The Predictive Power of Cyclical Consumption for Stock Market Returns in the Nordic Countries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Changes in the Arctic: Background and Issues for Congress

Changes in the Arctic: Background and Issues for Congress Updated May 22, 2020 Congressional Research Service https://crsreports.congress.gov R41153 Changes in the Arctic: Background and Issues for Congress Summary The diminishment of Arctic sea ice has led to increased human activities in the Arctic, and has heightened interest in, and concerns about, the region’s future. The United States, by virtue of Alaska, is an Arctic country and has substantial interests in the region. The seven other Arctic states are Canada, Iceland, Norway, Sweden, Finland, Denmark (by virtue of Greenland), and Russia. The Arctic Research and Policy Act (ARPA) of 1984 (Title I of P.L. 98-373 of July 31, 1984) “provide[s] for a comprehensive national policy dealing with national research needs and objectives in the Arctic.” The National Science Foundation (NSF) is the lead federal agency for implementing Arctic research policy. Key U.S. policy documents relating to the Arctic include National Security Presidential Directive 66/Homeland Security Presidential Directive 25 (NSPD 66/HSPD 25) of January 9, 2009; the National Strategy for the Arctic Region of May 10, 2013; the January 30, 2014, implementation plan for the 2013 national strategy; and Executive Order 13689 of January 21, 2015, on enhancing coordination of national efforts in the Arctic. The office of the U.S. Special Representative for the Arctic has been vacant since January 20, 2017. The Arctic Council, created in 1996, is the leading international forum for addressing issues relating to the Arctic. The United Nations Convention on the Law of the Sea (UNCLOS) sets forth a comprehensive regime of law and order in the world’s oceans, including the Arctic Ocean. -

FI IIR 2021 Part4 IPPU

FINLAND’s INFORMATIVE INVENTORY REPORT 2021 Air Pollutant Emissions 1980-2019 under the UNECE CLRTAP and the EU NECD Part 4 – IPPU March 2021 FINNISH ENVIRONMENT INSTITUTE Centre for Sustainable Consumption and Production Environmental Management in Industry – Air Emissions Team 1 Photo on the cover page: Ari Andersin (2008), Valkeakoski, ympäristöhallinnon kuvapankki 2 PART 4 IPPU 4 INDUSTRIAL PROCESSES and PRODUCT USE (NFR 2) 4.1 Overview of the sector 4.2 Mineral Products (NFR 2.A) Overview of the NFR category Cement production Lime production Glass production . Quarrying and mining of minerals other than coal Construction and demolition Storage, handling and transport of mineral products Other Mineral products 4.3 Chemical Industry (NFR 2.B) Overview of the NFR category Ammonia production Nitric acid production Adipic acid production Carbide production Titanium dioxide production Soda ash production and use Other chemical industry Storage, handling and transport of chemical products 4.4 Metal Industry (NFR 2C) Overview of the NFR category Iron and steel production Ferroalloys production Aluminium production Lead production Zinc production Copper production Nickel production Other metal production Storage, handling and transport of metal products Domestic solvent use including fungicides Road paving with asphalt Asphalt roofing 4.5 Solvent and Other Product Use (NFR 2D) Coating applications Degreasing Dry cleaning Chemical products Printing Other solvent (2D3i) and product (2G) use 4.6 Other industry (NFR 2H) Pulp and paper Food and -

The Stigma of Feminism: Disclosures and Silences Regarding Female Disadvantage in the Video Game Industry in US and Finnish Media Stories

This is a self-archived version of an original article. This version may differ from the original in pagination and typographic details. Author(s): Kivijärvi, Marke; Sintonen, Teppo Title: The stigma of feminism : disclosures and silences regarding female disadvantage in the video game industry in US and Finnish media stories Year: 2021 Version: Published version Copyright: © 2021 The Author(s). Published by Informa UK Limited, trading as Taylor & Francis Group Rights: CC BY-NC-ND 4.0 Rights url: https://creativecommons.org/licenses/by-nc-nd/4.0/ Please cite the original version: Kivijärvi, M., & Sintonen, T. (2021). The stigma of feminism : disclosures and silences regarding female disadvantage in the video game industry in US and Finnish media stories. Feminist Media Studies, Early online. https://doi.org/10.1080/14680777.2021.1878546 Feminist Media Studies ISSN: (Print) (Online) Journal homepage: https://www.tandfonline.com/loi/rfms20 The stigma of feminism: disclosures and silences regarding female disadvantage in the video game industry in US and Finnish media stories Marke Kivijärvi & Teppo Sintonen To cite this article: Marke Kivijärvi & Teppo Sintonen (2021): The stigma of feminism: disclosures and silences regarding female disadvantage in the video game industry in US and Finnish media stories, Feminist Media Studies, DOI: 10.1080/14680777.2021.1878546 To link to this article: https://doi.org/10.1080/14680777.2021.1878546 © 2021 The Author(s). Published by Informa UK Limited, trading as Taylor & Francis Group. Published online: -

Minutes of the 2020 SBI Telco Meeting Recommendations For

STEROL BIOSYNTHESIS INHIBITOR (SBI) WORKING GROUP Minutes from Annual Meeting on January 24th, 2020, 08:00 - 16:00, Protocol of the discussions and recommendations of the SBI working group of the Fungicide Resistance Action Committee (FRAC); updated on June 17th during the virtual SBI WG meeting Participants of the SBI WG Meetings ADAMA Martin Huttenlocher excused for virtual call BASF Martin Semar Gerd Stammler Bayer Frank Goehlich excused for virtual call Andreas Mehl Andreas Goertz Corteva Mamadou Kane Mboup FMC Henry Ngugi Sumitomo Yuichi Matsuzaki Yves Senechal no participation in virtual call Ippei Uemura Syngenta Stefano Torriani Paolo Galli Irina Metaeva Helge Sierotzki Venue of the annual meeting: Lindner Congress Hotel, Frankfurt Hosting organization: FRAC/Crop Life International Disclaimer The technical information contained in the global guidelines/the website/the publication/the minutes is provided to CropLife International/RAC members, non- members, the scientific community and a broader public audience. While CropLife International and the RACs make every effort to present accurate and reliable information in the guidelines, CropLife International and the RACs do not guarantee the accuracy, completeness, efficacy, timeliness, or correct sequencing of such information. CropLife International and the RACs assume no responsibility for consequences resulting from the use of their information, or in any respect for the content of such information, including but not limited to errors or omissions, the accuracy or reasonableness of factual or scientific assumptions, studies or conclusions. Inclusion of active ingredients and products on the RAC Code Lists is based on scientific evaluation of their modes of action; it does not provide any kind of testimonial for the use of a product or a judgment on efficacy. -

Neste Annual Report 2019 | Content 2 2019 in Brief

Faster, bolder and together Annual Report 2019 Content 02 03 2019 in brief ................................... 3 Sustainability ............................... 20 Governance ................................. 71 CEO’s review .................................. 4 Sustainability highlights ....................... 21 Corporate Governance Statement 2019 ........ 72 Managing sustainability ....................... 22 Risk management............................. 89 Neste creates value ......................... 25 Neste Remuneration Statement 2019 ........... 93 Neste as a part of society ................... 26 01 Stakeholder engagement ...................... 27 Strategy ..................................... 7 Sustainability KPIs ............................ 31 Our climate impact ............................ 33 04 Innovation .................................... 10 Our businesses ............................... 11 Renewable and recycled raw materials ......... 38 Review by the Board of Directors ......... 105 Key events 2019 .............................. 14 Supplier engagement ......................... 45 Key figures .................................. 123 Key figures 2019 .............................. 16 Environmental management ................... 48 Calculation of key figures ..................... 125 Financial targets .............................. 17 Our people ................................... 52 Information for investors....................... 18 Human rights ............................... 52 Employees and employment ................ -

Altia Annual Report 2019

ANNUAL REPORT 2019 CEO’S REVIEW CEO Pekka Tennilä comments on Altia’s 7 year 2019 SUSTAINABILITY Altia's sustainability 54 work in 2019 FINANCIAL STATEMENTS 2019 Consolidated financial 118 statements of Altia Group ANNUAL BUSINESS BOARD CORPORATE FINANCIAL REPORT OVERVIEW REPORT SUSTAINABILITY GOVERNANCE STATEMENTS 2 2019 Altia in brief HEAD OFFICE DISTILLERY ALTIA IS A LEADING NORDIC ALCOHOLIC BEVERAGE PRODUCTION BRAND COMPANY operating in the wine and spirits markets in the Nordic and Baltic countries. We produce, import, market, sell and SALES OFFICE distribute both own and partner brand beverages. We export alcoholic WAREHOUSE beverages to approximately 30 countries in Europe, Asia and North America. We want to support the development of a modern, responsi- ble Nordic drinking culture. We own some of the best known and loved wine and spirits brands in the region. Our flagship brands are Koskenkorva, O.P. Anderson and Larsen. Other iconic Nordic brands are Chill Out, Blossa, Xanté, Let’s Jaloviina, Leijona, Explorer and Grönstedts, among others. drink The portfolio of own brands is complemented with partner brands from better global leading wine and spirits houses. We also provide our customers with production, packaging and logistics services. In addition, by-products from the production process, such as starch, feed components and technical ethanols, are sold to industrial customers. Sustainability is a strategic priority and a key success factor for us. We are proud to work with products that are the best choice for the environment and for the climate, promoted and consumed responsibly. Our Koskenkorva distillery is a forerunner in bio- and circular economy, making use of 100% of the Finnish barley it uses as a raw ingredient. -

ESPAD Report 2019. Results from the European School Survey Project on Alcohol and Other Drugs

ESPAD Report 2019 Results from the European School Survey Project on Results from the European School Survey Project on Alcohol and Other Drugs School Survey Project the European Results from Alcohol and Other Drugs The ESPAD Group ESPAD Report 2019 ESPAD Legal notice Union Member State or any institution, agency or other body of the European Union. Send us your feedback about this publication and help us improve We are always interested in hearing feedback and suggestions for improvement from our customers. Use the link below, or scan the QR code on the right, to send https://europa.eu/!Xy37DU Freephone number (*): 00 800 6 7 8 9 10 11 More information on the European Union is available on the internet (http://europa.eu). Print ISBN 978-92-9497-108-1 doi:10.2810/289970 PDF ISBN 978-92-9497-110-4 doi:10.2810/564360 EPUB ISBN 978-92-9497-109-8 doi:10.2810/892603 © European Monitoring Centre on Drugs and Drug Addiction, 2016 © European School Survey Project on Alcohol and Other Drugs, 2016 Reproduction is authorised provided the source is acknowledged. Credits for photos: iStock. Recommended citation: ESPAD Group (2016), ESPAD Report 2015: Results from the European School Survey Project on Alcohol and Other Drugs, Printed in Luxembourg Praça Europa 1, Cais do Sodré, 1249-289 Lisbon, Portugal Tel. +351 211210200 [email protected] I www.emcdda.europa.eu twitter.com/emcdda I facebook.com/emcdda ESPAD Report 2019 Results from the European School Survey Project on Alcohol and Other Drugs ESPAD Group Sabrina Molinaro, Julian Vicente, Elisa -

Late Ediacaran Organic Microfossils from Finland

Geological Magazine Late Ediacaran organic microfossils from www.cambridge.org/geo Finland Sebastian Willman and Ben J. Slater Original Article Department of Earth Sciences, Palaeobiology, Uppsala University, Villavägen 16, SE-75236, Uppsala, Sweden Cite this article: Willman S and Slater BJ. Late Abstract Ediacaran organic microfossils from Finland. Geological Magazine https://doi.org/10.1017/ Here we present a detailed accounting of organic microfossils from late Ediacaran sediments S0016756821000753 of Finland, from the island of Hailuoto (northwest Finnish coast), and the Saarijärvi meteorite impact structure (~170 km northeast of Hailuoto, mainland Finland). Fossils were Received: 16 March 2021 recovered from fine-grained thermally immature mudstones and siltstones and are preserved Revised: 10 June 2021 Accepted: 24 June 2021 in exquisite detail. The majority of recovered forms are sourced from filamentous prokaryotic and protistan-grade organisms forming interwoven microbial mats. Flattened Nostoc-ball-like Keywords: masses of bundled Siphonophycus filaments are abundant, alongside Rugosoopsis and Ediacaran; Bilateria; microbial mats; acritarchs; Palaeolyngbya of probable cyanobacterial origin. Acritarchs include Chuaria, Leiosphaeridia, impact crater; organic-walled microfossils; Symplassosphaeridium and Synsphaeridium. Significantly, rare spine-shaped sclerites of Baltica bilaterian origin were recovered, providing new evidence for a nascent bilaterian fauna in Author for correspondence: the terminal Ediacaran. These findings offer a direct body-fossil insight into Ediacaran Sebastian Willman, mat-forming microbial communities, and demonstrate that alongside trace fossils, detection Email: [email protected]; of a bilaterian fauna prior to the Cambrian might also be sought among the emerging record Ben Slater, Email: [email protected] of small carbonaceous fossils (SCFs). -

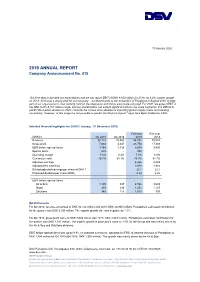

2019 ANNUAL REPORT Company Announcement No

7 February 2020 2019 ANNUAL REPORT Company Announcement No. 815 “Q4 2019 was in line with our expectations and we can report EBIT of DKK 6,654 million for 2019, an 8.4% organic growth on 2018. 2019 was a strong year for our company – not least thanks to the acquisition of Panalpina in August 2019. A large part of our organisation is now working hard on the integration and things are progressing well. For 2020, we expect EBIT in the DKK 8,200-8,700 million range, and our shareholders can expect significant returns via share buybacks. It is difficult to predict the market situation in 2020; currently the corona virus situation is impacting global supply chains and creating uncertainty. However, at this stage it is not possible to predict the financial impact,” says Jens Bjørn Andersen, CEO. Selected financial highlights for 2019 (1 January - 31 December 2019) Full-year Full-year (DKKm) Q4 2019 Q4 2018 2019 2018 Revenue 30,122 20,945 94,701 79,053 Gross profit 7,084 4,447 23,754 17,489 EBIT before special items 1,784 1,338 6,654 5,450 Special items 609 - 800 - Operating margin 5.9% 6.4% 7.0% 6.9% Conversion ratio 25.2% 30.1% 28.0% 31.2% Adjusted earnings 4,456 4,093 Adjusted free cash flow 3,678 3,916 Diluted adjusted earnings per share of DKK 1 22.1 22.1 Proposed dividend per share (DKK) 2.50 2.25 EBIT before special items Air & Sea 1,195 897 4,506 3,693 Road 272 239 1,251 1,147 Solutions 340 223 1,013 709 Q4 2019 results For Q4 2019, revenue amounted to DKK 30,122 million (Q4 2018: DKK 20,945 million). -

GENERAL ELECTIONS in FINLAND 14Th March 2019

GENERAL ELECTIONS IN FINLAND 14th March 2019 European Social-Democrats and populists Elections monitor run neck and neck in Finland The Social Democratic Party (SDP) came out ahead in the general elections in Finland on Corinne Deloy 14th April. With 17.7% of the vote and 40 seats (+6 in comparison with the previous election on 19th April 2015), the SDP led by Antti Rinne was only just ahead of the True Finns (PS), a populist, nationalist, Eurosceptic party led by Jussi Halla-aho, which won 17.5% of the vote and 39 seats (+1). The Conservative Assembly (KOK) led by Petteri Orpo, follows them Results closely with 17% of the vote and 38 seats (+1). “For the first time since 1999 we are the leading party in Finland,” said the Social Democratic leader, who had hoped however for a higher result for his party. The real loser in the election is the Centre Party (KESK), far-left party led by Li Andersson won 8.2% of the vote led by outgoing Prime Minister Juha Sipilä, the only party and 16 seats (+4). Finally, the Swedish People’s Party to have lost seats. It came fourth with 13.8% and 31 (SFP), representing the interests of the Swedish minority, seats (-18), the poorest result in its history. “We are the led by Anna-Maja Henriksson did not win its wager to biggest losers in these elections,” admitted the outgoing increase the number of its seats in the Eduskunta/ head of government when the results were announced. Riksdag, the only house of Parliament. -

UPM ANNUAL REPORT 2019 UPM ANNUAL REPORT 2019 3 UPM in Changing World

ANNUAL REPORT 2019 CONTENTS OUR OUR THE WAY ACCOUNTS STRATEGY 14 BUSINESSES 32 WE OPERATE 58 GOVERNANCE 100 FOR 2019 118 CONTENTS UPM IN CHANGING WORLD OUR STRATEGY OUR BUSINESSES THE WAY WE OPERATE GOVERNANCE ACCOUNTS FOR 2019 4 FUTURE BEYOND FOSSILS 16 UPM BIOFORE STRATEGY – 34 BIOFORE COMPANY 60 OUR RESPONSIBILITY 102 SIGNIFICANT DECISIONS 120 REPORT OF THE BOARD OF is a key driver for UPM going BEYOND FOSSILS Leading the forest-based TARGETS UPM’s Board of Directors made DIRECTORS forward. We create value by seizing the bioindustry into a sustainable, Our strategy guides us in achieving several significant decisions for limitless potential of bioeconomy. innovation driven and exciting our responsibility targets for 2030 the future. 144 FINANCIAL STATEMENTS 6 THE NEED FOR RESPONSIBLE future beyond fossils. and our contributions to UN SDGs. CHOICES 18 TOP PERFORMANCE 110 REMUNERATION 210 AUDITOR’S REPORT Our innovations create value and Continuous improvement, right 36 BUSINESS AREAS 62 VALUE FROM STAKEHOLDER business opportunities that go operating model, performance culture The direction and performance ENGAGEMENT 112 BOARD OF DIRECTORS beyond fossils. and effective capital allocation. of our six business areas. Active and open dialogue with 214 OTHER FINANCIAL our stakeholders provides valuable 114 GROUP EXECUTIVE TEAM INFORMATION 8 SUSTAINABLE AND SAFE 20 SPEARHEADS FOR GROWTH 52 NEW SUSTAINABLE input. SOLUTIONS We have selected three focus areas ALTERNATIVES Our alternatives for fossil-based where we are seeking significant growth. Developing wood-based 68 ENABLING PEOPLE GROWTH materials. renewable biofuels, naphtha and Our people and Aiming Higher 22 INNOVATING FOR GROWTH biochemicals. culture drive our success. -

Background and Issues for Congress

Changes in the Arctic: Background and Issues for Congress Updated November 4, 2020 Congressional Research Service https://crsreports.congress.gov R41153 Changes in the Arctic: Background and Issues for Congress Summary The diminishment of Arctic sea ice has led to increased human activities in the Arctic, and has heightened interest in, and concerns about, the region’s future. The United States, by virtue of Alaska, is an Arctic country and has substantial interests in the region. The seven other Arctic states are Canada, Iceland, Norway, Sweden, Finland, Denmark (by virtue of Greenland), and Russia. The Arctic Research and Policy Act (ARPA) of 1984 (Title I of P.L. 98-373 of July 31, 1984) “provide[s] for a comprehensive national policy dealing with national research needs and objectives in the Arctic.” The National Science Foundation (NSF) is the lead federal agency for implementing Arctic research policy. Key U.S. policy documents relating to the Arctic include National Security Presidential Directive 66/Homeland Security Presidential Directive 25 (NSPD 66/HSPD 25) of January 9, 2009; the National Strategy for the Arctic Region of May 10, 2013; the January 30, 2014, implementation plan for the 2013 national strategy; and Executive Order 13689 of January 21, 2015, on enhancing coordination of national efforts in the Arctic. On July 29, 2020, the Trump Administration announced that career diplomat James (Jim) DeHart would be the U.S. coordinator for the Arctic region. The Arctic Council, created in 1996, is the leading international forum for addressing issues relating to the Arctic. The United Nations Convention on the Law of the Sea (UNCLOS) sets forth a comprehensive regime of law and order in the world’s oceans, including the Arctic Ocean.