Research on Power Battery Full Life Cycle Asset Management

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CHINA FIELD TRIP May 10Th –12Th, 2011

CHINA FIELD TRIP May 10th –12th, 2011 This presentation may contain forward-looking statements. Such forward-looking statements do not constitute forecasts regarding the Company’s results or any other performance indicator, but rather trends or targets, as the case may be. These statements are by their nature subject to risks and uncertainties as described in the Company’s annual report available on its Internet website (www.psa-peugeot-citroen.com). These statements do not reflect future performance of the Company, which may materially differ. The Company does not undertake to provide updates of these statements. More comprehensive information about PSA PEUGEOT CITROËN may be obtained on its Internet website (www.psa-peugeot-citroen.com), under Regulated Information. th th China Field Trip - May 10 –12 , 2011 2 PSA in Asia – Market Forecast, PSA in China: ongoing successes and upsides Frédéric Saint-Geours Executive VP, Finance and Strategic Development Grégoire Olivier, Executive VP, Asia Table of contents Introduction China: the new auto superpower China: a global economic power The world’s largest automotive market The growth story is set to continue PSA in China China: a second home market for PSA 2 complementary JVs Key challenges in China and PSA differentiation factors A sustainable profitable growth Extending the Chinese Success ASEAN strategy Capturing the Indian opportunity th th China Field Trip - May 10 –12 , 2011 4 PSA – a global automotive player (1/2) > 39% of PSA’s 2010 sales are realized outside of Europe, of -

Analysis of the Dynamic Relationship Between the Emergence Of

Annals of Business Administrative Science 8 (2009) 21–42 Online ISSN 1347-4456 Print ISSN 1347-4464 Available at www.gbrc.jp ©2009 Global Business Research Center Analysis of the Dynamic Relationship between the Emergence of Independent Chinese Automobile Manufacturers and International Technology Transfer in China’s Auto Industry Zejian LI Manufacturing Management Research Center Faculty of Economics, the University of Tokyo E-mail: [email protected] Abstract: This paper examines the relationship between the emergence of independent Chinese automobile manufacturers (ICAMs) and International Technology Transfer. Many scholars indicate that the use of outside supplies is the sole reason for the high-speed growth of ICAMs. However, it is necessary to outline the reasons and factors that might contribute to the process at the company-level. This paper is based on the organizational view. It examines and clarifies the internal dynamics of the ICAMs from a historical perspective. The paper explores the role that international technology transfer has played in the emergence of ICAMs. In conclusion, it is clear that due to direct or indirect spillover from joint ventures, ICAMs were able to autonomously construct the necessary core competitive abilities. Keywords: marketing, international business, multinational corporations (MNCs), technology transfer, Chinese automobile industry but progressive emergence of independent Chinese 1. Introduction automobile manufacturers (ICAMs). It will also The purpose of this study is to investigate -

Development & Policy Forecast for Global and Chinese NEV Markets

Development & Policy Forecast for Global and Chinese NEV Markets in 2021 Invited by China EV 100, officials and experts from domestic and foreign government agencies, industry associations, research institutions and businesses attended the 7th China EV 100 Forum in January 15-17, 2021. The summary below captures the observations and insight of the speakers at the forum on the industry trend and policy forecast in the world and China in 2021. Ⅰ. 2021 Global & China Auto Market Trend 1. In 2021, the global auto market may resume growth, and the NEV boom is set to continue. 2020 saw a prevalent downturn of the auto sector in major countries due to the onslaught of COVID-19, yet the sales of NEVs witnessed a spike despite the odds, with much greater penetration in various countries. The monthly penetration of electric vehicles in Germany jumped from 7% to 20% in half a year and is expected to hit 12% in 2020, up 220% year on year; Norway reported an 80% market share of EVs in November, which is projected to exceed 70% for the whole year, topping the global ranking. Multiple consultancy firms foresee a comeback of global sales growth and a continuance of NEV boom in 2021 as coronavirus eases. 2. China's auto market as a whole is expected to remain stable in 2021, 1 with a strong boost in NEV sales. In 2020, China spearheaded global NEV market growth with record sales of 1.367 million units. The Development Research Center of the State Council expects overall auto sales to grow slightly in 2021, which ranges 0-2%. -

Chapter 2 China's Cars and Parts

Chapter 2 China’s cars and parts: development of an industry and strategic focus on Europe Peter Pawlicki and Siqi Luo 1. Introduction Initially, Chinese investments – across all industries in Europe – especially acquisitions of European companies were discussed in a relatively negative way. Politicians, trade unionists and workers, as well as industry representatives feared the sell-off and the subsequent rapid drainage of industrial capabilities – both manufacturing and R&D expertise – and with this a loss of jobs. However, with time, coverage of Chinese investments has changed due to good experiences with the new investors, as well as the sheer number of investments. Europe saw the first major wave of Chinese investments right after the financial crisis in 2008–2009 driven by the low share prices of European companies and general economic decline. However, Chinese investments worldwide as well as in Europe have not declined since, but have been growing and their strategic character strengthening. Chinese investors acquiring European companies are neither new nor exceptional anymore and acquired companies have already gained some experience with Chinese investors. The European automotive industry remains one of the most important investment targets for Chinese companies. As in Europe the automotive industry in China is one of the major pillars of its industry and its recent industrial upgrading dynamics. Many of China’s central industrial policy strategies – Sino-foreign joint ventures and trading market for technologies – have been established with the aim of developing an indigenous car industry with Chinese car OEMs. These instruments have also been transferred to other industries, such as telecommunications equipment. -

Fulbright-Hays Seminars Abroad Automobility in China Dr. Toni Marzotto

Fulbright-Hays Seminars Abroad Automobility in China Dr. Toni Marzotto “The mountains are high and the emperor is far away.” (Chinese Proverb)1 Title: The Rise of China's Auto Industry: Automobility with Chinese Characteristics Curriculum Project: The project is part of an interdisciplinary course taught in the Political Science Department entitled: The Machine that Changed the World: Automobility in an Age of Scarcity. This course looks at the effects of mass motorization in the United States and compares it with other countries. I am teaching the course this fall; my syllabus contains a section on Chinese Innovations and other global issues. This project will be used to expand this section. Grade Level: Undergraduate students in any major. This course is part of Towson University’s new Core Curriculum approved in 2011. My focus in this course is getting students to consider how automobiles foster the development of a built environment that comes to affect all aspects of life whether in the U.S., China or any country with a car culture. How much of our life is influenced by the automobile? We are what we drive! Objectives and Student Outcomes: My objective in teaching this interdisciplinary course is to provide students with an understanding of how the invention of the automobile in the 1890’s has come to dominate the world in which we live. Today an increasing number of individuals, across the globe, depend on the automobile for many activities. Although the United States was the first country to embrace mass motorization (there are more cars per 1000 inhabitants in the United States than in any other country in the world), other countries are catching up. -

Automotive Industry Weekly Digest

Automotive Industry Weekly Digest 12 Apr – 16 Apr 2021 IHS Markit Automotive Industry Weekly Digest - Apr 2021 WeChat Auto VIP Contents [OEM Highlights] GMC reveals Hummer electric SUV, ahead of early 2023 availability 3 [OEM Highlights] Xiaomi to invest up to USD10 bil. in EV production 6 [Sales Highlights] GM to unveil Envision Plus SUV on 18 April, reports sales growth of 69% y/y in China during Q1 8 [Sales Highlights] BYD posts sales growth of 33% y/y during March 9 [Shanghai Motor Show 2021] MG to unveil Cyberster sports car 11 [Shanghai Motor Show 2021] Xpeng to unveil P5 electric sedan 11 [GSP] Greater China Sales and Production Commentary -2021.03 13 [Supplier Trends and Highlights] HKT uses 5G standalone network with network slicing for trials of C-V2X applications 15 [Supplier Trends and Highlights] Commsignia combines cloud and V2X messaging in 4G, 5G V2N solution 15 Confidential. ©2021 IHS Markit. All rights reserved. 2 IHS Markit Automotive Industry Weekly Digest - Apr 2021 WeChat Auto VIP [OEM Highlights] GMC reveals Hummer electric SUV, ahead of early 2023 availability IHS Markit perspective Implications GMC has revealed the GMC Hummer electric SUV, debuted during a college basketball championship tournament on 3 April. The new EV is due in early 2023 as a 2024 model year product. Outlook Between the October 2020 reveal of the GMC Hummer electric pick-up and the Hummer electric SUV, GM has continued to push forward with announcements relative to investment and plans for an all-electric light-vehicle range by 2035. The GMC Hummer electric SUV and pick-up both are to set expectations on delivery of high levels of capability and performance. -

CHINA CORP. 2015 AUTO INDUSTRY on the Wan Li Road

CHINA CORP. 2015 AUTO INDUSTRY On the Wan Li Road Cars – Commercial Vehicles – Electric Vehicles Market Evolution - Regional Overview - Main Chinese Firms DCA Chine-Analyse China’s half-way auto industry CHINA CORP. 2015 Wan Li (ten thousand Li) is the Chinese traditional phrase for is a publication by DCA Chine-Analyse evoking a long way. When considering China’s automotive Tél. : (33) 663 527 781 sector in 2015, one may think that the main part of its Wan Li Email : [email protected] road has been covered. Web : www.chine-analyse.com From a marginal and closed market in 2000, the country has Editor : Jean-François Dufour become the World’s first auto market since 2009, absorbing Contributors : Jeffrey De Lairg, over one quarter of today’s global vehicles output. It is not Du Shangfu only much bigger, but also much more complex and No part of this publication may be sophisticated, with its high-end segment rising fast. reproduced without prior written permission Nevertheless, a closer look reveals China’s auto industry to be of the publisher. © DCA Chine-Analyse only half-way of its long road. Its success today, is mainly that of foreign brands behind joint- ventures. And at the same time, it remains much too fragmented between too many builders. China’s ultimate goal, of having an independant auto industry able to compete on the global market, still has to be reached, through own brands development and restructuring. China’s auto industry is only half-way also because a main technological evolution that may play a decisive role in its future still has to take off. -

Stanphyl Capital Management LLC Stanphyl Capital GP, LLC Stanphyl Capital Partners LP

Stanphyl Capital Management LLC Stanphyl Capital GP, LLC Stanphyl Capital Partners LP Friends and Fellow Investors: For June 2018 the fund was down approximately 13.8% (no that is not a misprint- please see the paragraph below) net of all fees and expenses. By way of comparison, the S&P 500 was up approximately 0.6% while the Russell 2000 was up approximately 0.7%. Year-to-date the fund is down approximately 16.2% while the S&P 500 is up approximately 2.6% and the Russell 2000 is up approximately 7.7%. Since inception on June 1, 2011 the fund is up approximately 67.4% net while the S&P 500 is up approximately 134.7% and the Russell 2000 is up approximately 113.7%. Since inception the fund has compounded at approximately 7.6% net annually vs 12.8% for the S&P 500 and 11.3% for the Russell 2000. (The S&P and Russell performances are based on their “Total Returns” indices which include reinvested dividends.) As always, investors will receive the fund’s exact performance figures from its outside administrator within a week or two; meanwhile I continue to waive the annual management fee until the entire fund regains its high- water mark. The fund was absolutely massacred this month, and it was primarily due to our large short position in Tesla, to which I added on each new piece of negative news, much of which was indicative of the kind of outright fraud (see below) that would immediately send a “normal stock” into a death spiral, and yet for most of the month Tesla’s stock kept levitating. -

P020110307527551165137.Pdf

CONTENT 1.MESSAGE FROM DIRECTOR …………………………………………………………………………………………………………………………………………………… 03 2.ORGANIZATION STRUCTURE …………………………………………………………………………………………………………………………………………………… 05 3.HIGHLIGHTS OF ACHIEVEMENTS …………………………………………………………………………………………………………………………………………… 06 Coexistence of Conserve and Research----“The Germplasm Bank of Wild Species ” services biodiversity protection and socio-economic development ………………………………………………………………………………………………………………………………………………… 06 The Structure, Activity and New Drug Pre-Clinical Research of Monoterpene Indole Alkaloids ………………………………………… 09 Anti-Cancer Constituents in the Herb Medicine-Shengma (Cimicifuga L) ……………………………………………………………………………… 10 Floristic Study on the Seed Plants of Yaoshan Mountain in Northeast Yunnan …………………………………………………………………… 11 Higher Fungi Resources and Chemical Composition in Alpine and Sub-alpine Regions in Southwest China ……………………… 12 Research Progress on Natural Tobacco Mosaic Virus (TMV) Inhibitors…………………………………………………………………………………… 13 Predicting Global Change through Reconstruction Research of Paleoclimate………………………………………………………………………… 14 Chemical Composition of a traditional Chinese medicine-Swertia mileensis……………………………………………………………………………… 15 Mountain Ecosystem Research has Made New Progress ………………………………………………………………………………………………………… 16 Plant Cyclic Peptide has Made Important Progress ………………………………………………………………………………………………………………… 17 Progresses in Computational Chemistry Research ………………………………………………………………………………………………………………… 18 New Progress in the Total Synthesis of Natural Products ……………………………………………………………………………………………………… -

State of Automotive Technology in PR China - 2014

Lanza, G. (Editor) Hauns, D.; Hochdörffer, J.; Peters, S.; Ruhrmann, S.: State of Automotive Technology in PR China - 2014 Shanghai Lanza, G. (Editor); Hauns, D.; Hochdörffer, J.; Peters, S.; Ruhrmann, S.: State of Automotive Technology in PR China - 2014 Institute of Production Science (wbk) Karlsruhe Institute of Technology (KIT) Global Advanced Manufacturing Institute (GAMI) Leading Edge Cluster Electric Mobility South-West Contents Foreword 4 Core Findings and Implications 5 1. Initial Situation and Ambition 6 Map of China 2. Current State of the Chinese Automotive Industry 8 2.1 Current State of the Chinese Automotive Market 8 2.2 Differences between Global and Local Players 14 2.3 An Overview of the Current Status of Joint Ventures 24 2.4 Production Methods 32 3. Research Capacities in China 40 4. Development Focus Areas of the Automotive Sector 50 4.1 Comfort and Safety 50 4.1.1 Advanced Driver Assistance Systems 53 4.1.2 Connectivity and Intermodality 57 4.2 Sustainability 60 4.2.1 Development of Alternative Drives 61 4.2.2 Development of New Lightweight Materials 64 5. Geographical Structure 68 5.1 Industrial Cluster 68 5.2 Geographical Development 73 6. Summary 76 List of References 78 List of Figures 93 List of Abbreviations 94 Edition Notice 96 2 3 Foreword Core Findings and Implications . China’s market plays a decisive role in the . A Chinese lean culture is still in the initial future of the automotive industry. China rose to stage; therefore further extensive training and become the largest automobile manufacturer education opportunities are indispensable. -

Chinese Medical Journal Volume 127 September 30, 2014 Supplement 2

Chinese Medical Journal Volume 127 September 30, 2014 Supplement 2 Report on Cardiovascular Diseases in China 2012 Outline of report on cardiovascular diseases in China 1 Writing Committee of Annual Report on Cardiovascular Diseases in China Cardiovascular diseases 6 Liu Mingbo Hypertension 8 Wang Zengwu Hypertension in children and adolescents 16 Mi Jie, Dong Hongbo Tobacco use and its association with cardiovascular disease in China 21 Yang Xiaohui, Ma Changsheng Dyslipidemia 26 Li Ying Diabetes mellitus in China’s adult 31 Lu Zuqian, Xu Zhangrong, Li Guangwei Overweight and obesity, deficiency of physical activities, and diet and nutrition 39 Zhao Liancheng, PengYaguang Prevalence rate of metabolic syndrome 43 Zuo Huijuan Epidemiological studies of coronary heart disease 45 Zeng Zhechun Clinical study on coronary heart disease 49 Wang Chunning Stroke in China: prevalence, mortality, and trends 55 Wang Jinwen Clinical study on stroke 57 Du Wanliang, Wang Jinwen, Wang Yongjun Chronic kidney disease in China 61 Wang Yu Cardiovascular surgery 64 Luo Xinjin, Hu Shengshou Peripheral arterial disease 68 Li Xiaoying Cardiac arrhythmia in China 71 Zhang Shu, Fan Xiaohan, Ning Xiaohui Pulmonary hypertension 76 Li Wen, Yang Tao, Jing Xiaoli, He Jianguo Heart failure 79 Zhang Jian Community-based prevention and control of cardiovascular diseases 83 Chen Weiwei Medical expenditure of cardiovascular diseases 85 Liu Kejun About Chinese Medical Journal Chinese Medical Journal (CMJ) is a fully open-access, international peer reviewed general medical journal, published semimonthly in English by the Chinese Medical Association. Established in 1887, now CMJ is the oldest medical periodical in China and distributed worldwide. The Journal is abstracted and/or indexed in Biological Abstracts, Chemical Abstracts, Science Citation Index (SCI), Embase, Social Scisearch, etc. -

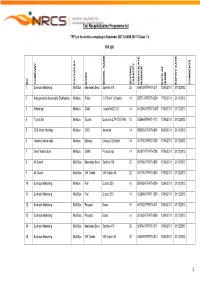

TRP Programme List July Revision 64

- 1 -Last saved by nthitemd - 1 -19 Taxi Recapitalization Programme list TRP List for vehicles complying to September 2007 & SANS 20107 Clause 7.6 TRP 2009 ISSUE DATE EXPIRY COMMENTS NO COMPANY CATEGORY NAME MODEL NAME SEATING CAPACITY CERTIFICATE NUMBER OF DATE 1 Bustruck Marketing Midi Bus Mercedes Benz Sprinter 518 22 556739-TRP07-0311 13/06/2011 31/12/2013 2 Amalgamated Automobile Distributors Minibus Foton 2.2 Petrol 13 Seater 14 550713-TRP07-0309 17/06/2011 31/12/2013 3 Whallinger Minibus CAM Inyathi XGD 2.2i 14 541394-TRPO7-0609 17/06/2011 31/12/2013 4 Toyota SA Minibus Toyota Quantum 2.7P 15S TAXI 15 555664-TRP07-1110 17/06/2011 31/12/2013 5 CCE Motor Holdings Minibus CMC Amandla 14 550826-TRP07-0609 20/06/2011 31/12/2013 6 Nanfeng Automobile Minibus Ekhaya Ekhaya 2.2i Hatch 14 551700-TRP07-0709 17/06/2011 31/12/2013 7 Great Wall motors Minibus GWM Proteus Mpi 14 551517-TRP07-0709 17/06/2011 31/12/2013 8 Mr Coach Midi Bus Mercedes Benz Sprinter 518 22 551798-TRP07-0809 17/06/2011 31/12/2013 9 Mr Coach Midi Bus VW Crafter VW Crafter 50 22 551799-TRP07-0809 17/06/2011 31/12/2013 10 Bustruck Marketing Minibus Fiat Ducato 250 16 551958-TRP07-0809 13/06/2011 31/12/2013 11 Bustruck Marketing Midi Bus Fiat Ducato 250 19 552898-TRP07-1209 13/06/2011 31/12/2013 12 Bustruck Marketing Midi Bus Peugeot Boxer 19 557082-TRP07-0411 13/06/2011 31/12/2013 13 Bustruck Marketing Midi Bus Peugeot Boxer 16 551959-TRP07-0809 13/06/2011 31/12/2013 14 Bustruck Marketing Midi Bus Mercedes Benz Sprinter 416 22 556740-TRP07-0311 13/06/2011 31/12/2013 15