TRP Programme List July Revision 64

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Guangzhou Automobile Group

China / Hong Kong Company Guide Guangzhou Automobile Group Version 6 | Bloomberg: 2238 HK Equity | 601238 CH Equity | Reuters: 2238.HK | 601238.SS Refer to important disclosures at the end of this report DBS Group Research . Equity 7 May 2019 Japanese JCEs leading growth H: BUY Last Traded Price (H) ( 7 May 2019):HK$8.14(HSI : 29,363) More clarity on JVs future strategy. Guangzhou Auto (GAC) and its Price Target 12-mth (H):HK$9.60 (17.9% upside) (Prev HK$17.86) Japanese JCE partners have agreed on key priorities to grow the business. The medium-term plans include capacity expansion and new A: HOLD model development (both traditional and new energy vehicles). Last Traded Price (A) ( 7 May 2019):RMB11.61(CSI300 Index : 3,721) Price Target 12-mth (A):RMB11.30 (2.7% downside) (Prev RMB21.71) Another key factor is that both partners have agreed to maintain the current shareholding structure, hence removing uncertainties. The Analyst Rachel MIU+852 36684191 [email protected] Japanese auto brands have gained market share from 15.6% in December 2016 to 19% in February 2019 aided by their product What’s New range, pricing, and proactive business strategy. Despite the tough • More clarity on development of Japanese JCEs, key 1Q19 auto market, GAC’s Japanese JCEs managed to chalk up strong earnings driver in the future volume sales growth and decent profit contributions to the group. • Self-brand going through short-term adjustment and Where we differ? We expect normalisation of Trumpchi sales to have should start to normalise in 2H19 a meaningful impact on earnings, on anticipation of a recovery in • Maintain BUY, TP revised down slightly to HK$9.60 the PV market in 2H19. -

CHINA CORP. 2015 AUTO INDUSTRY on the Wan Li Road

CHINA CORP. 2015 AUTO INDUSTRY On the Wan Li Road Cars – Commercial Vehicles – Electric Vehicles Market Evolution - Regional Overview - Main Chinese Firms DCA Chine-Analyse China’s half-way auto industry CHINA CORP. 2015 Wan Li (ten thousand Li) is the Chinese traditional phrase for is a publication by DCA Chine-Analyse evoking a long way. When considering China’s automotive Tél. : (33) 663 527 781 sector in 2015, one may think that the main part of its Wan Li Email : [email protected] road has been covered. Web : www.chine-analyse.com From a marginal and closed market in 2000, the country has Editor : Jean-François Dufour become the World’s first auto market since 2009, absorbing Contributors : Jeffrey De Lairg, over one quarter of today’s global vehicles output. It is not Du Shangfu only much bigger, but also much more complex and No part of this publication may be sophisticated, with its high-end segment rising fast. reproduced without prior written permission Nevertheless, a closer look reveals China’s auto industry to be of the publisher. © DCA Chine-Analyse only half-way of its long road. Its success today, is mainly that of foreign brands behind joint- ventures. And at the same time, it remains much too fragmented between too many builders. China’s ultimate goal, of having an independant auto industry able to compete on the global market, still has to be reached, through own brands development and restructuring. China’s auto industry is only half-way also because a main technological evolution that may play a decisive role in its future still has to take off. -

Automotive in South Asia from Fringe to Global

Automotive in South Asia From Fringe to Global Extended Version of the Industry Case Study Done for: South Asia’s Turn Policies to Boost Competitiveness and Create the Next Export Powerhouse Priyam Saraf October, 2016 THE WORLD BANK GROUP . Acknowledgements: This case study was authored by Priyam Saraf ([email protected]), an Economist with the Trade & Competitiveness Global Practice of the World Bank Group. Michel Bacher, auto sector advisor, provided invaluable industry inputs on benchmarking with China, Vietnam, and Republic of Korea. The author is grateful to Vincent Palmade (Lead Economist, World Bank Group) for his excellent inputs and guidance throughout the process. The author would like to acknowledge the valuable comments made by the peer reviewers: Uri Dadush (Carnegie Endowment for International Peace), Navin Girishankar (World Bank Group), Pravin Krishna (Johns Hopkins University), and Shubham Chaudhuri (World Bank Group). Comments provided by Martin Rama, William Maloney, Esperanza Lasagabaster, Sanjay Kathuria, Denis Medvedev, Mike Ferrantino, Sebastian Saez, Daria Taglioni, Paramita Dasgupta, Amjad Bashir, and Jana Malinska from the World Bank and Emmanuel Pouliquen, Shamsher Singh, Arvind Srinivasan and Ramesh Ramanathan from the International Financial Corporation (IFC) helped improve the paper. Deeksha Kokas, Atisha Kumar and Lucia Garcia Velazquez provided superb research support. The author would like to acknowledge the many automotive firms and related public and private organizations that gave us their precious -

State of Automotive Technology in PR China - 2014

Lanza, G. (Editor) Hauns, D.; Hochdörffer, J.; Peters, S.; Ruhrmann, S.: State of Automotive Technology in PR China - 2014 Shanghai Lanza, G. (Editor); Hauns, D.; Hochdörffer, J.; Peters, S.; Ruhrmann, S.: State of Automotive Technology in PR China - 2014 Institute of Production Science (wbk) Karlsruhe Institute of Technology (KIT) Global Advanced Manufacturing Institute (GAMI) Leading Edge Cluster Electric Mobility South-West Contents Foreword 4 Core Findings and Implications 5 1. Initial Situation and Ambition 6 Map of China 2. Current State of the Chinese Automotive Industry 8 2.1 Current State of the Chinese Automotive Market 8 2.2 Differences between Global and Local Players 14 2.3 An Overview of the Current Status of Joint Ventures 24 2.4 Production Methods 32 3. Research Capacities in China 40 4. Development Focus Areas of the Automotive Sector 50 4.1 Comfort and Safety 50 4.1.1 Advanced Driver Assistance Systems 53 4.1.2 Connectivity and Intermodality 57 4.2 Sustainability 60 4.2.1 Development of Alternative Drives 61 4.2.2 Development of New Lightweight Materials 64 5. Geographical Structure 68 5.1 Industrial Cluster 68 5.2 Geographical Development 73 6. Summary 76 List of References 78 List of Figures 93 List of Abbreviations 94 Edition Notice 96 2 3 Foreword Core Findings and Implications . China’s market plays a decisive role in the . A Chinese lean culture is still in the initial future of the automotive industry. China rose to stage; therefore further extensive training and become the largest automobile manufacturer education opportunities are indispensable. -

Takata Allocation Schedule V3 (01.30.2018).Xlsx

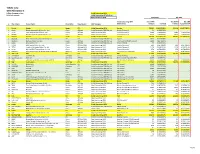

2:16-cr-20810-GCS-EAS Doc # 60-2 Filed 02/01/18 Pg 1 of 3 Pg ID 514 EXHIBIT B 2:16-cr-20810-GCS-EAS Doc # 60-2 Filed 02/01/18 Pg 2 of 3 Pg ID 515 Takata Corp OEM Allocation % Initial Consenting OEM Inflator shipping volume Initial Consenting OEM Roll‐up Units in thousands Joining OEM Non‐Consenting OEM Shipments ALL OEM Initial Consenting OEM Total PSAN Total PSAN ALL OEM # Short Name Formal Name Head office OEM Category Relationship Inflators % of total Inflators ALLOCATION % 1 Honda Honda Japan Initial Consenting OEM Honda 53,397 14.8215192% 53,419 14.8277907% 2CHAC Honda Automobile (China) Co., Ltd. China Initial Consenting OEM Roll‐up Honda Chinese JV 23 0.0062715% ‐ ‐ 3GHAC GAC Honda Automobile Co., Ltd. China Joining OEM Honda Chinese JV 3,682 1.0220562% 3,682 1.0220562% 4WDHAC Dongfeng Honda Automobile Co., Ltd. China Joining OEM Honda Chinese JV 4,323 1.2000105% 4,323 1.2000105% 5 Toyota Toyota Japan Initial Consenting OEM Toyota 44,018 12.2181997% 48,881 13.5681391% 6 NUMMI New United Motor Manufacturing, Inc. US Initial Consenting OEM Roll‐up Toyota 1,922 0.5335676% ‐ ‐ 7Daihatsu Daihatsu Motor Co., Ltd. Japan Initial Consenting OEM Roll‐up Toyota owned (100% owned) 2,908 0.8072901% ‐ ‐ 8HINO Hino Motors, Ltd. Japan Initial Consenting OEM Roll‐up Toyota affiliate 33 0.0090817% ‐ ‐ 9GTMC GAC Toyota Motor Co., Ltd. China Joining OEM Toyota Chinese JV 602 0.1671380% 602 0.1671380% 10 TFTM Tianjin FAW Toyota Motor Co., Ltd. China Joining OEM Toyota Chinese JV 3,069 0.8517936% 3,069 0.8517936% 11 SFTMCF Changchun Fengyue Company of Sichuan FAW Toyota Motor Co., Ltd. -

China Autos Driving the EV Revolution

Building on principles One-Asia Research | August 21, 2020 China Autos Driving the EV revolution Hyunwoo Jin [email protected] This publication was prepared by Mirae Asset Daewoo Co., Ltd. and/or its non-U.S. affiliates (“Mirae Asset Daewoo”). Information and opinions contained herein have been compiled in good faith from sources deemed to be reliable. However, the information has not been independently verified. Mirae Asset Daewoo makes no guarantee, representation, or warranty, express or implied, as to the fairness, accuracy, or completeness of the information and opinions contained in this document. Mirae Asset Daewoo accepts no responsibility or liability whatsoever for any loss arising from the use of this document or its contents or otherwise arising in connection therewith. Information and opin- ions contained herein are subject to change without notice. This document is for informational purposes only. It is not and should not be construed as an offer or solicitation of an offer to purchase or sell any securities or other financial instruments. This document may not be reproduced, further distributed, or published in whole or in part for any purpose. Please see important disclosures & disclaimers in Appendix 1 at the end of this report. August 21, 2020 China Autos CONTENTS Executive summary 3 I. Investment points 5 1. Geely: Strong in-house brands and rising competitiveness in EVs 5 2. BYD and NIO: EV focus 14 3. GAC: Strategic market positioning (mass EVs + premium imported cars) 26 Other industry issues 30 Global company analysis 31 Geely Automobile (175 HK/Buy) 32 BYD (1211 HK/Buy) 51 NIO (NIO US/Buy) 64 Guangzhou Automobile Group (2238 HK/Trading Buy) 76 Mirae Asset Daewoo Research 2 August 21, 2020 China Autos Executive summary The next decade will bring radical changes to the global automotive market. -

Download Automotive Patent Trends 2019 – Technologies

A U T O M O T I V E P A T E N T T R E N D S 2 0 1 9 Cipher Automotive is the only patent intelligence software that includes a taxonomy of over 200 technologies critical to the future of the car AU T O M O T I V E @ C I P H E R . A I Cipher Automotive Patent Trends 2019 provides a strategic overview of patented technologies in Foreword the sector. Patent intelligence is critical at a time when there is an accelerating shifrom conventional technologies to connectivity, autonomy, shared services and electrification. It is not only the OEMs and their suppliers who are investing billions in automotive R&D, but an entire network of technology companies and a vast swathe of start-ups that are now able to participate at a time when barriers to entry have been lowered. These dynamics are placing increasing pressure on legal, intellectual property and R&D teams alike. We have now reached the point where there are over two million new patents published a year, and it is harder than ever to understand whether the patents you own are the ones that truly serve your business objectives. Advances in AI have made it possible to access information about who owns patented technology. The analysis of technologies and companies in the pages that follow were generated in less than 4 hours - by a machine that does not tire, drink coffee or take holidays. Nigel Swycher, CEO and Steve Harris, CTO This section covers nine technology areas within the automotive industry, identifies the top patent Section 1: owners, shows the growth of patenting, highlights a few important technologies within each area, and includes league tables across the major geographies. -

China Annex VI

Annex I. Relations Between Foreign and Chinese Automobile Manufacturers Annex II. Brands Produced by the Main Chinese Manufacturers Annex III. SWOT Analysis of Each of the Ten Main Players Annex IV. Overview of the Location of the Production Centers/Offices of the Main Chinese Players Annex V. Overview of the Main Auto Export/Import Ports in China Annex VI. An Atlas of Pollution: The World in Carbon Dioxide Emissions Annex VII. Green Energy Vehicles Annex VIII. Further Analysis in the EV vehicles Annex IX. Shifts Towards E-mobility Annex I. Relations Between Foreign and Chinese Automobile Manufacturers. 100% FIAT 50% Mitsubishi Guangzhou IVECO 50% Beijing Motors 50% Hyundai 50% GAC Guangzhou FIAT GAC VOLVO 91.94% Mitsubishi 50% 50% 50% 50% 50% (AB Group) Guangzhou BBAC 50% Hino Hino Dongfeng DCD Yuan Beiqi 50% 50% NAVECO Invest Dongfeng NAC Yuejin 50% Cumins Wuyang 50% Guangzhou GAC Motor Honda 50% Yuejin Beiqi Foton Toyota 50% Cumins DET 50% 55.6% 10% 20% 50% Beiqi DYK 100% Guangzhou Group Motors 50% 70% Daimler Toyota 30% 25% 50% 65% Yanfeng SDS shanghai 4.25% 100% 49% Engine Honda sunwin bus 65% 25% visteon Holdings Auto 50% (China) UAES NAC Guangzhou 50% Beilu Beijing 34% Denway Automotive 50% Foton 51% 39% motorl Guangzhou 50% Shanghai Beiqi Foton Daimler 100% 30% 50% VW BAIC Honda Kolben 50% 90% Zhonglong 50% Transmission 50% DCVC schmitt Daimler Invest 100% 10% Guangzhou piston 49% DFM 53% Invest Guangzhou Isuzu Bus 100% Denway Beiqi 33.3% Bus GTE GTMC Manafacture xingfu motor 50% 20% SAIC SALES 100% 20% 100% 100% DFMC 100% Shanghai -

The Way of Chery to Achieve the Most Successful Auto

THE WAY OF CHERY TO ACHIEVE THE MOST SUCCESSFUL AUTO BRAND IN CHINA Thesis Yan Tao Degree Programme in International Business International Marketing Management SAVONIA UNIVERSITY OF APPLIED SCIENCES Business and Administration, Varkaus Degree Programme, Bachelor of Business Administration, International Business, International Marketing Management Author Yan Tao Title of Study The Way of Chery to Achieve the Most Successful Auto Brand in China Type of Project Date Pages Thesis 14.12.2010 62+3 Supervisor of Study Executive organization Virpi Oksanen Abstract The automobile market in China is in the state of growth. The development of new energy vehicles and the automobile industry is taking place in the forms of regrouping and restructuring. This offers Chery a great opportunity to develop and promote the brand. As one of the most influential and famous auto brand, Chery Auto has achieved an extraordinary growth rate and has become the pride of Chinese national automobile industry. Nevertheless, there is still certain potential in product quality, service and business culture which develops the brand image further. In consequence, issues regarding to manufacturing, service and business culture are needed to improve and strengthening. However, the brand advantage of Chery Auto is not protruding. Compared with international automotive corporations, Chery Auto is not dominant in brand recognition and brand core value. Furthermore, multi-brand strategy leads to dilution of major brands. There are many sub-brands under Chery; nevertheless, no sub-brand achieves big sales. None of Chery Auto’s four sub-brands, Chery, Rely, Karry or Riich, is dominant in the automobile market. Its position in market is not stable. -

P ASAJ E ROS Y MIX to CA RGA Tabla No. 1. CLASIFICACIÓN

MINISTERIO DE TRANSPORTE Tabla No. 1. CLASIFICACIÓN SEGÚN CLASE, TIPO Y MARCA PARA EL AÑO FISCAL 2011 MODALIDAD CLASE Y CARROCERIA GRUPO MARCA Aro, Asia, Austin, Barreiro, Baw, Bock Wall, Chana, Changfeng, Changhe, Dacia, Daewoo, Datsun, Desoto, Deutz, Dfm, Dragon, Ernest Gruber, Faw, Fiat, Forland, Foton, Golden Dragon, Goleen, GWM, Hafei, Hersa, Higer, Huali, Ifa, Jac, Jiangchan, F Jinbei, JMC, Kaizer, Kamaz, Kiamaster, Kraz, Land Rover, Man, Mudan, PH Omega, Tractocamiónes y Camionetas Ramírez, Reo, Saic, Sinotruck, Sisu, Skoda, Steyr, Studebaker, Tata, T-King, Tmd, y Camiónes con carrocería Uaz, Wartburg, White, Willco, Willys, World Star, Xinkai, Yutong, ZX Auto estacas, estibas, niñera, panel, picó, planchón, portacontenedor Agrale, Ample, Chevrolet, Citroen, Daihatsu, Dina, Delta, Dodge, Fargo, Ford, GMC, y reparto. Hino, Hyundai, Kia, International, Isuzu, Iveco, Honda, Magirus, Mazda, Mitsubishi, G Mercury, Nissan, Non Plus Ultra, Peugeot, Renault, Renno, Ssangyong, Schacman, Suzuki, Toyota, Volkswagen Freigthliner, Kenworth, Mack, Marmon, Mercedes Benz, Pegaso, Scania, Volvo y H Wester Star Aro, Asia, Austin, Barreiro, Baw, Bock Wall, Chana, Changfeng, Changhe, Dacia, Daewoo, Datsun, Desoto, Deutz, Dfm, Dragon, Ernest Gruber, Faw, Fiat, Forland, Foton, Golden Dragon, Goleen, GWM, Hafei, Hersa, Higer, Huali, Ifa, Jac, Jiangchan, I Jinbei, JMC, Kaizer, Kamaz, Kiamaster, Kraz, Land Rover, Man, Mudan, PH Omega, Camionetas, Camiónes con Ramírez, Reo, Saic, Sinotruck, Sisu, Skoda, Steyr, Studebaker, Tata, T-King, Tmd, Uaz, Wartburg, -

OEM PSAN Inflator Sales Data Schedule

Takata Corp OEM Allocation % Inflator shipping volume Initial Consenting OEM Units in thousands Initial Consenting OEM Roll-up Non-Consenting OEM Shipments ALL OEM Initial Consenting OEM Total PSAN Total PSAN ALL OEM # Short Name Formal Name Head office Classification OEM Category Relationship Inflators % of total Inflators ALLOCATION % 1 Honda Honda Japan CG Initial Consenting OEM Honda 53,397 14.8215192% 53,419 14.8277907% 2 CHAC Honda Automobile (China) Co., Ltd. China Affiliate Initial Consenting OEM Roll-up Honda Chinese JV 23 0.0062715% - - 3 GHAC GAC Honda Automobile Co., Ltd. China Affiliate Non-Consenting OEM Honda Chinese JV 3,682 1.0220562% 3,682 1.0220562% 4 WDHAC Dongfeng Honda Automobile Co., Ltd. China Affiliate Non-Consenting OEM Honda Chinese JV 4,323 1.2000105% 4,323 1.2000105% 5 Toyota Toyota Japan CG Initial Consenting OEM Toyota 44,018 12.2181997% 48,881 13.5681391% 6 NUMMI New United Motor Manufacturing, Inc. US CG Initial Consenting OEM Roll-up Toyota 1,922 0.5335676% - - 7 Daihatsu Daihatsu Motor Co., Ltd. Japan Affiliate Initial Consenting OEM Roll-up Toyota owned (100% owned) 2,908 0.8072901% - - 8 HINO Hino Motors, Ltd. Japan Affiliate Initial Consenting OEM Roll-up Toyota affiliate 33 0.0090817% - - 9 GTMC GAC Toyota Motor Co., Ltd. China Affiliate (KSS) Non-Consenting OEM Toyota Chinese JV 602 0.1671380% 602 0.1671380% 10 TFTM Tianjin FAW Toyota Motor Co., Ltd. China Affiliate (KSS) Non-Consenting OEM Toyota Chinese JV 3,128 0.8683364% 3,128 0.8683364% 11 SFTM Sichuan FAW Toyota Motor Co., Ltd. -

V24n54a15.Pdf

Aportes a la investigación y a la docencia REVISTA INNOVARJOURNAL Building Chinese Cars in Mexico: The Grupo Salinas-FAW Alliance Álvaro Cuervo-Cazurra PhD from Massachusetts Institute of Technology and University of Salamanca. Professor. Northeastern University. Boston, USA. E-mail: [email protected] Miguel A. Montoya PhD from University of Barcelona. Professor. Tecnológico de Monterrey, campus Guadalajara. Mexico. E-mail: [email protected] PRODUCIR AUTOS CHINOS EN MéXICO: LA ALIANZA ENTRE EL GRUPO SALINAS Y FAW ABSTRACT: Ricardo Salinas Pliego was the CEO of Grupo Salinas, one of the largest business RESUMEN: Ricardo Salinas Pliego era el CEO del Grupo Salinas, uno de los groups in Mexico, and in 2009 he faced a challenge. Two years earlier, he had negotiated with mayores grupos empresariales de México, y en 2009 enfrentó un desafío. Dos años antes había negociado con FAW, la empresa automotriz china, the Chinese car company FAW to import Chinese cars into Mexico as an initial step towards their para importar autos chinos a México como un paso inicial hacia su manu- manufacturing. However, the global crisis of 2008 made him question the viability of the project factura. Sin embargo, la crisis global de 2008 le hizo cuestionar la viabi- lidad del proyecto y tuvo que decidir si cerrar la operación o continuar con and he had to decide whether to close the operation or continue in the hope of a quick recovery. la esperanza de una recuperación rápida. Fue una decisión difícil porque el This was a difficult decision because the group had sold several thousand cars and established grupo había vendido varios miles de carros y había establecido una red de concesionarios.