JCR Affirmed J-1+ Rating on CP of Hankyu Hanshin Holdings

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

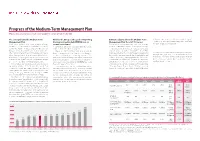

Progress of the Medium-Term Management Plan Making Steady Progress to Reach Our Management Goals Ahead of Schedule

Interview with the President Progress of the Medium-Term Management Plan Making steady progress to reach our management goals ahead of schedule The concept behind the Medium-Term Why has the Group set the goal of improving Estimates adjusted from the Medium-Term fiscal 2016 is expected to exceed the previous plan’s target of Management Plan the interest-bearing debt/EBITDA ratio to Management Plan: fiscal 2016 forecast 7.0 times to 6.8 times. We are steadily taking steps to reach these On the occasion of the management integration of Hankyu around seven times? Current estimates indicate that we will achieve our goals slightly management goals as early as possible. and Hanshin, the Group formulated and announced the six- To answer this question, I will once again explain the manage- ahead of schedule and forecasts have been adjusted accordingly. year Hankyu Hanshin Holdings Group 2007 Medium-Term ment indicators that the Group is aiming for. Operating income for the fiscal 2016 target year is forecast to Management Plan (fiscal 2008–fiscal 2013), for which we estab- The Group’s mainstay railway and real estate leasing surpass the previous plan (¥83.0 billion) by ¥2.0 billion to ¥85.0 Over six years have passed since the management integration lished yearly adjusted estimates and implemented initiatives to businesses generate stable cash flows. Yet, these businesses billion, reflecting currently robust railway operation revenue and of Hankyu Holdings, Inc. and Hanshin Electric Railway Co., Ltd. in achieve the plan’s targets. This plan was intended to clarify the are characterized by the need to own large amounts of fixed higher rental income mainly from the Umeda Hankyu Building. -

List of Employment for Undergraduate Students in 2014-2016

List of employment for Undergraduate stduents in 2014-2016 As of May 1st, 2017 Construction/Real estate business ITOCHU Urban Community/AIBLE INC./Okuraya homes/Okumura corporation/Kinoshita Group/Kyoritsu maintenance/ Kyowanissei/Kudo corporation/Shonan Station Building, Shonan Misawa Homes/Starts Corporation/ Sumitomo Real Estate/Sumitomo forestry home service/Sekisui House/Sekiwa Real Estate/Daikin Air Techno/ Taiseioncho/Takara Leben/ Tokyu Livable/Tokyo Building, Tokyo Reiki Inc./Nishimatsu Construction/Nihon Housing, Housecom/PanaHome/Misawa Homes Shizuoka/ Misawa Homes Tokyo/Mitsui Fudosan Realty/LUMINE Manufacture ADVANEX/Alps Electric/ITO EN/FDK/Kanebo Cosmetics/kawamura Electric/Kewpie/Kyowa Hakko Kirin/Cross Company/Koike sanso Kogyo/ Korg, Sanwa Tekki/JFE Shoji Coil Center/Shindengen Electric Manufacturing/SUZUKI Motor/ThreeBond Group/Daiwa Industries Takara Standard/Tachikawa Corporation/tanico/Chugai Mining/THK/DNP Multi Print/DISCO/ACCRETECH/Torii Pharmaceutical Triumph International Japan/NAKAMURAYA/Niigata Power Systems/Nifco/Nihon Pharmaceutical/NIWAKA/NOEVIR/Punch Industry P&G Maxfactor/Hitachi Construction Machinery Japan/Beyonz/fabrica communications/Furukawa Battery/HOYA/MEIKO/Meidensha HIROTA/RENOWN/YKKAP/Wacol Holdings Transportation ITOCHU Logistics/AIRDO/Odakyu Electric Railway/Kanagawa Chuo Kotsu/K.R.S./Kokusai motorcars/Sakai Moving Service/ Sagawa Global Logistics/SANKYU/J-AIR/JAL Express/JAL Cargo Service/JAL Ground Service/JAL SKY/All Nippon Airways/DNP logistics/ Nippon Konpo Unyu Soko/Nippon Express/Japan -

OSAKA MEANS BUSINESS Some of Osaka's Biggest Companies Have Joined Forces in a Bid to Create a New Commercial District to Take on Tokyo's

Insight OSAKA MEANS BUSINESS Some of Osaka's biggest companies have joined forces in a bid to create a new commercial district to take on Tokyo's. Mitchell Labiak reports alk across Umeda’s business in Osaka, which is why 2.5 million people to the area designated as one 59-acre main footbridge the rst train station in the city every day. Only one other area business improvement district Wand pretty much was built here in the 1870s. of Japan boasts a higher footfall: (BID), which would be one of the everything you see, from Commerce in Umeda grew so Shinjuku, Tokyo. rst public-private partnerships department stores to o ces, quickly that by 1910, the old Hankyu Hanshin, which under the new BID regulations from hotels to six of the district's station had been demolished and already generates more than introduced in 2018. seven train stations, is owned by replaced with a bigger one. 50% of its ¥224.7bn (£1.68bn) Norio Mizuno, manager for Bay one company: Hankyu Hanshin. Fast-forward 100 years and annual real estate revenue in Area development at the city of The business district in Japan's the formation of the Umeda Umeda, believes the area has Osaka government, says that second city, Osaka, is already an Area Management Alliance in the capacity to handle far more such is the momentum behind impressive sight thanks to the 2009 between Hankyu Hanshin, tra c. It says that two more train the scheme that even if there brilliantly futuristic Grand Front Japan Railways (JR) and the joint stations – a JR station that will is a change in government, it is Osaka – a 19-acre mixed-use venture company that owns connect directly to the airport unlikely to hamper progress. -

Notice of Convocation of the 12Th Annual General Meeting of Shareholders

These documents are partial translations of the Japanese originals for reference purposes only. In the event of any discrepancy between these translated documents and the Japanese originals, the originals shall prevail. The Company assumes no responsibility for this translation or for direct, indirect or any other forms of damages arising from the translations. (Securities Code: 8714) June 1, 2021 To Shareholders with Voting Rights: Atsushi Ukawa Representative Director, President and CEO Senshu Ikeda Holdings, Inc. 18-14, Chayamachi, Kita-ku, Osaka, Japan NOTICE OF CONVOCATION OF THE 12TH ANNUAL GENERAL MEETING OF SHAREHOLDERS You are cordially notified of the 12th Annual General Meeting of Shareholders of Senshu Ikeda Holdings, Inc. (the “Company”). The meeting will be held for the purposes described below. If you do not attend the meeting, you may still exercise your voting rights in writing or electronically (on the Internet). Please review the Reference Documents for the General Meeting of Shareholders described hereinafter, then follow the methods described on pages 3 to 6 to exercise your voting rights by 5:40 p.m., on Tuesday, June 22, 2021, Japan time. The Annual General Meeting of Shareholders will be broadcast live via the Internet. For details, please refer to page 7. Viewing the live webcast over the Internet is not deemed attendance of the General Meeting of Shareholders under the Companies Act. Accordingly, if you participate in the meeting via the Internet, you will not be able to ask questions, exercise your voting rights, or propose a motion, which is permitted to the shareholders attending the General Meetings of Shareholders. -

The Japanese Real Estate Investment Market 2018

The Japanese Real Estate Investment Market 2018 November 2018 Otemachi Financial City Grand Cube, 1-9-2 Otemachi, Chiyoda-ku, Tokyo 100-0004, Japan Population movements in Japan Macro fundamentals of Japan Overview of real estate investment market in Japan Office market Residential market Retail property market Logistics property market Hotel market Real estate investment products Copyright(C) Nomura Research Institute, Ltd. All rights reserved. Population movements in Japan In 2015, depopulation was observed for the first time in Japan, based on the national census. The decline in number of households was not confirmed by the national census in 2015; hence, the rise is expected to continue. The population of people 65 years or older is expected to level off in 2025 and head downwards from 2040. Population and households in Japan Population Households ← Actual Forecast → (thousand) (thousand) 140,000 70,000 120,000 60,000 100,000 50,000 80,000 40,000 65- 15-64 60,000 30,000 0-14 households 40,000 20,000 20,000 10,000 0 0 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050 2055 2060 2065 Source: National Institution of Population and Social Security Research and MIC “Population Census” Note 1: Population forecast is based on the data of population census in 2015. Note 2: The solid line shows the actual households based on the population census and dotted line shows the predicted households based on the population census in 2010. Note 3: Median-fertility (median-mortality) projection is used in population and household forecast. -

Meet 65,000 Buyers in Hotel, Restaurant and Food Service Industry

Japan’s Largest Exhibition for Hospitality Standard Booth (Space ONLY) Special Trade show for Food-service, Accommodation & Leisure industries 1 booth=9㎡ (W2,970mm× D2,970mm× H2,700mm) Early bird 2700㎜ Early bird discount discount 47 [Until Jul. 31] 378,000 JPY (tax incl.) 75,600 Final application JPY No carpet [Until Sep. 28] 453,600 JPY (tax incl.) 2970㎜ 2970㎜ Option: Package Plan Trade show for Food-service & Home delivery 40 1 booth with Package W2,970×D2,970×H2,700 unit/ mm Company name Outlet 507,600 JPY (Early bird) Price Fascia board 583,200 JPY (Final Application) (incl. Construction fee & 8% consumption tax) 1. Fascia board + Company name 5-3 Rental equipment (Choose 3 items) Trade show for Kitchen equipment 2. Outlet (100V, Single phase) J. Rectangle table (Choose 1 item) 3. Carpet (Choose your own color) K. Wall shelf (x 1 unit) 4. Meeting set L. White cloth (2200x1000mm x 3 units) 5. Rental equipments (Choose your own)※ M. Brochure stand (A4 size, 6 rows) 5-1 Electrical equipment (Choose 3 items) N. Panel stand (Choose 1 item) 2700 A. Fluorescent light (40W) O. Fire extinguisher B. Spotlight (100W) P. Table-top brochure stand & Business card box C. Arm spotlight (100W) Q. Hanger stand (x 1 unit) & Hangers (x 10 units) 5-2 Rental equipment (Choose 1 item) ※Check the official website or contact the Secretariat Carpet D. Reception counter 6. Electricity (Choose your own color) E. Square table (Choose 1 item) Electric wiring work (Up to 1kW/ 100V) Date Venue F. Counter table (φ600xH1000mm) Electricity usage (1kW/ For set up & show period ) 2970 Tue Fri G. -

Hankyu REIT, Inc. 19-19 Chayamachi, Kita-Ku, Osaka Growth Strategy/Management Policy

HEP Five HANKYU NISHINOMIYA GARDENS Kitano Hankyu Building Hankyu Corporation Head Office Building Dew Hankyu Yamada AEON MALL SAKAIKITAHANADA Takatsuki-Josai Shopping Center MANDAI Toyonaka Honan Store Ueroku F Building Kita-Aoyama San cho-me Building Nitori Ibaraki-Kita Store DAILY QANAT Izumiya Horikawa Marutamachi Store Kohnan Hiroshima Nakano-Higashi Store kotocross Hankyu Kawaramachi Sphere Tower Tennozu LIFE Shimoyamate Store Shiodome East Side Building MANDAI Gojo Nishikoji Store Hotel Gracery Tamachi KOHYO Onohara Store LAXA Osaka OASIS Town Itami Konoike th Fiscal Period Semi-Annual Report LaLaport KOSHIEN METS OZONE 25 Vessel Inn Hakata Nakasu From June 1, 2017 to November 30, 2017 Hankyu REIT, Inc. 19-19 Chayamachi, Kita-ku, Osaka http://www.hankyu-reit.jp/eng/ Growth Strategy/Management Policy Implementation of management that emphasizes stability of 1 Distribution Policy distributions in the medium-to-long-term period Further sustainable growth of portfolio by utilizing the comprehensive Hankyu REIT, Inc. 2 External Growth Strategy strengths of the Hankyu Hanshin Holdings Group 3 Internal Growth Strategy Deepening of operational management 25th Fiscal Period Semi-Annual Report From June 1, 2017 to November 30, 2017 4 Financial Strategy Implementation of stable financial operations and LTV controls Table of Contents To Our Unitholders 03 To Our Unitholders Hankyu REIT is implementing measures toward 04 25th Fiscal Period Highlights continued growth and enhancement of distributions. 06 Topics We hereby report on the management status of Hankyu REIT for the 25th fiscal period from June 1, 2017 to November 30, 2017. ◦Achieving Continued Growth through Public Offering In the fiscal period under review (25th fiscal period), Hankyu REIT took a solid and Property Acquisitions step forward toward expanding its asset scale, enhancing portfolio quality and raising distributions on an ongoing basis. -

Hotel Hankyu RESPIRE"

News Release March 20, 2019 To: Media organizations Hankyu Hanshin Hotels Co., Ltd. New hotel brand "Hotel Hankyu RESPIRE" Name Decided for Hotel in Yodobashi Umeda Tower (tentative name) Scheduled to open in November 2019 Hankyu Hanshin Hotels Co., Ltd. (Head office: Kita-ku, Osaka; President and Representative Director: Kazuhide Fujimoto) has decided the name of its new hotel scheduled to open in Yodobashi Umeda Tower (tentative name), which is being developed by Yodobashi Holdings Co., Ltd. (Head office: Shinjuku, Tokyo; President: Terukazu Fujisawa). With the inauguration of this new hotel, we will establish an accommodation-focused hotel brand called "Hotel Hankyu RESPIRE." As the first hotel in the brand, this new hotel will be named Hotel Hankyu RESPIRE OSAKA. With the decision made for Osaka to host the World Expo 2025 and expectations for the city to experience further growth as an international tourist city, we will aim to open the hotel in November 2019.1 1. The hotel was originally scheduled to open in the beginning of 2020, but since the plan is progressing well, we will aim to open the hotel in November 2019. The new hotel's logo Exterior of the Yodobashi Umeda Tower (tentative name) Hotel Hankyu RESPIRE OSAKA Plan Outline Location: 1-1 Ofuka-cho, Kita-ku, Osaka Number of guest rooms: 1,032 (Double414, twin399, triple171, quadruple48) Open date: November 2019 Ancillary facilities: One banquet hall, one restaurant, fitness room (free for staying guests) Inquiries regarding this release: Naoya Matsui, Rie Izumaru, Keita Yamano, Sales Planning, Marketing Department, Hankyu Hanshin Hotels Co., Ltd. -

Notice of the 98Th Annual General Meeting of Shareholders (309Kb/Pdf)

This document has been translated from a part of the Japanese original for reference purposes only. In the event of any discrepancy between this translated document and the Japanese original, the original shall prevail. The Company assumes no responsibility for this translation or for direct, indirect or any other forms of damages arising from the translation. (Securities Code 8818) May 31, 2021 To Those Shareholders with Voting Rights Koichi Minami President Keihanshin Building Co., Ltd. 2-14 Kawaramachi 4-chome, Chuo-ku Osaka-shi, Osaka NOTICE OF THE 98TH ANNUAL GENERAL MEETING OF SHAREHOLDERS You are hereby notified that the 98th Annual General Meeting of Shareholders of the Company will be held as described below. Instead of attending the meeting in person, you can exercise your voting rights in writing or by electronic means, including the Internet. Please review the Reference Documents for the General Meeting of Shareholders and exercise your voting rights by 5:00 p.m. on June 17, 2021 (Thursday) in accordance with the instructions on the next page. 1. Date and Time: Friday, June 18, 2021 at 10:00 a.m. 2. Place: “Emerald Room,” 2nd floor of Viale Osaka 3-1-3 Azuchimachi, Chuo-ku, Osaka 3. Agenda of the Meeting: Matters to be reported: 1. The Business Report, the Consolidated Financial Statements and the audit results of the Consolidated Financial Statements by the Independent Accounting Auditor and the Audit & Supervisory Board for the 98th fiscal term (from April 1, 2020 to March 31, 2021) 2. The Non-Consolidated Financial Statements for the 98th fiscal term (from April 1, 2020 to March 31, 2021) Proposals to be resolved: Proposal 1: Appropriation of Surplus Proposal 2: Election of Three (3) Directors Proposal 3: Election of One (1) Audit & Supervisory Board Member 1 If you would like to exercise your voting rights in writing, please indicate your votes for or against each of the proposals on the enclosed Voting Rights Exercise Form and return it so that it will reach the Company no later than the deadline stated above. -

<For Translation Purposes Only> Notice Concerning the Acquisition of Assets 1

<For translation purposes only> January 16, 2009 For Immediate Release REIT Issuer Hankyu REIT, Inc. (Securities Code: 8977) 19-19 Chaya-machi, Kita-ku, Osaka Mineo Yamakawa, Executive Director Asset Management Company Hankyu REIT Asset Management, Inc. Mineo Yamakawa, President & Representative Director Contact: Hideo Natsuaki General Manager, Investor Relations Dept. Email: [email protected] Notice Concerning the Acquisition of Assets Hankyu REIT, Inc. (hereafter “Hankyu REIT”) hereby notifies today that the acquisitions of the assets mentioned below have been decided. Details 1. Overview of Acquisition (1) LAXA Osaka (i) Acquired asset: Real estate trust beneficiary interests Trustee: Mitsubishi UFJ Trust and Banking Corporaton (ii) Property name: LAXA Osaka (iii) Proposed acquisition price: 5,122,800,000 yen (excluding acquisition-related expenses, property tax, city planning tax and consumption tax, among others) (iv) Proposed acquisition date: January 22, 2009 (v) Seller: ZEKUTO GK (vi) Acquisition funds: Debt financing (2) LaLaport KOSHIEN (site) (i) Acquired asset: Real estate trust beneficiary interests Trustee: Mitsubishi UFJ Trust and Banking Corporation (ii) Property name: LaLaport KOSHIEN (site) (iii) Proposed acquisition price: 7,350,000,000 yen (excluding acquisition-related expenses, property tax, city planning tax and consumption tax, among others) (iv) Proposed acquisition date: January 22, 2009 (v) Seller: ZEKUTO GK (vi) Acquisition funds: Debt financing 1 (3) Namba Hanshin Building (i) Acquired asset: Real estate trust -

Members Club Guide

ENGLISH MEMBERS CLU B GU I DE Terms of Membership of the Hankyu-Hanshin-Daiichi Hotel Group Members' Club Article 11. Loss or Theft of or Damage to the Hotel Card Article 1. Membership Requirements 1.In the case of the loss or theft of or damage to the Hotel Card, please contact the administration office of the 1. A "Member" refers to an individual who accepted the Terms of Membership of the Hankyu-Hanshin-Daiichi Hotel Group Members' Club ("Administration Office"). Hankyu-Hanshin-Daiichi Hotel Group Members' Club ("Terms of Membership"), applied for 2.To have the Hotel Card reissued, please apply to the Administration Office or any of the Hotels. In the case of membership to Hankyu Hanshin Hotels Co., Ltd. ("Company"), has been admitted by the Company, application to the Administration Office, the Company will verify the Member's registered personal information and has received a Hankyu-Hanshin-Daiichi Hotel Group Members' Club Card ("Hotel Card") on loan. Membership will be granted to persons aged 18 or over. The date of birth and other similar information be transferred to the new Hotel Card. In the case of application to any of the Hotels, a new Hotel Card with no may be checked for admission purposes. balance will be issued on the spot, and upon the checking of the applicant's personal information by the Administration Office, the points balance will be transferred to the new Hotel Card. The Hotel Card will not be Article 2. Use of the Hotel Card 1.Members may receive services from hotels of the Hankyu-Hanshin-Daiichi Hotel Group ("Hotels") upon presentation of the Hotel Card. -

Hankyu Hanshin Holdings 2020

Hankyu Hanshin Holdings 2020 https://www.hankyu-hanshin.co.jp/en/ Printed in Japan Hankyu Hanshin Holdings Group Management Philosophy Message from the Top Management What we try to achieve In October 2006, Hankyu Hanshin Holdings was established as a result of the management integration of Hankyu Holdings and Hanshin Electric Railway. Since then, the Hankyu Hanshin Holdings Group has worked in unison to heighten the competitiveness of each business. At the same time, the Group Mission has used its collective strength to increase its overall profitability and grow its earnings. In conjunction By delivering “Safety and Comfort” and “Dreams and Excitement”, with these efforts, we have steadily improved our financial position. we create satisfaction among our customers and contribute to society. However, the business environment of the Group is likely to change significantly as the population of areas served by its railway lines declines due to falling birth rates and an aging population, and as the lifestyles and conditions of everyday life evolve with the progress of technological innovation. What is important to us Aiming to become a corporate group that can focus strongly on sustained growth even in such an environment, we announced the Hankyu Hanshin Holdings Group Long-Term Management Vision for Values 2025 (fiscal 2026) in 2017. We have also formulated a medium-term management plan, which covers 1 Customer First fiscal 2019 through fiscal 2022, as concrete actions for the realisation of the long-term vision, and are Everything we do is for the customer. That’s where it all starts. steadily advancing measures based on the plan.