Trajectory of Automotive Industry and Government Intervention in Central

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rdsg 2016-Sk<0142>

ROCZNIKI DZIEJÓW SPOŁECZNYCH I GOSPODARCZYCH Tom LXXVI – 2016 HUBERT WILK Instytut Historii PAN PRÓBA MODERNIZACJI POLSKIEGO PRZEMYSŁU MASZYNOWEGO W DRUGIEJ POŁOWIE LAT 60. PRZYPADEK FIATA 125P Tempo postępu technicznego narzuca nam życie, narzuca nam sytuacja, świat, w któ- rym żyjemy. Władysław Gomułka1 Zarys treści: Tekst dotyczy podjętej w latach 60. XX w. próby zmodernizowa- nia polskiego przemysłu maszynowego. Działania decydentów zostały przed- stawione na przykładzie negocjacji i podpisania kontraktu licencyjnego na produkcję w FSO nowego samochodu fi ata 125p. Zawarcie umowy z włoskim Fiatem i rozpoczęcie wytwarzania średniolitrażowej osobówki miało mieć pozy- tywny wpływ na strukturę eksportu przemysłu maszynowego. The content outline: The paper focuses on the attempts of modernising the Polish machine industry in the 1960s. The undertakings of the decision- -makers are illustrated through the case of negotiating and signing license contract for the production of new motor vehicle, Fiat 125p, by the FSO. The cooperation with the Italian automobile company Fiat and the production of a car with mid-sized engine was meant to positively infl uence the structure of the export sector of the machine industry. Słowa kluczowe: PRL, przemysł motoryzacyjny, samochody, motoryzacja, duży fi at, lata 60. XX w. Keywords: Polish People’s Republic, automotive industry, cars, motorization, Fiat 125p, the 1960s 1 Przemówienie końcowe Władysława Gomułki podczas X Plenum Komitetu Cen- tralnego PZPR w dniu 18 kwietnia 1962 r., w: X Plenum Komitetu Centralnego Polskiej Zjednoczonej Partii Robotniczej w dniach 16–18 IV 1962 r., Warszawa 1962, s. 547. http://dx.doi.org/10.12775/RDSG.2016.14 412 Hubert Wilk Po październikowym przełomie społeczeństwo Polski coraz odważ- niej zaczynało domagać się dostępu do samochodów. -

Acta 115.Indd

Acta Poloniae Historica 115, 2017 PL ISSN 0001–6829 Mariusz Jastrząb and Joanna Wawrzyniak Department of Social Sciences, Kozminski University Joanna Wawrzyniak Institute of Sociology, University of Warsaw ON TWO MODERNITIES OF THE POLISH AUTOMOTIVE INDUSTRY: THE CASE OF FABRYKA SAMOCHODÓW OSOBOWYCH AND ITS STAFF (1948–2011)* Abstract Focusing on the history of the Polish main car factory, the FSO, the paper examines two modernisation waves in the country’s automotive industry: the socialist Government’s purchase of a license from the Italian Fiat in the 1960s and the acquisition of the factory by the Daewoo Corporation in the 1990s. The history of the FSO as an enterprise shows, above all, the pitfalls of dependent development. It has, however, resulted in the training of a class of specialists and engineers for whom the implementation of foreign technologies and management cultures presented opportunities for self-advancement, redefi nitions of their identity, along with reconsiderations of the value and meaning of work. Keywords: passenger cars, automotive industry, Fabryka Samochodów Osobowych (FSO), Fiat, Daewoo, Poland, socialism, capitalism, transformation 1 * Research work fi nanced within the programme of the Ministry of Science and Higher Education (Poland), under the name ‘The National Programme for the Development of Humanities’, between 2012–18. The authors would like to thank two anonymous readers for their helpful comments and Hanna Gospodarczyk for an initial report on the FSO and for delving into the archives of the Ministry of Treasury. Our gratitude goes also to interviewees participating in the project ‘From a Socialist Factory to an International Corporation: Archive Collection of Narrative Biographical Interviews’ for sharing with us their recollections, as well as to the students of the Institute of Sociology of the University of Warsaw for conducting these interviews (see also n. -

Summary of Background and Experience Bogdan

SUMMARY OF BACKGROUND AND EXPERIENCE BOGDAN THADDEUS FIJALKOWSKI Full Professor of Cracow University of Technology in Krakow and State Higher Vocational School in Nowy Sacz, Poland Academic Training Master of Science Electrics, Szczecin University of Technology (Politechnika Szczecinska), at present West-Pomeranian University of Technol- ogy (Zachodnio-Pomorski Uniwersytet Technologiczny), Szczecin, Poland, 1959 Doctor of Philosophy Electronics, Mining and Metallurgical Academy (Akademia Gorniczo-Hutnicza), Cracow, Poland, 1965 Doctor of Science Dynamics, Poznan University of Technology (Politechnika Poznanska), Poznan, Poland, 1988 Titular Professor Engineering Sciences, Cracow University of Technology (Politechnika Krakowska), Cracow, Poland, 1997 Full Professor Engineering Sciences, Cracow University of Technology (Politechnika Krakowska), Cracow, Poland, 2000 Professional Experience 1958-61 Teaching Assistant, Chair of Theoretical Electrotechnics, Szczecin University of Technology (Politechnika Szczecinska), Szczecin, Poland 1961-65 Teaching Senior Assistant, Chair of Mining Electrotechnics, Mining and Metallurgical Academy (Akademia Gorniczo-Hutnicza), Cracow, Poland 1965-68 Assistant Professor, Chair of Mining Electrotechnics, Mining and Metallurgi- cal Academy (Akademia Gorniczo-Hutnicza), Cracow, Poland 1968-69 Consultants for Automation and Mechanisation Works of the Non-ferrous Metal Industry - "ZAM", Kety, Poland 1968-72 Assistant Professor and Chairman, Mining Automation and Cybernetics Laboratory, Mining Electrotechnics Institution, -

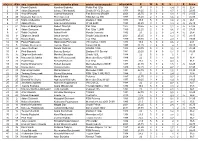

Miejsce Ekipa Imię I Nazwisko Kierowcy Imię I Nazwisko Pilota Marka I Model Pojazdu Rok Pojazdu R W a Q S I P Suma 1 13 Paweł

miejsce ekipa imię i nazwisko kierowcy imię i nazwisko pilota marka i model pojazdu rok pojazdu R W A Q S I P Suma 1 13 Paweł Głębicki Karolina Głębicka Polski Fiat 125p 1968 17 3 3 0 1,4 3 -5 22,4 2 34 Adam Bojanowski Łukasz Chlorkowski Skoda S110L De Luxe 1973 18,25 5 2 0 1,7 1 -5 22,95 3 56 Artur Wołowski Joanna Wołowska Fiat Seicento BRUSH 2003 25,75 0 1 0 1,8 1 -5 24,55 4 45 Krzysztof Kwiecień Piotr Kwiecień FSO Syrena 105 1973 18,25 2 1 0 1,6 2 24,85 5 23 Marta Godlewska Jolanta Wróbel Zastava 1100p 1978 19,5 5 3 0 1,6 2 -5 26,1 6 31 Adam Wierny Agnieszka Mocarska W124 E280 1993 23,25 3 1 0 1,9 2 -5 26,15 7 21 Mateusz Budzyński Robert Tkaczyk Fiat 126p 1977 19,25 5 2 0 1,1 5 -5 27,35 8 4 Adam Gorczyca Basia Kryczałło Fiat 126p 1.2MPI 1989 22,25 2 1 0 0,6 7 -5 27,85 9 51 Rafał Chyliński Adrian Kreft Honda Concerto 1992 23 2 2 0 2,4 4 -5 28,4 10 9 Zbigniew Jarosik Jakub Jarosik Skoda Czołg Octavia 2001 25,25 3 1 0 1,2 3 -5 28,45 11 14 Maciej Kopiś Mateusz Kopiś Fiat 126p 1979 19,75 2 3 1 2,3 1 29,05 12 48 Paweł Pająkowski Małgorzata Pozorska VW Garbus 1303S 1974 18,5 5 3 0 0,6 2 29,1 13 5 Bartosz Mielczarek Tomasz Myszk Ikarus 260.04 1985 21,25 2 4 0 2 1 30,25 14 20 Jacek Woźniak Dorota Woźniak SKODA 105S 1983 20,75 5 0 0 3,2 2 30,95 15 8 Piotr Bartnicki Bartosz Burdzel Zastava 101 Special 1981 20,25 5 4 0 1,7 5 -5 30,95 16 36 Zbigniew Borkowski Monika Skoczylas Skoda 120L 1988 22 5 3 0 0 1 31 17 18 Marzena Stefańska Marek Pietruszewski Mercedes-Benz 420SEC 1988 22 5 3 1 0,4 0 31,4 18 33 Paweł Kępa Krzysztof Banach Fiat 125p 1982 20,5 -

Samochody Z Żerania 1951-1977 / Marek Kuc. – Warszawa, 2017 Spis

Samochody z Żerania 1951-1977 / Marek Kuc. – Warszawa, 2017 Spis treści Od autora 7 Podziękowania 9 Powstanie i rozwój Fabryki Samochodów Osobowych 11 FSO Warszawa (1951-1973) 18 Warszawa M20 (1951) 18 Warszawa Pickup (prototyp 1955) 20 Warszawa M20 U (prototyp 1956) 21 Warszawa M20 model 1957 (później Warszawa 200) 21 Warszawa M20 Sanitarka (od 1957) 23 Warszawa M20 (pakiet modernizacji 1958 i 1959) 23 Warszawa 200P Pickup (od 1958) 24 Warszawa Ghia (prototypy 1959) 25 Warszawa 201 (od 1960) 26 Warszawa sedan (przedprototypy 1961) 27 Warszawa 202 (od 1962) 29 Warszawa 201P/202P Pickup, 201F/202F Furgon i Furgon przeszklony oraz 202A sanitarka (od 1963) 29 Warszawa 203/204, 223/224 w różnych wersjach (1964) 30 Warszawa 210 (prototyp 1964) 32 Warszawa 203 Taxi/204 Taxi (od 1965) 34 Warszawa ze zmodernizowanym układem napędowym (prototypy 1965-1969) 34 Warszawa ze zmodernizowanym przodem (prototypy 1967) 35 Warszawa - zmiana oznaczenia modelu i zakończenie produkcji (1968-1973) 37 FSO Syrena (1957-1972) 40 Syrena (prototypy 1954-1957) 40 Syrena 100 (od 1957) 42 Syrena z płytą podłogową zamiast ramy i silnikiem S-16 (prototyp 1958) 43 Syrena 101 (1960-1962) 43 Syrena Mikrobus (prototyp 1960) 44 Syrena Sport (prototyp 1960) 45 Syrena Kombi (prototyp 1961) 46 Syrena 104 (prototyp 1961) 47 Syrena 102 (1962-1963) 48 Syrena 102 S (1963) 49 Syrena 103/103 S (1963-1966) 49 Syrena 110 (prototypy 1964-1966) 50 Syrena 104 (1966-1972) 53 Syrena 104 Pickup/104 Furgon (prototypy 1968) 54 Syrena „laminat" (prototyp 1968) 54 Syrena 607 (prototyp 1970/1971) -

Sto Lat Polskiego Przemysłu Samochodów Osobowych

NierównościSpołeczneaWzrostGospodarczy,nr57(1/2019) DOI: 10.15584/nsawg.2019.1.26 ISSN1898-5084 mgr Arkadiusz D. Leśniak-Moczuk1 doktorant – Uniwersytet w Białymstoku Stolatpolskiegoprzemysłusamochodówosobowych Wstęp „Samochód króluje wszędzie i spełnia każdą pracę w dziedzinie komunika- cji. Przewozi bezpiecznie osoby z szybkością większą od pośpiesznego pociągu, nosi cierpliwie wielotonowe ładunki, rozwozi towary do najdalszych zakątków cywilizowanych krajów, dociera wszędzie tam, gdzie prowadzi jako taka droga, współzawodniczy z tramwajem i koleją żelazną, a nawet z samolotem. (…). Nie- sie pomoc w nagłych wypadkach, ratuje ludzi i dobytek, gasi pożary, zamiata i czyści ulice, ciągnie ładowne wozy przyczepne, (…) jest narzędziem pracy dla osób, środkiem godziwej rozrywki, zapewnia miły wypoczynek, jest narzędziem sportu krajowego i międzynarodowego i środkiem propagandy narodowej, czyn- nikiem obronności kraju” (Rychter, 1948, s. 3). Już w średniowieczu rozpoczęto próby budowy pojazdu mechanicznego wy- korzystując wiatr lub siłę żywej istoty znajdującej się na pojeździe. W 1600 r., w Holandii, Simon Stevin opracował wóz żaglowy poruszany przez wiatr na ko- łach i podwoziu mieszczącym 28 osób, poruszający się z szybkością 34 km na go- dzinę na trasie 68 km. W Anglii wykorzystano siłę latawców zaprzężonych do pojazdów konnych. Kroniki podają konstrukcję wehikułu poruszanego przez ukryte w skrzyniach konie biegnące po taśmie napędzającej koła. W Norymberdze w Niemczech w 1649 r. artysta kowal Johann Hautsch skonstruował drewniany wóz triumfalny ozdobiony skrzydlatym koniem z głową orła i aniołami dmącymi w trąby (wydającymi sygnały dźwiękowe), poruszany sprężyną naciąganą przed jazdą przez czterech pachołków (lub korbami przy kołach poruszanymi przez pachołków umieszczonych w czterech skrzyniach), osiągający prędkość 1,5 km na godzinę przez 200 m (Rychter, 1948, s. -

Turniej Techniczno – Motoryzacyjny 15-03-2019

TURNIEJ TECHNICZNO – MOTORYZACYJNY 15-03-2019 1. Arkusze mniejsze od A4 to A. A3 i A2 B. A5 i A6 C. B5 i B6 D. B2 i B3 2. Wartość odczytana na suwmiarce to A. 2,5 cm B. 6,3 cm C. 0,25 mm D. 0,3 mm 3. Dokładność odczytu na suwmiarce przedstawionej na rysunku wynosi A. 0,01mm B. 0,02mm C. 0,1mm D. 0,2mm 4. Poprawnie zrzutowany prostopadłościan znajduje się na rysunku: ODPOWIEEDŹ D. 5. Błędnie zwymiarowany otwór znajduje się na rysunku: ODPOWIEDŹ C. 6. Stop nieżelazny to A. stal B. mosiądz C. żeliwo D. staliwo 7. Brakujący rzut przedmiotu znajduje się na rysunku: ODPOWIEDŹ C. 8. Niewłaściwie zwymiarowana figura znajduje się na rysunku: ODPOWIEDŹ D. 9. Na rysunku przedstawiono A. tokarkę numeryczną B. frezarkę poziomą C. tokarkę konwencjonalną D. szlifierkę do wałków i otworów 11. Jaką drogę pokona samochód jadący już z prędkością początkową 15 m/s, który nagle zaczął jechać ruchem jednostajnie przyśpieszonym przez 3 sekundy i osiągnął prędkość 21 m/s? A. 45 m B. 54 m C. 61 m D. 105 m 12. Ile wynosi pojemność blaszanego naczynia w kształcie sześcianu o wewnętrznej krawędzi 10 cm? A. 0,1 litra B. 1 litr C. 10 litrów D. 100 litrów 12. Porównaj podane wartości prędkości i oceń, która z nich jest największa A. 500 m/min B. 200 mm/s C. 60 km/h D. 20 m/s 13. Traktor ciągnie kłodę po torze prostoliniowym siłą F = 2000 N. Ciężar kłody wynosi G = 4000 N. Ile wynosi wypadkowa wszystkich sił działających na kłodę, jeżeli porusza się ona ze stałą prędkością? A. -

Test Nr 11 - Historia Polskiej Motoryzacji

Test nr 11 - historia polskiej motoryzacji (test jednokrotnego wyboru – tylko jedna odpowiedź jest prawidłowa) 1. Poprzednikiem Poloneza był samochód: a. Warszawa b. Polski Fiat 125p c. Syrena 2. Produkcję Poloneza rozpoczęto: a. 3 maja 1978 roku b. 22 kwietnia 2002 roku c. 22 września 1975 roku 3. Produkcję Poloneza zakończono: a. 22 września 1975 roku b. 3 maja 1978 roku c. 22 kwietnia 2002 roku 4. Poloneza produkowano przez: a. 20 lat b. prawie 24 lata c. 26 lat 5. Ile Polonezów zostało wyprodukowanych (bez dostawczych Trucków i vanów Cargo)? a. 1 061 807 b. pół miliona c. 2 065 708 6. Jaką maksymalną prędkość osiągał Polonez? a. 125 km/h b. 150 km/h c. 175 km/h 7. Polonez był konstrukcyjnie przystosowany do przewozu maksymalnie: a. 4 osób b. 5 osób c. 9 osób 8. Polonez rozpędzał się do 100 km/h w czasie około: a. 10 sekund b. 12 sekund c. 18 sekund 9. Najczęściej produkowane były Polonezy z silnikiem o pojemności: a. 1300 cm sześciennych i 1500 cm sześciennych b. 1500 cm sześciennych i 1900 cm sześciennych c. 1800 cm sześciennych i 2000 cm sześciennych 10. Złote FSO Polonezy Caro otrzymali od rządu: a. siatkarze za zdobycie złotego medalu na Olimpiadzie w Montrealu b. piłkarze ręczni za zdobycie mistrzostwa Europy c. piłkarze nożni za zdobycie srebrnego medalu na Olimpiadzie w Barcelonie w 1992 roku 11. Od 1 kwietnia 1997 roku do 22 kwietnia 2002 roku producentem Poloneza był: a. koncern Fiata b. concern Opla c. Daewoo –FSO 12. 41 335 sztuk Polonezów wyeksportowano do: a. Bułgarii b. -

Make Model Version Kw Hp Body Motor Code Crit

MAKE MODEL VERSION KW HP BODY MOTOR CODE CRIT. POS. YEAR AUTOBIANCHI A 111 1.4 51 70 Saloon 124 BLC.000 R 08/69- 11/72 AUTOBIANCHI PRIMULA Berlina 1.2 48 65 Saloon R 01/68- 12/70 FIAT 124 (124_) 1200 48 65 Saloon 124 A.000 R 02/73- 07/75 FIAT 124 (124_) 1200 (TA) 44 60 Saloon 124 A.000 R 02/67- 10/73 FIAT 124 (124_) 1400 51 70 Saloon 124 B2.000 R 12/68- 12/72 FIAT 124 (124_) 1500 55 75 Saloon 124 B2.000 R 01/73- 07/75 FIAT 124 (124_) 1500 59 80 Saloon 124 AC.000 R 04/72- 07/75 FIAT 124 (124_) 1600 70 95 Saloon 124 A9.000, R 01/73- 132 AC.000 07/75 FIAT 124 Coupe (124_) 1400 Sport 66 90 Coupe 124 AC.000 R 06/67- 10/72 FIAT 124 Coupe (124_) 1600 (BC 1) 74 100 Coupe 125 B.000 R 11/71- 10/73 FIAT 124 Coupe (124_) 1600 (BC 1) 81 110 Coupe 125 B.000 R 04/70- 10/73 FIAT 124 Coupe (124_) 1600 Sport 76 104 Coupe 132 AC.000 R 08/72- 12/75 FIAT 124 Coupe (124_) 1600 Sport 80 108 Coupe 132 AC.000 R 08/72- 12/75 FIAT 124 Coupe (124_) 1800 Sport 82 112 Coupe R 01/73- 02/76 FIAT 124 Coupe (124_) 1800 Sport 87 118 Coupe R 01/73- (CC1) 02/76 FIAT 124 Familiare 1.4 51 69 Estate 124 B.000 R 09/67- (124_) 05/71 FIAT 124 Familiare 1200 44 60 Estate 124 A.000 R 04/67- (124_) 05/73 FIAT 124 Familiare 1200 48 65 Estate 124 A.000 R 05/73- (124_) 03/75 FIAT 124 Spider (124_) 1500 Sport 66 90 Convertible 124 AC.000 R 02/67- (BS) 12/72 FIAT 124 Spider (124_) 1600 Sport 82 112 Convertible 125 B.000 R 11/69- (BS) 08/73 FIAT 124 Spider (124_) 1600 Sport 74 100 Convertible 125 B.000 R 11/69- (BS1) 08/73 FIAT 124 Spider (124_) 1600 Sport 80 108 Convertible 125 B.000 -

Miejscenr Startowy Kierowca Pilot Pojazd Rocznikrocznik Punktyquiz

Miejscenr startowy kierowca pilot pojazd rocznikrocznik punktyquiz koło Pomocprzebranieświatłaitinerer suma 1 22 Marek Kosiński Tadeusz Ostrowicz Fiat 131 S Mirafiori 1977 19,25 0 1,25 0 0 0 1 21,5 2 13 Paweł Głębicki Karolina Mielewczyk Polski Fiat 125p 1968 17 0,5 7 0 -5 0 4,5 24 3 41 Piotr Bartnicki Maurycy Kiszkiel-Makiewicz Zastava 1100S 1981 20,25 0,5 5,25 0 -5 0 3 24 4 57 Jakub Zadrożny Piotr Spieglanin Alfa Romeo gt 1300 junior 1970 17,5 0,5 3,75 0 0 0 2,5 24,25 5 6 Jarosław Szewka MZ ES 250/2 Trophy 1967 16,75 1 1 0 0 0 6 24,75 6 16 Jacek Woźniak Dorota Woźniak Audi 80 GLS 1980 20 0 2 0 0 0 3 25 7 50 Adam Wierny Kamila Chełstowska Mercedes W115 200D 1975 18,75 2 2,5 0 0 0 2,5 25,75 8 10 Łukasz Kaźmierczak Marcin Lechecki Fiat 125p sanitarka 1989 22,25 2 5,75 -5 -5 0 6,5 26,5 8 29 Michał Zdończyk Aleksandra Rapacka-Zdończyk Fiat Cinquecento 1994 23,5 0 6,5 0 -5 0 1,5 26,5 10 19 Zbigniew Jarosik Jakub Jarosik Skoda Octavia 2001 25,25 0,5 2,25 -5 0 0 4 27 10 61 Tomasz Zieliński Wioleta Sekula Zastava 1100p 1980 20 1,5 4,5 0 0 0 1 27 12 38 Krzysztof Anioł Urszula Pączek Mercedes W124 1989 22,25 2 4,75 -5 0 0 3,5 27,5 13 34 Artur Szukała Jarosław Aleksiejew Mercedes 280 se 1974 18,5 1,5 1,5 0 0 0 6,5 28 13 49 Radosław Szymański Justyna Szymańska Mercedes W123 1980 20 1,5 0,5 0 0 0 6 28 15 18 Michał Srock Paulina Bielawska Mercedes 208 1993 23,25 2 0,25 0 -5 0 8,5 29 15 25 Michał Schulz Robert Kuchta Wartburg 353W Tourist 1987 21,75 0 3,25 0 0 0 4 29 17 2 Tomasz Groszewski Sylwia Wyrębska FSO 125p 1300 RHD 1984 21 0 7,25 0 -5 0 6 29,25 -

2016-Collector-Guide.Pdf

IXO MODELS road cars le mans & gt 4-11 20-25 rally cars truck collection 12-19 26-27 IST MODELS 28-31 PRX MODELS resin models diecast models 32-37 38-47 JCOLLECTION MODELS 48-51 5 IXO Models range is articulated around ROAD CARS the following thematics: Classic and Modern road cars, Classic and Modern racing cars, Classic and Modern bikes, Classic trucks and an outstanding selection of the best models from the 20’s and 30’s, IXO Museum. COMING SOON BERLIET 11CV Dauphine BMW 2000 CS BMW 2000 CS BMW 2002 BMW 2002 tii 1939 1966 1966 1972 - Police 1972 MUS 055 CLC 257 CLC 256 CLC 255 CLC 254 MOC | BMW 2002tii BMW M3 (E30) CHEVROLET Camaro CLC 1972 1990 - Nurburgring Taxi 2011 - Dubaï Police CLC 253 MOC 234 MOC 171 | MUS BUGATTI Type 41 Royale 1928 MUS 053 CHEVROLET Camaro CHEVROLET Corvette C3 BUGATTI Type 57 Galibier 2012 1980 1935 MOC 173 CLC 251 MUS 058 DELAGE D6-70 DELAGE D8 120-S Pourtout Aéro Coupe CITROEN DS3 “KENZO” CITROEN DS3 “Sport Chic” CITROËN Traction 7A 1936 1937 Edition 2010 2011 1934 MUS 057 MUS 054 MOC 120 MOC 122 CLC 265 7 DONKERVOORT D8GTO FACEL VEGA Excellence FORD CROWN Victoria 2013 1960 (Police Interceptor) MOC 152 MUS 051 MOC 161 ROAD CARS HONDA CIVIC SIR EG9 (Japan Specs) MOC 179 MOC | CLC GUMPERT APOLLO S HOMMEL RS Berlinette HONDA CIVIC SIR EG9 2010 1999 (Europe Specs) MOC 106 CLC 263 MOC 177 | MUS HOTCHKISS ANJOU HOTCHKISS ANTHEOR Cabriolet ISUZU ASKA CX JAGUAR MKVII JAGUAR XJ 1951 1953 1990 1954 2011 MOC 185 CLC 239 CLC 243 CLC 241 MOC 149 JAGUAR XK 140 Convertible JAGUAR XKR-S JAGUAR XKR-S JEEP C7 Laredo LAMBORGHINI -

Eladásra Kínált Tárgyak 2015. 04. 24

Eladásra kínált tárgyak listája 26db vezetékes telefon: 1db LB 24 Induktoros telefon (1924), 5000Ft 1db Siemens & Halske W38 Vezetékes telefon (1938), 5000Ft 2db induktoros telefon (1956), 5000Ft/db 1db BHG vizsgáló telefon fadobozban, 10000Ft 1db MM Mechanikai M űvek CB75MM fekete (1984), 4000Ft 1db MM Mechanikai M űvek CB75MM sárga, 4000Ft 1db MM Mechanikai M űvek CB75MM zöld/fehér, 4000Ft 1db MM Mechanikai M űvek CB75MM fehér, 4000Ft 1db MM Mechanikai M űvek CB667 piros (1976), 4000Ft 1db MM Mechanikai M űvek telefonvonal vizsgáló kagyló fehér, 4000Ft 1db CONCORDE 508MT számmemóriás vezetékes telefonkészülék, 1000Ft 1db SIEMENS Euroset 805 vezetékes telefonkészülék, 1000Ft 1db Stempo- Phone nyomógombos telefon (1980-as évek), 2000Ft 1db Nyomógombos telefon (1986), 1000Ft 1db ALPHA 59-2 nyomógombos vezetékes telefonkészülék (1990), 1000Ft 1db TRIFON 410 kiskazettás, üzenetrögzít ős vezetékes telefonkészülék (1993), 2000Ft 1db BUTTERFLY T-20 vezetékes telefon 1000Ft 1db ORTOPHON 22 vezetékes telefon, 1000Ft 1db ERICSSON vezetékes telefon, 1000Ft 1db KONTRAX GAMMA vezetékes telefon, 1000Ft 1db PANASONIC EASA Phone KX-T2365H, 1000Ft 1db CANON FAX-B110, 1000Ft 1db SANYO SFX210, 1000Ft 1db OLIVETTI JET-LAB 500 (2001), 1000Ft 1db PHILIPS Magic-3 Primo Fax (2003). 1000Ft Vezetékes telefonvonal kiegészít ő eszköz, szerszámok (135db): 1db iker- jelfogó, 3000Ft 1db telefonvonal villámvéd ő sor 3000Ft 100db villámvéd ő patronnal. 5000Ft 1db központi leválasztó kapocssor, 1000Ft 1db vezetékrendez ő, 1000Ft 30db-os készlet CA-1001 telefonközpont szerviz szerszámai (1971), 10000ft 1db ALCATEL 1000 ADSL LP (2005). 1000Ft 1db vezeték nélküli telefon: ASCOM AVEN 265 (2000). 5000Ft 6db személyhívó: Motorola Bravo (1988), 3000Ft NEC PA3AEA-1B (1990), 3000Ft NEC PA3E6-26B (1990), 3000Ft NEC 4C Acyclon, 3000Ft NEWTRON NT-300 Canada2421101 496A (1990), 3000Ft NOKIA OPERATOR TXT (1990).