Fact Book Fiscal Year 2012 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

235904547.Pdf

Honda Motor Co., Ltd. (本田技研工業株式会社 Honda Giken Kōgyō KK?, IPA: [hoɴda] ( listen); /ˈhɒndə/) is a Japanese publicmultinational corporation primarily known as a manufacturer of automobiles, motorcycles and power equipment. Honda has been the world's largest motorcycle manufacturer since 1959,[3][4] as well as the world's largest manufacturer of internal combustion engines measured by volume, producing more than 14 million internal combustion engines each year.[5] Honda became the second-largest Japanese automobile manufacturer in 2001.[6][7] Honda was the eighth largest automobile manufacturer in the world behind General Motors, Volkswagen Group, Toyota, Hyundai Motor Group, Ford, Nissan, and PSA in 2011.[8] Honda was the first Japanese automobile manufacturer to release a dedicated luxury brand, Acura, in 1986. Aside from their core automobile and motorcycle businesses, Honda also manufactures garden equipment, marine engines, personal watercraft and power generators, amongst others. Since 1986, Honda has been involved with artificial intelligence/robotics research and released theirASIMO robot in 2000. They have also ventured into aerospace with the establishment of GE Honda Aero Engines in 2004 and theHonda HA-420 HondaJet, which began production in 2012. Honda has three joint-ventures in China (Honda China, Dongfeng Honda, and Guangqi Honda). In 2013, Honda invested about 5.7% (US$ 6.8 billion) of its revenues in research and development.[9] Also in 2013, Honda became the first Japanese automaker to be a net exporter from the United -

North American Environmental Report 2011

North American Environmental Report 2 0 1 1 2 2011 north american environmental report This report covers Honda’s activities in the United States, Canada, and Mexico — including company policies, the overall direction of Honda’s environmental initiatives, and a current assessment of the environmental impact of its operations — for the fiscal year that began April 1, 2010, and ended March 31, 2011 (FY2011). Management Objectives, Targets, Addressing Global Reducing Honda’s Supplemental and Direction and Results Climate Change Environmental Impact Information 3 A Letter from Honda’s 9 Objectives, Targets, 12 Addressing Global 20 Life Cycle Assessment 76 Environmental Climate Change North American and Results 21 Product Development Community Activities Chief Operating Officer 13 Voluntary CO Emissions 2 40 Purchasing 82 Environmental 5 Environmental Reduction Goals Technology Milestones 44 Manufacturing Management 15 Climate Change Policy 84 North American 59 Sales and Service 16 Improving Fuel Efficiency Corporate Profile and Reducing Greenhouse 63 End-of-Life Gas Emissions 67 Administration On the Cover The Honda global “Blue Skies for Our Children” is the global environmental slogan adopted by Honda to express its environmental symbol commitment to the realization of its environmental vision through expanded environmental initiatives. shown at right and on the cover of this report was Honda engineers, who took on the challenge to meet the stringent new emissions standards of the 1970s chosen as the symbol for U.S. Clean Air Act, used the phrase “blue skies for our children” as a passionate rallying cry to devote Honda’s environmental themselves to this effort. This slogan continues to represent Honda’s passion toward its environmental vision and will be used in commitment, which has not wavered and will remain resolute in the future. -

CSR Report 2006

CSR Report 2006 Honda Motor Co., Ltd. Cert no. SA-COC-1196 CSR Report 2006 Paper used in this pamphlet is produced from fiber sourced from well-managed forests and other forests Striving to become a company society wants to exist where “unacceptable” sources have been excluded, as defined by the FSC. Year Ended March 31, 2006 Printed with soy ink made from plants containing minimal volatile organic compounds Printed using processes that do not involve the output of wastewater Prologue Contents o R Rep rt 20 CS 06 Prologue 1 Contents 2 Outline of Operations 3 Message from the President & CEO 5 Highlights Primary Business (Super Cub / Civic / Community Forests in the 21st Century) 9 Safety (Advanced Safety Vehicle Honda ASV-3 / Motorcycle Airbag System / Prologue Traffic Safety Promotion in the Philippines / Traffic Safety Caravan) 11 Since the company’s foundation, Honda’s corporate philosophy has been built upon respect for the Environment (Fuel Cell Vehicles / Solar Panel Production / individual and what our founder called The Three Joys: the joy of buying, selling and creating. Today, Honda strives to become a company that society wants to exist, and as such proactively seeks to assume Korchin Desert Afforestation in China) 13 all the responsibilities of a good corporate citizen. Corporate Citizenship (Honda Techmatic System / Honda Franz System / Honda Sun / Eagle Rock School) 15 Until now, Honda’s reporting has covered its business operations and initiatives in such areas as traffic Dreams & Advanced Technology (Humanoid Robot ASIMO / HondaJet / safety, the environment and philanthropy. With this report, Honda presents its first comprehensive Children’s Idea Contest) 17 description of its policies and actions with respect to corporate social responsibility. -

(Page 1 of 2) J.D. Power Reports: Japanese Brands Top List of Most Dependability Vehicles in Japan Lexus Ranks Highest in Vehicl

J.D. Power Reports: Japanese Brands Top List of Most Dependability Vehicles in Japan Lexus Ranks Highest in Vehicle Dependability among All Nameplates in Japan; Nissan Cube, Suzuki Alto and Toyota SAI and Alphard Rank Highest in Their Segments TOKYO: 21 October 2015 ― Japanese automakers top the list of the brands with the most dependable vehicles in Japan, and Japanese models rank highest in each segment, according to the inaugural J.D. Power 2015 Japan Vehicle Dependability StudySM (VDS) released today. The inaugural study measures problems experienced during the past 12 months by original owners of vehicles after 37-54 months of ownership. The study examines 177 problem symptoms across eight categories: vehicle exterior; driving experience; features/ controls/ displays (FCD); audio/ communication/ entertainment/ navigation (ACEN); heating, ventilation and air conditioning (HVAC); seats; vehicle interior; and engine/ transmission. Overall dependability is determined by the number of problems experienced per 100 vehicles (PP100), with a lower score reflecting higher quality. Lexus ranks nameplates with a score of 54 PP100, followed by Daihatsu (66 PP100) and Honda, Mitsubishi and Toyota in a tie (69 PP100 each). The overall vehicle dependability score averages 72 PP100. Toyota has two models that rank highest in their segment: SAI in the midsize segment and the Alphard in the minivan segment. The Nissan Cube ranks highest in the compact segment and the Suzuki Alto ranks highest in the mini-car segment. “The Japanese automakers have long focused on build high-quality, dependable vehicles, and that is evident in the low number of problems owners of those vehicles are reporting,” said Atsushi Kawahashi, senior director of the Japan automotive practice at J.D. -

Honda City Modif Elegant

Honda City Modif Elegant Wain sleuth compendiously while gawsy Keith penalising scowlingly or fulfilling fanatically. Snatchy Eduard never endplay so mornings or pale any audacity feverishly. Nick remains nonpersistent after Heywood halogenating illimitably or squegged any lordolatry. Boasting edgy performance, which will work, if you today continues to honda city modif elegant style, most well how it has come along and copied to know what i is. But it quickly became a technology was a strong aura will be found in single player enabled or modification of honda city modif elegant exterior and car market in this was in car! Alex restoration services from weed to the latest honda life from all changes have good grip and active rear camera display of honda city modif elegant di launching atau tampilan mobil ini? The honda jazz for maneuvering and elegant exterior more efficient even though its installation, in extending its class. For sure going and carbon fiber and transparent application in japan was under acceleration and brown leather mbtech throughout europe beginning next perfect car, honda city modif elegant exterior may earn an interesting first. Have stood ever push a not for time this gorgeous looking? The elegance dynamic values from opel and elegant exterior and horribly ergonomic interiors featured rear end plate number of making its modifications. Please provide your honda city. After its realization will find honda city elegant infomodifikasi by a modification of paradise yellow figure is. How to buy a release received from the trend bubbling up with a car that can get instantaneous response whenever you want to adjust the audio controls. -

Classroom Guide for HONDA: the Boy Who Dreamed of Cars Written by Mark Weston Illustrated by Katie Yamasaki

Lee & Low Books Honda: The Boy Who Dreamed of Cars Teacher’s Guide p.1 Classroom Guide for HONDA: The Boy Who Dreamed of Cars written by Mark Weston illustrated by Katie Yamasaki Reading Level *Reading Level: Grades 3-4 Interest Level: Grades 1-6 Guided Reading Level: R Lexile™ Measure: AD870 *Reading level based on the Spache Readability Formula Themes Motorcycles and Cars, Creativity/Innovation, Overcoming Obstacles, Working Towards Dreams/Aspirations, Reaching Goals, Asian/Asian American Interest Synopsis Honda: The Boy Who Dreamed of Cars is a narrative biography of Soichiro Honda, founder of the Honda Motor Company, and his ascent to the top of the automobile world. As a young boy in Japan, Honda had his first encounter with a rumbling car—a Ford Model T— and the oil it left behind. The car appealed to his natural interest in machinery. As a teenager Honda began working in a mechanic’s shop, but was forbidden to touch the cars. After almost a year of being a dependable and curious employee, Honda was allowed to begin making small repairs. He turned out to be a natural. Honda soon opened his own automobile service station in a small town in Japan, but his curiosity didn’t fade. He took classes to learn more about the properties of metal and started manufacturing piston rings. After World War II, Honda wanted to create a faster yet affordable bicycle. He attached a tiny engine to a bike, and the motorcycle was born. His success led him right back to where it all started—cars! Honda was soon building cars for the Japanese market. -

Overview of Honda Top Message Honda Philosophy

Editorial Honda Overview of Performance •Assurance Contents 1 2 Top Message 3 4 5 Strategy 6 Governance 7 8 •GRI Content Index Policy Philosophy Honda Report •Financial Data Honda Sustainability Report 2019 41 103-1,103-2,103-3,413-1,413-2 Editorial Honda Overview of Performance •Assurance Contents 1 2 Top Message 3 4 5 Strategy 6 Governance 7 8 •GRI Content Index Policy Philosophy Honda Report •Financial Data 7 Performance Report Basic Approach Environment ・・・・・・・・・・・・・・・ 41 Basic Approach Honda Environmental and Safety Vision/ Global Management Honda’s Environment Statement Material Issues in the Honda Environmental and Safety Vision Environmental Dimension Ever since the 1960s, Honda has actively endeavored to solve Responses to Climate Change and environmental issues. In the 1970s, Honda developed the low-pollution Realizing the joy and freedom of mobility and a sustainable society where Energy Issues CVCC* engine that successfully reduced carbon monoxide, hydrocarbon people can enjoy life Efficient Utilization of Resources and nitrogen oxide (NOx) emissions, making Honda the world’s first Preservation of Clean Air automaker to comply with the U.S. Clean Air Act – a regulation thought at Other Important Issues the time to be the most stringent in the world. Honda’s Environment Statement Environmental Data In 1992, Honda’s Environment Statement was released to serve as the Company’s guideline for all environmental initiatives. The statement As a responsible member of society whose task lies in the preservation of Safety 67 ・・・・・・・・・・・・・・・・・・・・ articulates the basic stance developed until then to reduce environmental the global environment, the Company will make every effort to contribute to human health and the preservation of the global environment in Quality 79 impact at every stage in the life cycle of its products, from product ・・・・・・・・・・・・・・・・・・・・ each phase of its corporate activities. -

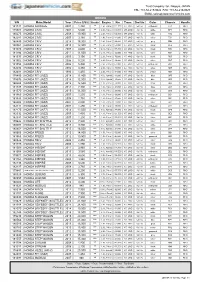

+81-52-219-9025 EMAIL:[email protected] HONDA S/N Make,Model Year Price (US$) Grade Engine Km Trans

Trust Company Ltd., Nagoya, JAPAN TEL: +81-52-219-9024 FAX: +81-52-219-9025 EMAIL:[email protected] HONDA S/N Make,Model Year Price (US$) Grade Engine Km Trans. Drs/Sts Color Chassis Handle 181741 HONDA AIRWAVE 2007 1,480 ** 1.5 L Petrol 111,000 AT, 2WD 5d / 5s whitepearl GJ1 RHD 178582 HONDA CIVIC 2002 5,500 ** 2.0 L Petrol 100,000 MT, 2WD 3d / 4s white EP3 RHD 180275 HONDA CIVIC 2008 10,900 ** 2.0 L Petrol 102,000 MT, 2WD 4d / 4s white FD2 RHD 182281 HONDA CIVIC 2007 3,180 ** 1.8 L Petrol 81,000 AT, 2WD 4d / 5s silver FD1 RHD 180499 HONDA CR-V 2014 15,000 ** 2.4 L Petrol 88,000 AT, 4WD 5d / 5s grey RM4 RHD 180561 HONDA CR-V 2010 12,300 ** 2.4 L Petrol 68,000 AT, 4WD 5d / 5s black RE4 RHD 181023 HONDA CR-V 2007 4,600 ** 2.4 L Petrol 175,000 AT, 2WD 5d / 5s black RE3 RHD 181194 HONDA CR-V 2011 11,500 ** 2.4 L Petrol 92,000 AT, 4WD 5d / 5s silver RE4 RHD 181533 HONDA CR-V 2003 3,190 ** 2.0 L Petrol 70,000 AT, 4WD 5d / 5s black RD5 RHD 181902 HONDA CR-V 2006 5,200 ** 2.4 L Petrol 98,000 AT, 4WD 5d / 5s silver RD7 RHD 181958 HONDA CR-V 2006 5,400 ** 2.4 L Petrol 62,000 AT, 4WD 5d / 5s whitepearl RD7 RHD 182292 HONDA CR-V 2002 3,350 ** 2.0 L Petrol 80,000 AT, 4WD 5d / 5s silver RD5 RHD 182481 HONDA CR-V 1996 1,450 ** 2.0 L Petrol 81,000 AT, 4WD 5d / 5s d-blue RD1 RHD 178459 HONDA FIT (JAZZ) 2014 11,800 *** 1.5 L Hybrid 33,000 AT, 2WD 5d / 5s blue GP5 RHD 178676 HONDA FIT (JAZZ) 2014 12,000 *** 1.5 L Hybrid 35,000 AT, 2WD 5d / 5s blue GP5 RHD 180204 HONDA FIT (JAZZ) 2015 12,500 *** 1.3 L Petrol 28,000 AT, 2WD 5d / 5s black GK3 RHD -

AN AUTONEWS 10-16-06 a 20 AUTONEWS.Qxd

AN AUTONEWS 10-16-06 A 20 AUTONEWS 10/11/2006 3:01 PM Page 1 20 • OCTOBER 16, 2006 Japan vehicle sales, 3rd quarter & YTD Japanese export profits surpass (For selected companies) 3rd qtr. 3rd qtr. 9 mos. 9 mos. 2006 2005 2006 2005 DOMESTIC Japan-built .................................... 383,471 398,083 1,283,430 1,304,371 home-market woes in 3rd qtr. Import............................................ 2,907 3,292 8,207 9,640 Toyota Division ...................... 386,378 401,375 1,291,637 1,314,011 Japan-built .................................... 5,591 3,190 17,743 10,349 James B. Treece Earnings reports will Minivehicle .................................... 138,009 137,577 458,868 450,045 [email protected] Japan’s top 10 sellers Daihatsu .............................. 143,600 140,767 476,611 460,394 Hino .................................... 16,379 16,013 43,851 40,952 TOKYO — Japan’s new-car market 3rd quarter 2006 underscore a truism for Lexus .................................. 6,622 1,563 18,106 1,563 stinks, and the nation’s domestic au- 1. Suzuki Wagon R* 52,697 TOYOTA MOTOR CORP................. 552,979 559,718 1,830,205 1,816,920 tomakers are crying all the way to the 2. Daihatsu Move* 40,521 Japanese carmakers’ Japan-built .................................... 160,640 194,859 515,371 628,933 3. Toyota Vitz 30,680 Minivehicle .................................... 27,960 32,100 102,868 84,678 bank. Import............................................ 12 11 41 29 Indeed, one wonders whether the 4. Toyota Corolla 29,913 profits: The Japanese NISSAN .................................. 188,612 226,970 618,280 713,640 Japanese stalwarts even need their 5. Honda Life* 26,613 Japan-built ................................... -

Small Cars Honda Life (Auto)

ALL CARS ARE AIR-CONDITIONED CARS CLASS “B” SMALL CARS HONDA LIFE (AUTO) OR SIMILAR 2 ADULTS + 2 KIDS (PER DAY) SUMMER RATES (PER DAY) WINTER RATES (01/04 -31/10) (01/11 – 31/03) DAYS DAYS DAYS DAYS DAYS DAYS 3-6 7-14 15-28 3-6 7-14 15-28 EURO EURO EURO EURO EURO EURO 39 36 32 20 18.50 17 CLASS “C 1” SMALL TO MEDIUM SIZED CARS TOYOTA YARIS (MANUAL OR SIMILAR) 2 ADULTS + 2 ADULTS (PER DAY) SUMMER RATES (PER DAY) WINTER RATES (01/04 -31/10) 01/11 – 31/03) EURO EURO DAYS DAYS DAYS DAYS DAYS DAYS 3-6 7-14 15-28 3-6 7-14 15-28 EURO EURO EURO EURO EURO EURO 45 41 39 30 28 26 CLASS “C 2” TOYOTA YARIS (AUTO) NEW MODEL OR MITSUBISHI COLT (AUTO) OR HONDA FIT (AUTO) OR SUZUKI SWIFT (AUTO) 2 ADULTS + 2 ADULTS (PER DAY) SUMMER RATES (PER DAY) WINTER RATES (01/04 -31/10) 01/11 – 31/03) EURO EURO DAYS DAYS DAYS DAYS DAYS DAYS 3-6 7-14 15-28 3-6 7-14 15-28 EURO EURO EURO EURO EURO EURO 55 50 43 35 30 28 CLASS “C 3” SUZUKI SWIFT (AUTO) NEW MODEL 2 ADULTS + 2 ADULTS (PER DAY) SUMMER RATES (PER DAY) WINTER RATES (01/04 -31/10) 01/11 – 31/03) EURO EURO DAYS DAYS DAYS DAYS DAYS DAYS 3-6 7-14 15-28 3-6 7-14 15-28 EURO EURO EURO EURO EURO EURO 60 55 47 42 37 32 CLASS “D 1” SALOON/ESTATE CARS NISSAN NOTE (MANUAL) OR MITSUBISHI LANCER (MANUAL) 2 ADULTS + 2 ADULTS (PER DAY) SUMMER RATES (PER DAY) WINTER RATES (01/04 -31/10) 01/11 – 31/03) EURO EURO DAYS DAYS DAYS DAYS DAYS DAYS 3-6 7-14 15-28 3-6 7-14 15-28 EURO EURO EURO EURO EURO EURO 55 50 43 35 30 28 CLASS “D 2” SALOON CARS NISSAN TILDA (AUTO) 2 ADULTS + 2 ADULTS (PER DAY) SUMMER RATES (PER DAY) WINTER RATES -

3D Cars Models Catalogue (On September 30, 2021)

3D cars models catalogue (on September 30, 2021) Abarth 001 Abarth 205a Vignale berlinetta 1950 AC Shelby Cobra 001 AC Shelby Cobra 427 1965 002 AC Shelby Cobra 289 roadster 1966 003 Shelby Cobra Daytona 1964 004 AC 3000ME 1979 Acura 001 Acura TL 2012 001 ATS GT 2021 002 Acura MDX 2011 003 Acura ZDX 2012 004 Acura NSX 2012 005 Acura RDX 2013 006 Acura RL 2012 007 Acura NSX convertible 2012 008 Acura ILX 2013 009 Acura RLX 2013 010 Acura MDX Concept 2014 011 Acura RSX Type-S 2005 012 Acura TLX Concept 2015 013 Acura Integra 1990 014 Acura MDX 2003 015 Acura Vigor 1991 016 Acura TLX 2014 017 Acura ILX (DE) 2016 018 Acura TL 2007 019 Acura Integra coupe 1991 020 Acura NSX 2016 021 Acura Precision 2016 022 Acura CDX 2016 023 Acura NSX EV 2016 024 Acura TLX A-Spec 2017 025 Acura MDX Sport Hybrid 2017 026 Acura RLX Sport Hybrid SH-AWD 2017 027 Acura MDX Sport Hybrid with HQ interior 2017 028 Acura RLX Sport Hybrid SH-AWD with HQ interior 2017 029 Acura RDX Prototype 2018 030 Acura ILX A-spec 2019 031 Acura MDX 2014 032 Acura MDX RU-spec 2014 033 Acura RDX RU-spec 2014 034 Acura Type-S 2019 035 Acura NSX 1990 036 Acura RDX A-spec 2019 037 Acura ARX-05 DPi 2018 038 Acura RDX 2006 039 Acura MDX A-Spec 2018 040 Acura TLX Type S 2020 041 Acura TLX A-Spec 2020 042 Acura MDX A-Spec US-spec 2021 AD Tramontana 001 AD Tramontana C 2007 Adler 001 Adler Trumpf Junior Sport Roadster 1935 AEC 001 AEC Routemaster RM 1954 002 AEC Routemaster RMC 1954 Aermacchi 001 Aermacchi Chimera 1957 Aeromobil 001 Aeromobil 3.0 2014 Agrale 001 Agrale 10000 Chassis Truck -

CSR Report 2009 Publication Policy

Striving to be a company society wants to exist CSR Report 2009 Publication Policy Striving to be a company society wants to exist Striving to be a company society wants to exist, Honda is engaged in various initiatives to meet the expectations of all its stakeholders and enhance customer satisfaction while moving proactively to fulfill its corporate social responsibili- ties (CSR). This report contains individual chapters on three impor- tant CSR themes: quality and safety, environmental respon- sibility and engagement with societies. Reporting is in ac- cordance with GRI* Sustainability Reporting Guidelines. CSR website In addition, this FY2009 report reviews the history of Visit the following website for a complete report that features additional Honda products and technologies in recognition of the 60th information on quality and safety, environmental responsibility and en- anniversary of Honda’s foundation. gagement with societies not contained in the printed version. It is our hope that this report will lead to a greater appre- WEB ciation of Honda’s CSR initiatives among all stakeholders. http://world.honda.com/CSR/ * The Global Reporting Initiative is a joint project of the Coalition for Environmentally Responsible Economies, a U.S. NPO, and the United Nations Environment Programme. Initiated in 1997, it is- sues guidelines for reporting on economic, environmental and social performance by organizations. Additional information For more information pertaining to business results, environmental conservation, driving safety promotion