@Eneral Assembly Distr

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Roll to Hard Core Punk: an Introduction to Rock Music in Durban 1963 - 1985

Lindy van der Meulen FROM ROCK 'N 'ROLL TO HARD CORE PUNK: AN INTRODUCTION TO ROCK MUSIC IN DURBAN 1963 - 1985 This thesis has been submitted in fulfilment of the degree of Master of Music at the University of Natal DECEMBER 1 995 ACKNOWLEDGEMENTS The financial assistance of the Centre for Science Development (HSRC, South Africa) towards this research project is hereby acknowledged. Opinions expressed and conclusions arrived at, are those of the author and are not necessarily to be attributed to the Centre for Science Development. The valuable assistance and expertise of my supervisors, Professors Christopher Ballantine and Beverly Parker are also acknowledged. Thanks to all interviewees for their time and assistance. Special thanks to Rubin Rose and David Marks for making their musical and scrapbook collections available. Thanks also to Ernesto Marques for making many of the South African punk recordings available to me. DECLARATION This study represents original work of the author and has not been submitted in any other form to another University. Where use has been made of the work of others, this has been duly acknowledged in the text . .......~~~~ . Lindy van der Meulen December 1995. ABSTRACT This thesis introduces the reader to rock music in Durban from 1963 to 1985, tracing the development of rock in Durban from rock'n'roll to hard core punk. Although the thesis is historically orientated, it also endeavours to show the relationship of rock music in Durban to three central themes, viz: the relationship of rock in Durban to the socio-political realities of apartheid in South Africa; the role of women in local rock, and the identity crisis experienced by white, English-speaking South Africans. -

Elements FASCIST Relationship A

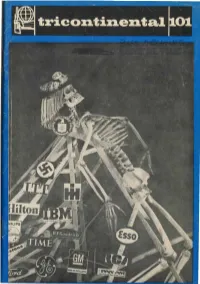

IPJtricontinental�01! Year XI - 1976 Published in Spanish, English, and French by the Executive Secretariat of the Organization of Solidarity of the Peoples of Africa, Asia and Latin America Tricontinental Bulletin authorizes the total or partial reproduction of its articles and information OSPAAAL P.O.B. 4224 Radiogram OSPAAAL Habana, Cuba summary URUGUAY-SOUTH 2 Elenients in a fascist AFRICA relationship UNITED STATES 9 The CIA., Washington and the transnationals Hector Danilo CHILE 22 Our faith is unshakable OAS 25 A. history of aggressions Susana Seleme PUERTO RICO LU Letter from a hero BRAZIL 44, A. challenge to censorship DEMOCRATIC 46 Constitution KAMPUCHEA 0 Appea Is and Messages SOUTH AFRICA 62 Why Soweto URUGUAY 64, Liberty for the political prisoners (�:x::x:::occc::ccx::o::::::iococcx:::,o::::;c::c::x::x:::x:::,:::)c::;cx:::x:...: J>�GiNA COURO Th,? econo�11ic policy can be summed up in the statement by the Minister of tl}a� legislation must be E co�om1cs blind and neutral toward foreign capital . d1stinc 1 an d practice no t on between it and domestic c apital." Pa_rallel to s thi policy of selling the country to foreign investors is th l elements a press1�n, ass ss cy 0 re a inatio . n and torture designed o s l � t i ence forever by physiiat�i'_ the voices that imina_ ion, FASCIST accuse the dictatorship. relationship Uruguay. a small country of 186 926 km� located in what is called the southern cone of the South American continent. flanked by Brazil and Argentina and with extensive bor ders along the Plata River, is suffering under an overtly fascist regime today. -

Protrax Catalogue Protrax Backing Tracks

PROTRAX CATALOGUE PROTRAX BACKING TRACKS July - August 2021 Customer Service & General Enquiries e: [email protected] w: www.protraxonline.com ABOUT THE CATALOGUE ProTrax Productions (South Africa) The backing tracks in this catalogue are arranged e: [email protected] in alphabetical order according to the song title, t: (+27) 82 770 0902 (Weekdays 08h30 to 17h00 - GMT +2) irrespective of language or genre. The availability f: (+27) 86 684 4187 a:191 Lisdogan Avenue, Lisdogan Park, Pretoria, 0083 of catalogued backing tracks may change without notice. ProTrax Music Production House (Australia) e: [email protected] Visit www.protraxonline.com to browse content, f: (+61) 450 778 577 (Weekdays 10h00 to 15h00 - GMT +8) listen to demos or search for backing tracks by: a: P.O. Box 717, South Fremantle, Western Australia, 6162 Genre Latest Additions PROTRAX RECORDING STUDIO Specials Top 10 Charts Bookings & Enquiries (South Africa) w: www.protraxstudio.com e: [email protected] On the website you can also request new tracks, t: (+27) 82 770 0902 (Weekdays 08h30 to 17h00) demos in different keys and view our terms of use. f: (+27) 6 684 4187 a: 191 Lisdogan Avenue, Lisdogan Park, Pretoria, 0083 PROTRAX KARAOKE EXCLUSIVES Customer Service & General Enquiries e: [email protected] w: www.protraxkaraoke.com t: (+27) 82 770 0902 (Weekdays 08h30 to 17h00) ProTrax Backing Track Catalogue J u l y - A u g u s t 2021 P a g e | 1 Joe Niemand from A Candle Burning Pam Thum A New Day Aan Jou Vas Eden "Faith Like Potatoes" A Cradle Prayer Rebecca St. -

Masses Of'people Welcome Their Majesties in Shanghai'

University of Nebraska at Omaha DigitalCommons@UNO Kabul Times Digitized Newspaper Archives 11-9-1964 Kabul Times (November 9, 1964, vol. 3, no. 207) Bakhtar News Agency Follow this and additional works at: https://digitalcommons.unomaha.edu/kabultimes Part of the International and Area Studies Commons Recommended Citation Bakhtar News Agency, "Kabul Times (November 9, 1964, vol. 3, no. 207)" (1964). Kabul Times. 761. https://digitalcommons.unomaha.edu/kabultimes/761 This Newspaper is brought to you for free and open access by the Digitized Newspaper Archives at DigitalCommons@UNO. It has been accepted for inclusion in Kabul Times by an authorized administrator of DigitalCommons@UNO. For more information, please contact [email protected]. , '. .- .~-'- .' . ' . :'- . " . , ..- - ~ : '. : .' . ." , " NOliEMBER 'S, 1964 PAGE 4 . - . - '-- : - .-: - - . .' '. ' : -. " .' .' .- ~ "-' , ~.- " . !Afgh3n-lndian TracIe (Parade Honours I " ' .. Talks Begin Here ' 'I, • '. - - - '<-"";.. • .;1 " .... : -.. , ', ... NEWS" STAlls,' .. KABUL, N1iv:, B.-The, mem- '&if " October Revol utJfto', .~ 'THE- WEATHER' , . ,.. : ·-Forecast·lt;,: Ali AD..tIa~J' .. ' bers of the Indian ·trade delega-, e: ~i)I'. I. .. ~y Max. +ZZOC. MInImum + zoe• , . Kabul' TIDles ds' avanable,.at:· ' .. :: .., tioQ, accompanied...bY a represen- '~M<lSCOW, Nov. :8, '(TiIss).-fhe - ,, ~ -.. ~ -:~oatIo~M~=liJPl\ Sun sets today at 5.5 p.m. • -, , 'Khr'ber 'Res1iurallt; ,Splnpr': ," : tative of the Ministry of Comer- '. Sun rises tomorrow at 6.2% am; , ' , " "&tel;, Kabul Haw;,,~····· th~ !!~~Mi~~,: Y'etierday's TemperaktteS , .' -', . Naw near Park Ctpeml' Kabul . .- .- .October • c100k . Tomorrow's Outlook: Cloudy , .,Inte,rnaUolia! AirpOrt;.' "', ::. ' :' pldce in ·Rl!l{.t4.~\ Westethy., -" ~- It !waS reviewea 'by the USSR , . , . '. '- - .:: - '. M¥.1ster 'C)"!' -neteiICe- '- Manhal --'------:_-.:.....:...,...--....;...- -. , Mfli,riovski.' '{ II(!¥.}? :, " · _.' --. - , fore the - bilogii"ftii\~l'l'lofHjlit.. I I ..-- . -

I COURTS Alleged That the Eccuaed Vere Teetified That Ha Could Ba Conaidersd As Phyeically Responeible for the Death of Sn Expert on the ANC

0aga 40 -'•_"• • J » adjourned to mid Uctober to alio* for Una of the state's first vitneaaea defence preparations. Ihe state has not vae Lieut*~Col. Harmanue Stedlar, vho I COURTS alleged that the eccuaed vere teetified that ha could ba conaidersd as phyeically responeible for the death of sn expert on the ANC. According to hie PRETORIA TREASON TRIAL. 2 vomen at the Silverton bank, nor has teatiaony, the ANC vea formed in 1912 1. Nciebithi Johnson Lubiei (28), it clsiaed that all the accuaad vera aa tha South African Native National 2* Petrue Teepo Haehigo (20), involved in the Soekmekeer attack or Congress, but later changed ita naae. 3. Nophtali Honone (24), 4. lkanyeng Hoitt Molebetoi (27). tha planning of tha bank aiege* What In 1944 tha ANC Youth Leegue vae foraed 5. Hioiiic Benjamin tau (24)t the prosecution doea claim ia that under the leadership of inter alia Nelaon 6. Phumulani Grant Sheri (2a), )# Jeremiah Radebe (26), each of the accuaad Joined and Handala, Walter Sisulu and Oliver Tambo. 0. Boyce Johannee Bogale (26), participated in an ANC conaplracy to The Youth League introduced e more 9. I hoes a Mngadi (29) . overthrow the atete; that the Silverton militant etmoaphere into the ANC, and Aa datailad on pagea 39 - 41 or WiP 14, end Soekaekaar incidents vere part of during the 1950a a programme of thfc 9 accueed listed abova currently that general conapiracy, and that the demonatrationa and paaaiva reaiatance face charges of High treason, murder, accuaad are ell eccordingly raaponaible took place. attempted border and robbery vith for acta in furtherance of tha in the mid 19SGe the Congress aggravating circumstancea, aa veil aa conapiracy. -

Rockabilly Ravens

Rockabilly Ravens The Band Hailing from an era where rock ‘n roll was King and pinup girls were Queen, the Rockabilly Ravens bring you a real taste of Rockabilly music. Formed in the Alabama State Penitentiary and inspired by the original Hound Dog and his Jailhouse Rock, the band was originally a front to entertain the guards while inmates worked on tunnelling out of jail. The Ravens are a collection of the baddest rock ‘n rollers who know how to entertain. After gaining notoriety, they decided to change their names and take the show on the road. Playing every honky-tonk bar in the South, the Ravens developed a reputation as the essential Rockabilly band. With leather jackets, tattoos and their very own Raven–haired pinup girl, the band can get any party started with high energy, up- tempo Rockabilly music. A selection of classic hits and modern anthems bring the Ravens soaring into the 21st century. Rock ‘n roll is alive and well, and in good hands! The Rockabilly Ravens are a high-quality, star-studded ensemble featuring Samantha Peo (multiple Naledi Award winner and judge on Strictly Come Dancing), singer Musa Sakupwanya (featured in shows by Nataniel), Martin Rocka (guitarist with Wonderboom and former musical director of Idols), American preliminary Grammy Award nominee John Fresk as the Musical Director, and a horn and rhythm section with formidable experience. The Rockabilly Ravens balance timeless rockabilly classics with arrangements of contemporary hits done in the rockabilly style. They're a refreshing, fun and energetic class act, guaranteed to appeal to a broad and diverse demographic. -

February 1981 1

16 HF BM) HEALTH CARE for profit FEBRUARY 1981 1 - THE ARTICLE thmt follows mm h supplement to thin The contribution ia an exploratory one, as far as this is cencsrned. tfortt In Progrcia represents a departure from and does not aim to be definitive or complete- Contributors submitting matarlml far previous editorial policy. u tad been It certainly falls into the category of work inclusion In future supplements should decided not to include contributions in WIP in progreaa. One of the reasona for presenting Include a non-technical, aaaily accessible which, beceuas of terminology used, vers not it in sTIP la to elicit comment and response, summary of their mrticle for inclusion In the fairly easily accessible to those without m and the author, David Kaplan, has specifically mmin body of HP, specific training in the area being discussed. requeated critical comment on the article. The contribution which follows BeJtes use of Thia will assist in the development and certain complex concepts, and the terminology furthering of a debate which touchee on the used and Ideas explored are difficult reading atructure of the South African economy, the for the non-expert* likely form of future capitalist development, The editors nonetheless felt that the and the implications of both structure and article was an laportant one. making a development. contribution of contemporary value, and having Comment can be Bent to the editors, or definite ett^ategic implications. The editors directly to were unwilling to deprive WI^ readerahlp of David Kaplan, the ideaa and information contained in the Department of Economic Hlatory, University of Cape Town, article because of their complexity, snd it 7700 Rondeboech, was accordingly decided to Include it as a CAPE TOW. -

Claiming Sounds, Constructing Selves: the Racial and Social

Claiming Sounds, Constructing Selves: The Racial and Social. Imaginaries ofSouth African Popular Music Mary Robertson Submitted in fulfilment ofthe requirements for the degree ofMaster of Arts in the Department ofMusic University of KwaZulu-Natal 2005 Acknowledgements: Without a number ofpeople and institutions, this thesis would not have been possible, and I would like to convey my sincere appreciation to all ofthose listed below. Firstly, I would like to thank the NRF for their generous financial assistance throughout the course ofmy Masters. Secondly, I would like to thank my supervisor Professor ehris Ballantine for his encouragement, insight, and support, and for being as excited as me by the issues explored in this research project. Thirdly, I would like to thank my friends and family. To my parents, thank you for using up your free minutes on my weekly blow-by-blow accounts of my progress. To Lindelwa (and Lindo), thank you for always challenging me, and for teaching iny landlord more than he wanted to know about Bhaktin. And to Jay, thank you for your never-ending patience, and for being there. And for the coffee. Finally, I would like to thank my research participants, who gave me their time and allowed me a glimpse into their lives and experiences, and from whom I have learnt a great deal. Declaration I declare that this dissertation is my own, original work. It has not been submitted before for any degree or examination. ->J;,-/k----~.....:::....:-"'<------ Signed: -!lfM-I-..........:.'.:..1-. Durban, _3_ day of IV(; Vtfh her ,2005. Abstract: This thesis explores some of the ways in which listening to South African popular music allows individuals to enter into imaginative engagements with others in South Africa, and in so doing, negotiate their place in the social landscape. -

814-2367.Pdf

814 MZM2\ 86 Maxaquene a comprehensive account of the first urban upgrading experience in the new Mozambique Ingemar Saevfors t:: ~ Human settlements 37 and socio-cultural environments UNESCO 814—2367 Maxaquene a comprehensive account of the first urban upgrading experience in the new Mozambique Ingemar Saevfors L~7fl’, ~ ~ ~Ur~ LY ~ ~~‘‘ ~) ~ e~141/1L2 LO: ~ ~1A~ Human settlements and socio-cultural environments March 1986 UNESCO MAXAQUEXE A comprehensive account of the first urban upgrading experience in the new Mozambique. GREDITS L.engua~econsul tants: uw Rosellini. Los Angeles Sara Goodman • Lund Manuscript reviews: Carol Hogel. Helsinki Per Rathswan, Gothenburg Graphic materials: Stefen Waliwark. UaeA Anchy de la Garza, Uppsala © 1984, Ingemar Saevfora. All rights reaerved. INDEX 01 PREFACE 02 THE CONTEXT Project background. Hietory. econonty. politice. Deecription of the caniço aettleaente. 03 THE PLAN Urban planning principlee. Current etrategiee. The upgrading approach. Concepte developed in the pro- ject. 04 THE PROJECT linplementation of the plan. Mobilization. Confront— ing the realities. OS THE CRITICS Post project developinent. Poiltical repercuesions. Criticiem~profeesional and general. 06 THE COLORS Fiction story for personal coaprehension of caniço conditione. YELLOW PAGES: 07 SINPLIFIED AERIAL PHOTOGRAPHY EquipRent, flight plenning. calculations, in flight procedures. 08 STAKING otrr WITHOUT DEMOLITION Method deecription. equipinent. limite. COST REVIEW Project Costa on different levels. Hidden costa for dweliers. BIBLIOGRAPHY A8REVIATIONS AND VOCABULARY 01 PREFACE What you are about to remd now is neither a report nor a Though nearly conipleted, the manual was oever published. scientific record. It ia not a fiction story sither, Mevertheless, the need for e comprehenaive document becauae it carries a large number of data, hopefully about the project beceme apparent. -

The Retro Catalogue Classic South African Rock and Pop Reissues

The Retro Catalogue Classic South African rock and pop reissues Freshcd 147 The Complete Asylum Kids 21 track retrospective of one of the most influential post-punk and pre-alternative bands in South African rock..Both the band`s albums plus 2 bonus tracks. Freshcd 146 Abstract Truth –Silver Trees/ Totem A two albums-on-1-cd retrospective of one of the pioneers of early 70`s South African progressive rock, a unique heady brew of folk ,psych, jazz and rock. Freshcd 148 Astral Daze Volume 1-Various Artists An 18 track compilation of classic South African psychedelic music ranging from the late 60`s onwards. Includes many unreleased tracks from the likes of John & Philipa Cooper, Dickie Loader, Buzzard, The Invaders and The Third Eye. Freshcd 162 Astral Daze Volume 2-Various Artists Another 18 psychedelic gems from the South African underground including the likes of The Gonks, Hedgehoppers, Omega Limited, McCully Workshop and The Tidal Wave. Freshcd 151 Arapaho-Wild Warriors 20 track retrospective of one of the hardest rocking bands of the mid 90`s. Includes “Butterfly angel” , “Wicked wonder” and “Innocent child” . Freshcd 166 Canamii –Concept Rare prog rock album originally released in 1980, similar to Renaissance, Curved Air and early ELP with strong female vocals,synths guiatrs and classical keyboards. Freshcd 116 Circus-In the arena Mid 70`s progressive pomp rock in the vein of early Queen and City Boy. Includes a stunning version of Procol Harum`s “ Conquistador”. Freshcd 136 Celtic Rumours-Slow Rain For fans of the New Romantic movement comes The Complete Celtic Rumours –an 18 track collection drawn from the band`s two albums including the hits “ Slow rain” , “This day‟ and “Wish”. -

Promag: the History, the Future

FOURTH QUARTER 2014 VOLUME 22 NUMBER 4 PROMAG: THE HISTORY, THE FUTURE upfront Fourth Quarter 2014 Volume 22 Number 4 PROMAG is published quarterly by Electrosonic A TRIP DOWN MEMORY LANE CONTENTS SA and distributed to the professional audio, video and lighting industry. © PROMAG and When I decided to write a cover story about the DIARY history and future of PROMAG, I did not quite realise Electrosonic SA. All rights reserved. Trademarks what I was letting myself in for. Since its inception Integrated Systems Europe, NAB SHOW, are the property of their respective owners. in 1993, Pro-Magazine (as it was called then) was 2 Prolight + Sound 2015, IFSEC South Africa published quarterly, without skipping one issue. This Editorial and subscriptions means I had a tremendous number of magazines (92 Managing Editor – Terry Bourquin to be precise) to read in a very short period. Tight NEWS 011 770 9800 or [email protected] deadlines didn’t help. Panavision Evolve unveils Crestron demo wall, Light in the East, SA’s AV industry This is a task one needs to do without the normal 3 Editor - Khuboni Communications to embrace global standards, James Thom- interruptions of work, and I muttered Thank God for weekends” as I left the office with a pack of as Engineering joins Milos Group, EFC kick- Design and production - Minesh Juggan magazines under each arm. What an entertaining ing it M-series style, AV systems give Red and enlightening weekend it was! In this issue I’m Bull wings, CM Lodestar Electric Chain Hoist, Cover Image - PROMAG: THE HISTORY, THE proud to share with you my trip down PROMAG’s the undisputed industry workhorse, Train- FUTURE memory lane. -

Michael Waddacor

Introducing Michael Waddacor Passionate music writer, critic and documentarian “Michael Waddacor is without a doubt one of the finest rock music critics and writers I have had the pleasure of working with. His knowledge of the music business is mind- boggling and he has always demonstrated an almost child-like enthusiasm for all things musical. I would dearly love to see Michael back at the helm doing what he does best ― writing and commenting on the music scene. His contribution can only enrich our industry,” Georg Voros, drummer, composer and educator, 2011, Johannesburg Michael Waddacor ― music writer 1 O V E R T U R E A rare master of his craft ― and a man of great passion THE REALMS of music burst open with lustrous colour, rich textures and enrapturing vistas when a certain artist, album or trend is subjected to the searching vision and exacting skills of an adroit music writer and commentator. Over the years, commendable music publications in America and Britain have exposed us to the distinctive voices and engaging styles of respected music writers. Among them, we celebrate and admire Ralph Gleason, Greil Marcus, Nick Kent, David Fricke, Rob Young, Ian MacDonald, Stephen Holden, Dave Marsh, Robert Christgau, David Cavanagh and Timothy White. In South Africa, our music fraternity has Michael Waddacor ― a master of his craft, both as an original and engaging writer, and as an erudite and passionate music commentator and historian. An uncompromising music enthusiast since the age of eight, Michael has been writing on rock and other forms of contemporary music since commencing his journalism career in January 1979 at The Herald newspaper in Zimbabwe.