A Neural Network and Genetic Algorithm Hybrid Model for Modeling Exchange Rates: the Case of the US Dollar/ Kuwaiti Dinar

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

0.30560 0.30570 Daily Treasury Market Commentary KUWAITI DINAR

KUWAITI DINAR 0.30560 0.30570 Daily Treasury Market Commentary October 28, 2020 Foreign Exchange Developments: Economic Updates: The euro fell against the dollar on Wednesday following a New orders for key US-made capital goods increased Currency Price MTD % 3M% YTD% media report that France's government was leaning to six-year high in September, wrapping up a quarter EUR/USD 1.1779 0.51 0.55 5.07 toward reinstating a national lockdown to curb a of potentially record growth in business spending and GBP/USD 1.3043 0.98 0.87 -1.64 resurgence in coronavirus cases. the economy. AUD/USD 0.7145 -0.24 -0.18 1.75 The dollar, however, gave up early gains against other Britain must spell out how far it wants to diverge from USD/CHF 0.909 -1.28 -0.98 -6.09 major currencies as sentiment turned bearish due to European Union rules if it wants access to the bloc's USD/JPY 104.26 -1.16 -0.81 -4.25 uncertainty about the outcome of the U.S. presidential financial market from January, a top European USD/CAD 1.3191 -0.97 -1.39 1.57 election next week. The euro fell 0.14% to $1.1780 in Asia Commission official said on Tuesday. on Wednesday, down for a third consecutive session. Sterling held steady at $1.3035, supported by hopes for a Local & GCC news: last-minute trade deal between Britain and the European Kuwait's central bank announced on Tuesday it was Index Price Change MTD% YTD% Union. -

Countries Codes and Currencies 2020.Xlsx

World Bank Country Code Country Name WHO Region Currency Name Currency Code Income Group (2018) AFG Afghanistan EMR Low Afghanistan Afghani AFN ALB Albania EUR Upper‐middle Albanian Lek ALL DZA Algeria AFR Upper‐middle Algerian Dinar DZD AND Andorra EUR High Euro EUR AGO Angola AFR Lower‐middle Angolan Kwanza AON ATG Antigua and Barbuda AMR High Eastern Caribbean Dollar XCD ARG Argentina AMR Upper‐middle Argentine Peso ARS ARM Armenia EUR Upper‐middle Dram AMD AUS Australia WPR High Australian Dollar AUD AUT Austria EUR High Euro EUR AZE Azerbaijan EUR Upper‐middle Manat AZN BHS Bahamas AMR High Bahamian Dollar BSD BHR Bahrain EMR High Baharaini Dinar BHD BGD Bangladesh SEAR Lower‐middle Taka BDT BRB Barbados AMR High Barbados Dollar BBD BLR Belarus EUR Upper‐middle Belarusian Ruble BYN BEL Belgium EUR High Euro EUR BLZ Belize AMR Upper‐middle Belize Dollar BZD BEN Benin AFR Low CFA Franc XOF BTN Bhutan SEAR Lower‐middle Ngultrum BTN BOL Bolivia Plurinational States of AMR Lower‐middle Boliviano BOB BIH Bosnia and Herzegovina EUR Upper‐middle Convertible Mark BAM BWA Botswana AFR Upper‐middle Botswana Pula BWP BRA Brazil AMR Upper‐middle Brazilian Real BRL BRN Brunei Darussalam WPR High Brunei Dollar BND BGR Bulgaria EUR Upper‐middle Bulgarian Lev BGL BFA Burkina Faso AFR Low CFA Franc XOF BDI Burundi AFR Low Burundi Franc BIF CPV Cabo Verde Republic of AFR Lower‐middle Cape Verde Escudo CVE KHM Cambodia WPR Lower‐middle Riel KHR CMR Cameroon AFR Lower‐middle CFA Franc XAF CAN Canada AMR High Canadian Dollar CAD CAF Central African Republic -

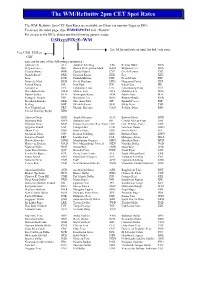

WM/Refinitiv 2Pm CET Spot Rates

The WM/Refinitiv 2pm CET Spot Rates The WM/ Refinitiv 2pm CET Spot Rates are available on Eikon via monitor Pages or RICs. To access the index page, type WMRESPOT01 and <Return> For access to the RICs, please use the following generic codes : USDxxxFIXzE=WM Use M for mid rate or omit for bid / ask rates Use USD, EUR or GBP xxx can be any of the following currencies : Albania Lek ALL Austrian Schilling ATS Belarus Ruble BYN Belgian Franc BEF Bosnia Herzegovina Mark BAM Bulgarian Lev BGN Croatian Kuna HRK Cyprus Pound CYP Czech Koruna CZK Danish Krone DKK Estonian Kroon EEK Ecu XEU Euro EUR Finnish Markka FIM French Franc FRF Deutsche Mark DEM Greek Drachma GRD Hungarian Forint HUF Iceland Krona ISK Irish Punt IEP Italian Lira ITL Latvian Lat LVL Lithuanian Litas LTL Luxembourg Franc LUF Macedonia Denar MKD Maltese Lira MTL Moldova Leu MDL Dutch Guilder NLG Norwegian Krone NOK Polish Zloty PLN Portugese Escudo PTE Romanian Leu RON Russian Rouble RUB Slovakian Koruna SKK Slovenian Tolar SIT Spanish Peseta ESP Sterling GBP Swedish Krona SEK Swiss Franc CHF New Turkish Lira TRY Ukraine Hryvnia UAH Serbian Dinar RSD Special Drawing Rights XDR Algerian Dinar DZD Angola Kwanza AOA Bahrain Dinar BHD Botswana Pula BWP Burundi Franc BIF Central African Franc XAF Comoros Franc KMF Congo Democratic Rep. Franc CDF Cote D’Ivorie Franc XOF Egyptian Pound EGP Ethiopia Birr ETB Gambian Dalasi GMD Ghana Cedi GHS Guinea Franc GNF Israeli Shekel ILS Jordanian Dinar JOD Kenyan Schilling KES Kuwaiti Dinar KWD Lebanese Pound LBP Lesotho Loti LSL Malagasy Ariary -

Security Council GENERAL

UNITED NATIONS S Distr. Security Council GENERAL S/AC.26/1999/17 30 September 1999 Original: ENGLISH UNITED NATIONS COMPENSATION COMMISSION GOVERNING COUNCIL REPORT AND RECOMMENDATIONS MADE BY THE PANEL OF COMMISSIONERS CONCERNING THE SECOND INSTALMENT OF “E4” CLAIMS GE.99-66179 S/AC.26/1999/17 Page 2 CONTENTS Paragraphs Page Introduction .................... 1 - 3 4 I. OVERVIEW OF THE SECOND INSTALMENT CLAIMS .... 4 - 7 4 II. THE PROCEEDINGS ................ 8 - 27 5 III. LEGAL FRAMEWORK ................ 28 8 IV. VERIFICATION AND VALUATION OF CLAIMS ...... 29 8 V. THE CLAIMS ................... 30- 109 8 A. Contract .................. 31- 43 9 1. Compensability ............. 36 9 2. Verification and valuation method . 37 9 3. Evidence submitted .......... 38- 43 10 B. Real property ............... 44- 51 11 1. Compensability ............. 45- 46 11 2. Verification and valuation method . 47 11 3. Evidence submitted ........... 48- 51 11 C. Tangible property ............. 52- 65 12 1. Compensability ............. 53 12 2. Verification and valuation method . 54 12 3. Evidence submitted ........... 55- 65 12 (a) Tangible property ......... 55- 56 12 (b) Stock ............... 57- 59 13 (c) Cash ............... 60- 61 13 (d) Vehicles ............. 62- 65 14 D. Income-producing property ......... 66- 69 14 E. Payment or relief to others ........ 70- 78 15 1. Compensability ............. 71- 74 15 2. Verification and valuation method . 75 16 3. Evidence submitted ........... 76- 78 17 F. Loss of profits .............. 79- 85 17 1. Compensability ............. 80 17 2. Verification and valuation method . 81 17 3. Evidence submitted ........... 82- 85 18 G. Receivables ................ 86- 92 18 1. Compensability ............. 87- 88 18 2. Verification and valuation method . 89 19 3. Evidence submitted ........... 90- 92 19 H. -

North York Coin Club Founded 1960 MONTHLY MEETINGS 4TH Tuesday 7:30 P.M

North York Coin Club Founded 1960 MONTHLY MEETINGS 4TH Tuesday 7:30 P.M. AT Edithvale Community Centre, 131 Finch Ave. W., North York M2N 2H8 MAIL ADDRESS: NORTH YORK COIN CLUB, 5261 Naskapi Court, Mississauga, ON L5R 2P4 Web site: www.northyorkcoinclub.com Contact the Club : Executive Committee E-mail: [email protected] President ........................................Bill O’Brien Director ..........................................Roger Fox Auction Manager..........................Paul Johnson Phone: 416-897-6684 1st Vice President ..........................Henry Nienhuis Director ..........................................Paul Johnson Editor ..........................................Paul Petch 2nd Vice President.......................... Director ..........................................Andrew Silver Receptionist ................................Franco Farronato Member : Secretary ........................................Henry Nienhuis Junior Director ................................ Draw Prizes ................................Bill O’Brien Treasurer ........................................Ben Boelens Auctioneer ......................................Dick Dunn Social Convenor ..........................Bill O’Brien Ontario Numismatic Association Past President ................................Nick Cowan Royal Canadian Numismatic Assocation THE BULLETIN FOR MARCH 2017 PRESIDENT’S MESSAGE NEXT MEETING Good day to all fellow numismatists and Speaking about the R.C.N.A., it’s not too TUESDAY, MARCH 28 our members and friends who receive -

CURRENCY BOARD FINANCIAL STATEMENTS Currency Board Working Paper

SAE./No.22/December 2014 Studies in Applied Economics CURRENCY BOARD FINANCIAL STATEMENTS Currency Board Working Paper Nicholas Krus and Kurt Schuler Johns Hopkins Institute for Applied Economics, Global Health, and Study of Business Enterprise & Center for Financial Stability Currency Board Financial Statements First version, December 2014 By Nicholas Krus and Kurt Schuler Paper and accompanying spreadsheets copyright 2014 by Nicholas Krus and Kurt Schuler. All rights reserved. Spreadsheets previously issued by other researchers are used by permission. About the series The Studies in Applied Economics of the Institute for Applied Economics, Global Health and the Study of Business Enterprise are under the general direction of Professor Steve H. Hanke, co-director of the Institute ([email protected]). This study is one in a series on currency boards for the Institute’s Currency Board Project. The series will fill gaps in the history, statistics, and scholarship of currency boards. This study is issued jointly with the Center for Financial Stability. The main summary data series will eventually be available in the Center’s Historical Financial Statistics data set. About the authors Nicholas Krus ([email protected]) is an Associate Analyst at Warner Music Group in New York. He has a bachelor’s degree in economics from The Johns Hopkins University in Baltimore, where he also worked as a research assistant at the Institute for Applied Economics and the Study of Business Enterprise and did most of his research for this paper. Kurt Schuler ([email protected]) is Senior Fellow in Financial History at the Center for Financial Stability in New York. -

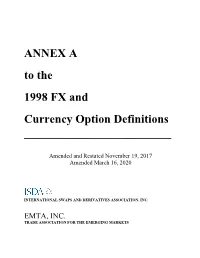

ANNEX a to the 1998 FX and CURRENCY OPTION DEFINITIONS AMENDED and RESTATED AS of NOVEMBER 19, 2017 I

ANNEX A to the 1998 FX and Currency Option Definitions _________________________ Amended and Restated November 19, 2017 Amended March 16, 2020 INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. EMTA, INC. TRADE ASSOCIATION FOR THE EMERGING MARKETS Copyright © 2000-2020 by INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. EMTA, INC. ISDA and EMTA consent to the use and photocopying of this document for the preparation of agreements with respect to derivative transactions and for research and educational purposes. ISDA and EMTA do not, however, consent to the reproduction of this document for purposes of sale. For any inquiries with regard to this document, please contact: INTERNATIONAL SWAPS AND DERIVATIVES ASSOCIATION, INC. 10 East 53rd Street New York, NY 10022 www.isda.org EMTA, Inc. 405 Lexington Avenue, Suite 5304 New York, N.Y. 10174 www.emta.org TABLE OF CONTENTS Page INTRODUCTION TO ANNEX A TO THE 1998 FX AND CURRENCY OPTION DEFINITIONS AMENDED AND RESTATED AS OF NOVEMBER 19, 2017 i ANNEX A CALCULATION OF RATES FOR CERTAIN SETTLEMENT RATE OPTIONS SECTION 4.3. Currencies 1 SECTION 4.4. Principal Financial Centers 6 SECTION 4.5. Settlement Rate Options 9 A. Emerging Currency Pair Single Rate Source Definitions 9 B. Non-Emerging Currency Pair Rate Source Definitions 21 C. General 22 SECTION 4.6. Certain Definitions Relating to Settlement Rate Options 23 SECTION 4.7. Corrections to Published and Displayed Rates 24 INTRODUCTION TO ANNEX A TO THE 1998 FX AND CURRENCY OPTION DEFINITIONS AMENDED AND RESTATED AS OF NOVEMBER 19, 2017 Annex A to the 1998 FX and Currency Option Definitions ("Annex A"), originally published in 1998, restated in 2000 and amended and restated as of the date hereof, is intended for use in conjunction with the 1998 FX and Currency Option Definitions, as amended and updated from time to time (the "FX Definitions") in confirmations of individual transactions governed by (i) the 1992 ISDA Master Agreement and the 2002 ISDA Master Agreement published by the International Swaps and Derivatives Association, Inc. -

Multi-Currency Capability

■ www.unisonmarketplace.com Multi-Currency Capability Unison Marketplace now offers a new feature that will support multiple currencies. This feature will allow Buyers to solicit requirements on the Marketplace and receive bids from the Seller community in different currencies (i.e. EUR, MXN, THB, CNY, PLN, etc.). Based on feedback from our growing pool of customers in remote areas and across global agencies, we have implemented this feature to further adapt to unique purchasing needs. Benefits Bid in your local currency. Increased access Faster bidding. Bid and receive orders in your local to opportunities. Submit your bids without the need to convert currency when accepted by Buyers on the More opportunities may be available from to USD when the Buyer allows multiple Marketplace. global customers. currencies. Utilizing Multi-Currency Submitting a bid in an alternative currency: 1. When bidding on a buy, a list of buyer-selected currencies will be available to choose from on the ‘Terms’ page. Using the drop down menu, select the currency in which you wish to bid. 2. On the ‘Line Items’ page, enter your pricing in your selected currency. 1 3. Review the pricing on the ‘Review and Submit’ page before submitting your bid. Please note: the pricing will appear in your selected currency, however all bids will be converted to U.S. dollars for Buyer evaluation If you have questions about Multi-Currency capabilities, at the currency exchange rate indicated in the please contact [email protected]. bidding requirements. The Buyer will see both the U.S. dollar and selected currency when reviewing your bid. -

CCT Master Currency List-WU

Currency Bank Name Africa Code Kenyan Shilling KES Stanbic Bank, Nairobi Namibian Dollar NAD Standard Bank Namibia, Ltd, Windhoek South African Rand ZAR Standard Bank of South Africa, Johannesburg Currency Bank Name Asia Code Chinese Yuan CNY Citic Bank Hong Kong Dollar HKD Standard Chartered Bank, Hong Kong Indian Rupee INR ICICI Bank Japanese Yen JPY Standard Chartered Bank, Tokyo Singapore Dollar SGD The Bank of New York Mellon Thai Bhat THB HSBC Bank, Bangkok Currency Bank Name Australia / Oceania Code Australian Dollar AUD HSBC Bank, Sydney Fiji Dollar FJD Westpac Banking Corporation, Suva New Zealand Dollar NZD Westpac Banking Corporation, Wellington Samoan Tala WST Westpac Bank Samoa Limited, Apia Tahitian (Central Polynesian) Franc XPF Banque de Polynesie, Papeete Vanuatu Vatu VUV Westpac Banking Corporation, Port Vila Currency Bank Name Europe Code British Pound GBP HSBC Bank PLC, London Czech Republic Koruna CZK Ceskoslovenska Obchodni Banka Danish Krone DKK Danske Bank, Copenhagen Euro (Main)* EUR HSBC Bank PLC, London Hungarian Forint HUF HSBC Bank PLC, London Latvian Lats LVL HSBC Bank PLC, London Lithuanian Litas LTL HSBC Bank PLC, London Norwegian Krone NOK Den Norske Bank, Oslo Polish Zloty PLN ING Bank, Poland Swedish Krona SEK Skandinaviska Enskilda Banken (SEB), Stockholm Swiss Franc CHF Credit Suisse, Zurich Currency Bank Name Middle East Code Bahrain Dinar BHD HSBC Bank PLC, London Israeli Shekel ILS HSBC Bank PLC, London Jordanian Dinar JOD HSBC Bank PLC, London Kuwaiti Dinar KWD HSBC Bank PLC, London Omani Rial -

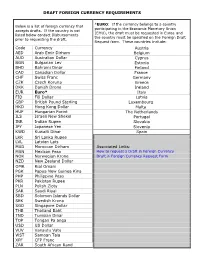

Below Is a List of Foreign Currency That Accepts Drafts

DRAFT FOREIGN CURRENCY REQUIREMENTS *EURO: If the currency belongs to a country Below is a list of foreign currency that participating in the Economic Monetary Union accepts drafts. If the country is not (EMU), the draft must be requested in Euros and listed below contact Disbursements the country must be specified on the Foreign Draft prior to requesting the draft. Request form. These countries include: Code Currency Austria AED Arab Emir Dirham Belgium AUD Australian Dollar Cyprus BGN Bulgarian Lev Estonia BHD Bahraini Dinar Finland CAD Canadian Dollar France CHF Swiss Franc Germany CZK Czech Koruna Greece DKK Danish Drone Ireland EUR Euro* Italy FJD Fiji Dollar Latvia GBP British Pound Sterling Luxembourg HKD Hong Kong Dollar Malta HUF Hungarian Forint The Netherlands ILS Israeli New Shekel Portugal INR Indian Rupee Slovakia JPY Japanese Yen Slovenia KWD Kuwaiti Dinar Spain LKR Sri Lanka Rupee LVL Latvian Lats MAD Moroccan Dirham Associated Links: MXN Mexican Peso How to request a Draft in Foreign Currency NOK Norwegian Krone Draft in Foreign Currency Request Form NZD New Zealand Dollar OMR Rial Omani PGK Papua New Guinea Kina PHP Philippine Peso PKR Pakistan Rupee PLN Polish Zloty SAR Saudi Riyal SBD Solomon Islands Dollar SEK Swedish Krona SGD Singapore Dollar THB Thailand Baht TND Tunisian Dinar TOP Tongan Pa anga USD US Dollar VUV Vanautu Vatu WST Samoan Tala XPF CFP Franc ZAR South African Rand . -

List of Currencies Sorted by Iso Currency Code and Country Or Area Name

ANNEX F.II LIST OF CURRENCIES SORTED BY ISO CURRENCY CODE AND COUNTRY OR AREA NAME Currency ISO code Currency name Country name AED UAE Dirham United Arab Emirates AFN Afghani Afghanistan ALL Lek Albania AMD Armeniam Dram Armenia ANG Netherlands Antillian Guilder Curaçao ANG Netherlands Antillian Guilder Sint Maarten AOA Kwanza Angola ARS Argentine Peso Argentina AUD Australian Dollar Australia AUD Australian Dollar Christmas Island AUD Australian Dollar Cocos (Keeling) Islands AUD Australian Dollar Kiribati AUD Australian Dollar Nauru AUD Australian Dollar Tuvalu AWG Aruban Florin Aruba AZN Azerbaijanian Manat Azerbaijan BAM Convertible Mark Bosnia and Herzegovina BBD Barbados Dollar Barbados BDT Taka Bangladesh BGN Bulgarian Lev Bulgaria BHD Bahraini Dinar Bahrain BIF Burundi Franc Burundi BMD Bermudian Dollar Bermuda BND Brunei Dollar Brunei Darussalam BOB Boliviano Bolivia (Plurinat.State) BRL Brazilian Real Brazil BSD Bahamian Dollar Bahamas BTN Ngultrum Bhutan BWP Pula Botswana BYN Belarusian Ruble Belarus BZD Belize Dollar Belize CAD Canadian Dollar Canada CDF Congolese Franc Congo, Dem. Rep. of the CHF Swiss Franc Liechtenstein CHF Swiss Franc Switzerland CLP Chilean Peso Chile CNY Yuan Renminbi China COP Colombian Peso Colombia CRC Costa Rican Colón Costa Rica CUP Cuban Peso Cuba CVE Cabo Verde Escudo Cabo Verde CZK Czech Koruna Czechia DJF Djibouti Franc Djibouti DKK Danish Krone Denmark DKK Danish Krone Faroe Islands DKK Danish Krone Greenland DOP Dominican Peso Dominican Republic DZD Algerian Dinar Algeria EGP Egyptian Pound -

(Gcc): a Kuwaiti Perspective

Durham E-Theses ECONOMIC AND MONETARY INTEGRATION IN THE GULF COOPERATION COUNCIL (GCC): A KUWAITI PERSPECTIVE ALTRAD, SAADI,S,E,F How to cite: ALTRAD, SAADI,S,E,F (2011) ECONOMIC AND MONETARY INTEGRATION IN THE GULF COOPERATION COUNCIL (GCC): A KUWAITI PERSPECTIVE , Durham theses, Durham University. Available at Durham E-Theses Online: http://etheses.dur.ac.uk/899/ Use policy The full-text may be used and/or reproduced, and given to third parties in any format or medium, without prior permission or charge, for personal research or study, educational, or not-for-prot purposes provided that: • a full bibliographic reference is made to the original source • a link is made to the metadata record in Durham E-Theses • the full-text is not changed in any way The full-text must not be sold in any format or medium without the formal permission of the copyright holders. Please consult the full Durham E-Theses policy for further details. Academic Support Oce, Durham University, University Oce, Old Elvet, Durham DH1 3HP e-mail: [email protected] Tel: +44 0191 334 6107 http://etheses.dur.ac.uk 2 DURHAM UNIVERSITY ECONOMIC AND MONETARY INTEGRATION IN THE GULF COOPERATION COUNCIL (GCC): A KUWAITI PERSPECTIVE By SAADI S. F. AL TRAD A thesis submitted for the degree of Doctor of Philosophy School of Government and International Affairs Institute for Middle Eastern and Islamic Studies 2011 Abstract ABSTRACT The State of Kuwait is has been a member of the Gulf Cooperation Council (GCC) since its establishment in 1980. Kuwait is a geographically small but oil-rich country, whose economic development in recent years is the result of an increase in both the production and prices of oil, which now accounts for almost 90% of exports.