Study of U.S. Inland Containerized Cargo Moving Through Canadian and Mexican Seaports

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Port of Prince Rupert Delivers Another Record Year

Port of Prince Rupert Delivers Another Record Year rupertport.com The Prince Rupert Port Authority (PRPA) announced today another record year in volume. A grand total of 29.9 million tonnes of cargo moved through the Port of Prince Rupert in 2019 – 12% more than the 26.7 million tonnes handled the previous year and the highest total volume to date for the Port. Supporting the overall positive trend was strong Follow the BCMEA performance at DP World’s Fairview Container Terminal with over 1.2 million TEUs at an increase on social media of 17% over 2018, the addition of propane volume through AltaGas’ Ridley Island Propane Export Terminal, and growth in coal handled at Ridley Terminal where cargo levels were up 18% over the previous year. (continued) We’re looking for your good news stories to share! Please submit to Grace Sullivan: [email protected] 500 – 349 Railway Street, Vancouver, British Columbia V6A 1A4 604.688.1155 www.bcmea.com January 16, 2020 The BCMEA Bulletin January 16, 2020 Port of Prince Rupert Delivers Another Record Year (continued) Northland Cruise Terminal also saw a year-over-year increase in passenger volumes of 35%, totalling over 12,400 visitors to Prince Rupert through cruise travel. “The Port of Prince Rupert’s consistent record-breaking annual volumes confirms the Port’s growing role in Canadian trade,” said Shaun Stevenson, President and CEO of the Prince Rupert Port Authority. “The Port of Prince Rupert has a reputation for offering strategic advantages to shippers. The 2019 volumes illustrate the growing market demand for the Prince Rupert gateway and further validates our plans for growth and expansion over the next several years.” PRPA’s latest economic impact study released in 2019 revealed that port-related growth has resulted in the Port of Prince Rupert handling approximately $50 billion in trade value annually and supports an estimated 3,600 direct supply-chain jobs in northern BC, $310 million in annual wages, and $125.5 million in annual government revenue. -

WCCC Board of Directors Quarterly Meeting

WCCC Board of Directors Quarterly Meeting Tuesday, April 21 – Wednesday, April 22, 2009 Hosts: Alaska Department of Transportation and Public Facilities and the Alaska Railroad Corporation 327 W Ship Creek Avenue Anchorage, Alaska 99501 (Note: All Times as Alaska Daylight Time – 1 Hour Earlier than WA, OR, CA) SANDAG Staff Contact: Linda Culp, (619) 699-6957; [email protected] Conference Call Information For All Meetings: 1-877-356- 9437, Access Code 9805119 Tuesday, April 21, 2009 2:00 pm ITS, Operations, and Environment Committee Alternative Fuel Corridor Program Climate Change Activities Alaska Environmental Strategies Best Practices Manual Wednesday, April 22, 2009 8:30 am WCCC Board of Directors Coalition Business Plan Outreach Program Funding Opportunities Goods Movement Committee Federal Relations Committee Marad Port and Intermodal System Report Goods Movement in Alaska 2:00 pm Adjourn www.westcoastcorridors.org MEETING LOCATION Meetings are being hosted by the Alaska Department of Transportation and Public Facilities and the Alaska Railroad Corporation. The physical location will be at the Railroad Corporation: Alaska Railroad Corporation 327 W Ship Creek Avenue Anchorage, Alaska 99501 Offices are about 7 miles from the Ted Stevens Anchorage International Airport. Please RSVP for the meeting as we may have transportation arranged to and from the airport and we’ll need your name for security reasons at the office. 2 ITS, Operations and Environment Committee Tuesday, April 21, 2009 2:00 PM Bruce Agnew, Rex Burkholder, Co-Chairs Agenda ITEM # ACTION 1. WELCOME AND INTRODUCTIONS (Bruce Agnew, Co-Chair) 2. ALTERNATIVE FUEL CORRIDOR PROGRAM: +2A. INTERSTATE CLEAN TRANSPORTATION CORRIDOR INFORMATION (Cliff Gladstein, President, Gladstein & Neandross) This program, started in 1996, has led to $50 million for alternative fueling stations on parts of I-5, CA-99, I-10, I-15, and I-80 in California, Nevada, and Utah. -

Ohio, Ex-Seatrain Ohio

NATIONAL REGISTER ELIGIBILITY ASSESSMENT VESSEL: SS Ohio, ex-Seatrain Ohio Seatrain Puerto Rico, the first in a line of seven converted T2 tankers and sistership of the Ohio, underway circa late 1960s. Victory Ships and Tankers, L.A. Sawyer and W.H. Mitchell Vessel History The Seatrain Ohio was built in 1967 as a combination railway car/container‐carrying vessel for Seatrain Lines, Inc. of New York. It was constructed by recombining modified sections from three WWII T2 class tankers.1 The ship spent its active career on charter to the U.S. Military Sea Transportation Service (MSTS),2 which later became the Military Sealift Command (MSC). Engineer Graham M. Brush founded Seatrain Lines in 1928 to ferry railway cars loaded with goods between New Orleans, Louisiana and Havana, Cuba. The vessels were fitted with tracks and other special equipment so that railcars could move directly from the docks into the ships’ holds. The first vessel he adapted to carry railcars was a cargo ship. This vessel, the Seatrain New Orleans, carried loaded freight cars from New Orleans to Cuba for the first time in January of 1929. There were many advantages to this new service. It cut down on the amount of time 1 The T2 tanker, or T2, was an oil tanker constructed and produced in large quantities in the U.S. during World War II. The largest "navy oilers" at the time, nearly 500 of them, were built between 1940 and the end of 1945. 2 MSTS was a post-World War II combination of four predecessor government agencies that handled similar sealift functions. -

BERTH PRODUCTIVITY the Trends, Outlook and Market Forces Impacting Ship Turnaround Times

JULY 2014 BERTH PRODUCTIVITY The Trends, Outlook and Market Forces Impacting Ship Turnaround Times JOC Port Productivity Brought to you by JOC, powered by PIERS JOC Group Inc. WHITEPAPER, JULY 2014 BERTH PRODUCTIVITY: The Trends, Outlook and Market Forces Impacting Ship Turnaround Times TABLE OF CONTENTS Introduction. 1 Berth Productivity . 3 The Trends, Outlook and Market Forces Impacting Ship Turnaround Times Asia’s Troubled Outlook . 9 Why a Steady Dose of Mega-ships Limits the Potential for Berth Productivity Gains Racing the Clock in Europe . .11 Big Projects Pave the Way for the World’s Biggest Ships Behind the Port Productivity Numbers . .14 About the JOC Port Productivity Rankings. 16 The Rankings. 17 Validation Methodology. 23 Rankings Methodology . .23 About the Report. .24 About JOC Group Inc. .24 TABLES Rankings the Ports . 17 Top Ports: Worldwide . 17 Top Ports: Americas. .18 Top Ports: Asia. .18 Top Ports: Europe, Middle East, Africa. 18 Rankings the Terminals. .19 Top Terminals: Worldwide. .19 Top Terminals: Americas . .19 Top Terminals: Asia . .20 Top Terminals: Europe, Middle East, Africa . .20 Port Productivity by Ship Size. 21 Top Ports Globally, VESSELS LESS THAN 8,000 TEUS . .21 Top Terminals Globally, 8,000-TEU VESSELS AND LARGER . .21 Top Terminals Globally, VESSELS LESS THAN 8,000 TEUS . 22 Top Ports Globally, VESSELS 8,000+ TEUS . 22 +1.800.952.3839 | www.joc.com | www.piers.com ii © Copyright JOC Group Inc. 2014 WHITEPAPER, JULY 2014 BERTH PRODUCTIVITY: The Trends, Outlook and Market Forces Impacting Ship Turnaround Times Introduction ENHANCING BERTH PRODUCTIVITY By Peter Tirschwell Executive Vice If there’s an issue in the container shipping world that’s hotter than port President/Chief productivity, I’m not aware of it. -

I-15 Corridor System Master Plan Update 2017

CALIFORNIA NEVADA ARIZONA UTAH I-15 CORRIDOR SYSTEM MASTER PLAN UPDATE 2017 MARCH 2017 ACKNOWLEDGEMENTS The I-15 Corridor System Master Plan (Master Plan) is a commerce, port authorities, departments of aviation, freight product of the hard work and commitment of each of the and passenger rail authorities, freight transportation services, I-15 Mobility Alliance (Alliance) partner organizations and providers of public transportation services, environmental their dedicated staff. and natural resource agencies, and others. Individuals within the four states and beyond are investing Their efforts are a testament of outstanding partnership and their time and resources to keep this economic artery a true spirit of collaboration, without which this Master Plan of the West flowing. The Alliance partners come from could not have succeeded. state and local transportation agencies, local and interstate I-15 MOBILITY ALLIANCE PARTNERS American Magline Group City of Orem Authority Amtrak City of Provo Millard County Arizona Commerce Authority City of Rancho Cucamonga Mohave County Arizona Department of Transportation City of South Salt Lake Mountainland Association of Arizona Game and Fish Department City of St. George Governments Bear River Association of Governments Clark County Department of Aviation National Park Service - Lake Mead National Recreation Area BNSF Railway Clark County Public Works Nellis Air Force Base Box Elder County Community Planners Advisory Nevada Army National Guard Brookings Mountain West Committee on Transportation County -

Chapter 5: Freight Rail

Chapter 5: Freight Rail Table of Contents Introduction .................................................................................................................................................. 3 Wisconsin’s Rail Freight Network ............................................................................................................. 3 History of freight rail in Wisconsin ........................................................................................................ 3 WisDOT’s response to changes in statewide freight rail service .......................................................... 4 Milwaukee Road ................................................................................................................................... 4 Rail Transit Commissions ...................................................................................................................... 4 Wisconsin’s current freight rail network .............................................................................................. 5 Freight rail classifications ...................................................................................................................... 5 Commodities moved ............................................................................................................................. 6 2030 freight shipments forecast ........................................................................................................... 8 Wisconsin’s intermodal facilities ....................................................................................................... -

Eastern Canada Ports Battle for Mega-Ship Calls Peter Ford, Principal, Skyrock Advisors, LLC, and Dr

Analysis: Eastern Canada ports battle for mega-ship calls Peter Ford, principal, SkyRock Advisors, LLC, and Dr. Jean-Paul Rodrigue, professor of global studies & geography, Hofstra University May 23, 2018 3:59PM EDT The Port of Montreal is the largest on Canada's east coast. [Photo credit: Port of Montreal.] Every new terminal or port development has risks, particularly in a mature market with established stakeholders. The risk can be mitigated if container volumes have a pronounced upward trend, but the financial crisis of 2007-2008 has shifted growth expectations closer to the range of 2 to 3 percent annual growth rate at the global level, but around 5 percent for the North American East Coast. Still, these figures are subject to caution considering growing trade contentions as well as technological changes in global manufacturing and supply chains with the outsourcing and offshoring model being reconsidered. Ocean carriers have responded to this environment by unprecedented industry consolidation, with more merger and acquisition activity happening in the last three years than in the decade preceding, and then further consolidating into mega-alliances with lines focusing on larger vessels to create scale economies and reduce slot costs. Many shipping lines are also involved in container terminal operations with various concession and ownership schemes. 1. All is not quiet on the East Coast front The Canadian East Coast has been a very stable market in the last 50 years with established ports, mainly Montreal and Halifax, assuming dominance. While Montreal experienced a growth relatively on par with the US East Coast, the volumes handled by Halifax barely changed in the last 20 years but have recently shown sign of upward momentum due to new services. -

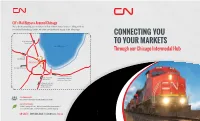

Connecting You to Your Markets

CN's Rail Bypass Around Chicago We've been connecting our customers to their markets faster for years. Along with our streamlined interchange points, we offer a truly efficient supply chain advantage. CONNECTING YOU to Vancouver and Prince Rupert TO YOUR MARKETS Lake Michigan Through our Chicago Intermodal Hub to the U.S. Midwest CHICAGO CN’s bypass rail line to Toronto and the east to Decatur and coast ports of Montreal, Indianapolis Halifax and Saint John to Memphis and the Gulf ports of Mobile and New Orleans CUSTOMER SERVICE One point of contact for all your supply chain needs. OUR GREEN PROMISE CN Rail is energy efficient. We are committed to environmental initiatives that make us the best choice for greener shipping. CN SALES | 1-888-668-4626 | [email protected] | cn.ca CN012020 Port of Prince Rupert Port of Vancouver Port of Halifax Port of The superior network solution Montreal Toronto NY/NJ for all your supply chain logistics Chicago Philadelphia CN provides a one-stop shop, including freight forwarding to Wilmington move your product along the best supply chain routes. Through our partnerships with ocean carriers and major Canadian port gateways, we offer a single line seamless service from last port of call in Asia to Chicago in only 16 days. Port of Mobile Port of New Orleans • 23 intermodal terminals across North America PORT OF PORT OF PORT OF PORT OF PORT OF PORT OF TRANSIT TIME Prince Rupert Vancouver Montreal Halifax New Orleans Mobile • Network reach to 3 coasts serving multiple TORONTO 5th am 5th am same day pm 2nd am 3rd pm 3rd pm Canadian and U.S. -

Review of Maritime Transport 2018 65

4 In 2017, global port activity and cargo handling of containerized and bulk cargo expanded rapidly, following two years of weak performance. This expansion was in line with positive trends in the world economy and seaborne trade. Global container terminals boasted an increase in volume of about 6 per cent during the year, up from 2.1 per cent in 2016. World container port throughput stood at 752 million TEUs, reflecting an additional 42.3 million TEUs in 2017, an amount comparable to the port throughput of Shanghai, the world’s busiest port. While overall prospects for global port activity remain bright, preliminary figures point to decelerated growth in port volumes for 2018, as the growth impetus of 2017, marked by cyclical recovery and supply chain restocking factors, peters out. In addition, downside risks weighing on global shipping, such as trade policy risks, geopolitical factors and structural shifts in economies such as China, also portend a decline in port activity. Today’s port-operating landscape is characterized by heightened port competition, especially in the container market segment, where decisions by shipping alliances regarding capacity deployed, ports of call and network structure can determine the fate of a container port terminal. The framework is also being influenced by wide- PORTS ranging economic, policy and technological drivers of which digitalization is key. More than ever, ports and terminals around the world need to re-evaluate their role in global maritime logistics and prepare to embrace digitalization- driven innovations and technologies, which hold significant transformational potential. Strategic liner shipping alliances and vessel upsizing have made the relationship between container lines and ports more complex and triggered new dynamics, whereby shipping lines have stronger bargaining power and influence. -

Baja California, Mexico, and a Vegetation Map of Colonet Mesa Alan B

Aliso: A Journal of Systematic and Evolutionary Botany Volume 29 | Issue 1 Article 4 2011 Plants of the Colonet Region, Baja California, Mexico, and a Vegetation Map of Colonet Mesa Alan B. Harper Terra Peninsular, Coronado, California Sula Vanderplank Rancho Santa Ana Botanic Garden, Claremont, California Mark Dodero Recon Environmental Inc., San Diego, California Sergio Mata Terra Peninsular, Coronado, California Jorge Ochoa Long Beach City College, Long Beach, California Follow this and additional works at: http://scholarship.claremont.edu/aliso Part of the Biodiversity Commons, Botany Commons, and the Ecology and Evolutionary Biology Commons Recommended Citation Harper, Alan B.; Vanderplank, Sula; Dodero, Mark; Mata, Sergio; and Ochoa, Jorge (2011) "Plants of the Colonet Region, Baja California, Mexico, and a Vegetation Map of Colonet Mesa," Aliso: A Journal of Systematic and Evolutionary Botany: Vol. 29: Iss. 1, Article 4. Available at: http://scholarship.claremont.edu/aliso/vol29/iss1/4 Aliso, 29(1), pp. 25–42 ’ 2011, Rancho Santa Ana Botanic Garden PLANTS OF THE COLONET REGION, BAJA CALIFORNIA, MEXICO, AND A VEGETATION MAPOF COLONET MESA ALAN B. HARPER,1 SULA VANDERPLANK,2 MARK DODERO,3 SERGIO MATA,1 AND JORGE OCHOA4 1Terra Peninsular, A.C., PMB 189003, Suite 88, Coronado, California 92178, USA ([email protected]); 2Rancho Santa Ana Botanic Garden, 1500 North College Avenue, Claremont, California 91711, USA; 3Recon Environmental Inc., 1927 Fifth Avenue, San Diego, California 92101, USA; 4Long Beach City College, 1305 East Pacific Coast Highway, Long Beach, California 90806, USA ABSTRACT The Colonet region is located at the southern end of the California Floristic Province, in an area known to have the highest plant diversity in Baja California. -

2012 Corridor System Master Plan

MARCH 2012 CALIFORNIANEVADAARIZONAUTAH I-15 CORRIDOR SYSTEM MASTER PLAN MOVINGPEOPLE MOVINGGOODS Acknowledgements The I-15 Corridor System Master Plan (Master Plan) and the • City of Orem associated technical studies are products of the hard work and • City of Rancho Cucamonga commitment of each of the I-15 Mobility Alliance (Alliance) partner organizations and their dedicated staff. Their efforts are a • City of South Salt Lake testament of outstanding partnership and a true spirit of collabo- • City of St. George ration, without which this Master Plan could not have succeeded. • Clark County Department of Aviation Susan Martinovich, Director of the Nevada Department of Transportation (NDOT) and 2011 American Association of State • Clark County Public Works Highway Transportation Officials (AASHTO) President, served • County of San Bernardino as the Chair of the Alliance’s Executive Board and, through her agency, provided the initial funding for this effort. Without this • DesertXpress support, the creation of the Master Plan and Alliance would not • Economic Development Corporation of Utah have been possible. Her leadership and vision were an inspiration to all those participating in the Alliance. • El Dorado Holdings • Envision Utah I-15 Mobility Alliance Partners • Federal Highway Administration The I-15 Mobility Alliance partners that have participated in this • Federal Railroad Administration effort are listed below in alphabetical order. • Five County Association of Governments • American Magline Group • Freeway and Arterial System -

NCIT the National Center for Intermodal Transportation

NCIT The National Center for Intermodal Transportation INTERMODAL TRANSPORTATION SYSTEM FOR ASIAN GOODS TO U.S. VIA MEXICO: AN ANALYSIS JUNE 2010 Ismail Capar, Arunachalam Narayanan, Malini Natarajarathinam Industrial Distribution Program Texas A&M University, College Station, TX – 77843‐3367 1 DISCLAIMER The contents of this report reflect the views of the authors, who are responsible for the facts and the accuracy of the information presented herein. This document is disseminated under the sponsorship of the Department of Transportation University Transportation Centers Program, in the interest of information exchange. The U.S. Government assumes no liability for the contents or use thereof. 2 TABLE OF CONTENTS Introduction ........................................................................................................................................ 5 Trade Data ................................................................................................................................................. 5 Road infrastructure: ........................................................................................................................... 8 Technical evaluation of Regional Logistical Infrastructure ............................................................... 9 Highway corridor 2012: ............................................................................................................................ 9 Ranking the Highway Corridor road networks: .....................................................................................