can collaborate, discuss, Enterprise Value ($mm): $3.76 propose and vote on trade ideas, and follow influencers in the market on the Voleo Common Shares (M): 107.7 Leaderboard using Voleo’s patent-pending platform. Voleo operates as a discount brokerage in the US and is FINRA-licensed in all 50 states. The company offers a Float: 74% bespoke, as well as turn-key white-label solution for financial institutions around Volume (3 Month Average): 76,012 the world looking to enhance their brokerage offering and engage customers in a 52 Week Range: $0.04-$0.30 unique and gamified way. The company is headquartered in Vancouver, Canada. Industry: Information Technology BALANCE SHEET ($mm, except per sh data) 9/30/19 SUMMARY Total Cash: $1.98 • Cutting Edge Technology – Voleo has developed a cutting edge, patent- Total Assets: $2.68 pending, social trading technology for retail investors. The application is Debt: $0.00 available on iOS, android, and web applications. Equity: $2.2 • Registered Broker-Dealer – Voleo is registered in the U.S. as a broker- Equity per share: $0.02 dealer with FINRA, SIPC, and SEC. In addition, the Company also has strategic collaborations with Nasdaq and TMX Group. -

Payments Market Update SUMMER 2020 Payments Market Update–Summer 2020

Payments Market Update SUMMER 2020 Payments Market Update–Summer 2020 Dear Clients and Friends, Houlihan Lokey is pleased to present its Payments Market Update for the summer of 2020. We hope that you and your families remain safe and healthy. We have continued adapting to this fluid market and are busy helping our clients navigate financing, M&A, and other strategic alternatives. Please reach out to any of us if you would like to connect or brainstorm regarding any current needs or sector topics. We have included industry insights, select recent transaction announcements, and a public markets overview to help you stay ahead in our dynamic industry. We hope you find this update to be informative and that it serves as a valuable resource to you in staying abreast of the market. We look forward to staying in touch. Kind regards, Rob Freiman Director, Fintech [email protected] 212.497.7859 Additional Houlihan Lokey Fintech Contacts Corporate Finance Financial and Valuation Advisory Mark Fisher Tim Shortland David Sola Andrew Stull Oscar Aarts Managing Director Managing Director Managing Director Managing Director Director [email protected] [email protected] [email protected] [email protected] [email protected] Kegan Greene Chris Pedone Reggie Graham Director Director Senior Vice President [email protected] [email protected] [email protected] Payments Subsectors Covered: B2B PAYMENTS BLOCKCHAIN CREDIT CARDS DEBIT CARDS DISBURSEMENTS FOREIGN EXCHANGE FRAUD PROTECTION INTEGRATED PAYMENTS ISSUER PROCESSING LOAN PROCESSING LOYALTY/ REWARDS MERCHANT ACQUIRING MOBILE PAYMENTS MONEY TRANSFER NETWORKS P2P PAYMENTS PAYMENT FACILITATORS POS HARDWARE POS SOFTWARE / ISVs PREPAID UNATTENDED / KIOSKS / ATMS VERTICAL PAYMENTS 2 Market Insights and Observations While the COVID-19 pandemic reduced economic activity (and associated payments) across the globe, the crisis is likely to accelerate innovation across the sector. -

For Personal Use Only Use Personal for Scheme, Other Than As a Wameja Shareholder Or Wameja DI Holder

Wameja Limited ACN 052 947 743 SCHEME BOOKLET For a scheme of arrangement between Wameja Limited ABN 59 052 947 743 and the holders of shares in Wameja in relation to the proposed acquisition of Wameja by Burst Acquisition Co. Pty. Ltd ACN 644 142 834, a subsidiary of Mastercard. Your directors unanimously recommend that you vote in favour of the Scheme in the absence of a superior proposal. This is an important document and requires your immediate attention. You should read it in its entirety before voting on the Scheme. If you are in any doubt about how to deal with this document, please consult your financial, legal, taxation or other professional adviser. Financial Adviser * Please refer to Section 14.4 (c) of this Scheme Booklet for disclosure of the interests of Directors in the For personal use only Scheme, other than as a Wameja Shareholder or Wameja DI Holder. For personal use only WAMEJA LTD | SCHEME BOOKLET CONTENTS Overview of this Scheme Booklet 4 What should you do? 5 Important Notices 6 Important Dates 10 Letter from the Chairman 11 What you will receive under the Scheme 13 1. Reasons to vote in favour of the Scheme 14 2. Reasons why you may consider voting against the Scheme 16 3. Frequently asked questions 17 4. Scheme Meeting details and how to vote on the Scheme 24 5. Summary of the Scheme 26 6. Information about Wameja 33 7. Information about Mastercard 40 8. Information about HomeSend 46 9. Risks associated with the Scheme 50 10. Implementation of the Scheme 52 11. -

Alberta Securities Commission Page 1 of 2 Reporting Issuer List - Cover Page

Alberta Securities Commission Page 1 of 2 Reporting Issuer List - Cover Page Reporting Issuers Default When a reporting issuer is noted in default, standardized codes (a number and, if applicable a letter, described in the legend below) will be appear in the column 'Nature of Default'. Every effort is made to ensure the accuracy of this list. A reporting issuer that does not appear on this list or that has inappropriately been noted in default should contact the Alberta Securities Commission (ASC) promptly. A reporting issuer’s management or insiders may be subject to a Management Cease Trade Order, but that order will NOT be shown on the list. Legend 1. The reporting issuer has failed to file the following continuous disclosure document prescribed by Alberta securities laws: (a) annual financial statements; (b) an interim financial report; (c) an annual or interim management's discussion and analysis (MD&A) or an annual or interim management report of fund performance (MRFP); (d) an annual information form; (AIF); (e) a certification of annual or interim filings under National Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (NI 52-109); (f) proxy materials or a required information circular; (g) an issuer profile supplement on the System for Electronic Disclosure By Insiders (SEDI); (h) a material change report; (i) a written update as required after filing a confidential report of a material change; (j) a business acquisition report; (k) the annual oil and gas disclosure prescribed by National Instrument -

Etika U Tehnologijama 2018

Etika u tehnologijama 2018. Vahid Razavi Prevod na srpski: Valerija Majus Marinković Attribution-NonCommercial-NoDerivatives 4.0 International (CC BY-NC-ND 4.0) (Detaljnije informacija nalaze se na kraju knjige) Predgovor srpskom izdanju Vahida sam upoznala nedugo pošto je stigao u Srbiju. Neki moji prijatelji već su bili deo njegovog BizCloud tima i pričali su mi samo najbolje o ovom Amerikancu-Irancu koji je došao u Beograd da započne svoj posao i pritom se dobro provede. Moji prijatelji su bili veoma zadovoljni što imaju priliku da rade za američku kompaniju, a da se pritom nisu osećali iskorišćeno ili potcenjeno na bilo koji način. Zapravo su bili oduševljeni svojim novim poslodavcem. Brzo smo postali prijatelji. Pretpostavljam da za njega kao Iranca nije bilo teško da se uklopi u ovo društvo gde su nam još uvek bitni porodica i prijatelji. Vrlo brzo Vahid je postao deo moje porodice. Glasan, uvek dobro raspoložen i ambiciozan, spreman da pomogne, da podrži dobru ideju, da ohrabri na iskorak, na napredak. Uvek sam bila sigurna u to na čemu sam s Vahidom i smatrala sam da je čovek od reči, čovek koji razume i poštuje prave vrednosti u životu. Svima nama, njegovim beogradskim prijateljima, bilo je veoma teško kad smo shvatili kako se slomio kad je drugi put boravio u Srbiji, posle svih lomova i razočaranja koje je doživeo u svojoj zemlji, u SAD. Zaista smo svi bili veoma zabrinuti i ja nisam mogla da zamislim šta se to desilo toj gromadi, toj prirodnoj sili pozitivne ambicije i dobre energije, pa da završi na psihijatriji u stranoj zemlji. -

Transactionwatch

TransactionWatch Week of: Weekly Newsletter For Payments Executives That Covers The Most Important March 30th – April 3rd And Relevant Merchant Acquiring Deals And Activity This report is based upon information considered reliable by The Strawhecker Group® (TSG), but the accuracy and completeness of such information is not guaranteed or warranted to be error-free. Information provided is as reasonably available, not to be deemed all inclusive. TSG assumes no obligation to update the content hereof. This report is subject to the terms and conditions of a separate license with recipient, is further protected by copyright under U.S. Copyright laws and is the property of TSG. Recipient may not copy, reproduce, distribute, publish, display, modify, create derivative works, transmit, exploit, or otherwise disseminate any part of this report except as expressly permitted under recipient’s license with TSG. The Strawhecker Group (TSG) is not endorsed, sponsored by, or in any other way affiliated with any companies identified in this presentation. The trademarks of third parties displayed herein are the property of such parties, and, are provided merely for identification purposes. TSG claims no rights therein. This document has not been prepared, approved or licensed by any entity identified in this report. © Copyright 2020. The Strawhecker Group ®. All Rights Reserved. Deal Activity Summary March 30th – April 3rd This Week’s M&A Overview Table of Contents In the wake of the COVID-19 pandemic, activity in the overall M&A space has Deal Activity Summary seen a slowdown across a wide range of industries, including merchant acquiring. As small-to-medium sized businesses (SMBs) take a hit due to lower COVID-19 Industry Impact consumer spending or temporary closures, many merchant acquirers and Historical M&A Tracker payment processors are largely affected. -

Fintech in Canada – British Columbia Edition, 2016

FinTech in Canada British Columbia Edition 2016 British Columbia Edition Table of Contents Participating Stakeholders ......................................................... ii Foreword ................................................................................... iii Canada’s FinTech Opportunity .................................................. iv Executive Summary .................................................................. vi Types of FinTech ....................................................................... 1 FinTech Law ............................................................................ 15 FinTech in Other Countries ...................................................... 18 Stakeholder Views ................................................................... 32 Canada as a FinTech Leader ................................................... 39 Roadmap to Leadership ........................................................... 47 Authors & Contributors ............................................................. 48 Sources.................................................................................... 49 FinTech in Canada – Towards Leading the Global Financial Technology Transition Page | i © 2016, Digital Finance Institute; McCarthy Tétrault LLP British Columbia Edition Participating Stakeholders Approximately 30% of the stakeholders who participated in the FinTech Report elected to do so without attribution. FinTech in Canada – Towards Leading the Global Financial Technology Transition Page | ii © 2016, -

Alberta Securities Commission Page 1 of 2 Reporting Issuer List - Cover Page

Alberta Securities Commission Page 1 of 2 Reporting Issuer List - Cover Page Reporting Issuers Default When a reporting issuer is noted in default, standardized codes (a number and, if applicable a letter, described in the legend below) will be appear in the column 'Nature of Default'. Every effort is made to ensure the accuracy of this list. A reporting issuer that does not appear on this list or that has inappropriately been noted in default should contact the Alberta Securities Commission (ASC) promptly. A reporting issuer’s management or insiders may be subject to a Management Cease Trade Order, but that order will NOT be shown on the list. Legend 1. The reporting issuer has failed to file the following continuous disclosure document prescribed by Alberta securities laws: (a) annual financial statements; (b) an interim financial report; (c) an annual or interim management's discussion and analysis (MD&A) or an annual or interim management report of fund performance (MRFP); (d) an annual information form; (AIF); (e) a certification of annual or interim filings under National Instrument 52-109 Certification of Disclosure in Issuers' Annual and Interim Filings (NI 52-109); (f) proxy materials or a required information circular; (g) an issuer profile supplement on the System for Electronic Disclosure By Insiders (SEDI); (h) a material change report; (i) a written update as required after filing a confidential report of a material change; (j) a business acquisition report; (k) the annual oil and gas disclosure prescribed by National Instrument -

The European Payments Industry Consolidates Around Its Two Largest Players

Rise of the champions: the European Payments industry consolidates around its two largest players Introduction From barters and coins to cash pooling to cashless exchanges, the payments industry has undergone a massive transformation since its inception. During the era of booming e-commerce, payment methods are evolving rapidly, with the scope of becoming faster, simpler, and more secure for all parties. The main segments of the payment ecosystem include acquirers/processors, issuers, card networks, gateways, ISOs/MSPs, and non card payments. 1. Acquirers/processors Acquiring (merchant) banks, also known as payment processors , (e.g., Worldpay, Worldline, Barclaycard, First Data, Nexi, Ingenico, Nets) process credit and debit card payments on behalf of a merchant, that is a business that wants to take card payments. Acquirers allow merchants to accept payments from the card-issuing banks (see point 3) through a point of sale terminal. They offer both the hardware and the software needed to “acquire” the payments, meaning to receive it and correctly linking it to a network on the likes of Mastercard. Oftentimes, these players also develop software that the banks use to handle the volume of payments and even perform analysis on the flows. This is a particularly interesting and value added area that is receiving a lot of attention lately, as for the commercial banks it is more and more cost effective to rely on external IT software rather than bear the costs of developing it in-house. In that regard, a particular solution is the ‘Payment as a Service’ (‘PaaS’) technology, which uses the Software-as-a-Service (‘SaaS’) model to connect a group of international payment systems, simplifying payments for the end customer. -

Payments Insights. Opinions. Volume 21

#payments insights. opinions. Customer expectations, Three forces pushing banks to modernize payments technology and regulation infrastructure demand that financial organizations update payments Payments systems have always been complex and a critical part of the banking world. systems before the next wave But over the past decade, dynamic changes within payments have created even greater challenges for financial organizations and have driven the need for payments of disruption. transformation. In particular, more complex regulation, advancing technology and demands from customers to create a consistent, seamless experience across multiple channels are pushing banks, FinTechs and payment processors to invest heavily in payments modernization. Upgrading infrastructure to address these challenges, while keeping costs under control, requires financial organizations to first understand the drivers of change. Continued on page 3 Volume 26 03 Three forces pushing banks to modernize payments infrastructure Customer expectations, technology and regulation demand financial organizations update payments systems before the next wave of disruption. 05 How Africa’s growing mobile money market is evolving Africa’s fast-growing mobile money market offers opportunities to boost financial inclusion and tap the continent’s economic potential. Editorial 08 Welcome to the first issue of #payments for 2020. Can issuing capabilities strengthen acquirers’ competitive position? In this newsletter, we explore a diverse set of topics that we know are top of mind Since European Union (EU) regulators introduced a for many financial institutions this year. fee cap on credit card transactions, acquirers have been seeking new ways to boost margins. Some are • The ongoing challenge to modernize payments architecture is explored in an now issuing their own cards, to protect profitability and create competitive advantage. -

Payments Market Update FALL 2020 Payments Market Update—Fall 2020

Payments Market Update FALL 2020 Payments Market Update—Fall 2020 Houlihan Lokey is pleased to present its Payments Market Update for the fall of 2020. Dear Clients and Friends, We are pleased to present our Payments Market Update for the fall of 2020. We hope that you and your families remain safe and healthy. We have continued adapting to this fluid market and are busy helping our Rob Freiman clients navigate M&A, financing, and other strategic alternatives. Please reach out to any of us if you would Director, Fintech like to connect or brainstorm regarding any current needs or sector topics. [email protected] We have included industry insights, select recent transaction announcements, and a public markets 212.497.7859 overview (including some new additions, such as Nuvei and Shift4, with Billtrust coming soon) to help you stay ahead in our dynamic industry. We hope you find this update to be informative and that it serves as a valuable resource to you in staying abreast of the market. We look forward to staying in touch. Cheers, Additional Houlihan Lokey Fintech Contacts Corporate Finance Financial and Valuation Advisory Mark Fisher Tim Shortland David Sola Andrew Stull Oscar Aarts Managing Director Managing Director Managing Director Managing Director Director [email protected] [email protected] [email protected] [email protected] [email protected] Kegan Greene Chris Pedone Reggie Graham Director Director Senior Vice President [email protected] [email protected] [email protected] Payments Subsectors Covered: B2B PAYMENTS BLOCKCHAIN CREDIT CARDS DEBIT CARDS DISBURSEMENTS