Preparatory Survey on Industrial Zone

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Naming of Traditional Rice Varieties by the Farmers of Laos S

CHAPTER 10 Naming of traditional rice varieties by the farmers of Laos S. Appa Rao, J.M. Schiller, C. Bounphanousay, A.P. Alcantara, and M.T. Jackson The collection of traditional rice varieties from throughout Laos, together with a sum- mary of the diversity observed and its conservation, has been reviewed in Chapter 9 of this monograph. While undertaking the collection of germplasm samples from 1995 to early 2000, information was collected from farmers on the special traits and significance of the different varieties, including the vernacular names and their mean- ings. Imperfect as literal translations might be, the names provide an insight into the diversity of the traditional rice varieties of Laos. Furthermore, the diversity of names can, when used with care, act as a proxy for genetic diversity. When collecting started, variety names were recorded in the Lao language and an agreed transliteration into English was developed. The meanings of the variety names were obtained from all possible sources, but particularly from the farmers who donated the samples, together with Lao extension officers and Lao research staff members who understood both Lao and English. Variety names were translated literally, based on the explanations provided by farmers. For example, the red color of glumes is often described in terms of the liquid from chewed betel leaf, which is dark red. Aroma is sometimes indicated by the names of aromatic flowers like jasmine or the response to the aroma that is emitted by the grain of particular varieties during cooking. This chapter provides a summary of the information collected on the naming of traditional Lao rice varieties. -

Preparatory Survey on Vientiane Logistics Park (VLP) Project (PPP Infrastructure Project) in Lao P.D.R

Ministry of Public Works and Transport Lao Peoople’s Democratic Republic (Lao PDR) Preparatory Survey on Vientiane Logistics Park (VLP) Project (PPP Infrastructure Project) In Lao P.D.R. Final Report July 2015 Japan International Cooperation Agency (JICA) Nippon Express Co., Ltd. Nittsu Research Institute and Consulting, Inc. Nittsu Real Estate Co., Ltd. OS International Development Center of Japan Inc. JR 15-054 Ministry of Public Works and Transport Lao Peoople’s Democratic Republic (Lao PDR) Preparatory Survey on Vientiane Logistics Park (VLP) Project (PPP Infrastructure Project) In Lao P.D.R. Final Report July 2015 Japan International Cooperation Agency (JICA) Nippon Express Co., Ltd. Nittsu Research Institute and Consulting, Inc. Nittsu Real Estate Co., Ltd. International Development Center of Japan Inc. Exchange Rate (February 2015) 1USD=118.59JPN 1THB=3.64JPN 1KIP=0.015JPN Preparatory Survey on Vientiane logistics Park (VLP) Project in Lao PDR. Final Report Preparatory Survey on Vientiane Logistics Park (VLP) Project (PPP Infrastructure Project) in Lao P.D.R. Final Report Summary 1. Project Name Vientiane Logistics Park (VLP) (1) Project Site The Thanaleng area where the VLP is planned is located 15 km east-west from downtown Vientiane. It lies opposite Nong Khai Municipality of Thailand, so that Thanaleng has been traditionally a strategic place as a river-crossing point. In 1993, the first Friendship Bridge was completed at the Thanaleng area, which continues to hold its strategic position as an international cross border point. Dongphosy Forest is located approximately 3 km north from the bridge, which is under Vientiane Capital. The railway passes through the forest, and the Thanaleng station is located 3.5 km from the bridge. -

National Integrated Water Resources Management Support Project (Cofinanced by the Government of Australia and the Spanish Cooperation Fund for Technical Assistance)

Technical Assistance Consultant’s Report Project Number: 43114 August 2014 Lao People’s Democratic Republic: National Integrated Water Resources Management Support Project (Cofinanced by the Government of Australia and the Spanish Cooperation Fund for Technical Assistance) Prepared by: IDOM Ingenieria Y Consultoria S.A. (Vizcaya, Spain) in association with Lao Consulting Group Ltd. (Vientiane, Lao PDR) For: Ministry of Natural Resources and Environment Department of Water Resources Nam Ngum River Basin Committee Secretariat This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. NATIONAL INTEGRATED WATER RESOURCES MANAGEMENT SUPPORT PROGRAM ADB TA-7780 (LAO) PACKAGE 2: RIVER BASIN MANAGEMENT NIWRMSP - PACKAGE 2 FINAL REPORT August 2014 NIWRMSP - PACKAGE 2 FINAL REPORT National Integrated Water Resources Management Support Program ADB TA-7780 (LAO) Package 2 - River Basin Management CONTENTS EXECUTIVE SUMMARY IN ENGLISH ................................................................................................... S1 EXECUTIVE SUMMARY IN LAO ........................................................................................................... S4 1. BACKGROUND ............................................................................................................................... 1 2. RESOURCES ASSIGNED TO THE TECHNICAL ASSISTANCE .................................................. 2 3. WORK DEVELOPED AND OBJECTIVES -

Working for Health in the Lao People's Democratic Republic, 1962-2012

YEARS Working for Health in the Lao People’s Democratic Republic 5 1962–2012 Fifty Years Working for Health in the Lao People’s Democratic Republic 1962–2012 WHO Library Cataloguing in the Publication Data Fifty years: working for health in the Lao People’s Democratic Republic, 1962-2012 1. Delivery of healthcare. 2. Health services. 3. Laos. 4. National health programs. 5. Primary health care. I. World Health Organization Regional Office for the Western Pacific. ISBN 978 92 9061 601 6 (NLM Classification: WA 530) © World Health Organization 2013 All rights reserved. The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the World Health Organization concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. Dotted lines on maps represent approximate border lines for which there may not yet be full agreement. The mention of specific companies or of certain manufacturers’ products does not imply that they are endorsed or recommended by the World Health Organization in preference to others of a similar nature that are not mentioned. Errors and omissions excepted, the names of proprietary products are distinguished by initial capital letters. The World Health Organization does not warrant that the information contained in this publication is complete and correct and shall not be liable for any damages incurred as a result of its use. Publications of the World Health Organization can be obtained from Marketing and Dissemination, World Health Organization, 20 Avenue Appia, 1211 Geneva 27, Switzerland (tel: +41 22 791 2476; fax: +41 22 791 4857; email: [email protected]). -

Lao People's Democratic Republic United Nations Development Programme

ສາທາລະນະລດັ ປະຊາທິປະໄຕ ປະຊາຊນົ ລາວ ອງົ ການສະຫະປະຊາຊາດເພ� ອການພດັ ທະນາ Lao People's Democratic Republic United Nations Development Programme Government of Lao People’s Democratic Republic Executing Entity/Implementing Partner: Ministry of Agriculture and Forestry, MAF, Vientiane, Lao PDR Implementing Entity/Responsible Partner: National Agriculture and Forestry Research Institute, NAFRI United Nations Development Programme Analysis of conditions for Farmer Organizations and Cooperatives from a viewpoint of Climate Change Adaptation and Resilience, and recommendations for improvements Project ID:00076176 / ATLAS Award ID 60492 Improving the Resilience of the Agriculture Sector in Lao PDR to Climate Change Impacts (IRAS Lao Project) Project Contact : Mr. Khamphone Mounlamai, Project Manager Email Address : [email protected] EDITED VERSION - 23/11/2012 Disclaimer The views, analysis and opinions expressed in this report are those of the author at the time of the study implementation. They should not be interpreted as representing views or position of IRAS project, UNDP or any other government institution, international organization or project. IRAS Laos Project Analysis of conditions for Farmer Organizations and Cooperatives from a viewpoint of Climate Change Adaptation and Resilience, and recommendation for improvements Table of Content Table of Content ................................................................................................................................. i I. Project Information and Resources ......................................................................................... -

330 Forest Utilization by Local People in Sang Thong

FOREST UTILIZATION BY LOCAL PEOPLE IN SANG THONG DISTRICT Khamvieng Xayabouth* 1. Introduction Lao People’s Democratic Republic is a landlocked country in Southeast Asia, occupying the northern section of the Indochinese peninsula. It is surrounded by China, Vietnam, Cambodia and Myanmar. Laos is mountainous country, particularly in the north where the peaks rise to 2,500 meters. The high mountains along the eastern border which separate Laos from Vietnam are the source of east- west rivers which cross the country emptying into the Mekong river which flows through the country for almost 500 kilometers and defines the boundary between Laos and both Thailand and Myanmar. The population of Laos is approximately 4.5 million (1996). The majority of this population lives on the fertile plains along the Mekong River. The population growth is estimated to be approximately 2.9 percent a year. Although still a minority, the percent of population living in urban areas is growing steadily and the labor force is estimated to be about 1.5 million. The economy of the country is dominated by agriculture. Agriculture products constitute 60 percent of the gross national product (GNP) with 85-90 percent of the total labor force employed in agricultural activities. The principle agriculture products are rice, wheat, potatoes, and fruits. Industry accounts for about 16 percent of the GNP. The major industrial products are tin, timber, tobacco, textiles and electric power. Laos is divided into 16 provinces, one prefecture and one special region which are further divided into districts. There are totally 112 districts and 11,424 villages (1988). -

Thematic Interpretation Plan Savannakhet Province Lao People's Democratic Republic

Thematic Interpretation Plan Savannakhet Province Lao People’s Democratic Republic GMS-Sustainable Tourism Development Project in Lao PDR Lao National Tourism Administration Prepared by: Linda Susan McIntosh, PhD Candidate Thematic Interpretation and Textile Specialist 33 Soi 1 Sukhumvit Road Klongtoey-nua, Wattana What is Thematic Interpretation? Thematic Interpretation is the practice of verbal and non-verbal communication, using illustrated and non-illustrated techniques to present complex subject matter in an interesting and engaging way. One model of Thematic Interpretation is TORE™ = Thematic, Organized, Relevant, and Enjoyable “Successful interpretation provokes people to think. Their thinking creates meanings in their own minds. Themes can stay with us, even when we forget the smaller facts that support them. Strong themes stick in our minds, some of them forever”. Themes, because they are whole ideas, are expressed in the same form as information already stored in our minds. So when we communicate a theme effectively we give visitors something they can readily relate, self-appropriate, and incorporate into their thinking. Themes are ideas not topics: Examples of Themes: An Example of a Topic: • Birds are a fascinating group of animals • Birds because of their special adaptations for flight. • Native birds everywhere are in a fight for their lives because of overdevelopment and Having a theme helps us prepare educational and promotional materials. It makes our job a lot easier because with a theme we able to understand what to include and not include in a presentation to visitors. 2 SAVANNAKHET HISTORIC TRAIL - Background The SAVANNAKHET HISTORIC TRAIL is a new tour circuit consisting of historic, cultural and natural attractions, situated along the East-West Corridor in Savannakhet Province, Lao PDR. -

Download 6.62 MB

Social Safeguards Monitoring Report Semi-Annual Report Reporting Period: July – December 2020 June 2021 Lao PDR: Climate-Friendly Agribusiness Value Chains Sector Project Prepared by the Ministry of Agriculture and Forestry assisted by the Project Management Consultants for the Lao People’s Democratic Republic and the Asian Development Bank. This social safeguards monitoring report is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. G0585-Lao: Climate-Friendly Agribusiness Value Chains Sector Project Semi-Annual Safeguards Monitoring Report July - December 2020 Semi-Annual Social Safeguards Monitoring Report G0585-Lao: Climate-Friendly Agribusiness Value Chains Sector Project ADB 48409-004 / Grant 0585-LAO Report for period of July - December 2020 Prepared by the Ministry of Agriculture and Forestry (MAF) assisted by Project Management Consultants (PMC) for the Asian Development Bank. ADB Grant 0585-LAO i G0585-Lao: Climate-Friendly Agribusiness Value Chains Sector Project Semi-Annual Safeguards Monitoring Report July - December 2020 Contents 1 Executive Summary 4 2 Introduction 6 2.1 Background of the Report 6 2.2 Basic -

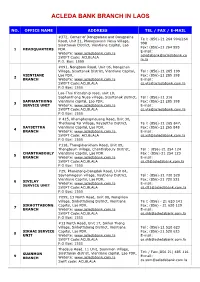

Acleda Bank Branch in Laos

ACLEDA BANK BRANCH IN LAOS NO. OFFICE NAME ADDRESS TEL / FAX / E-MAIL #372, Corner of Dongpalane and Dongpaina Te l: (856)-21 264 994/264 Road, Unit 21, Phonesavanh Neua Village, 998 Sisattanak District, Vientiane Capital, Lao Fax: (856)-21 264 995 1 HEADQUARTERS PDR. E-mail: Website: www.acledabank.com.la [email protected] SWIFT Code: ACLBLALA m.la P.O. Box: 1555 #091, Nongborn Road, Unit 06, Nongchan Village, Sisattanak District, Vientiane Capital, Tel : (856)-21 285 199 VIENTIANE Lao PDR. Fax: (856)-21 285 198 2 BRANCH Website: www.acledabank.com.la E-mail: SWIFT Code:ACLBLALA [email protected] P.O Box: 1555 Lao-Thai friendship road, unit 10, Saphanthong Nuea village, Sisattanak district, Tel : (856)-21 316 SAPHANTHONG Vientiane capital, Lao PDR. Fax: (856)-21 285 198 3 SERVICE UNIT Website: www.acledabank.com.la E-mail: SWIFT Code:ACLBLALA [email protected] P.O Box: 1555 # 415, Khamphengmeuang Road, Unit 30, Thatluang Tai Village, Xaysettha District, Te l: (856)-21 265 847, XAYSETTHA Vientiane Capital, Lao PDR. Fax: (856)-21 265 848 4 BRANCH Website: www.acledabank.com.la, E-mail: SWIFT Code: ACLBLALA [email protected] P.O Box: 1555 #118, Thongkhankham Road, Unit 09, Thongtoum Village, Chanthabouly District, Tel : (856)-21 254 124 CHANTHABOULY Vientiane Capital, Lao PDR Fax : (856)-21 254 123 5 BRANCH Website: www.acledabank.com.la E-mail: SWIFT Code:ACLBLALA [email protected] P.O Box: 1555 #29, Phonetong-Dongdok Road, Unit 04, Saynamngeun village, Xaythany District, Tel : (856)-21 720 520 Vientiane Capital, Lao PDR. -

World Bank Document

FOR OFFICIAL USE ONLY Report No: PAD3071 Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION PROJECT APPRAISAL DOCUMENT ON A PROPOSED CREDIT IN THE AMOUNT OF SDR 18.2 MILLION (US$25 MILLION EQUIVALENT) Public Disclosure Authorized TO THE LAO PEOPLE’S DEMOCRATIC REPUBLIC FOR A LAO PDR CIVIL REGISTRATION AND VITAL STATISTICS PROJECT March 9, 2020 Public Disclosure Authorized Health, Nutrition, and Population Global Practice East Asia and Pacific Region Public Disclosure Authorized This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. The World Bank Lao PDR Civil Registration and Vital Statistics Project (P167601) CURRENCY EQUIVALENTS (Exchange Rate Effective January 31, 2020) Currency Unit = Lao Kip (LAK) LAK 8,884.94 = US$1 US$1.3770 = SDR 1 FISCAL YEAR January 1–December 31 Regional Vice President: Victoria Kwakwa Acting Country Director: Gevorg Sargsyan Regional Director: Daniel Dulitzky Practice Manager: Daniel Dulitzky Task Team Leader(s): Samuel Lantei Mills The World Bank Lao PDR Civil Registration and Vital Statistics Project (P167601) ABBREVIATIONS AND ACRONYMS APIS Advanced Programming and Information Systems CMIS Civil Management Information System CPF Country Partnership Framework CRVS Civil Registration and Vital Statistics DA Designated Account DCM Department of Citizen Management DHIS2 District Health Information Software DOHA District Office of Home Affairs ECOP -

25-6 Drainage System

Final Report The Study on Vientiane Water Supply Development Project Figure 25-6 Drainage System Legend River, Canal, Trench, Natural Swamp Planned Drain Cannal Reservoir Irrigation Canal Thatluang Irrigation Pumping Station Swamp Boundary of Master Plan Source: Vientiane Urban Development Master Plan, Urban Research Institute, MCTPC 2 - 43 Final Report The Study on Vientiane Water Supply Development Project 2.5.3 GDP Projection An accurate long-term projection of the GDP is necessary for formulating the future framework of the socio-economic structure in the project sites. Official economic projections in “Five-year National Development Plan 2001-2005” and “Long-term Development Plan 2001-2020” were described in Section 5.1. The Five-year Plan has a more specific projection that includes sectoral scenarios, but the “Long-term Plan” shows overall targets for the year 2020. In this study, then, the future projections are based on the “Five-year Plan” projection scenario. The criteria for the projection are assumed as follows. (1) That major sectors grow at the following annual rates until 2005 as proposed in the “Five-year Plan”: 4.5% in the agricultural sector, 10.5% in the industrial sector, 8.5% in the services sector and a 7.0% rise from import duties. As a result, the GDP is expected to grow at 7.0% per annum on average during the planned period. (2) That after 2005, the respective sectors grow at the same rates as set in the “Five-year Plan” until the target year 2020. The GDP projected with the above assumptions are shown in Table 25-1. -

Vientiane Times Ministry Lends Muscle to National Circus

VientianeThe First Times National English Language Newspaper TUESDAY MARCH 15, 2016 ISSUE 63 4500 kip Singapore company builds network in Lao service sector Times Reporters conference equipment makers have taken advantage of this The Mekong Group is a and set up their factories here.” Singapore-based company “Today, we ventured which has a particular focus on into another opportunity, the Laos due to the stable political insurance sector.” conditions, low crime rate, pro- The company has been business government policy doing business in the Mekong and low cost of living. region for the past 20 years. Mr Michael Aw, CEO “Eventually we will expand of the Mekong Group Pte to serve the neighbouring countries along the Mekong River,” Mr Aw said. The Mekong Group specialises in Asean chiefs of defence forces link hands during their 13th informal meeting in Vientiane yesterday. providing various business services to Lao companies and state owned enterprises. “We will connect Asean defence chiefs vow to consultants, investors, and joint venture partners to Laos and bring opportunities from Laos to Singapore,” he said. deepen ties for regional security A 2014 report from the Ministry of Planning Times Reporters trust, confidence and capacities to all through dialogues, and Declaration of the Conduct of and Investment noted that in addressing regional non- military-to-military interaction Parties in the South China Sea Singapore is a major investor Asean chiefs of defence forces, traditional security challenges in activities to deepen defence and work towards the early Mr Michael Aw. in Laos with total Singaporean who convened in Vientiane an effective and timely manner.