Automobile Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Contacts in Japan Contacts in Asia

TheDirectoryof JapaneseAuto Manufacturers′ WbrldwidePurchaslng ● Contacts ● トOriginalEqulpment ● トOriginalEqulpment Service トAccessories トMaterials +RmR JA払NAuTOMOBILEMANUFACTURERSAssocIATION′INC. DAIHATSU CONTACTS IN JAPAN CONTACTS IN ASIA OE, Service, Accessories and Material OE Parts for Asian Plants: P.T. Astra Daihatsu Motor Daihatsu Motor Co., Ltd. JL. Gaya Motor 3/5, Sunter II, Jakarta 14350, urchasing Div. PO Box 1166 Jakarta 14011, Indonesia 1-1, Daihatsu-cho, Ikeda-shi, Phone: 62-21-651-0300 Osaka, 563-0044 Japan Fax: 62-21-651-0834 Phone: 072-754-3331 Fax: 072-751-7666 Perodua Manufacturing Sdn. Bhd. Lot 1896, Sungai Choh, Mukim Serendah, Locked Bag No.226, 48009 Rawang, Selangor Darul Ehsan, Malaysia Phone: 60-3-6092-8888 Fax: 60-3-6090-2167 1 HINO CONTACTS IN JAPAN CONTACTS IN ASIA OE, Service, Aceessories and Materials OE, Service Parts and Accessories Hino Motors, Ltd. For Indonesia Plant: Purchasing Planning Div. P.T. Hino Motors Manufacturing Indonesia 1-1, Hinodai 3-chome, Hino-shi, Kawasan Industri Kota Bukit Indah Blok D1 No.1 Tokyo 191-8660 Japan Purwakarta 41181, Phone: 042-586-5474/5481 Jawa Barat, Indonesia Fax: 042-586-5477 Phone: 0264-351-911 Fax: 0264-351-755 CONTACTS IN NORTH AMERICA For Malaysia Plant: Hino Motors (Malaysia) Sdn. Bhd. OE, Service Parts and Accessories Lot P.T. 24, Jalan 223, For America Plant: Section 51A 46100, Petaling Jaya, Hino Motors Manufacturing U.S.A., Inc. Selangor, Malaysia 290 S. Milliken Avenue Phone: 03-757-3517 Ontario, California 91761 Fax: 03-757-2235 Phone: 909-974-4850 Fax: 909-937-3480 For Thailand Plant: Hino Motors Manufacturing (Thailand)Ltd. -

Master List of DTP Participants

Institute of Business Administration, Karachi Center for Executive Education Directors' Training Program Certification Year - No Program Name Designation Organization No. Certitied CCL Pharmaceuticals 215 IBA/DTP - 0213 2019 Dr. Shahzad Khan Chief Operating Officer CCL Pharmaceuticals Pvt Ltd Pvt Ltd 216 IBA/DTP - 0214 2019 IBA-Karachi Faisal Jalal IBA Faculty IBA-Karachi 217 IBA/DTP - 0215 2019 Self Lubna Pathan Director own Business 218 IBA/DTP - 0216 2019 Indus Clean Energy Masood Hasan Khan Head of Commercial Indus Clean Energy 219 IBA/DTP - 0217 2019 Avanceon Limited Naveed Ali Baig Director Avanceon Limited Senior Executive Vice President - 220 IBA/DTP - 0218 2019 Premier Insurance Nina Afridi Premier Insurance Head of HR & Administration 221 IBA/DTP - 0219 2019 Hinopak Motors Ltd. Yoshihiko Nanami President & CEO Hinopak Motors Ltd. 222 IBA/DTP - 0220 2019 Hinopak Motors Ltd. Shigeru Tsuchiya Executive Vice President Hinopak Motors Ltd. Vice President & Director 223 IBA/DTP - 0221 2019 Hinopak Motors Ltd. Takehito Sasaki Hinopak Motors Ltd. Production Vice President & Chief Financial 224 IBA/DTP - 0222 2019 Hinopak Motors Ltd. Fahim Aijaz Sabzwari Hinopak Motors Ltd. Officer 225 IBA/DTP - 0223 2019 Hinopak Motors Ltd. Naushad Riaz Vice President Hinopak Motors Ltd. 226 IBA/DTP - 0224 2019 Hinopak Motors Ltd. Syed Samad Siraj Deputy General Manager Hinopak Motors Ltd. 227 IBA/DTP - 0225 2019 Hinopak Motors Ltd. Muhammad Zahid Hasan Deputy General Manager Hinopak Motors Ltd. 228 IBA/DTP - 0226 2019 Hinopak Motors Ltd. Ahsan Waseem Akhtar Senior Manager HR, Admin & HSE Hinopak Motors Ltd. 229 IBA/DTP - 0227 2019 Hinopak Motors Ltd. Abdul Basit Departmental Head Finance Hinopak Motors Ltd. -

Materom Dialog Nr

MATEROM DIALOG NR. 23 AUGUST-OCTOMBRIE 2015 06 PROFESIONALISM ȘI VALOARE BOSCH LA BORDUL 36 LA TRAINING-UL ATE BMW M3 10 NEXUS AUTOMOTIVE PRODUSE PENTRU IUBITORII 42 INTERNAȚIONAL DE MOTO 22 EXPERT ÎN CONTROLUL VIBRAȚIILOR CELE MAI PRETIOASE PIESE SUNT LA NOI! 04 Zilele Clientului Materom Materom 06 Training-ul ATE Materom 07 Puțin praf, de lungă durată ATE Editorial 08 Dezmembrări auto Materom 09 Materom la Mureș Classic Days Materom 10 Nexus Automotive Internațional Materom La final de semestru... 11 Profită și tu de programul NORA Materom 12 Noul catalog electronic KYB ară frumoasă, vacanță, Ne îndreptăm cu multă care aleg furnizori naționali, neavoastră, dragi parteneri și 13 Despre produse Divinol concedii, e semn că a prețuire spre dumneavoastră, care la rândul lor investesc pro- colegi, să scriem istorie în Ro- 14 Set lanț de distribuție Ruville V trecut jumătate din an. dragi clienți și vă mulțumim în fitul în România și contribuie la mânia, să lăsăm copiilor noștri 15 Liniile de înaltă presiune AIC Privim la rezultatele companiei mod deosebit dumneavoastră, bunăstarea economiei noastre. o țară mai bună ca “afară“, o so- 16 Originea mecanismului acționare geam AcRolcar noastre și ne bucurăm să con- care ne-ați ales ca furnizor de Avem modele de patrioți ro- cietate cu valori morale și spiri- 18 Curele dințate: diagnoză și soluții Contitech statăm că avem recoltă bogată, piese și accesorii auto și care mâni, din toate timpurile, oa- tuale și cu bunăstare materială. 19 Recondiționatorul anului 2015 Borg o creștere bruscă ce ne aduce ne confirmați în fiecare zi, prin meni care au muncit din greu încredere că vor urma rezultate comenzile lansate spre noi, că și au fost mândrii de identita- Dumnezeu să ne ajute! 20 Despre Lucas Lucas și mai bune până la finele aces- v-am câștigat încrederea prin tea lor. -

Hinopak Motors Limited List of Shareholders Not Provided Their Cnic S.No Folio No

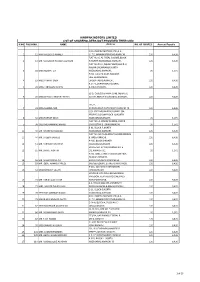

HINOPAK MOTORS LIMITED LIST OF SHAREHOLDERS NOT PROVIDED THEIR CNIC S.NO FOLIO NO. NAME Address NO. OF SHARES Amount Payable C/O HINOPAK MOTORS LTD.,D-2, 1 12 MIR MAQSOOD AHMED S.I.T.E.,MANGHOPIR ROAD,KARACHI., 120 6,426 FLAT NO. 6, AL-FAZAL SQUARE,BLOCK- 2 13 MR. MANZOOR HUSSAIN QURESHI H,NORTH NAZIMABAD,KARACHI., 120 6,426 FLAT NO.19-O, IQBAL PLAZA,BLOCK-O, NAGAN CHOWRANGI,NORTH 3 18 MISS NUSRAT ZIA NAZIMABAD,KARACHI., 20 1,071 H.NO. E-13/40,NEAR RAILWAY LINE,GHARIBABAD, 4 19 MISS FARHAT SABA LIAQUATABAD,KARACHI., 120 6,426 R.177-1,SHARIFABADFEDERAL 5 24 MISS TABASSUM NISHAT B.AREA,KARACHI., 120 6,426 52-D, Q-BLOCK,PAHAR GANJ, NEAR LAL 6 28 MISS SHAKILA ANWAR FATIMA KOTTHI,NORTH NAZIMABAD,KARACHI., 120 6,426 171/2, 7 31 MISS SAMINA NAZ AURANGABAD,NAZIMABAD,KARACHI-18. 120 6,426 C/O. SYED MUJAHID HUSSAINP-394, PEOPLES COLONYBLOCK-N, NORTH 8 32 MISS FARHAT ABIDI NAZIMABADKARACHI, 20 1,071 FLAT NO. A-3FARAZ AVENUE, BLOCK- 9 38 SYED MOHAMMAD HAMID 20GULISTAN-E-JOHARKARACHI, 20 1,071 B-91, BLOCK-P,NORTH 10 40 MR. KHURSHID MAJEED NAZIMABAD,KARACHI. 120 6,426 FLAT NO. M-45,AL-AZAM SQUARE,FEDRAL 11 44 MR. SALEEM JAWEED B. AREA,KARACHI., 120 6,426 A-485, BLOCK-DNORTH 12 51 MR. FARRUKH GHAFFAR NAZIMABADKARACHI. 120 6,426 HOUSE NO. D/401,KORANGI NO. 5 13 55 MR. SHAKIL AKHTAR 1/2,KARACHI-31. 20 1,071 H.NO. 3281, STREET NO.10,NEW FIDA HUSSAIN SHAIKHA 14 56 MR. -

History of Pakistan's Automobile Industry

History of Pakistan’s Automobile Industry Following international trends, the automobile industry in Pakistan showed substantial growth in the years under review. The growth was aided by favorable government policies during this period and levy of lower import duties on raw material inputs and on intermediate products. A significant rise in demand for automobiles, propelled at least partly by easy availability of auto leases and loans from banks and leasing companies at low financial cost, was instrumental in the fast growth of the sector. The expansion in the sector, besides boosting the country‟s industrial output, also provided significant direct and indirect employment opportunities. In the past years, there has been a high growth of more than 40 percent per year in the automobile market. The growth declined somewhat in 2008 and 2009 due mainly to a dip in demand because of rising prices and lease financing becoming expensive for the consumers. Pakistan Car Industry The first automobile plant was set up in May 1949 by General Motor & Sales Co. It was set up on an experimental basis, however grew into an assembly plant. Seeing such progress, three major auto manufacturers from the US collaborated with Pakistani business men to set up; Ali Automobiles to manufacture Ford Products in 1955, Haroon Industries to assemble Chrysler Dodge cars in 1956, Khandawalla Industries to assemble American Motor Products in 1962, and Mack Trucks Plant in 1963. However towards the end of the seventies all automobile assembly in Pakistan stopped, until 1983 when Pak Suzuki started manufacturing their vehicles in Pakistan. Further Toyota Indus Motors was set up in 1990, followed by Honda. -

Topline Market Review P

Pakistan Weekly January 12, 2018 REP‐057 Topline Market Review Gains erode as profit taking ensues KSE‐100 Index +1.0 % WoW; Weekly net FIPI US$26mn Topline Research Best Local Brokerage House [email protected] Brokers Poll 2011-14, 2016-17 Tel: +9221‐35303330, Ext: 133 Topline Securities, Pakistan www.jamapunji.pk Best Local Brokerage House 2015-16 Index gains 1% in outgoing week as profit taking ensues Market Weekly Data KSE Volume & Value KSE‐100 Index 42,933.72 (Shares mn) Volume Value (US$mn) 330 150 1‐Week Change (%) 1.0% 260 Market Cap (Rs tn) 8.9 106 190 1‐Week Change (%) 0.2% 63 Market Cap (US$ bn) 80.6 120 1‐Week Change (%) 0.2% 50 20 18 18 18 18 18 ‐ ‐ 1‐Week Avg. Daily Vol (shares mn) 276.4 ‐ ‐ ‐ n n n n n aa aa aa aa aa J J J J J ‐ ‐ 1‐Week Avg. Daily Value (Rs bn) 12.2 ‐ ‐ ‐ 9 8 1‐Week Avg. Daily Value (US$ mn) 110.2 10 11 12 Source: PSX Source: PSX Outgoing week saw the culmination of the Santa Clause rally which commenced on December 20, 2017 and peaked on Jan 10, 2018 with a net gain of 14%. Since then index has had red two sessions correcting 2%/697pts, which has trimmed weekly gains to 1%/410pts with the index closing the week at 42,934pts level. Going forward, equities maybe further pressured as agitation movement by opposition parties begin on Jan 17 to protest against the Model Town. PtiitiParticipation idimproved siifitlignificantlyasprofitswerebkdbooked, average volumes idincreased 30% WWWoW whilevalue rose 44%. -

Authorized Sales, Service & Spare Parts (3S) Dealers

16 Authorized Sales, Service & Spare Parts (3S) Dealers KARACHI LAHORE FAISALABAD Honda Shahrah-e-Faisal Honda City Sales Honda Faisalabad 13-Banglore Town, 75 B, Block L, Gulberg III, East Canal Road. Main Shahrah-e-Faisal Ferozepur Road. Tel: (041) 8731741-4 Tel: (021) 34527070, 34527373, Tel: (042) 35841100-06 Fax: (041) 8524029 34547113-6 Fax: (042) 35841107 Fax: (021) 34526758 Honda Chenab Honda Fort 123 JB Raja Wala Green View Colony. Honda Defence 32 Queens Road. Tel: (041) 2603449, 2603549 67/1, Korangi Road Near HINO Circle. Tel: (042) 36314162-3 5500897, 5508297 Tel: (021) 35805291-4 36309062-3, 36313925 Fax: (041) 2603349 Fax: (021) 35805294 Fax: (042) 36361076 PESHAWAR Honda Site Honda Point Honda North C 1, Main Manghopir Road, SITE. Main Defence Road. Main University Road. Tel: (021) 32577411-2, 32564926 Tel: (042) 35700994-5 Tel: (091) 5854901, 5700807, 5700808 32570301, 32569381 Fax: (042) 35700993 Fax: (091) 5854753 Fax: (021) 32577412, 32565056 Honda Canal Bank MIRPUR A.K. Honda South 13-B,Block-K, Johar Town, 1 B/1, Sec. 23, Korangi Industrial Area. Shoukat Khanaum Bypass. Honda Empire Tel: (021) 35050251-4 Tel: (042) 35300822-33, 7029360-61 Mian Muhammad Road, Fax: (021) 35064599 Fax: (042) 35300841 Quaid-e-Azam Chowk. Tel: (058274) 51501,1032701 Honda Drive In MULTAN Fax: (058274) 51500-3 118 C, Rashid Minhas Road. Honda Breeze Tel: (021) 34992832-7, 34992824 GUJRANWALA 63 Abdali Road. Fax: (021) 34992825 Tel: (061) 4588871-3 Honda Gujranwala 4548881, 4542862 G.T. Road. Honda Quaideen Fax: (061) 4588874 Tel: (055) 3893481-3 233-A-2, PECHS. -

Project Report Customer Satisfaction on Honda City

Project Report CUSTOMER SATISFACTION ON PREMIUM SEGMENT CARS WITH SPECIAL REFERENCE TO HONDA CITY 1 Acknowledgement A Good start leads to a Fine end. The ideal way to begin documenting this project work would be to extend my earnest gratitude to everyone who has encouraged, motivated and guided me to make a fine effort for successful completion of this project. I am very thankful to Siddhanta Mangal Kashyap, Head Marketing, Cogtest Service Pvt. Ltd for guiding me throughout the project. My sincere gratitude to the IMT- Gurgaon team for extending their co-operation for successful completion of my project. A final word of thanks goes to my friends and colleagues and everyone else who made this project possible. Your contributions have been most appreciated 2 PROJECT SUBMITTED IN PARTIAL FULFILLMENT FOR THE AWARD OF PGDM in MARKETING Declaration I hereby declare that this project report titled “Customer Satisfaction with Special reference to Premium segment car Honda City” submitted by me to Institute of Management Technology Ghaziabad is a bonafide work undertaken by me and it is not submitted to any other University or Institute for the Award of any degree diploma/certificate or published any time before. (Signature) 3 Index CHAPTER 1 Page no INTRODUCTION - 5 OBJECTIVES OF STUDY - 7 SCOPE AND LIMITATION OF STUDY - 9 RESEARCH METHODOLOGY - 11 CAR STATISTICS IN INDIA - 18 COMPANY PROFILE - 23 COMPETITORS PROFILE - 37 CHAPTER 2 FINDING AND ANALYSIS - 46 CONCLUSION - 59 FINDINGS & SUGGESTION - 61 BIBLIOGRAPHY - 62 4 Introduction The automobile industry today is the most lucrative industry. Due to the increase in disposable income in both rural and urban sector and easy finance being provided by all the financial institutions, the passenger car sales have increased. -

The Automotive Sector in Pakistan

Final Report THE AUTOMOTIVE SECTOR IN PAKISTAN TABLE OF CONTENTS LIST OF ACRONYMS 1 EXECUTIVE SUMMARY 4 CHAPTER 1: INTRODUCTION 9 1.1. Terms of Reference 9 1.2. History of the Sector 10 1.3. Review of Literature 12 CHAPTER 2: THE AUTOMOTIVE SECTOR 16 2.1. Coverage 16 2.2. Sizing of the Sector 16 2.3. Contribution To The Economy 26 2.4. Demand Analysis 32 CHAPTER 3: POLICY AND REGULATORY FRAMEWORK 34 3.1. TRIMS 34 3.2. Investment Policy 36 3.3. Trade Policies 38 3.4. Tariff Policy 39 3.5. Auto Industry Development Programme 43 3.6. Policy and Standards 44 CHAPTER 4: EXTENT OF EFFECTIVE PROTECTION 45 4.1. Methodology 45 4.2. Results 46 4.3. Recommendations on Tariff Reform 47 CHAPTER 5: ASSESSMENT OF COMPETITION IN THE SECTOR 52 5.1. Methodology for Assessing Degree of Competition 52 5.2. Measure of Extent of Competition 53 5.3. Assessment of Competition in the Automotive Sector 54 CHAPTER 6: PROFILE OF THE SAMPLE OF VENDORS 58 6.1. Objectives of the Survey 58 6.2. The Sample 58 6.3. Legal Status 61 ii 6.4. Membership of Associations 61 6.5. Investment and Capacity 62 6.6. Turnover 63 6.7. Employment 63 6.8. Cost Structure 64 6.9. Gross Profit and Value Added 64 CHAPTER 7: KEY ISSUES IN THE VENDING INDUSTRY 66 7.1. Impact of Tariff Protection 66 7.2. Extent of Competition 70 7.3. Degree of Competitiveness 71 7.4. Factors Influencing Growth 71 7.5. -

Companies Listed On

Companies Listed on KSE SYMBOL COMPANY AABS AL-Abbas Sugur AACIL Al-Abbas CementXR AASM AL-Abid Silk AASML Al-Asif Sugar AATM Ali Asghar ABL Allied Bank Limited ABLTFC Allied Bank (TFC) ABOT Abbott (Lab) ABSON Abson Ind. ACBL Askari Bank ACBL-MAR ACBL-MAR ACCM Accord Tex. ACPL Attock Cement ADAMS Adam SugarXD ADMM Artistic Denim ADOS Ados Pakistan ADPP Adil Polyprop. ADTM Adil Text. AGIC Ask.Gen.Insurance AGIL Agriautos Ind. AGTL AL-Ghazi AHL Arif Habib Limited AHSL Arif Habib Sec. AHSM Ahmed Spining AHTM Ahmed Hassan AIBL Asset Inv.Bank AICL Adamjee Ins. AJTM Al-Jadeed Tex AKDCL AKD Capital Ltd AKDITF AKD Index AKGL AL-Khair Gadoon ALFT Alif Tex. ALICO American Life ALNRS AL-Noor SugerXD ALQT AL-Qadir Tex ALTN Altern Energy ALWIN Allwin Engin. AMAT Amazai Tex. AMFL Amin Fabrics AMMF AL-Meezan Mutual AMSL AL-Mal Sec. AMZV AMZ Ventures ANL Azgard Nine ANLCPS Azg Con.P.8.95 Perc.XD ANLNCPS AzgN.ConP.8.95 Perc.XD ANLPS Azgard (Pref)XD ANLTFC Azgard Nine(TFC) ANNT Annoor Tex. ANSS Ansari Sugar APL Attock Petroleum APOT Apollo Tex. APXM Apex Fabrics AQTM Al-Qaim Tex. ARM Allied Rental Mod. ARPAK Arpak Int. ARUJ Aruj Garments ASFL Asian Stocks ASHT Ashfaq Textile ASIC Asia Ins. ASKL Askari Leasing ASML Amin Sp. ASMLRAL Amin Sp.(RAL) ASTM Asim Textile ATBA Atlas Battery ATBL Atlas Bank Ltd. ATFF Atlas Fund of Funds ATIL Atlas Insurance ATLH Atlas Honda ATRL Attock Refinery AUBC Automotive Battery AWAT Awan Textile AWTX Allawasaya AYTM Ayesha Textile AYZT Ayaz Textile AZAMT Azam Tex AZLM AL-Zamin Mod. -

India-Pakistan Trade: Perspectives from the Automobile Sector in Pakistan

Working Paper 293 India-Pakistan Trade: Perspectives from the Automobile Sector in Pakistan Vaqar Ahmed Samavia Batool January 2015 1 INDIAN COUNCIL FOR RESEARCH ON INTERNATIONAL ECONOMIC RELATIONS Table of Contents List of Abbreviations ................................................................................................................... iii Abstract ......................................................................................................................................... iv 1. Introduction ........................................................................................................................... 1 2. Methodology and Data .......................................................................................................... 2 3. Automobile Industry in Pakistan ......................................................................................... 3 3.1 Evolution and Key Players............................................................................................ 4 3.2 Structure of the Industry ............................................................................................... 6 3.3 Production structure ..................................................................................................... 7 3.4 Market Structure ........................................................................................................... 8 4. Automobile Trade of Pakistan............................................................................................ 10 4.1 Import -

Financial Analysis of Toyota Indus Motor Company

Financial Analysis of Toyota Indus Motor Company 2017 Financial Analysis of Toyota Indus Motor Company Financial Year 2011-2016 Ayesha Majid Lahore School of economics 5/1/2017 Financial Analysis of Toyota Indus Motor Company i Table of Contents Preamble .................................................................................................................... 1 Categories of Financial Ratios Analysed ................................................................ 1 Limitations .............................................................................................................. 2 Toyota Indus Motors................................................................................................... 3 Company Profile ..................................................................................................... 3 Financial Profile ...................................................................................................... 3 Introduction ............................................................................................................. 4 Mission Statement ............................................................................................... 5 Vision Statement ................................................................................................. 5 Slogan ................................................................................................................. 5 Quote Summary as on 1st May 2017 .......................................................................... 6