06-15 Gov Transactiondetail with Notes

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Remote Desktop Redirected Printer

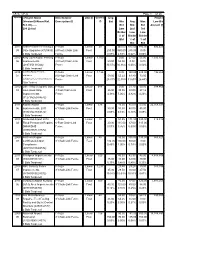

%F-% %F-% Page 1 of 26 Opened --Project Name Item Number Unit (f) Quantity Eng Project (VersionID/Aksas/Ref. Description (f) (f) Est Min Avg Max Low Bid Std. ID)------ Bid Bid Bid Amount (f) 286 Listed Low 2nd 3rd Bidder Low Low % of Bidder Bidder Bid % of % of Bid Bid 2017 Sitka Perimeter Fencing & F-162a Linear 20 245.00 612.50 980.00 692,400 08 Gate Upgrades (47258//0) (8 Foot) Chain-Link Foot 250.00 980.00 245.00 0.00 2 Bids Tendered Fence 0.87% 2.83% 0.62% 0.00% 2010 King Cove Airport Fencing F-162a Linear 7,700 0.00 27.50 55.00 1,395,100 06 Improvements (8 Foot) Chain-Link Foot 59.00 55.00 0.00 0.00 (28973/51335/64) Fence 30.37% 30.36% 0.00% 0.00% 2 Bids Tendered 2014 Cold Bay Airport Fencing F-162a Linear 1,126 0.00 100.04 244.00 192,264 01 and Gates [8'] High Chain-Link Foot 59.00 55.23 61.80 73.00 (42046/14-25-1-013/56779/4572) Fence 28.31% 32.35% 31.65% 26.44% 7 Bids Tendered 2010 Lake Hood Seaplane Base F-162a Linear 648 0.00 21.79 30.05 384,465 09 Lake Hood Strip 4 Foot Chain-Link Foot 25.00 30.05 30.00 27.12 Improvements Fence 4.39% 5.06% 4.82% 4.20% (31273/52597/4572) 4 Bids Tendered 2011 Kodiak Airport F-162a Linear 576 40.00 45.00 50.00 22,758,321 06 Improvements, 2011 6' Chain-Link Fence Foot 50.00 50.00 40.00 45.00 (33348/52739/4572) 0.09% 0.13% 0.10% 0.09% 3 Bids Tendered 2013 Girdwood Airport 2012 F-162a Linear 13 54.55 171.93 320.00 415,812 02 Flood Permanent Repairs 6-Foot Chain-Link Foot 20.00 115.00 87.00 315.00 DMVA/DHS Fence 0.07% 0.36% 0.00% 0.00% (39936/55713/4572) 6 Bids Tendered 2009 Northern Region F-162a -

Aviation Advisory Board Meeting Minutes August 5-6, 2010 in Unalakleet, Alaska

Aviation Advisory Board Meeting Minutes August 5-6, 2010 in Unalakleet, Alaska Chairman Lee Ryan called meeting to order at 9:05am. PRESENT: Lee Ryan, Jim Dodson, Tom George, Tom Nicolos, Mike Salazar, Mike Stedman, Judy McKenzie, Frank Neitz, Steve Strait EXCUSED ABSENCE: Al Orot, Ken Lythgoe OTHERS IN ATTENDANCE: Marc Luiken (DOT&PF), Rebecca Cronkhite (DOT&PF), Jeff Roach (DOT&PF), Linda Bustamante (DOT&PF), Commissioner Leo von Scheben (DOT&PF), Harry Johnson, Jr. - Unalakleet Airport Manager, Laura Lawrence – Staff to Senator Donny Olson, Representative Neal Foster, Chuck Degnan, Jim Tweto. MINUTES: Approved by the board prior to meeting – via email. Agenda Addition – Add time for public comments to agenda which could happen throughout the day as the public stops in for the meeting. Announcement from Deputy Commissioner: Deputy Commissioner Luiken thanked Chairman Lee Ryan for hosting the meeting in Unalakleet and welcomed new board members, Tom Nicolos and Mike Stedman. AGENDA: Alaska International Airports System (AIAS) and Statewide Aviation Update: Deputy Commissioner Luiken provided an overview of the AIAS. Marketing efforts of the Anchorage Airport include: 1. Plans to hire two key positions - marketing and air service development. 2. Interview with Supply Chain Management for an online story 3. Air Cargo Summit – International carriers invited to meet with representative from U.S. DOT to better understand the unique cargo transfer rights available in Alaska and to review fuel supply issues. The State is conducting a study to review fuel storage and all aspects of fuel availability at the international airports. Public Comment: Junior Johnson, Unalakleet Airport Manager expressed concern over Emmonak Airport not having a village contractor. -

(Asos) Implementation Plan

AUTOMATED SURFACE OBSERVING SYSTEM (ASOS) IMPLEMENTATION PLAN VAISALA CEILOMETER - CL31 November 14, 2008 U.S. Department of Commerce National Oceanic and Atmospheric Administration National Weather Service / Office of Operational Systems/Observing Systems Branch National Weather Service / Office of Science and Technology/Development Branch Table of Contents Section Page Executive Summary............................................................................ iii 1.0 Introduction ............................................................................... 1 1.1 Background.......................................................................... 1 1.2 Purpose................................................................................. 2 1.3 Scope.................................................................................... 2 1.4 Applicable Documents......................................................... 2 1.5 Points of Contact.................................................................. 4 2.0 Pre-Operational Implementation Activities ............................ 6 3.0 Operational Implementation Planning Activities ................... 6 3.1 Planning/Decision Activities ............................................... 7 3.2 Logistic Support Activities .................................................. 11 3.3 Configuration Management (CM) Activities....................... 12 3.4 Operational Support Activities ............................................ 12 4.0 Operational Implementation (OI) Activities ......................... -

Notice of Adjustments to Service Obligations

Served: May 12, 2020 UNITED STATES OF AMERICA DEPARTMENT OF TRANSPORTATION OFFICE OF THE SECRETARY WASHINGTON, D.C. CONTINUATION OF CERTAIN AIR SERVICE PURSUANT TO PUBLIC LAW NO. 116-136 §§ 4005 AND 4114(b) Docket DOT-OST-2020-0037 NOTICE OF ADJUSTMENTS TO SERVICE OBLIGATIONS Summary By this notice, the U.S. Department of Transportation (the Department) announces an opportunity for incremental adjustments to service obligations under Order 2020-4-2, issued April 7, 2020, in light of ongoing challenges faced by U.S. airlines due to the Coronavirus (COVID-19) public health emergency. With this notice as the initial step, the Department will use a systematic process to allow covered carriers1 to reduce the number of points they must serve as a proportion of their total service obligation, subject to certain restrictions explained below.2 Covered carriers must submit prioritized lists of points to which they wish to suspend service no later than 5:00 PM (EDT), May 18, 2020. DOT will adjudicate these requests simultaneously and publish its tentative decisions for public comment before finalizing the point exemptions. As explained further below, every community that was served by a covered carrier prior to March 1, 2020, will continue to receive service from at least one covered carrier. The exemption process in Order 2020-4-2 will continue to be available to air carriers to address other facts and circumstances. Background On March 27, 2020, the President signed the Coronavirus Aid, Recovery, and Economic Security Act (the CARES Act) into law. Sections 4005 and 4114(b) of the CARES Act authorize the Secretary to require, “to the extent reasonable and practicable,” an air carrier receiving financial assistance under the Act to maintain scheduled air transportation service as the Secretary deems necessary to ensure services to any point served by that air carrier before March 1, 2020. -

APPENDIX a Document Index

APPENDIX A Document Index Alaska Aviation System Plan Document Index - 24 April 2008 Title Reference # Location / Electronic and/or Paper Copy Organization / Author Pub. Date Other Comments / Notes / Special Studies AASP's Use 1-2 AASP #1 1 WHPacific / Electronic & Paper Copies DOT&PF / TRA/Farr Jan-86 Report plus appendix AASP #2 DOT&PF / TRA-BV Airport 2 WHPacific / Electronic & Paper Copies Mar-96 Report plus appendix Consulting Statewide Transportation Plans Use 10 -19 2030 Let's Get Moving! Alaska Statewide Long-Range http://dot.alaska.gov/stwdplng/areaplans/lrtpp/SWLRTPHo 10 DOT&PF Feb-08 Technical Appendix also available Transportation Policy Plan Update me.shtml Regional Transportation Plans Use 20-29 Northwest Alaska Transportation Plan This plan is the Community Transportation Analysis -- there is 20 http://dot.alaska.gov/stwdplng/areaplans/nwplan.shtml DOT&PF Feb-04 also a Resource Transportation Analysis, focusing on resource development transportation needs Southwest Alaska Transportation Plan 21 http://dot.alaska.gov/stwdplng/areaplans/swplan.shtml DOT&PF / PB Consult Sep-04 Report & appendices available Y-K Delta Transportation Plan 22 http://dot.alaska.gov/stwdplng/areaplans/ykplan.shtml DOT&PF Mar-02 Report & appendices available Prince William Sound Area Transportation Plan 23 http://dot.alaska.gov/stwdplng/areaplans/pwsplan.shtml DOT&PF / Parsons Brinokerhoff Jul-01 Report & relevant technical memos available Southeast Alaska Transportation Plan http://www.dot.state.ak.us/stwdplng/projectinfo/ser/newwave 24 DOT&PF Aug-04 -

FSX/Prepar3d Airport: 7AK Akutan, Alaska, USA

FSX/Prepar3D Airport: 7AK Akutan, Alaska, USA Airport: 7AK - Akutan Airport Location: Akutan Island, Alaska USA Creator: Wayne Roberts ([email protected]) Revised: Conrad F. Staeheli, CH-8807 Freienbach, Switzerland This is a NEW airport. Location: Akutan Airport (IATA: KQA[2], ICAO: PAUT, FAA LID: 7AK) is a state owned, public use airport serving Akutan, a city on Akutan Island in the Aleutians East Borough of the U.S. state of Alaska. The airport is located on Akun Island, 6 miles (10 km) east of Akutan Island. Scheduled air service is subsidized by the Essential Air Service program. https://skyvector.com/airport/7AK/Akutan-Airport http://www.airnav.com/airport/7AK History: The airport was opened in 2012. Akutan was previously served by amphibious airplane service to Akutan Seaplane Base, located on Akutan Island, however, in 2012 operator PenAir announced that they would retire their Grumman Goose aircraft and as a result the traditional airport on Akun Island was built to serve Akutan. The new airport is connected to Akutan by a hovercraft. Boats and amphibious aircraft, hovercraft, or helicopter are the only means of transportation into and out of Akutan. A 200-foot (61 m) dock and a small boat mooring basin are available. Meanwhile the Hovercraft has been sold due to high costs, an Helicopter-Service has been established by Maritime Helicopters. Grant Aviation offers daily flights from Unalaska/Dutch Harbour (ICAO: PADU) to Akutan (7AK, ICAO: PAUT) and back again. https://en.wikipedia.org/wiki/Akutan_Airport Changes were made based on 2012 construction plans. Custom models have been added. -

TABLE of CONTENTS Page

Alaska Aviation System Plan Update Yukon-Kuskokwim Region Air Versus Roads Access Construction and Maintenance Baseline Cost Comparison January 2013 YUKON-KUSKOKWIM REGION AIR VERSUS ROADS ACCESS CONSTRUCTION AND MAINTENANCE BASELINE COST COMPARISON ALASKA AVIATION SYSTEM PLAN UPDATE Prepared for: State of Alaska Department of Transportation and Public Facilities Division of Statewide Aviation 4111 Aviation Drive Anchorage, Alaska 99502 Prepared by: DOWL HKM 4041 B Street Anchorage, Alaska 99503 (907) 562-2000 W.O. 59825.10 January 2013 Yukon-Kuskokwim Region Air Versus Roads Access Alaska Aviation System Plan Update Construction and Maintenance Baseline Cost Comparison January 2013 TABLE OF CONTENTS Page 1.0 INTRODUCTION ...............................................................................................................1 2.0 ROADS COST ESTIMATE ................................................................................................4 2.1 Design Criteria ..................................................................................................................5 2.2 Roadway Unit Costs and Assumptions .............................................................................6 2.2.1 Roadway Unit Costs ...................................................................................................6 2.2.2 Roadway Cost Assumptions .......................................................................................7 2.2.3 Drainage Unit Costs and Assumptions .......................................................................8 -

Airport Diagram Airport Diagram

10266 JUNEAU INTL (JNU) (PAJN) AIRPORT DIAGRAM AL-1191 (FAA) JUNEAU, ALASKA ATIS 135.2 JUNEAU TOWER 118.7 278.3 GND CON 121.9 CLNC DEL 121.9 VAR 21.7^ E 1514 JANUARY 2010 ANNUAL RATE OF CHANGE 0.3^ W 58 22'N AK, 13 JAN 2011 to 10 MAR TERMINAL & TWR ELEV FIRE STATION 21 B1 8 B A B2 8W 083.1^ D1 C1 C H A D D2 E1 8457 X 150 E A FIELD F1 ELEV F A ELEV 21 4900 X 450 20 G 26W 263.2^ SEAPLANE AK, 13 JAN 2011 to 10 MAR 26 LANDING AREA 58 21'N RWY 08-26 S-75, D-200, 2D-340, 2D/2D2-500 CAUTION: BE ALERT TO RUNWAY CROSSING CLEARANCES. READBACK OF ALL RUNWAY HOLDING INSTRUCTIONS IS REQUIRED. 134 36'W 134 35'W 134 34'W 134 33'W JUNEAU, ALASKA AIRPORT DIAGRAM JUNEAU INTL (JNU) (PAJN) 10266 (JNU4.JNU) 10210 JUNEAU INTL (JNU) (PAJN) JUNEAU FOUR DEPARTURE SL-1191 (FAA) JUNEAU, ALASKA ATIS 135.2 GND CON HAINES 121.9 245 HNS H 318^ SN JUNEAU TOWER N59^12.73' 118.7 (CTAF) 278.3 W135^25.85' ANCHORAGE CENTER L-1 133.9 JUNEAU RADIO 122.2 9000 318^ (54) LOCALIZER 109.9 For Haines Transition only. I * I-JDL LDJ BARLO COGHLAN ISLAND Chan 36 N58^21.63' 212 CGL C N58^21.53'-W134^38.17' W134^53.35' LG 4000 * N58^21.56'-W134^41.98' 1000 SISTERS ISLAND 114.0 SSR RS 8 2 Chan 87 248^ N58^10.66' 312^ 276^ W135^15.53' L-1, H-1 113^ 5500 046^ 198^ (21) AK, 13 JAN 2011 to 10 MAR (16) R-046 RADKY A15 R-018 SSR N58^16.00' 197^ W134^37.01' 5500 7000 127^ LEVEL ISLAND (119) 116.5 LVD DVL Chan 112 ELEPHANT N56^28.06' W133^04.99' 391 EEF E F L-1, H-1 N58^10.26'-W135^15.48' L-1 128^ R-220 CAUTION: Rapidly rising terrain to above 3000' MSL north, east and south of airport. -

State of Alaska Itb Number 2515H029 Amendment Number One (1)

STATE OF ALASKA ITB NUMBER 2515H029 AMENDMENT NUMBER ONE (1) AMENDMENT ISSUING OFFICE: Department of Transportation & Public Facilities Statewide Contracting & Procurement P.O. Box 112500 (3132 Channel Drive, Room 145) Juneau, Alaska 99811-2500 THIS IS NOT AN ORDER DATE AMENDMENT ISSUED: February 9, 2015 ITB TITLE: De-icing Chemicals ITB OPENING DATE AND TIME: February 27, 2015 @ 2:00 PM Alaska Time The following changes are required: 1. Attachment A, DOT/PF Maintenance Stations identifying the address and contact information and is added to this ITB. This is a mandatory return Amendment. Your bid may be considered non-responsive and rejected if this signed amendment is not received [in addition to your bid] by the bid opening date and time. Becky Gattung Procurement Officer PHONE: (907) 465-8949 FAX: (907) 465-2024 NAME OF COMPANY DATE PRINTED NAME SIGNATURE ITB 2515H029 - De-icing Chemicals ATTACHMENT A DOT/PF Maintenance Stations SOUTHEAST REGION F.O.B. POINT Contact Name: Contact Phone: Cell: Juneau: 6860 Glacier Hwy., Juneau, AK 99801 Eric Wilkerson 465-1787 723-7028 Gustavus: Gustavus Airport, Gustavus, AK 99826 Brad Rider 697-2251 321-1514 Haines: 720 Main St., Haines, AK 99827 Matt Boron 766-2340 314-0334 Hoonah: 700 Airport Way, Hoonah, AK 99829 Ken Meserve 945-3426 723-2375 Ketchikan: 5148 N. Tongass Hwy. Ketchikan, AK 99901 Loren Starr 225-2513 617-7400 Klawock: 1/4 Mile Airport Rd., Klawock, AK 99921 Tim Lacour 755-2229 401-0240 Petersburg: 288 Mitkof Hwy., Petersburg, AK 99833 Mike Etcher 772-4624 518-9012 Sitka: 605 Airport Rd., Sitka, AK 99835 Steve Bell 966-2960 752-0033 Skagway: 2.5 Mile Klondike Hwy., Skagway, AK 99840 Missy Tyson 983-2323 612-0201 Wrangell: Airport Rd., Wrangell, AK 99929 William Bloom 874-3107 305-0450 Yakutat: Yakutat Airport, Yakutat, AK 99689 Robert Lekanof 784-3476 784-3717 1 of 6 ITB 2515H029 - De-icing Chemicals ATTACHMENT A DOT/PF Maintenance Stations NORTHERN REGION F.O.B. -

Invitation to Bid Invitation Number 2519H037

INVITATION TO BID INVITATION NUMBER 2519H037 RETURN THIS BID TO THE ISSUING OFFICE AT: Department of Transportation & Public Facilities Statewide Contracting & Procurement P.O. Box 112500 (3132 Channel Drive, Suite 350) Juneau, Alaska 99811-2500 THIS IS NOT AN ORDER DATE ITB ISSUED: January 24, 2019 ITB TITLE: De-icing Chemicals SEALED BIDS MUST BE SUBMITTED TO THE STATEWIDE CONTRACTING AND PROCUREMENT OFFICE AND MUST BE TIME AND DATE STAMPED BY THE PURCHASING SECTION PRIOR TO 2:00 PM (ALASKA TIME) ON FEBRUARY 14, 2019 AT WHICH TIME THEY WILL BE PUBLICLY OPENED. DELIVERY LOCATION: See the “Bid Schedule” DELIVERY DATE: See the “Bid Schedule” F.O.B. POINT: FINAL DESTINATION IMPORTANT NOTICE: If you received this solicitation from the State’s “Online Public Notice” web site, you must register with the Procurement Officer listed on this document to receive subsequent amendments. Failure to contact the Procurement Officer may result in the rejection of your offer. BIDDER'S NOTICE: By signature on this form, the bidder certifies that: (1) the bidder has a valid Alaska business license, or will obtain one prior to award of any contract resulting from this ITB. If the bidder possesses a valid Alaska business license, the license number must be written below or one of the following forms of evidence must be submitted with the bid: • a canceled check for the business license fee; • a copy of the business license application with a receipt date stamp from the State's business license office; • a receipt from the State’s business license office for -

List of Airports by IATA Code: a Wikipedia, the Free Encyclopedia List of Airports by IATA Code: a from Wikipedia, the Free Encyclopedia

9/8/2015 List of airports by IATA code: A Wikipedia, the free encyclopedia List of airports by IATA code: A From Wikipedia, the free encyclopedia List of airports by IATA code: A B C D E F G H I J K L M N O P Q R S T U V W X Y Z See also: List of airports by ICAO code A The DST column shows the months in which Daylight Saving Time, a.k.a. Summer Time, begins and ends. A blank DST box usually indicates that the location stays on Standard Time all year, although in some cases the location stays on Summer Time all year. If a location is currently on DST, add one hour to the time in the Time column. To determine how much and in which direction you will need to adjust your watch, first adjust the time offsets of your source and destination for DST if applicable, then subtract the offset of your departure city from the offset of your destination. For example, if you were flying from Houston (UTC−6) to South Africa (UTC+2) in June, first you would add an hour to the Houston time for DST, making it UTC−5, then you would subtract 5 from +2. +2 (5) = +2 + (+5) = +7, so you would need to advance your watch by seven hours. If you were going in the opposite direction, you would subtract 2 from 5, giving you 7, indicating that you would need to turn your watch back seven hours. Contents AA AB AC AD AE AF AG AH AI AJ AK AL AM AN AO AP AQ AR AS AT AU AV AW AX AY AZ https://en.wikipedia.org/wiki/List_of_airports_by_IATA_code:_A 1/24 9/8/2015 List of airports by IATA code: A Wikipedia, the free -

Project Listing by Community - All Final FY09 Ch 29 SLA08

Project Listing by Community - All Final FY09 Ch 29 SLA08 Refnum AP/AL Project Title Fund Total Project Total Adak (HD 37) Department of Environmental Conservation 46415 AL Adak: Design and Construction of Water and Sewer Facilities 777,464 1002 Fed Rcpts 585,217 1003 G/F Match 192,247 AK Cap Inc (1197): 0 ASLC Bonds (1186): 0 AHFC Div (1139): 0 General Fund Total: 192,247 Federal Total: 585,217 Other Total: 0 Community Total: 777,464 Akiachak (HD 38) Department of Education and Early Development 45752 AP Yupiit School District - Library Resources for District School Libraries 60,000 1197 AK Cap Inc 60,000 Department of Environmental Conservation 46416 AL Akiachak: Design and Construction of Water and Sewer Facilities 2,571,014 1002 Fed Rcpts 1,935,267 1003 G/F Match 635,747 State of Alaska Released May 23, 2008 1-27-2011 11:34 am Office of Management and Budget Page 1 of 148 Project Listing by Community - All Final FY09 Ch 29 SLA08 Refnum AP/AL Project Title Fund Total Project Total Akiachak (HD 38) Department of Transportation and Public Facilities 43254 AL Akiachak: Airport Relocation 8,000,000 1002 Fed Rcpts 8,000,000 AK Cap Inc (1197): 60,000 ASLC Bonds (1186): 0 AHFC Div (1139): 0 General Fund Total: 635,747 Federal Total: 9,935,267 Other Total: 60,000 Community Total: 10,631,014 Akiak (HD 38) Department of Commerce, Community, and Economic Development 45777 AP Akiak - Village Police Safety Building 400,000 1197 AK Cap Inc 400,000 AK Cap Inc (1197): 400,000 ASLC Bonds (1186): 0 AHFC Div (1139): 0 General Fund Total: 0 Federal Total: