Agung Podomoro Land

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Supply RETAIL SECTOR

Research & Forecast Report Jakarta I Retail Accelerating success. “Limited new retail supply in DKI Jakarta brought the After the start of operations of Baywalk Mall, which is located occupancy rate up 2% to 89.3%. In contrast, the greater within the Green Bay Pluit Complex, Jakarta saw little new retail Jakarta area outside DKI Jakarta registered a slight decline space provided from the extension projects at Mall Puri Indah in occupancy to 82% due to the opening of two new retail (around 3,000 sq m) and Mall Kelapa Gading (around 6,000 sq centers. In the meantime, the average asking base rental m). These extended spaces are designed as F&B areas. With rate in Jakarta climbed by 3.3% q-o-q to IDR491,675 / sq m the small addition, the Jakarta retail cumulative supply moved / month. Similarly in the greater Jakarta area, the average upward to 4.32 million sq m as of 1Q 2014. Of this, 2.86 million sq asking base rent moved to IDR302,618 / sq m / month, m or 66.3% was marketed for lease. representing a 9.2% increase compared to last quarter.” Historically, after growing by 10% and bringing huge supply to - Ferry Salanto, Associate Director | Research the market in 2009, the annual growth of supply of retail space in Jakarta began weakening. From 2010 to 2013, the average growth was only 3.6% per year. In 2014, the growth of supply for shopping centres in Jakarta will continue declining. Although St RETAIL SECTOR Moritz is a huge mall expected to enter the market, overall, the total additional supply is only 138,200 sq m. -

PT Agung Podomoro Land Tbk

PT Agung Podomoro Land Tbk Public Expose 2 Desember 2019 0 Disclaimer Presentasi ini dipersiapkan semata-mata dan secara eksklusif untuk para pihak terundang untuk tujuan diskusi. Baik presentasi maupun isinya tidak boleh diperbanyak, atau digunakan tanpa izin tertulis dari PT Agung Podomoro Land Tbk. Presentasi ini dapat berisi pernyataan yang menyampaikan harapan berorientasi masa depan yang mewakili pandangan Perusahaan saat ini untuk perkiraan kejadian dan keuangan masa depan. Pandangan tersebut disajikan berdasarkan asumsi saat ini, yang mungkin memiliki berbagai risiko dan potensi perubahan. Disajikan berdasarkan asumsi yang dianggap benar pada saat ini, dan berdasarkan data yang tersedia pada saat presentasi ini dibuat. Perusahaan tidak dapat menjaminan bahwa pandangan tersebut akan, sebagian atau secara keseluruhan, akhirnya terwujud. Hasil yang sebenarnya dapat berbeda secara signifikan dari yang diproyeksikan. 1 Agenda 1. Tentang Perusahaan 2. Kinerja Operasional 3. Kinerja Keuangan 2 PT Agung Podomoro Land Tbk (APLN) Pendapatan Berulang .Malls .Hotels .Lainnya .Pengembang terkemuka dan terdiversifikasi .Pionir pengembangan superblock .Model pengembangan property terintegrasi . IPO di tahun 2010 Penjualan .Pengembangan Superblock .Rumah tapak/apartemen .Lainnya 3 Project Locations 4 Lahan untuk pengembangan* (Hektar) Medan; Balikpapan; 4,9 5,2 Greater Jakarta; Batam; 58,2 40,8 Bandung; 1,8 Karawang ; 5,7 Bogor; 91,2 Dalam Pengembangan Pengembangan; 209 Mendatang; 554 Bali; 7,4 Makassar; 15,0 Jakarta; 36,3 Bandung; 120,5 * Tidak termasuk reklamasi Karawang; 374,9 5 Agenda 1. Tentang Perusahaan 2. Kinerja Operasional 3. Kinerja Keuangan 6 Sekilas 2019 . Penjualan Sofitel senilai Rp 1,6 triliun pada Maret 2019. Pelunasan Obligasi Berkelanjutan I APLN Tahap II Tahun 2014 sebesar Rp750 miliar Juni 2019 . -

Perjanjian Perkawinan Dan Asas Keseimbangan

Calyptra: Jurnal Ilmiah Mahasiswa Universitas Surabaya Vol.7 No.1 (2018) PERJANJIAN PERKAWINAN DAN ASAS KESEIMBANGAN STEVEN SAMUEL Fakultas Hukum Universitas Surabaya Abstrak-Masyarakat terdiri dari individu atau kelompok-kelompok yang berhimpun untuk berbagai keperluan dan tujuan. Salah satu bentuk hubungan antara individu dalam masyarakat ialah melakukan perkawinan. Perkawinan menimbulkan akibat hukum bagi pihak suami dan istri dalam perkawinan yaitu terbentuknya harta benda dalam perkawinan. Oleh karena itu, Pasal 29 Undang-Undang Nomor 1 Tahun 1974 tentang Perkawinan memberikan kesempatan bagi para pihak untuk dapat membuat perjanjian perkawinan. Ketentuan ini juga memberikan kesempatan bagi para calon mempelai untuk mengesampingkan ketentuan yang mengatur seluk beluk harta perkawinan yang di atur dalam Pasal 35 Undang-Undang Nomor 1 Tahun 1974 sehingga para calon mempelai dapat menggunakan karakteristik dalam BW. Meskipun perjanjian perkawinan dapat dilakukan penyimpangan, tetapi Asas Keseimbangan juga melekat dalam perjanjian tersebut. Tujuan utama dari Asas Keseimbangan adalah kepatutan sosial atau menjamin tercapainya keseimbangan antara 1 individu dengan individu lainnya atau individu dengan masyarakat. Dengan dapat melakukan penyimpangan terhadap Pasal 29 Undang-Undang Nomor 1 Tahun 1974, isi perjanjian perkawinan tersebut tidak boleh bertentangan dengan kepatutan sosial salah satunya yaitu norma kesusilaan. Berkenaan dengan adanya Asas Keseimbangan, diharapkan Asas Keseimbangan mendukung para pihak untuk mencapai tujuan yang diseimbangkan dan yang memberikan dasar bagi penyesuaian atau penghapusan sebagian dari suatu perjanjian. Kata Kunci : Perkawinan, Perjanjian Perkawinan, Asas Keseimbangan, Kepatutan Sosial, Kesusilaan. Abstract-Community consists of individuals or groups who come together for a variety of purposes and objectives. One form of the relationship between individuals in the community is to conduct marriages. -

BAB II TINJAUAN OBJEK STUDI 2.1. Tinjauan Umum Apartemen

BAB II TINJAUAN OBJEK STUDI 2.1. Tinjauan Umum Apartemen 2.1.1. Pengertian Apartemen a. Apartemen merupakan tempat tinggal suatu bangunan bertingkat yang lengkap dengan ruang duduk, kamar tidur, dapur, ruang makan, jamban, dan kamar mandi yang terletak pada satu lantai, bangunan bertingkat yang terbagi atas beberapa tempat tinggal. (Kamus Umum Bahasa Indonesia, 1994, p : 69). b. Beberapa unit hunian yang saling berbagi akses yang sama dan dilingkupi oleh struktur kulit bangunan yang sama. (Site Planning,1984 : 252). c. Sebuah unit tempat tinggal yang terdiri dari Kamar Tidur, Kamar Mandi, Ruang Tamu, Dapur, Ruang Santai yang berada pada satu lantai bangunan vertikal yang terbagi dalam beberapa unit tempat tinggal. Apartemen harus memberikan keindahan, kenyamanan, keamanan dan privasi bagi keluarga yang tinggal di dalamnya. (Joseph De Chiara & John Hancock Callender Time Server Standart, 1968). d. Sebuah ruangan atau beberapa susunan ruangan dalam beberapa jenis yang memiliki kesamaan dalam suatu bangunan yang digunakan sebagai rumah tinggal. (Stein, 1967). e. Apartemen merupakan bangunan hunian yang dipisahkan secara horisontal dan vertikal agar tersedia hunian yang berdiri sendiri dan mencakup bangunan bertingkat rendah atau bangunan tinggi, dilengkapi berbagai fasilitas yang sesuai dengan standar yang ditentukan. ( Ernst Neufert, 1980, p : 86 ). f. Kamar atau beberapa kamar (ruangan) yang diperuntukkan sebagai tempat tinggal, terdapat di dalam suatu bangunan yang biasanya mempunyai kamar atau ruangan- ruangan lain semacam itu (Poerwadarminta, 1991). g. Apartemen adalah bangunan yang memuat beberapa grup hunian, yang berupa rumah flat atau rumah petak bertingkat yang diwujudkan untuk mengatasi masalah perumahan akibat kepadatan tingkat hunian dan keterbatasan lahan dengan harga yang terjangkau di perkotaan. -

Edisi 37 | II-2016

1 EDISI 37 | II-2016 WWW.PODOMOROMAGAZINE.COM PODOMOROINTERIOR DESIGN • PROPERTY • LIFESTYLE MODERN INDONESIA PENATAAN YANG DIBUAT SERUPA DENGAN RUANG DALAM HUNIAN MENYAMBUT KEDATANGAN PENGUNJUNG DENGAN HANGAT. Rp49,000 ISSN 2442-2479 4 1 PODOMORO - EDISI 37 | II - 2016 2 3 EDITor’S LETTER Tanah Air yang sempat loyo pada tahun lalu. Kini, masyarakat yang berencana membeli rumah kedua pun akan mendapatkan kemudahan merealisasikan mimpinya untuk ”naik kelas”. Menanggapi berita baik tersebut, majalah Podomoro pun mengulas soal dampak yang akan ditimbulkan jika aturan baru ini segera direalisasikan. Langsung saja membuka halaman Property Outlook,dan Anda akan mendapatkan gambaran lebih lengkap mengenai hal ini. Berbagai informasi menarik dan informatif juga masih setia kami suguhkan kepada Anda. Untuk mengetahui produk rumah tangga dan furnitur terbaru, langsung saja membuka halaman Highlights. Sementara pilihan perabotan dengan tema organik dan tropikal telah kami seleksi dalam rubrik Accent. Bagi INDRA WIDJAJA ANTONO Anda yang mencari inspirasi desain interior, silahkan tengok section Design yang mengulas rancangan interior hunian, toko, MENYAMBUT SINYAL dan kantor. Bagian Lifestyle akan membawa Anda POSITIF PROPERTI menjelajahi dunia teknologi, mode, dan otomotif yang sedang digandrungi kaum urban. Tak lupa, rubrik Food tetap hadir INDONESIA dengan ulasan soal dessert bar yang sedang booming di ibu kota. Yang istimewa, halaman Travel kali ini kami hadirkan dalam dua tema – Tokyo dan Rinjani – agar panduan liburan Anda semakin komplet. emasuki semester kedua 2016, Segmen Property and the Podomoro ekonomi Indonesia rupanya juga masih setia menyapa Anda, dengan masih diuji dengan sejumlah halaman Lobby’s Hall sebagai bagian tantangan di berbagai industri. pembuka. Sementara itu, info terkini MMeski demikian, sejumlah sentimen positif mengenai proyek-proyek terbaru Agung sudah mulai terlihat, dan memberikan secercah Podomoro Land dapat Anda temukan harapan bagi masyarakat. -

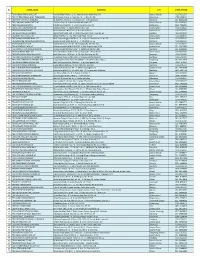

No STORE NAME ADDRESS2 CITY STORE PHONE 1 TBS

No STORE_NAME ADDRESS2 CITY STORE_PHONE 1 TBS PONDOK INDAH MALL JKT Pondok Indah Mall Lt. 1 - JL. Metro Pondok Indah Blok IIIB Jakarta Selatan 021-7692353 2 TBS CIPUTRA SERAYA MALL PEKANBARU Mall Ciputra Seraya Lt. Dasar No.18 - Jl. Riau No. 58 Pekanbaru 0761-868618 3 TBS PARIS VAN JAVA BANDUNG RL B20 Paris Van Java - Jl. Sukajadi 137 - 139, Bandung Bandung 022-82063649 4 TBS GANDARIA MAIN STREET JKT Gandaria City - Jl. Sultan Iskandar Muda No. 57 Jakarta Selatan 021-29053091 5 TBS E-WALK BALIKPAPAN E Walk Superblok GF - Jl. Jendral Sudirman No. 71 Balikpapan 0542-7586881 6 TBS KELAPA GADING MALL JKT Kelapa Gading - Jl. Boulevard Raya Kav. 144 Jakarta Utara 021-4533422 7 TBS PLAZA SENAYAN JKT Plaza Senayan 2 ND Floor - JL. Asia Afrika No. 8 Jakarta Pusat 021-5725179 8 TBS GALAXY MALL SURABAYA Galaxy Mall G.101-102 - Jl. Dharmahusada Indah Timur No.14 Surabaya 031-5915032 9 TBS PLUIT MEGA MALL JKT Mega Mall Pluit GF - JL. Pluit Indah Raya No. 36 Jakarta Utara 021-6683878 10 TBS TAMAN ANGGREK MALL JKT Mall Taman Anggrek UG Floor - JL. Letjen S. Parman Kav. 21 No. 78 Jakarta Barat 021-5639296 11 TBS BANDUNG INDAH PLAZA BANDUNG Bandung Indah Plaza GF NO. 5 - Jl. Merdeka No. 56 Bandung 022-4233521 12 TBS BLOK M PLAZA JKT Blok M Plaza UG - 01 - 02 - Jl. Bulungan No. 76 Keb. Baru Jakarta Selatan 021-7209041 13 TBS INDONESIA PLAZA JKT Plaza Indonesia LB# B-08 FLOOR - Jl. MH Thamrin Kav.28-30 Jakarta Pusat 021-29923853 14 TBS TRANS STUDIO MALL BANDUNG Bandung Supermall 1ST Floor - Jl. -

List Store Ibox

List Store iBox NO Store Name Addres 1 IBOX NEW KOTA KASABLANKA JL. Casablanca Raya Kav. 88, Jakarta Selatan, DKI 2 IBOX CILANDAK TOWN SQUARE Cilandak Town Square Ground Floor #065, Jl. T.B. 3 IBOX GANDARIA CITY Gandaria City 1st Floor #189, Jl. KH. M. Syafi'i Hadzami 4 IBOX KEMANG Lippo Mall Kemang 2nd Floor L2-27, Jl. Pangeran 5 IBOX PEJATEN VILLAGE Pejaten Village Lt. L2 – 08-09 Jl. Warung Jati Barat No. 6 IBOX RATU PLAZA 2 Ratu Plaza 1st Floor #8, Jl. Jendral Sudirman No. 9 7 IBOX MALL OF AMBASSADOR II Mal Ambasador 3rd Floor #18, Jl. Prof. Dr. Satrio Kav. FIRST FLOOR, UNIT NO. FL1 - 22 MARGO CITY, JL. 8 IBOX MARGO CITY MARGONDA RAYA NO. 358, DEPOK 16423 Ground Floor / 01 Jl. Juanda No. 99 Bakti Jaya Sukma 9 IBOX PESONA SQUARE DEPOK Jaya, Kota Depok, Jawa Barat 16418 10 IBOX FLAGSHIP SENAYAN CITY Senayan City 4th Floor #4-29 Jl. Asia Afrika Lot 19 Kode IBOX FLAGSHIP SUMMARECON Jl. Boulevard raya Gading Serpong Pakulonan Barat 11 MALL SERPONG Kelapa Dua Unit #GF211-212-215 IBOX BAYWALK MALL (GREEN Bay Walk Mall 4th Floor #36 Green Bay Pluit Jl. Pluit 12 BAY PLUIT) Karang Ayu, Penjaringan, Jakarta Utara 14450 Unit GF A3 001,002,016,017 Jl. Boulevard Artha Gading 13 IBOX MAL ARTHA GADING No.1, RT.18/RW.8, Klp. Gading Bar., Kec. Klp. Gading, Kota Jkt Utara, Daerah Khusus Ibukota Jakarta 14240 Mall of Indonesia Ground Floor #GF–A5 Jl. Raya 14 IBOX MALL OF INDONESIA NEW Boulevard Barat, Kelapa Gading, Jakarta Utara 14240 Jl. -

Jakarta Property Highlights

RESEARCH FIRST HALF 2012 Jakarta property highlights HIGHLIGHTS Indonesia's economy remained resilient, expanding at 6.4% (yoy) in the second quarter of 2012 as rising investment and domestic spending offset a slowdown in export demand due to Europe's sovereign debt crisis. Office space absorption remained strong with no signs of slowing down, marking the second consecutive record high since the second half last year. With surging corporate growth plans in a relatively tight market, a higher rental and price appreciation is expected. On the back of strong private consumption and aggressive retailer expansion, the Jakarta retail market continued to experience growing demand. The trend of promising retail sales growth and internationalization of retailers looks set to continue this year with a strong competitive landscape. Condominium prices continued to post a significant upward trend supported by positive buyer sentiment, lower interest rates and steady increases in sales. Continued demand coming from the Western and Asian expatriates, especially corporate tenants, together with the locals helped to sustain the pace of rental apartment growth. With increased business traveling from private companies and government institutions, the Jakarta hotel market recorded positive results across all three key performance metrics. FIRST HALF 2012 Jakarta property highlights ECONOMY IN BRIEF Maintained Growth Despite Global Headwinds Indonesia's economy remained resilient, expanding at 6.4% (yoy) in the second quarter of 2012 as rising investment and domestic spending offset a slowdown in export demand due to Europe's sovereign debt crisis. Strong consumer spending, strengthening infrastructure and foreign investment are expected to sustain growth with consensus forecasts within the low end of 6% target range in 2012 on weaker external demand. -

Laporan Notifikasi Pemberitahuan

V E R S I P U B L I K PENDAPAT KOMISI PENGAWAS PERSAINGAN USAHA NOMOR A13411, A13711 TENTANG PENGAMBILALIHAN SAHAM PERUSAHAAN PT KARYA GEMILANG PERKASA, DAN PT ALAM HIJAU TEDUH OLEH PT AGUNG PODOMORO LAND Tbk LATAR BELAKANG 1. Berdasarkan Peraturan Pemerintah No. 57 Tahun 2010 tentang Penggabungan atau Peleburan Badan Usaha dan Pengambilalihan Saham Perusahaan yang Dapat Mengakibatkan Terjadinya Praktik Monopoli dan Persaingan Usaha Tidak Sehat (PP No. 57 Tahun 2010) jo. Peraturan Komisi Pengawas Persaingan Usaha No. 10 Tahun 2010 tentang Pemberitahuan Penggabungan atau Peleburan Badan Usaha dan Pengambilalihan Saham Perusahaan (Perkom No. 10 Tahun 2010) jo. Peraturan Komisi Pengawas Persaingan Usaha No. 10 Tahun 2011 tentang Perubahan Peraturan Komisi Pengawas Persaingan Usaha No. 13 Tahun 2010 tentang Pedoman Pelaksanaan tentang Penggabungan atau Peleburan Badan Usaha dan Pengambilalihan Saham Perusahaan yang Dapat Mengakibatkan Terjadinya Praktik Monopoli dan Persaingan Usaha Tidak Sehat (Perkom No. 10 Tahun 2011), Komisi Pengawas Persaingan Usaha (Komisi) telah menerima Pemberitahuan dari PT Agung Podomoro Land Tbk atas pengambilalihan saham (akuisisi) perusahaan yang dilakukan oleh PT Agung Podomoro Land Tbk terhadap: 2. PT Karya Gemilang Perkasa yang diterima Komisi pada tanggal 19 Oktober 2011; dan 1 V E R S I P U B L I K 3. PT Alam Hijau Teduh yang diterima Komisi pada tanggal 17 November 2011. 4. Pada tanggal 29 November 2011 dokumen Pemberitahuan dinyatakan lengkap dan terhitung tanggal tersebut, Komisi melakukan Penilaian dengan mengeluarkan Surat Penetapan Nomor 85/KPPU/Pen/XI/2011. PARA PIHAK 5. Badan Usaha Pengambilalih: PT Agung Podomoro Land Tbk PT Agung Podomoro Land Tbk (APLN) adalah suatu perseroan yang berkedudukan di Jakarta Barat, didirikan dan menjalankan kegiatan usahanya menurut dan berdasarkan peraturan perundang-undangan Republik Indonesia. -

Jakarta Property Market Report

Research & Forecast Report 4Q 2013 Jakarta1st Quarter | Office 2014 Jakarta Property Market Report Accelerating success. Contents Office Sector 4 Apartment Sector 14 Retail Sector 24 Industrial Estate Sector 33 2 Research & Forecast Report | 1Q 2014 | Contents | Colliers International Highlights Office Sector After a gloomy 4Q 2013, leasing and sales of office space began to pick up momentum in 1Q 2014. Further, average asking base rental rates in the CBD showed a growth of 8.6% that brought the average rent to IDR247,444 / sq m / month. Similarly, asking By Ferry Salanto base rents in US dollar-denominated buildings moved upward slightly by 3.7% q-o-q to USD35.91 / sq m/ month. The average Associate Director | Research occupancy rate in the CBD stabilized at 96.5%. In terms of strata- [email protected] title office buildings, average asking prices also increased both in US dollars and in rupiah to USD4,750 / sq m and IDR45.9 million / sq m respectively. Apartment Sector The strong sales performance of under-construction apartment projects continued to trigger increases in the average asking price to IDR24.4 million / sq m or a 2.5% increase q-o-q. The CBD fetched the highest average price at IDR 38.3 million / sq m, an increase of 5.8% q-o-q while the average price in South Jakarta was registered at IDR 26.7 million / sq m, which grew by 3.2% from the last quarter. Not only price, but the average gross rental rate of apartments for lease located in the CBD and South Jakarta also trended upward by 3.4% compared to the previous quarter in anticipation of the increase in the operational costs and was recorded at USD26.56 / sq m/month. -

Strategi Bisnis Pt. Agung Podomoro Land (Apl) Dalam Terus Mengembangkan Bisnis

STRATEGI BISNIS PT. AGUNG PODOMORO LAND (APL) DALAM TERUS MENGEMBANGKAN BISNIS Oleh : Kanda Bagus Pratama Nim : 125100207111016 Kelas: TEP-E SEKILAS TENTANG PT. AGUNG PODOMORO LAND (APL) Siapa yang tak kenal PT Agung Podomoro Land (APL)? Pengembang properti ini adalah jagonya superblok. Mixed use development yang menggabungkan beragam fasilitas. Mulai perkantoran, lifestyle center, apartemen, hingga sarana pendidikan dan kesehatan. Di Ibu Kota, APL dikenal sukses menghadirkan produk properti berkualitas di lokasi yang strategis. Podomoro City di kawasan Jakarta Barat misalnya, merupakan superblok yang paling dibanggakan APL. Lokasinya yang strategis dan dilengkapi Central Park Mall yang memiliki lahan terbuka hijau seluas 1,5 hektare. Juga superblok lainnya di kawasan strategis seperti Kuningan City, Senayan City, dan Green Bay Pluit. Taman di dalam mal ini memiliki aneka jenis tanaman, dengan komposisi pohon- pohon rindang di lingkar dalam taman, tanaman hias di lingkar luar taman, ada pula beberapa jenis kolam dari yang masih kecil sampai dewasa untuk ikan jenis koi dan kura-kura dari Brasil. Kemajuan dan ekspansi bisnis kelompok usaha ini yang berkembang pesat dan sulit ditandingi oleh perusahaan properti lainnya. PT. Sunter Agung merupakan perusahaan pengembang real estat yang juga perusahaan induk dari Agung Podomoro Group, yang telah terjun dalam bisnis properti selama lebih dari 40 tahun. Baik perusahaan maupun semua anak perusahaan memiliki kepentingan besar dalam pengembangan real estat dan properti seperti hunian (perumahan, apartemen, townhouse), komersial (mall, ruko), perkantoran, dan pengembangan superblok inovatif multifungsi di daerah-daerah bisnis yang strategis. Perusahaan ini berdiri pada tahun 1969. Seiring dengan perkembangannya, Agung Podomoro Group telah mengambil alih beberapa pengembang properti di kawasan Sunter yang memiliki masalah keuangan. -

Marketing Strategy of Senior Living D'khayangan Jababeka Cikarang

MARKETING STRATEGY OF SENIOR LIVING D’KHAYANGAN JABABEKA CIKARANG By: Shita Oktaviani Nurhikmah 014201400120 A Skripsi presented to the Faculty of Business President University in partial fulfillment of the requirement for Bachelor Degree in Management March 2018 i SKRIPSI ADVISOR RECOMMENDATION LETTER This skripsi entitled “STRATEGY MARKETING OF SENIOR LIVING D’KHAYANGAN JABABEKA CIKARANG“ prepared and submitted by Shita Oktaviani Nurhikmah in partial fulfillment of the requirements for the degree of Bachelor in Faculty of Business has been reviewed and found to have satisfied the requirement for a skripsi to fit to be examined. I therefore recommend this skripsi for Oral Defense. th Cikarang, Indonesia, 29 March 2018 Acknowledged by, Recommended by, Dr. Dra. Genoveva, M.M Sonny V. Sutedjo, SE, MM Head of Management Study Program Advisor ii DECLARATION OF ORIGINALITY I declare that this skripsi, entitled “STRATEGY MARKETING OF SENIOR LIVING D’KHAYANGAN JABABEKA CIKARANG “ is to the best of my knowledge and beliefs, an original piece of work that has not been submitted, either in whole or in part, to another university to obtain a degree. Cikarang, Indonesia, 29 th March 2018 Shita Oktaviani N NIM : 01420140012 iii ABSTRACT This research highlights the marketing strategy for d‟khayangan, a senior living company at Jababeka Cikarang, so as to improve it sales. The objective of this research are to determine the current problems in marketing in Senior Living D‟khayangan, so the occupancy totally less than the total capacities, the consumer perception of d‟khayangan, and the effective promotion strategies for d‟khayangan to achieve the target. This research uses qualitative methods research.