Automotive-190704-3Q19 Strategy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ASEAN Light Vehicle Sales Update

February 2018 ASEAN Light Vehicle Sales Update ASEAN Light Vehicle Market Increases by 11% YoY in January 2018 In January 2018, total ASEAN Light Vehicle (LV) sales increased by 11% compared to the same month last year. This impressive result was driven by growth in every market except Malaysia, where sales declined by 2% year-on-year (YoY). Last December, automakers in Malaysia offered aggressive discounts, which pulled sales ahead, hence the downturn in January this year. Indeed, at 54k units sold, December 2017 marked the highest sales month last year, compared to an average of around 48k units in every other month. January’s total was also impacted by massive demand for the all-new Perodua Myvi, which led to a supply shortage. Local media reports indicate that that Perodua received 60k advance orders for the Myvi from mid-November 2017 to mid-March 2018, but delivered only 28k units of the model. Despite this downturn in the opening month of the year, the Malaysian LV market is still expected to post modest growth of 1.7% YoY, on sales of 582k for the full-year 2018. Support will come from new models launched by the country’s two national brands, as well as a strong rebound in exports, lower inflation from the strengthening ringgit, and additional government spending under the 2018 Budget, ahead of the upcoming general election. Sales in Thailand in January rose by 17% YoY, driven by a recovering economy and improving consumer confidence. With growth of 26.4% YoY, the PV segment made a substantial contribution to the increase, while the CV segment rose by 7.2% from the same month in 2017. -

Automotive-200103-1Q20 Strategy (Kenanga)

Sector Update 03 January 2020 Automotive NEUTRAL National Marques Overtaking on the Fast Lane ↔ By Wan Mustaqim Bin Wan Ab Aziz l [email protected] We maintain our NEUTRAL rating on the AUTOMOTIVE sector. The MIER consumer sentiment index scored 84.0 points (-9.0ppt QoQ, -23.5ppt YoY) in 3QCY19 which is below the optimistic threshold (>100pts) due to normalisation of consumer confidence post-tax holiday and weak macroeconomic outlook. Reflecting this, we are seeing car sales trending in favour of value-for-money national marques, as evident from their 11MCY19 TIV market share of 57%. Non-national marques on the other hand, are focusing on higher-margin lower-volume models (catering to higher purchasing power consumers). Notable developments in Automotive industry in 2019/2020 include: (i) national marques surpassing non-national marques in terms of market share, (ii) Proton has surpassed Honda as no.2 trailing behind Perodua, (iii) increasing number of new model launches, (iv) better incentives under National Automotive Policy 2020 (tentatively on 1QCY20), and (v) another OPR rate cut by 25bps (to 2.75%) in 2020, which should have minimal positive impact on vehicles loans. No changes to our 2019 TIV target of 600,000 units (+0.2%), and we introduce 2020 TIV target of 612,000 units (+2%) matching MAA’s target factoring the extra boost from national marques (Proton and Perodua). Our sector top-pick is BAUTO (OP; TP: RM2.65) for its defensible niche SUV market and attractive, steady dividend yield of 7.3%. National marques affirming leading market position . As of 11MCY19, the national marques (57%) continued to stay above non-national marques (43%) in terms of market share, marking a year not seen since 2013, owing to the outstanding sales from Perodua, especially after the introduction of its all-new Perodua Myvi and supported by the all-new Perodua Aruz (27,389 units delivered). -

Annual Report 2018 | 2019

Annual Report 2018 | 2019 CHAN E Weathering storms and braving changes brought on by a volatile economy, United Motors has set its course on the highway to sustainability, and to discovering innovative solutions. Driving sustainable initiatives and streamlining operations while embracing evolving technology, we have reinforced ourselves by rewiring our DNA and expanding our horizons. 02 UNITED MOTORS LANKA PLC Annual Report 2018 | 2019 UNITED MOTORS LANKA PLC Annual Report 2018 | 2019 03 Contents Vision and Mission 06 Our Beginnings 07 06-43 Our Journey Thus Far 08 Review of the Business Operational and Financial Highlights 11 Events of the Year 13 Group Structure 20 Chairman’s Message 22 Group CEO Review of Operations 26 Board of Directors 30 Senior Management Team 34 Management Discussion and Analysis 46 Business Review 55 46-89 Financial Capital 58 Manufactured Capital 60 Management Review Social & Relationship Capital 61 Human Capital 77 Natural Capital 87 Intellectual Capital 89 How We Govern 92 Audit Committee Report 107 92-127 Remuneration Committee Report 110 Governance Nomination Committee Report 112 Related Party Transactions Review Committee Report 113 Enterprise Risk Management 115 Directors’ Statement on Internal Controls 121 Annual Report of the Board of Directors 122 04 UNITED MOTORS LANKA PLC Annual Report 2018 | 2019 Financial Calendar 131 Statement of Directors’ Responsibility 132 131-204 CEO and CFO’s Responsibility Statement 134 Financial Information Independent Auditor’s Report 135 Statement of Profit or Loss and Other -

Dealership Staff Can Help Reduce the Number of Problems Owners Experience with Their New Vehicle

Dealership Staff Can Help Reduce The Number of Problems Owners Experience With Their New Vehicle Honda Receives Two Model-Level Awards For Initial Quality, Perodua and Toyota Each Get One KUALA LUMPUR: 27 November 2015 — The salesperson plays a critical role in reducing the number of problems owners experience with their new vehicle, according to the J.D. Power Asia Pacific 2015 Malaysia Initial Quality StudySM (IQS) released today. Automakers continue to add features, specifically entertainment and connectivity technology, to their vehicle. By explaining at the time of delivery all of the features of the vehicle and how they work, the salesperson can make sure the owner is comfortable with the technology thus significantly reducing the number of problems the owner experienced with their vehicle. The study finds that when the salesperson provides a comprehensive explanation of the vehicle and its features, owners report an average of 79 problems per 100 vehicles (PP100). In contrast, owners who indicate their salesperson provided no explanation, or only a partial explanation, report an average of 163 PP100. “With all of the new content automakers are putting in their vehicles, it is absolutely critical for salespeople to provide comprehensive explanation of vehicle, including a test drive, to make sure the customer fully understands how to operate all of the technology and its benefits,” said Rajaswaran Tharmalingam, country head, Malaysia, J.D. Power. “The technology may work exactly as it’s designed, but if the customer doesn’t know how to use it or had difficulties using it, they deem it a problem. The salesperson can greatly reduce those problems simply spending time with the customer during the delivery process going through the vehicle and its accessories.” Tharmalingam noted that given the importance of the test drive, only 59 percent of customers in Malaysia took one during their shopping process. -

PROCLAMATION of SALE MOTOR VEHICLES for Sale by Public Auction on Thursday, 13Th June 2019 @ 2.30 P.M Venue : Unit No

PROCLAMATION OF SALE MOTOR VEHICLES For Sale By Public Auction On Thursday, 13th June 2019 @ 2.30 p.m Venue : Unit No. 6 (B-0-6), Ground Floor, Block B Megan Avenue II, No 12, Jln Yap Kwan Seng, Kuala Lumpur www.ngchanmau.com/auto "Prospect bidders may submit bids for the Auto e-Bidding via www.ngchanmau.com/auto. *Please register at least one (1) working day before auction day for registration & verification purposes". To get a digital copy of auction listings by Car Make / Model, please SMS or Whatsapp to 012-5310600. LEGAL OWNER : CIMB BANK BERHAD (13491-P) / CIMB ISLAMIC BANK BERHAD (671380-H) REGN. TRANS RESERVE LOT REGISTRATION YEAR OF PUSPAKOM ENGINE CHASSIS MAKE & MODEL CARD REMARKS MISSIO PRICE NO NO MAKE VR 1 RESULT NUMBER NUMBER (YES / NO) N TYPE (RM) STORE YARD : G-MART SUNGAI SERAI - LOT 8253, BATU 11 3/4, JALAN HULU LANGAT, 43100 HULU LANGAT, SELANGOR TELEPHONE NO : (03) 9074 3815 VIEWING DATES : 7th & 10th June 2019 (10.00 AM - 4.00 PM) C101 VF6859 PERODUA ALZA 1.5 2016 NO PASSED G82B91K PM2M502G002296241 A 32,000.00 C102 BPL2786 PERODUA ALZA 1.5 2018 NO PASSED G53B57R PM2M502G002334048 A 41,000.00 C103 WC7514U PERODUA AXIA 1.0 2016 NO PASSED H29B48R PM2B200S003171513 A 18,600.00 C104 WC3976T PERODUA AXIA 1.0 2016 NO PASSED H21B93V PM2B200S003156396 A 18,600.00 C105 W2093G PERODUA MYVI 1.3 2013 NO PASSED T51A33T PM2M602S002140415 A 15,000.00 C106 WA2139M PERODUA MYVI 1.3 2014 YES PASSED T07B52A PM2M602S002183889 M 19,800.00 VR-1 NOT C107 WA1494D PERODUA MYVI 1.5 2014 NO WITHDRAWN R12A24L PM2M603S002103084 M 25,000.00 DONE -

Umw Holdings Berhad Corporate Presentation

BEYOND BOUNDARIES UMW HOLDINGS BERHAD CORPORATE PRESENTATION FEBRUARY 2020 UMW HOLDINGS BERHAD OUR BUSINESS DIVERSIFIED PORTFOLIO AUTOMOTIVE EQUIPMENT MANUFACTURING LANDBANK & ENGINEERING • Manufacture • Distribution • Manufacture of • Unlocking value • Assembly • Trading fan case of our vast landbank in • Distribution • Leasing • Manufacture of automotive Serendah • Sales & service • After-sales components service • Blending & distribution of lubricants UMW HOLDINGS BERHAD 2 OUR STRENGTH LEADER IN OUR CORE BUSINESS SEGMENTS AUTOMOTIVE EQUIPMENT MANUFACTURING & ENGINEERING • Leader in the Malaysian • Distribute Komatsu heavy • First Malaysian company to automotive industry with equipment in 5 countries in manufacture and assemble 51.4% market share (2019) the Asia-Pacific region. fan cases for Rolls-Royce as through Toyota, Lexus and a Tier 1 supplier. Perodua marques. • Hold more than 50% market share for Toyota forklift in • Manufacture and export Malaysia and Singapore; have KYB shock absorbers to 38 operations in 5 countries in countries from Malaysia. Asia-Pacific. UMW HOLDINGS BERHAD 3 OUR REVENUE AND PBT CONTRIBUTION SEGMENTAL BREAKDOWN 2014 2015 2016 2017 2018 1% 2% 6% 5% 6% 7% 6% 7% 7% 7% 13% 13% 14% 20% 13% 13% 14% 21% 22% 21% 86% 81% 81% 78% 81% 81% 79% 72% 71% 72% REVENUE PBT REVENUE PBT REVENUE PBT * REVENUE PBT * REVENUE PBT * Automotive Equipment Manufacturing & Engineering * Excluding Aerospace sub-segment (within Manufacturing & Engineering) which was loss-making due to start-up operations UMW HOLDINGS BERHAD 4 OUR INTERNATIONAL -

Global Trends and Malaysia's Automotive Sector

2021-3 Global Trends and Malaysia’s Automotive Sector: Ambitions vs. Reality Tham Siew Yean ISEAS - Yusof Ishak Institute Email: [email protected] March 2021 Abstract The paper seeks to examine the development of the Malaysian automotive sector in the midst of rapid global changes in technology, consumer preferences and sustainability concerns. The sector represents a case of infant industry protection which includes, among its objectives, the state’s aspiration to nurture Bumiputera entrepreneurs as national champions for the sector. Despite close to three decades of protection, the two national car projects continue to depend on foreign partners for technology support. The National Automotive Policies (NAPs) strive to push the sector towards the technology frontier with foreign and domestic investments while seeking to be a regional hub and grooming national Bumiputera champions. The inherent conflicts in these objectives create disincentives for investments while the domestic market is held captive to the national car producers. Although policies continue to espouse grand visions, the reality is that Malaysia’s car makers continue to be inward-looking and exporting remains insignificant. ------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------- JEL Classification: O14, O25 Keywords: Automotive Sector, Industrial Policy Global Trends and Malaysia’s Automotive Sector: Ambitions vs. Reality Tham Siew Yean 1. Introduction The use of state intervention for development has been espoused in theory and practice in many countries. The World Bank (1993) study on the East Asian miracle economies is often attributed to illustrate the success of state intervention in industrial policy. However, the study itself cautions that the use of industrial policy needs to be supported with good fundamental policies, evaluation and monitoring of the support given. -

News Release

Perusahaan Otomobil Nasional Sdn Bhd (100995-U) Persiaran Kuala Selangor, Seksyen 26, 40400 Shah Alam Selangor Darul Ehsan, Malaysia. T (+603) 5102 6000 F (+603) 5191 9120 News Release PROTON X70 AWARDED EXCEPTIONAL SCORES BY ASEAN NCAP - SUV awarded 5-star rating for occupant protection - Official public debut at KL International Motor Show Subang Jaya, 16 November 2018 – The Proton X70, the first SUV from PROTON, has successfully achieved a 5-star rating after being tested by the New Car Assessment Program for Southeast Asian Countries (ASEAN NCAP). Details for the latest round of ASEAN NCAP tests have been released, showing the newest Proton model sits near the top of its segment for occupant safety. Designed and manufactured to optimise occupant safety With a proven track record for manufacturing cars that obtain a 5-star ASEAN NCAP rating to defend – the Proton Iriz, Proton Persona, Proton Preve and Proton Suprima S are all 5-star rated, PROTON’s engineers and designers paid close attention to every detail to ensure the Proton X70 would obtain a high score based on the latest 2017-2020 testing protocol. Under the new protocol, safety assist technology is now taken into consideration and counts for 25% of the overall score. PROTON introduced Hot Press Forming (HPF) body structures, used to form the passenger cell of its cars, in 2012 and the same technology is one of the reasons why the Proton X70 is able to provide a high level of protection to its occupants. The HPF cell is supplemented with six airbags for all variants, ISOFIX child seat mounting points as well as seat belts with pretensioners and load limiters. -

Case Studies of Perodua Viva, Perodua Myvi and Proton Suprima

Journal of the Society of Automotive Engineers Malaysia Volume 3, Issue 3, pp 333-340, September 2019 e-ISSN 2550-2239 & ISSN 2600-8092 Parametric Study of a Blind Spot Zone: Case Studies of Perodua Viva, Perodua Myvi and Proton Suprima M. S. Muhamad Azmi*1,2, A. H. Ismail1,2, M. S. M. Hashim1,2, M. S. Azizizol1,2, S. Abu Bakar1,2, N. S. Kamarrudin1,2, I. I. Ibrahim1,2, M. R. Zuradzman1,2, A. Harun1,3, I. Ibrahim1,2, M. K. Faizi1,2, M. A. M. Saad1,2, M. F. H. Rani1,2, M. A. Rojan1,2 and M. H. Md Isa4 1Motorsports Technology Research Unit (MoTECH), Universiti Malaysia Perlis, Pauh Putra Campus, 02600 Arau, Perlis, Malaysia 2School of Mechatronic Engineering, Universiti Malaysia Perlis, Pauh Putra Campus, 02600 Arau, Perlis, Malaysia 3School of Microelectronic Engineering, Universiti Malaysia Perlis, Pauh Putra Campus, 02600 Arau, Perlis, Malaysia 4Malaysian Institute of Road Safety Research (MIROS, 43000 Kajang, Malaysia *Corresponding author: [email protected] ORIGINAL ARTICLE Open Access Article History: Abstract – The initial works on Blind Spot Zone (BSZ) identification presents the importance of the blind spot towards the everyday drive. The Received alarming collision rate in the blind spot zone especially when changing 20 Oct 2018 lanes has triggered the necessity of BSZ detection and warning system, focusing on a daily-used and affordable car segment. Such technologies Received in are recently available at top variant cars. Therefore, a low cost yet revised form facilitative BSZ detection and warning system is required. This paper 3 Aug 2019 presents the continuity experimental result of identification of the BSZ of Accepted three different car segments, i.e. -

Malaysia's Energy Efficient Vehicles (EEV) Concept (MAI, 2018)

© Journal of the Society of Automotive Engineers Malaysia www.journal.saemalaysia.org.my Global greenhouse emission from both urban development and uncontrolled pollution has resulted in today’s climate change. In addition, the increase in transport demands that utilize internal combustion engine has led to an escalating need for petroleum. This subsequently has resulted in the depletion of non-renewable resources. As one of the world’s oil producing nations, Malaysia also needs to find an alternative way to reserve energy while at the same time, reduce harmful emission from fuel combustion. To achieve such an objective, the National Automotive Policy (NAP) was conceived in 2014 after much debate and discussion on the environmental devastation and climate change affecting the nation (Zainul Abidin, 2018). One policy which stood as NAP’s main focus was to turn Malaysia into a regional hub of Energy Efficient Vehicles (EEV). What is EEV? People often wonder what EEV means aside from their benefits to the country’s economy and environment. Energy Efficient Vehicles (EEV) are vehicles that bring minimal harmful impacts to the environment in terms of carbon emission level (g/km) and fuel consumption (l/100km) compared to normal internal combustion engine vehicles. In order to control and reduce carbon emission, Malaysia has been involved in advanced technology transfer with more developed countries in addition to endorsing the Kyoto Protocol in 2002 to reduce 70 million tonnes of CO2 emission over a 20-year period. The country has also tried to apply the Clean Development Mechanism (CDM) to cut down at least 5% of CO2 emission compared to the current level where such a mechanism is used in the form of carbon credits or Certified Emission Reduction (CERs). -

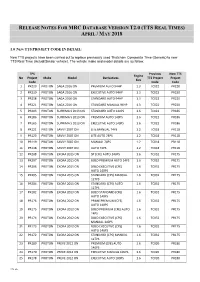

Release Notes for Mrc Database Version T2.0 (Tts Real Times) April / May 2018

RELEASE NOTES FOR MRC DATABASE VERSION T2.0 (TTS REAL TIMES) APRIL / MAY 2018 1.0 NEW TTS PROJECT CODE IN DETAIL: New TTS projects have been carried out to replace previously used Thatcham Composite Time (Generic) to new TTS Real Time (Actual/Similar vehicle). The vehicle make and model details are as follow: TPS Previous New TTS Engine No Project Make Model Derivatives TTS Project Project Size Code Code Code 1 PR220 PROTON SAGA 2016 ON PREMIUM AUTO 94HP 1.3 TC022 PR220 2 PR219 PROTON SAGA 2016 ON EXECUTIVE AUTO 94HP 1.3 TC022 PR220 3 PR218 PROTON SAGA 2016 ON STANDARD AUTO 94HP 1.3 TC022 PR220 4 PR221 PROTON SAGA 2016 ON STANDARD MANUAL 94HP 1.3 TC022 PR220 5 PR203 PROTON SUPRIMA S 2013 ON STANDARD AUTO 140PS 1.6 TC022 PR186 6 PR186 PROTON SUPRIMA S 2013 ON PREMIUM AUTO 140PS 1.6 TC022 PR186 7 PR165 PROTON SUPRIMA S 2013 ON EXECUTIVE AUTO 140PS 1.6 TC022 PR186 8 PR121 PROTON SAVVY 2007 ON LITE MANUAL 74PS 1.2 TC018 PR118 9 PR120 PROTON SAVVY 2007 ON LITE AUTO 74PS 1.2 TC018 PR118 10 PR119 PROTON SAVVY 2007 ON MANUAL 74PS 1.2 TC018 PR118 11 PR118 PROTON SAVVY 2007 ON AUTO 74PS 1.2 TC018 PR118 12 PR208 PROTON EXORA 2015 ON SP (CFE) AUTO 140PS 1.6 TC032 PR175 13 PR207 PROTON EXORA 2015 ON BOLD PREMIUM AUTO 14PS 1.6 TC032 PR175 14 PR206 PROTON EXORA 2015 ON BOLD EXECUTIVE (CFE) 1.6 TC032 PR175 AUTO 140PS 15 PR205 PROTON EXORA 2015 ON STANDARD (CPS) MANUAL 1.6 TC032 PR175 127PS 16 PR204 PROTON EXORA 2015 ON STANDARD (CPS) AUTO 1.6 TC032 PR175 127PS 17 PR182 PROTON EXORA 2013 ON BOLD STANDARD (CFE) 1.6 TC032 PR175 AUTO 140PS 18 PR176 PROTON -

News Release

Perusahaan Otomobil Nasional Sdn Bhd (100995-U) Persiaran Kuala Selangor, Seksyen 26, 40400 Shah Alam Selangor Darul Ehsan, Malaysia. T (+603) 5102 6000 F (+603) 5191 9120 News Release PROTON TO PURSUE EXPORT MARKETS IN 2021 - Saga and SUVs to spearhead growth in export sales - Target is to double export volume in the next 12 months Subang Jaya, 29 January 2021 – Following a year that saw it successfully overcoming challenges posed by the pandemic and launching a second SUV, Malaysian car manufacturer PROTON has set its sights on growing export sales in 2021. A flurry of activity in December that included the beginning of CKD operations in Kenya and the launch of the Proton X70 in Pakistan saw export sales end the year with an increase of nearly 50% compared to domestic sales that grew by 8.8%. For the coming year, the company has set itself another challenging target of doubling export sales over 2020, assuming that export activities are not overly hampered by restrictions due to the global pandemic. Spearheading the expansion will be PROTON’s most popular model, the evergreen Proton Saga, followed by the Proton X70 and Proton X50 as they are gradually introduced to more overseas markets. Exports to power PROTON’s future The export market is a vital part of PROTON’s long-term goal to be the third best-selling automotive brand in ASEAN by 2027. While sales leadership in the domestic market will always be a main priority, the company recognises that in order to grow for the future, it needs to expand its customer base and search for sales in other countries.