Annual Report 2010

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Second Homes in the Slovenian Alps with Special Emphasis on the Municipality of Bovec

HRVATSKI GEOGRAFSKI GLASNIK 81/1, 61−81 (2019.) UDK 338.488.2:643-022.348](497.4) Original scientific paper 911.3:338.48](497.4) Izvorni znanstveni članak DOI 10.21861/HGG.2019.81.01.03 Received / Primljeno 2018-11-30 / 30-11-2018 Miha Koderman Accepted / Prihvaćeno Marko Pavlič 2019-01-09 / 09-01-2019 Second homes in the Slovenian Alps with special emphasis on the Municipality of Bovec Vikendice u slovenskim Alpama s posebnim naglaskom na općinu Bovec In the past decades, second homes have caused Proteklih su desetljeća vikendice uzrokovale important transformations in the morphology of značajne transformacije u morfologiji tradicionalnih traditional village-based settlements in many mountain seoskih naselja u mnogim planinskim područjima. Te areas. Such changes are particularly evident in the intense su promjene osobito vidljive u naglašenoj koncentraciji concentration of these buildings in some settlements and vikendica u formi kuća u ponekim naseljima, a mogu se can occur in the form of multi-apartment recreational javljati i u obliku višestambenih apartmanskih zgrada za complexes, intentionally designed for second home users. odmor i rekreaciju. U ovom se radu analizira prostorni This paper analyses spatial development of registered razvoj registriranih vikendica u slovenskoj općini Bovec, second homes in the municipality of Bovec, Slovenia, pridonoseći tako razumijevanju specifičnosti toga thus contributing to understanding the specifics of this fenomena u širem alpskom području, ali i u drugim phenomenon in the wider Alpine region, as well as in other planinskim regijama. Autori proučavaju odabrana mountainous regions. The authors examine the selected obilježja stambenoga fonda vikendica u općini (lokaciju, characteristics of the municipal second home housing vrijeme izgradnje, intenzitet fenomena vikendaštva) i stock (location, age, intensity of the phenomenon) and prezentiraju podatke pomoću detaljnih kartografskih present the data in detailed cartographic representations. -

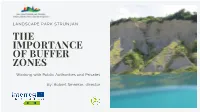

The Importance of Buffer Zones: Working with Public Authorities And

LANDSCAPE PARK STRUNJAN THE IMPORTANCE OF BUFFER ZONES Working with Public Authorities and Privates By: Robert Smrekar, director The development of a common strategy to foster the sustainable tourism involving public authorities and privates, and how a buffer zone serve as a tool to mitigate the impact of tourism Main topic: The Lanscape Park Strunjan Joint Decree of the Municipality of Piran and Izola in 1990. 428 Hectares 2 Nature Reserves, 1 Natural Monument, 13 Natural Values. Established by Two Local Municipalities PARK LOCATION Northern Adriatic, Gulf of Trieste, Slovenian Coast. PARK MANAGEMENT Public Institute Landscape Park Strunjan, est. 2009 700 YEARS OF TRADITION Saltpans The Smallest and the Northernmost Saltpans in the Mediterranean Basin The Only Slovenian Marine Lagoon - Stjuža THE HIGHEST FLYSCH CLIFF ON THE EAST ADRIATIC COAST METERS HIGH THE SEA "The Largest Marine Protected Area in the Slovenian Sea" THE LANDSCAPE One of the Most Conserved Cultural Landscape on Slovenian Coast. Pressure: 400.000 Visitors per year And Rising Overtourism. On Land And on the Sea Seeking the Balance Between Nature Protection, Businesses and Local Inhabitants The Engagement of Local Authorities Detailed Analysis Contact With Decision-makers Clear Vison Provide Solutions, Not Problems Two Buffer Zones: Belvedere Terraces (Municipality of Izola) and Strunjan (Municipality of Piran) Buffer Zones ENTRY POINTS Activities: (To be Included in Spatial Regulatory Acts) Stationary Traffic Alternatives to Car Visitors Awareness Buffer Zones Regulation -

Institutions Contact Person Priority 1, Strategic Theme 1: Innovation As

Institutions Contact person e-mail Priority 1, Strategic theme 1: Innovation as key for economic development Municipality of Koper, Verdijeve 10, 6000 Koper, Slovenia Ivana Štrkalj [email protected] Municipality of Izola, Sončno nabrežje 8, 6310 Izola, Slovenia Boštjan Lavrič [email protected] Regional development agency of Northern Primorska, Trg Edvarda Kardelja 3, 5000 Nova Gorica, Slovenia Tomaž Vadjunec [email protected] Chamber of Craft and Small Business of Slovenia, Celovška 71, 1000 Ljubljana, Slovenia Bogdan Sovinc [email protected] Primorska Technology Park, mednarodni prehod 6, vrtojba, 5290 Šempeter pri Novi Gorici Tanja Kožuh [email protected] Tehniški šolski center Nova Gorica, Cankarjeva 10, 5000 Nova Gorica, Slovenia Rosana Pahor [email protected] GEA College, Kidričevo nabrežje 2, 6330 Piran Majda Gartner [email protected] Centre of Excellence BIPC (www.cobik.si) Mladen Dakič [email protected] Priority 2, Strategic theme 1: Improving marine, coastal and delta rivers environment by joint management Institute for Water of the Republic of Slovenia, Hajdrihova 28 c, 1000 Ljubljana, Slovenia Leon Gosar [email protected] Jožef Stefan Institute, Jamova cesta 39, 1000 Ljubljana, Slovenia Sonja Lojen [email protected] Municipality of Izola, Sončno nabrežje 8, 6310 Izola, Slovenia Boštjan Lavrič [email protected] Slovenian national building and civil engineering institute, Dimičeva 12, 1000 Ljubljana Karmen Fifer [email protected] Municipality of Koper, Verdijeve 10, 6000 Koper, Slovenia Ivana Štrkalj [email protected] Priority 2, Strategic theme 2: Protection from ballast water pollution A single potential partnership with Slovenian institutions is in a process of establishment where the Institute for Water of the Republic of Slovenia will assume a role of a Lead Beneficiary. -

JULIAN ALPS TRIGLAV NATIONAL PARK 2The Julian Alps

1 JULIAN ALPS TRIGLAV NATIONAL PARK www.slovenia.info 2The Julian Alps The Julian Alps are the southeast- ernmost part of the Alpine arc and at the same time the mountain range that marks the border between Slo- venia and Italy. They are usually divided into the East- ern and Western Julian Alps. The East- ern Julian Alps, which make up approx- imately three-quarters of the range and cover an area of 1,542 km2, lie entirely on the Slovenian side of the border and are the largest and highest Alpine range in Slovenia. The highest peak is Triglav (2,864 metres), but there are more than 150 other peaks over 2,000 metres high. The emerald river Soča rises on one side of the Julian Alps, in the Primorska re- gion; the two headwaters of the river Sava – the Sava Dolinka and the Sava Bohinjka – rise on the other side, in the Gorenjska region. The Julian Alps – the kingdom of Zlatorog According to an ancient legend a white chamois with golden horns lived in the mountains. The people of the area named him Zlatorog, or “Goldhorn”. He guarded the treasures of nature. One day a greedy hunter set off into the mountains and, ignoring the warnings, tracked down Zlatorog and shot him. Blood ran from his wounds Chamois The Triglav rose and fell to the ground. Where it landed, a miraculous plant, the Triglav rose, sprang up. Zlatorog ate the flowers of this plant and its magical healing powers made him invulnerable. At the same time, however, he was saddened by the greed of human beings. -

BOHINJ GUEST CARD 2014 T: +386 (0)4 572 34 61, M: +386 (0)40 864 202, E: [email protected], TOURIST ASSOCIATION BOHINJ, Ribčev Laz 48, 4265 Boh

BOHINJ GUEST CARD RENTAL: - 5% on bread, on pastry and handicraft products purchased at Pr’ Vandrovc farm - 5% on visit to the Slovenian Alpine Museum in Mojstrana Bohinj Tourism and the Municipality of Bohinj offer a card to guests who stay at ALPE d.o.o., CLIMBING SCHOOL, Ravne v Bohinju 17, 4264 Bohinjska Bistrica, stand, every Saturday at the market in Bohinjska Bistrica *2+1 = visits of two museum collections in Jesenice are payable, the third visit is free. least two nights in Bohinj and pay tourist tax. The card is also intended for vacation t/f: +386 (0)4 574 77 40, m: +386 (0)40 349 669 and +386 (0)31 228 008, TOURIST ASSOCIATION BOHINJ, Ribčev Laz 48, 4265 Boh. jezero, t: +386 (0)4 574 60 10, KOBARID: KOBARID MUSEUM, D.O.O., Gregorčičeva 10, 5222 Kobarid, t: +386 (0)5 389 00 houses’ and apartment owners who pay lump sum tourist tax in accordance with e: [email protected], www.alpe-rjavina.si f: +386 (0)4 572 33 30, e: [email protected], www.bohinj-info.com 00, f: +386 (0)5 389 00 02, m: +386 (0)41 714 072, e: [email protected], the provisions of the Tourism Development Act and the Decree on tourist tax in the - 10% on climbing and hiking equipment rental CAMPSITE DANICA: - 5% all products from gift programme www.kobariski-muzej.si - 20% on visit to the museum Municipality of Bohinj. ALPINSPORT, Bohinjsko jezero d.o.o., Ribčev Laz 53, 4265 Boh. -

Case Study Slovenia

TOWN Small and medium sized towns in their functional territorial context Applied Research 2013/1/23 Case Study Report | Slovenia Version 05/09/2013 ESPON 2013 1 This report presents the interim results of an Applied Research Project conducted within the framework of the ESPON 2013 Programme, partly financed by the European Regional Development Fund. The partnership behind the ESPON Programme consists of the EU Commission and the Member States of the EU27, plus Iceland, Liechtenstein, Norway and Switzerland. Each partner is represented in the ESPON Monitoring Committee. This report does not necessarily reflect the opinion of the members of the Monitoring Committee. Information on the ESPON Programme and projects can be found on www.espon.eu The web site provides the possibility to download and examine the most recent documents produced by finalised and ongoing ESPON projects. This basic report exists only in an electronic version. © ESPON & University of Leuven, 2013. Printing, reproduction or quotation is authorised provided the source is acknowledged and a copy is forwarded to the ESPON Coordination Unit in Luxembourg. List of authors Nataša Pichler-Milanović, University of Ljubljana, Faculty of Civil and Geodetic Engineering, Ljubljana, Slovenia Samo Drobne, University of Ljubljana, Faculty of Civil and Geodetic Engineering, Ljubljana, Slovenia Miha Konjar, University of Ljubljana, Faculty of Civil and Geodetic Engineering, Ljubljana, Slovenia © Institute UL-FGG d.o.o, Jamova 2, SI-1001 Ljubljana, Slovenia ESPON 2013 i Table of contents -

D Ve Domo Vini • T W O Homelands 25 • 200 7 25 • 2007

DVE DOMOVINI ● TWO HOMELANDS Razprave o izseljenstvu ● Migration Studies 25 ● 2007 dve domovinidomovini Razprave in članki / Essays and Articles Pojasnilo k tematskemu sklopu Žumberčani – nekdanji in sedanji graničarji (Duška Knežević Hočevar) Problem »pripadnosti« Žumberčanov in Marindolcev v desetletjih pred two HomelandsHomelands razpustom Vojne krajine 1881 in po njem (Marko Zajc) Žumberk: meja, etničnost, veroizpoved, rodnost in migracije prebivalstva 25 • 2007 – demogeografska analiza (Damir Josipovič) Nekatere demografske značilnosti grkokatoliških Žumberčanov v Sloveniji (Peter Repolusk) Povratak na granicu: migracijska iskustva u trokutu Hrvatska-Njemačka- Slovenija (Jasna Čapo Žmegač) Ali se Žumberčani večinoma poročajo med seboj? Primer župnije v Radatovićih (Duška Knežević Hočevar) Poročne strategije župljanov Velikih Brusnic izpod Gorjancev pri Novem mestu (Irena Rožman) Krekova Vestfalska pisma: socialno-ekonomski pogledi in izseljenstvo (Marjan Drnovšek) Normativni vidiki in delovne razmere za migrante v Zvezni republiki Nemčiji (Marina Lukšič - Hacin) Izseljenska književnost in časopisje: zgovorne statistike (Janja Žitnik) Marie Prisland – her role in preserving Slovenian culture and tradition among Slovenian migrants in the United States (Mirjam Milharčič Hladnik) Ethnic, regional and national identities in the context of European cross border cooperation opportunities: a case study of Italian ethnic community in Slovene Istria (Ksenija Šabec) Način življenja hrvatskog iseljeničkog korpusa u Australiji: iskustva, mišljenja -

Mediterranean Action Plan

MAP Mediterranean Action Plan MAP Coastal Area Management Programme (CAMP) Slovenia: Final Integrated Report MAP Technical Reports Series No. 171 Note: The designations employed and the presentation of the material in this document do not imply the expression of any opinion whatsoever on the part of UNEP/MAP concerning the legal status of any State, Territory, city or area, or of its authorities, or concerning the delimitation of their frontiers or boundaries. Note: Les appellations employées dans ce document et la présentation des données qui y figurent n'impliquent de la part du PNUE/PAM aucune prise de position quant au statut juridique des pays, territoires, villes ou zones, ou de leurs autorités, ni quant au tracé de leurs frontières ou limites. This report was prepared under the co-ordination of the UNEP/MAP Priority Actions Programme, Regional Activity Centre (PAP/RAC). This series contains selected reports resulting from the various activities performed within the framework of the components of the Mediterranean Action Plan: Blue Plan (BP), Priority Actions Programme (PAP), Specially Protected Areas (SPA) and Regional Marine Pollution Emergency Response Centre for the Mediterranean Sea (REMPEC). Ce rapport a été préparé sous la coordination du Centre d'Activités Régionales pour le Programme d'Actions Prioritaires (CAR/PAP) du PNUE/PAM. Cette série rassemble des rapports sélectionnés établis dans le cadre de la mise en œuvre des diverses composantes du Plan d'Action pour la Méditerranée: Plan Bleu (PB), Programme d'Actions Prioritaires (PAP), Aires Spécialement Protégées (ASP) et Centre régional méditerranéen pour l'intervention d'urgence contre la pollution marine accidentelle (REMPEC). -

Report by the Republic of Slovenia on the Implementation of The

ACFC/SR (2000) 4 REPORT SUBMITTED BY THE REPUBLIC OF SLOVENIA PURSUANT TO ARTICLE 25, PARAGRAPH 1, OF THE FRAMEWORK CONVENTION FOR THE PROTECTION OF NATIONAL MINORITIES TABLE OF CONTENTS GENERAL EXPLANATION ABOUT DRAWING UP THE REPORT __________4 PART I _____________________________________________________________6 General information______________________________________________________ 6 Brief historical outline and social arrangement _______________________________ 6 Basic Economic Indicators ________________________________________________ 6 Recent general statements _________________________________________________ 7 Status of International Law________________________________________________ 8 The Protection of National Minorities and the Romany Community ______________ 9 Basic demographic data__________________________________________________ 11 Efficient measures for achieving the general goal of the Framework Convention __ 12 PART II ___________________________________________________________13 Article 1_______________________________________________________________ 13 Article 2_______________________________________________________________ 14 Article 3_______________________________________________________________ 16 Article 4_______________________________________________________________ 18 Article 5_______________________________________________________________ 26 Article 6_______________________________________________________________ 31 Article 7_______________________________________________________________ 37 Article 8_______________________________________________________________ -

Stakeholder Analysis in the Biomass Energy Development Based on the Experts’ Opinions: the Example of Triglav National Park in Slovenia

Folia Forestalia Polonica, series A, 2015, Vol. 57 (3), 173–186 ORIGINAL ARTICLE DOI: 10.1515/ffp-2015-0017 Stakeholder analysis in the biomass energy development based on the experts’ opinions: the example of Triglav National Park in Slovenia Gianluca Grilli1, 2 , Giulia Garegnani2, Aleš Poljanec3, 4, Andrej Ficko4, Daniele Vettorato2, Isabella De Meo5, Alessandro Paletto6 1 University of Trento, Department of Civil, Environmental and Mechanical Engineering, via Mesiano 77, 38123 Trento, Italy, phone: +39 0471 055 668, email: [email protected] 2 EURAC Research, Institute for Renewable Energy, Viale Druso Drususallee 1, Bozen, Italy 3 Slovenia Forest Service, Večna pot 2, 1000 Ljubljana, Slovenia 4 University of Ljubljana, Biotechnical Faculty, Department for Forestry and Renewable Forest Resources, Jamnikarjeva 101, 1000 Ljubljana, Slovenia 5 Council for Agricultural Research and Economics, Agrobiology and Pedology Centre – CREA-ABP, Firenze, Italy 6 Council for Agricultural Research and Economics, Forest Monitoring and Planning Research Unit – CREA-MPF, Trento, Italy AbstrAct The paper presents a method for identifying and classifying local stakeholders involved in renewable energy de- velopment. The method is based on the expert assessment and comprises three main steps: (1) identification of the independent experts considering their expertise and knowledge of the local context; (2) identification of the local stakeholders based on expert assessment; and (3) analytical categorisation of stakeholders taking into account the professional relationship network. Using forest biomass (bioenergy) production as example, the stakeholder analy- sis is illustrated on the case study of Triglav National Park, which is characterised by a high potential of woody biomass production and a large number of stakeholders involved in land use and management. -

Sustainability Report of the Petrol Group

sustainability report of the Petrol group sustainability report Printed on 100% recycled paper. We saved: 248 kg of wood, 2,988 liters of water, 281 kWh of energy, 29 kg of CO2, 285 km road by the average European car and 153 kg of waste (source calculated as follows: www.arjowigginsgraphic.com/cyclus.html). PETROL, Slovenska energetska družba, d.d., Ljubljana Dunajska cesta 50, 1527 Ljubljana Phone: +386 1 47 14 232 www.petrol.eu sustainability report of the Petrol group sustainability report 2 sustainability report Optimization of district heating systems: 50,095 MWh of energy savings 14,027 t CO2 savings Providing energy savings to end-users: 215,000 MWh of energy savings Optimization of lighting: Efficient heat production: 80,000 t CO savings 2 6,284 MWh of electricity savings 5,799 MWh of energy savings Waste heat: 2,866 t CO savings 4,360 t CO savings 2 2 4,306 MWh of energy savings 328 t CO2 savings Renovation of boiler room and installation Photovoltaics: of cogeneration of heat and electricity unit: 2.75 GWh of electricity produced 21,057 m³ of natural gas savings 4,218 t CO savings 1,273 t CO2 savings 2 Integrated projects (implemented several measures): 5,380 MWh of energy savings 2,126 t CO2 savings Supply of electricity Cogeneration of heat and electricity: from renewable energy sources: 3.2 million m³ of natural gas savings 20% of electricity supplied 6,161 t CO2 savings Biogas plant : production of 7,166 MWh of energy from 3.4 million m³ of biogas 462 5 EV charging stations at service stations Biofuels: service stations 11,572 t CO savings Wastewater treatment plant: Q Max Fuel: 2 2,655,157 m³ treated municipal water Efficient use of water: lower consumption; 69 small wastewater treatment lower emissions of harmful gases savings of 86,987 m³ of water plants at service stations All values refer to annual savings. -

Combined Strategic & Annual Programme Report on The

REPUBLIC OF SLOVENIA GOVERNMENT OFFICE FOR DEVELOPMENT AND EUROPEAN COHESION POLICY COMBINED STRATEGIC & ANNUAL PROGRAMME REPORT ON THE IMPLEMENTATION OF THE EEA FINANCIAL MECHANISM AND NORWEGIAN FINANCIAL MECHANISM 2009 - 2014 IN SLOVENIA Reporting period: January 2014 – December 2014 Prepared by: National Focal Point Government Office for Development and European Cohesion Policy 1 EXECUTIVE SUMMARY The main objective of the funds from NOR and EEA Financial Mechanisms 2009-2014 is to contribute to reducing economic and social differences and to enhance relations between beneficiary countries and donor countries. To attain its objectives, Slovenia and the donor countries determined the following priority areas: the environment and climate change, cultural heritage, research and scholarships, human and social development and civil society. Programmes SI01 (technical assistance and the fund for bilateral relations at national level), SI02 (EEA Financial Mechanism Programme) and SI05 (Norwegian Financial Mechanism Programme) were operated by the Ministry of Economic Development and Technology by 1 March 2014. On 1 March 2014 the new Government Office for Development and European Cohesion Policy was established and all above mentioned programmes are now managed by the Government Office for Development and European Cohesion Policy. SI03 (Funds for non-governmental organisations) is managed by the Regional Environmental Centre and the Centre for Information Service, Co-operation and Development of NGOs, SI04 (EEA and Norwegian scholarship programme) is managed by CMEPIUS and SI22 (Global fund for decent work and tripartite dialogue). Programmes SI01, SI03, SI04 and SI22 are in full implementation. For the programmes SI02 (EEA Financial Mechanism Programme) and SI05 (Norwegian Financial Mechanism Programme) the call for proposals was published on 27 December 2013 with the deadline for submission of project proposals 28 February 2014.