0.30560 0.30570 Daily Treasury Market Commentary KUWAITI DINAR

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Faysal Funds

Accounts forthe Quarter Ended September 30, 2008 FAYSAL BALANCED GROWTH FUND The Faysal Balanced Growth Fund (FBGF) is an open-ended mutual fund. The units of FBGF are listed on the Karachi Stock Exchange and were initially offered to the public on April 19, 2004. FBGFseeks to provide long-term capital appreciation with a conservative risk profile and a medium to long-term investment horizon. FBGF's investment philosophy is to provide stable returns by investing in a portfolio balanced between equities and fixed income instruments. Fund Information Management Company Faysal Asset Management Limited Board of Directors of the Management Company Mr. Khalid Siddiq Tirmizey, Chairman Mr. Salman Haider Sheikh, Chief Executive Officer Mr. Sanaullah Qureshi, Director Mr. Syed Majid AIi, Director Mr. Feroz Rizvi, Director CFO of the Management Company Mr. Abdul Razzak Usman Company Secretary of the Management Company Mr. M. Siddique Memon Audit Committee Mr. Feroz Rizvi, Chairman Mr. Sanaullah Qureshi, Member Mr. Syed Majid Ali, Member Trustee Central Depository Company of Pakistan Limited Suit #. M-13, 16, Mezzanine Floor, Progressive Plaza, Beaumont Road, Near PIDC House, Karachi. Bankers to the Fund Faysal Bank Limited MCB Bank Limited Bank Alfalah Limited Atlas Bank Limited The Bank of Punjab Auditors Ford Rhodes Sidat Hyder & Co., Chartered Accountants Legal Advisor Mohsin Tayebely & Co., 2nd Floor, Dime Centre, BC-4, Block-9, KDA-5, Clifton, Karachi. Registrars Gangjees Registrar Services (Pvt) Limited Room # 506, 5th Floor, Clifton Centre, Kehkashan Clifton - Karachi. Distributors Access Financial Services (Pvt.) Ltd. AKD Securities (Pvt.) Limited Faysal Asset Management Limited Faysal Bank Limited PICIC Commercial Bank Limited Reliance Financial Products (Pvt.) Limited Invest Capital & Securities (Pvt.) Limited Flow(Private) Limited IGI Investment Bank Limited Pak Oman Investment Bank Limited Alfalah Securities (Pvt) Limited JS Global Capital Limited t"''' e , FAYSAL BALANCED ~ . -

Habibmetro Modaraba Management (AN(AN ISLAMICISLAMIC FINANCIALFINANCIAL INSTITUTION)INSTITUTION)

A N N U A L R E P O R T 2017 1 HabibMetro Modaraba Management (AN(AN ISLAMICISLAMIC FINANCIALFINANCIAL INSTITUTION)INSTITUTION) 2 A N N U A L R E P O R T 2017 JOURNEY OF CONTINUOUS SUCCESS A long term partnership Over the years, First Habib Modaraba (FHM) has become the sound, strong and leading Modaraba within the Modaraba sector. Our stable financial performance and market positions of our businesses have placed us well to deliver sustainable growth and continuous return to our investors since inception. During successful business operation of more than 3 decades, FHM had undergone with various up and down and successfully countered with several economic & business challenges. Ever- changing requirement of business, product innovation and development were effectively managed and delivered at entire satisfaction of all stakeholders with steady growth on sound footing. Consistency in perfect sharing of profits among the certificate holders along with increase in certificate holders' equity has made FHM a sound and well performing Modaraba within the sector. Our long term success is built on a firm foundation of commitment. FHM's financial strength, risk management protocols, governance framework and performance aspirations are directly attributable to a discipline that regularly brings prosperity to our partners and gives strength to our business model which is based on true partnership. Conquering with the challenges of our operating landscape, we have successfully journeyed steadily and progressively, delivering consistent results. With the blessing of Allah (SWT), we are today the leading Modaraba within the Modaraba sector of Pakistan, demonstrating our strength, financial soundness and commitment in every aspect of our business. -

Prospectus, Especially the Risk Factors Given at Para 4.11 of This Prospectus Before Making Any Investment Decision

ADVICE FOR INVESTORS INVESTORS ARE STRONGLY ADVISED IN THEIR OWN INTEREST TO CAREFULLY READ THE CONTENTS OF THIS PROSPECTUS, ESPECIALLY THE RISK FACTORS GIVEN AT PARA 4.11 OF THIS PROSPECTUS BEFORE MAKING ANY INVESTMENT DECISION. SUBMISSION OF FALSE AND FICTITIOUS APPLICATIONS ARE PROHIBITED AND SUCH APPLICATIONS’ MONEY MAY BE FORFEITED UNDER SECTION 87(8) OF THE SECURITIES ACT, 2015. SONERI BANK LIMITED PROSPECTUS THE ISSUE SIZE OF FULLY PAID UP, RATED, LISTED, PERPETUAL, UNSECURED, SUBORDINATED, NON-CUMULATIVE AND CONTINGENT CONVERTIBLE DEBT INSTRUMENTS IN THE NATURE OF TERM FINANCE CERTIFICATES (“TFCS”) IS PKR 4,000 MILLION, OUT OF WHICH TFCS OF PKR 3,600 MILLION (90% OF ISSUE SIZE) ARE ISSUED TO THE PRE-IPO INVESTORS AND PKR 400 MILLION (10% OF ISSUE SIZE) ARE BEING OFFERED TO THE GENERAL PUBLIC BY WAY OF INITIAL PUBLIC OFFER THROUGH THIS PROSPECTUS RATE OF RETURN: PERPETUAL INSTRUMENT @ 6 MONTH KIBOR* (ASK SIDE) PLUS 2.00% P.A INSTRUMENT RATING: A (SINGLE A) BY THE PAKISTAN CREDIT RATING COMPANY LIMITED LONG TERM ENTITY RATING: “AA-” (DOUBLE A MINUS) SHORT TERM ENTITY RATING: “A1+” (A ONE PLUS) BY THE PAKISTAN CREDIT RATING AGENCY LIMITED AS PER PSX’S LISTING OF COMPANIES AND SECURITIES REGULATIONS, THE DRAFT PROSPECTUS WAS PLACED ON PSX’S WEBSITE, FOR SEEKING PUBLIC COMMENTS, FOR SEVEN (7) WORKING DAYS STARTING FROM OCTOBER 18, 2018 TO OCTOBER 26, 2018. NO COMMENTS HAVE BEEN RECEIVED ON THE DRAFT PROSPECTUS. DATE OF PUBLIC SUBSCRIPTION: FROM DECEMBER 5, 2018 TO DECEMBER 6, 2018 (FROM: 9:00 AM TO 5:00 PM) (BOTH DAYS INCLUSIVE) CONSULTANT TO THE ISSUE BANKERS TO THE ISSUE (RETAIL PORTION) Allied Bank Limited Askari Bank Limited Bank Alfalah Limited** Bank Al Habib Limited Faysal Bank Limited Habib Metropolitan Bank Limited JS Bank Limited MCB Bank Limited Silk Bank Limited Soneri Bank Limited United Bank Limited** **In order to facilitate investors, United Bank Limited (“UBL”) and Bank Alfalah Limited (“BAFL”) are providing the facility of electronic submission of application (e‐IPO) to their account holders. -

IBOR Transition Faqs

Sep 2021 IBOR Transition FAQs September 2021 About IBOR Transition This explanation and general risk warning is provided for customers of Al Ahli Bank Kuwait and each of its subsidiaries (collectively, “ABK”) who may have conventional products or agreements which uses the London Interbank Offered Rate ('LIBOR') or another inter-bank offered rate (together with LIBOR, the 'IBORs') as a benchmark rate. This explanation and general risk warning is provided for information purposes only and is subject to change. Where information in this explanation and general risk warning has been obtained from third party sources, we believe those sources to be reliable, but we do not guarantee the information’s accuracy, and you should note that it may be incomplete or condensed. Benchmark Reform LIBOR and other IBORs are currently the focus of international and national reforms. The UK Financial Conduct Authority (‘FCA’), which regulates LIBOR, has stated that it will no longer compel banks to submit rates for the calculation of LIBOR after the end of 2021. The US Federal Reserve and other regulators have also taken measures to move markets away from IBORs within set timelines. As a result, the continuation of LIBOR and other IBORs on their current basis cannot be guaranteed after 31 December 2021. These reforms may result in: (i) changes to the rules or methodologies used in calculating benchmark rates; (ii) restrictions on the use of benchmark rates; and/or (iii) discontinuance of benchmark rates. Even if certain benchmark rates might continue to be published, changes to their methodology, or restrictions on use, may mean that they are no longer representative of the underlying market and economic reality that the benchmark rate was originally intended measure or otherwise become no longer appropriate for products or agreements that customers have entered into with ABK. -

CEE Qu 3-08.Qxd

Analysis of the UniCredit Group CEE Research Network CEE Quarterly 03 2008 For authors see last page Imprint Disclaimer Published by UniCredit Group/Bank Austria Creditanstalt Aktiengesellschaft This document (the “Document”) has been prepared by UniCredito Italiano S.p.A. and its http://www.unicreditgroup.eu controlled companies1 (collectively the “UniCredit Group”). The Document is for information http://www.bankaustria.at purposes only and is not intended as (i) an offer, or solicitation of an offer, to sell or to buy any financial instrument and/or (ii) a professional advice in relation to any investment decision. Edited by CEE Research Department The Document is being distributed by electronic and ordinary mail to professional investors and [email protected] may not be redistributed, reproduced, disclosed or published in whole or in part. Information, Bernhard Sinhuber, Phone +43 (0)50505-41964 opinions, estimates and forecasts contained herein have been obtained from or are based upon sources believed by the UniCredit Group to be reliable but no representation or warranty, Produced by Bank Austria Identity & Communications Department, express or implied, is made and no responsibility, liability and/or indemnification obligation shall Editorial Desk ([email protected]), be borne by the UniCredit Group vis-à-vis any recipient of the present Document and/or any Phone +43 (0)50505-56141 third party as to the accuracy, completeness and/or correctness of any information contained in the Document. The UniCredit Group is involved in several businesses and transactions that may Printed by Holzhausen relate directly or indirectly to the content of the Document. -

Countries Codes and Currencies 2020.Xlsx

World Bank Country Code Country Name WHO Region Currency Name Currency Code Income Group (2018) AFG Afghanistan EMR Low Afghanistan Afghani AFN ALB Albania EUR Upper‐middle Albanian Lek ALL DZA Algeria AFR Upper‐middle Algerian Dinar DZD AND Andorra EUR High Euro EUR AGO Angola AFR Lower‐middle Angolan Kwanza AON ATG Antigua and Barbuda AMR High Eastern Caribbean Dollar XCD ARG Argentina AMR Upper‐middle Argentine Peso ARS ARM Armenia EUR Upper‐middle Dram AMD AUS Australia WPR High Australian Dollar AUD AUT Austria EUR High Euro EUR AZE Azerbaijan EUR Upper‐middle Manat AZN BHS Bahamas AMR High Bahamian Dollar BSD BHR Bahrain EMR High Baharaini Dinar BHD BGD Bangladesh SEAR Lower‐middle Taka BDT BRB Barbados AMR High Barbados Dollar BBD BLR Belarus EUR Upper‐middle Belarusian Ruble BYN BEL Belgium EUR High Euro EUR BLZ Belize AMR Upper‐middle Belize Dollar BZD BEN Benin AFR Low CFA Franc XOF BTN Bhutan SEAR Lower‐middle Ngultrum BTN BOL Bolivia Plurinational States of AMR Lower‐middle Boliviano BOB BIH Bosnia and Herzegovina EUR Upper‐middle Convertible Mark BAM BWA Botswana AFR Upper‐middle Botswana Pula BWP BRA Brazil AMR Upper‐middle Brazilian Real BRL BRN Brunei Darussalam WPR High Brunei Dollar BND BGR Bulgaria EUR Upper‐middle Bulgarian Lev BGL BFA Burkina Faso AFR Low CFA Franc XOF BDI Burundi AFR Low Burundi Franc BIF CPV Cabo Verde Republic of AFR Lower‐middle Cape Verde Escudo CVE KHM Cambodia WPR Lower‐middle Riel KHR CMR Cameroon AFR Lower‐middle CFA Franc XAF CAN Canada AMR High Canadian Dollar CAD CAF Central African Republic -

Islamic Banking Bulletin June 2013 Islamic

Islamic Banking Bulletin June 2013 Islamic Banking Department State Bank of Pakistan Islamic Banking Bulletin Apr-June 2013 Table of Contents “Islamic Finance News” Roadshow Pakistan 3 Keynote Address by Yaseen Anwar , Governor State Bank of Pakistan Islamic Banking Industry – Progress and Market Share 6 Country Model: Kingdom of Saudi Arabia 12 Adoption of AAOIFI Shariah Standards: Case of Pakistan 14 Events and Developments at IBD 20 (Shariah Islamic Banking Standard News 8: Case and ofView Pakistan)s 20 Annexure I: Islamic Banking Branch Network 24 Annexure II: Province wise Break-up of Islamic Banking Branch Network 25 Annexure III: City wise Break-up of Islamic Banking Branch Network 26 2 Islamic Banking Bulletin Apr-June 2013 Islamic Finance News Pakistan Roadshow Keynote Address Mr. Yaseen Anwar, Governor, State Bank of Pakistan, LRC, State Bank of Pakistan, Karachi Aug 27, 2013. Thank You for inviting me to speak at today‟s event. I am honored to have this opportunity of addressing such a distinguished audience. My appreciation to the organizers for once again having assembled a strong list of speakers at this year‟s Islamic Finance News Road show and a warm welcome to the international delegates. With all of us gathered here at the central bank sends a strong signal about commitment and determination of the State Bank of Pakistan and the Government towards ensuring sustainable growth of Islamic finance industry in the country. As I look around I am optimistic that the collective experience of speakers will lead to rich debates that will not only help us in understanding the key issues but will also enable us to map out the future of the industry. -

Bank Alfalah Limited SHELF PROSPECTUS for THE

ADVICE FOR INVESTORS INVESTORS ARE STRONGLY ADVISED IN THEIR OWN INTEREST TO CAREFULLY READ THE CONTENTS OF THIS PROSPECTUS ESPECIALLY THE RISK FACTORS GIVEN AT PART 6 OF THIS PROSPECTUS BEFORE MAKING ANY INVESTMENT DECISION. SUBMISSION OF FALSE AND FICTITIOUS APPLICATIONS IS PROHIBITED AND SUCH APPLICANT’S MONEY MAY BE FORFEITED UNDER SECTION 87(8) OF THE SECURITIES ACT, 2015 Bank Alfalah Limited SHELF PROSPECTUS FOR THE ISSUANCE OF RATED, SECURED, LISTED, REDEEMABLE TERM FINANCE CERTIFICATES OF PKR 50,000 MILLION (Under shelf registration over a period of 3-years) Date and Place of Incorporation: Karachi, June 21st, 1992, Incorporation Number: 0027580, Registered and Corporate Office: B.A. Building, I.I Chundrigar Road, Karachi, Contact Person: Muhammad Zeeshan, Contact Number: +92 21 3312 2126, Website: https://www.bankalfalah.com/, Email: [email protected] Type of Issue and Total Approved Issue Size: The Issue consists of Rated, Secured, Listed, Redeemable Term Finance Certificates (TFCs) having a Total Approved Issue Size of up to PKR 50,000 million. Time Period of Shelf Registration: The TFCs shall be issued in multiple tranches over a period of three (3) years from the date of publication of this prospectus. Size of Current Tranche Series A: Issue Size of Current Tranche Series A is PKR 11,000 million (inclusive of Green Shoe Option of PKR 1,000 million), out of which TFCs of PKR 9,000 million (82% of Issue Size) have been issued to and subscribed by Pre-IPO investors and TFCs of PKR 2,000 million (18% of Issue Size), inclusive of a Green Shoe Option of PKR 1,000 million, are being offered to the general public by way of an Initial Public Offering through this Shelf Prospectus. -

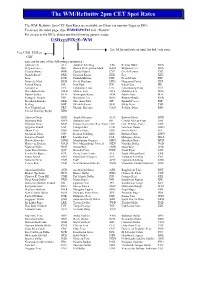

WM/Refinitiv 2Pm CET Spot Rates

The WM/Refinitiv 2pm CET Spot Rates The WM/ Refinitiv 2pm CET Spot Rates are available on Eikon via monitor Pages or RICs. To access the index page, type WMRESPOT01 and <Return> For access to the RICs, please use the following generic codes : USDxxxFIXzE=WM Use M for mid rate or omit for bid / ask rates Use USD, EUR or GBP xxx can be any of the following currencies : Albania Lek ALL Austrian Schilling ATS Belarus Ruble BYN Belgian Franc BEF Bosnia Herzegovina Mark BAM Bulgarian Lev BGN Croatian Kuna HRK Cyprus Pound CYP Czech Koruna CZK Danish Krone DKK Estonian Kroon EEK Ecu XEU Euro EUR Finnish Markka FIM French Franc FRF Deutsche Mark DEM Greek Drachma GRD Hungarian Forint HUF Iceland Krona ISK Irish Punt IEP Italian Lira ITL Latvian Lat LVL Lithuanian Litas LTL Luxembourg Franc LUF Macedonia Denar MKD Maltese Lira MTL Moldova Leu MDL Dutch Guilder NLG Norwegian Krone NOK Polish Zloty PLN Portugese Escudo PTE Romanian Leu RON Russian Rouble RUB Slovakian Koruna SKK Slovenian Tolar SIT Spanish Peseta ESP Sterling GBP Swedish Krona SEK Swiss Franc CHF New Turkish Lira TRY Ukraine Hryvnia UAH Serbian Dinar RSD Special Drawing Rights XDR Algerian Dinar DZD Angola Kwanza AOA Bahrain Dinar BHD Botswana Pula BWP Burundi Franc BIF Central African Franc XAF Comoros Franc KMF Congo Democratic Rep. Franc CDF Cote D’Ivorie Franc XOF Egyptian Pound EGP Ethiopia Birr ETB Gambian Dalasi GMD Ghana Cedi GHS Guinea Franc GNF Israeli Shekel ILS Jordanian Dinar JOD Kenyan Schilling KES Kuwaiti Dinar KWD Lebanese Pound LBP Lesotho Loti LSL Malagasy Ariary -

Pace (Pakistan) Limited

PACE (PAKISTAN) LIMITED UNCONSOLIDATED FINANCIAL STATEMENTS FOR THE PERIOD ENDED 30 SEPTEMBER 2020 Pace (Pakistan) Limited Company Information Board of Directors Shehryar Ali Taseer (Chairman) Non-Executive Aamna Taseer (CEO) Executive Shahbaz Ali Taseer Executive Shehrbano Taseer Non-Executive Mian Ehsan Ul Haq Non-Executive Kanwar Latafat Ali Khan Independent Shavez Ahmad Independent Chief Financial Officer Amir Hafeez Audit Committee Shavez Ahmad (Chairman) Mian Ehsan Ul Haq Kanwar Latfat Ali Khan Human Resource and Remuneration (HR&R) Committee Shavez Ahmad (Chairman) Aamna Taseer Kanwar Latafat Ali Khan Company Secretary Sajjad Ahmad Auditors KPMG Taseer Hadi & Co. Chartered Accountants Legal Advisers M/s. Imtiaz Siddiqui & Associates Bankers Allied Bank Limited Albaraka Bank (Pakistan) Limited Askari Bank Limited Bank Alfalah Limited Faysal Bank Limited Habib Bank Limited KASB Bank Limited MCB Bank Limited National Bank of Pakistan NIB Bank Limited Silkbank Limited Soneri Bank Limited Pair Investment Company Limited The Bank of Punjab United Bank Limited Registrar and Shares Transfer Office Corplink (Pvt.) Limited Wings Arcade, 1-K Commercial Model Town, Lahore Tele: + 92-42-5839182 Registered Office/Head Office 2nd Floor, Pace Shopping Mall Fortress Stadium, Lahore Cantt Lahore, Pakistan (042)-36623005/6/8 Fax: (042) 36623121, 36623122 DIRECTOR’S REPORT TO THE SHAREHOLDERS The Directors of Pace (Pakistan) Limited (“the Company”) take pleasure in presenting to its shareholders the Unconsolidated Interim Financial Statements of the Company for the quarter ended September 30, 2020. Operating Results: During period under review, the sales of the Company showed a decrease of Rs 51.85 million to come at Rs 89.57 million as compared to Rs. -

Frequently Asked Questions FAQ's What Type of Facility Is Ready Line?

SILKBANK READY LINE – Frequently Asked Questions FAQ’s What type of facility is Ready Line? It is a running finance facility. Mark-up is charged only on the utilized amount and for the number of days the loan amount is utilized. What is the tenor of the loan? Loan is extended for one year however the line is reviewed on yearly basis subject to the terms and conditions of the bank. What is the maximum loan amount that I can get? You can get any loan amount ranging from Rs. 50,000 to Rs. 2 million depending on your income level. How the pricing of this facility is determined? Pricing on Ready Line is variable and linked 1 year KIBOR. The mark-up rate is composed of 1 year KIBOR and a pre-defined spread. What is processing fee of Silkbank Ready Line? Processing fee is Rs 3,000 plus 16% FED. The Processing Fee can be reversed if the customer utilizes Rs. 20,000/- within 60 days from the date of disbursement. However, if you apply between 22nd April 2017 and 31st May (both dates inclusive), processing fee will be automatically reversed before payment due date. What is annual fee of Silkbank Ready Line? Annual fee is Rs 3,000 plus 16% FED and is not reversible. Where do I have to pay my monthly dues? You will submit your dues in your designated Re-payment account opened with Silkbank. Kindly do not submit payment in your Line Account to avoid confusion and imposition of Late Payment Charges (LPC). -

Security Council GENERAL

UNITED NATIONS S Distr. Security Council GENERAL S/AC.26/1999/17 30 September 1999 Original: ENGLISH UNITED NATIONS COMPENSATION COMMISSION GOVERNING COUNCIL REPORT AND RECOMMENDATIONS MADE BY THE PANEL OF COMMISSIONERS CONCERNING THE SECOND INSTALMENT OF “E4” CLAIMS GE.99-66179 S/AC.26/1999/17 Page 2 CONTENTS Paragraphs Page Introduction .................... 1 - 3 4 I. OVERVIEW OF THE SECOND INSTALMENT CLAIMS .... 4 - 7 4 II. THE PROCEEDINGS ................ 8 - 27 5 III. LEGAL FRAMEWORK ................ 28 8 IV. VERIFICATION AND VALUATION OF CLAIMS ...... 29 8 V. THE CLAIMS ................... 30- 109 8 A. Contract .................. 31- 43 9 1. Compensability ............. 36 9 2. Verification and valuation method . 37 9 3. Evidence submitted .......... 38- 43 10 B. Real property ............... 44- 51 11 1. Compensability ............. 45- 46 11 2. Verification and valuation method . 47 11 3. Evidence submitted ........... 48- 51 11 C. Tangible property ............. 52- 65 12 1. Compensability ............. 53 12 2. Verification and valuation method . 54 12 3. Evidence submitted ........... 55- 65 12 (a) Tangible property ......... 55- 56 12 (b) Stock ............... 57- 59 13 (c) Cash ............... 60- 61 13 (d) Vehicles ............. 62- 65 14 D. Income-producing property ......... 66- 69 14 E. Payment or relief to others ........ 70- 78 15 1. Compensability ............. 71- 74 15 2. Verification and valuation method . 75 16 3. Evidence submitted ........... 76- 78 17 F. Loss of profits .............. 79- 85 17 1. Compensability ............. 80 17 2. Verification and valuation method . 81 17 3. Evidence submitted ........... 82- 85 18 G. Receivables ................ 86- 92 18 1. Compensability ............. 87- 88 18 2. Verification and valuation method . 89 19 3. Evidence submitted ........... 90- 92 19 H.