2018 City-Wide Executive Challenge

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2019-2020 Membership

HARRY PHILLIPS AMERICAN INN OF COURT 2019-2020 MEMBERSHIP A Olatayo Atanda, Esq. Waller Lansden Dortch & Davis 511 Union Street, Suite 2700 Nashville, TN 37219 615-850-8861 [email protected] Barrister (2022) BPR No. 031007 B Kathryn Barnett, Esq. Morgan & Morgan 810 Broadway, Suite 500 Nashville, TN 37203 615-490-0944 [email protected] Master (2020) BPR No. 015361 Membership Chair Alan Stuart Bean, Esq. Starnes Davis Florie LLP 3000 Meridian Blvd., Suite 170 Franklin, TN 37067 615-905-7200 [email protected] Barrister (2022) BPR No. 026194 Raquel L. Bellamy, Esq. Bone McAllester Norton PLLC 511 Union Street, Suite 1600 Nashville, TN 37219 615-636-5781 [email protected] Barrister (2020) BPR No. 030636 Christen Blackburn, Esq. Lewis Thomason King Krieg & Waldrop 424 Church Street, Suite 2500 Nashville, TN 37219 615-574-6732 [email protected] Barrister (2021) BPR No. 027104 19 Gen. Andrée S. Blumstein Solicitor General Office of the Attorney General & Reporter P.O. Box 20207 Nashville, TN 37202-0207 615-741-3492 [email protected] Master (2023) BPR No. 009357 Counselor Seannalyn Brandmeir, Esq. State of Tennessee, Benefits Administration 1320 West Running Brook Road Nashville, TN 37209 615-532-4598 [email protected] Associate (2021) BPR No. 034158 Mr. Cole W. Browndorf [email protected] Student (2020) VU C Gen. Sarah K. Campbell Office of the Attorney General & Reporter P.O. Box 20207 Nashville, TN 37202-0207 615-532-6026 [email protected] Barrister (2021) BPR No. 034054 Rebecca McKelvey Castañeda, Esq. Stites & Harbison 401 Commerce Street, Suite 800 Nashville, TN 37219 615-782-2204 [email protected] Barrister (2022) BPR No. -

Healthcare Report 1H 2021

Investment Banking & Securities Offered Through SDR Capital Markets, Inc., Member FINRA & SIPC. ❑ ❑ ❑ ❑ ❑ ❑ 200 174 150 100 78 41 46 50 21 Financial Strategic - 52% 48% Amount TEV/ TEV/ Date Target B uyer(s) Segment ($ in Mil) Rev EB ITDA 6/25/2021 Alliance HealthCare Services Akumin Inpatient/Hospitals 820.00 - - 6/16/2021 23andM e VG Acquisition Pharma and Lab Services 3,500.00 14.2x - 6/15/2021 Springstone M edical Properties Trust Inpatient/Hospitals 950.00 - 14.1x 6/14/2021 University Health Care Cano Health Inpatient/Hospitals 600.00 - - 6/14/2021 One Homecare Solutions Humana Long Term & Behavioral Care - - - 6/7/2021 Iora Health One M edical Inpatient/Hospitals 2,100.00 - - 6/7/2021 Newport Academy Onex Inpatient/Hospitals 1,300.00 - - 6/1/2021 Veterans Evaluation Services M aximus Outpatient/Clinics 1,400.00 - - 6/1/2021 M ercy Quest Diagnostics Pharma and Lab Services - - - 5/13/2021 Redmond Regional M edical Center AdventHealth Inpatient/Hospitals 635.00 - - 5/6/2021 M eM D Walmart Outpatient/Clinics - - - 5/5/2021 Axia Women's Health Partners Group Outpatient/Clinics 800.00 - 20.0x Strategic Buyer Inv. Date Select Corporate Acquisitions IMAC Regeneration Center 6/25/2021 ▪ Active M edical Center (M edical Center) 6/14/2021 ▪ Fort Pierce Chiropractic 3/1/2021 ▪ NCH Chiropractic 2/4/2021 ▪ Willmitch Chiropractic Skylight Health Group 6/24/2021 ▪ The Doctors Center (US) 2/4/2021 ▪ River City M edical Associates 1/7/2021 ▪ Rocky M ountain Urgent Care Pennant Group 6/16/2021 ▪ First Call Hospice 5/1/2021 ▪ CardioVascular Home Care 4/1/2021 ▪ Pasco SW 1/16/2021 ▪ Sacred Heart Health LHC Group 6/2/2021 ▪ Heart of Hospice 1/5/2021 ▪ Grace Hospice of Oklahoma 1/5/2021 ▪ East Valley Hospice CRH Medical 5/27/2021 ▪ Northern Indiana Anesthesia Associates 4/1/2021 ▪ M iddle Arkansas Sedation Associates 3/14/20172/9/2021 ▪ Oak Tree Anesthesia Associates The Ensign Group 5/1/2021 ▪ WindsorDermatology Rehabilitation Center PC and Health Care Center 4/1/2021 ▪ The Ensign Group (3 Skilled Nursing Facilities in Colorado) 2/1/2021 ▪ San Pedro M anor 1/1/2021 ▪ St. -

Healthcare Transactions: Year in Review

HEALTHCARE TRANSACTIONS: YEAR IN REVIEW JANUARY 2019 bassberry.com OVERVIEW 2018 marked a year of continued robust healthcare merger and acquisition activity, with deal volume surpassing that of 2017. The dollar volume of healthcare deals also exceeded 2017, highlighted by CVS Health Corp. (NYSE: CVS) surviving regulatory scrutiny and finalizing its purchase of Aetna for $69 billion, and Cigna (NYSE: CI) closing its $67 billion merger with pharmacy benefit manager Express Scripts (Nasdaq: ESRX). Private equity firm KKR & Co. Inc. (NYSE: KKR) acquired Envision Healthcare Corporation (NYSE: EVHC) in a going private transaction for $9.9 billion; and in November, LifePoint Health, Inc. (Nasdaq: LPNT) merged with Apollo Global Management-owned RCCH HealthCare Partners for an estimated $5.6 billion. Not only do these deals show the energy of the industry, but they also represent a seismic shift in healthcare. Cross-sector transactions, such as the CVS-Aetna and Cigna-Express Scripts transactions, are becoming more frequent and disrupt traditional industry models. By seeking alliances across industry lines, healthcare companies aim both to reduce costs and improve care coordination as well as realign incentives to better meet consumer demands. As providers fight to stay profitable in the wake of value-based reimbursement, these cross-sector combinations may foreshadow the future of the healthcare industry. Many of these same drivers also have led to increasing private equity investment in the industry. The need for innovation and disruption via consolidation adds further appeal to investors. The injection of capital by private equity firms allows healthcare providers to cut costs and increase efficiencies, and the shift in reimbursement presents a unique opportunity for firms to help providers and systems reposition. -

Regional Economic Development Guide Tabletable of Contents

NASHVILLEREGIONAL ECONOMIC DEVELOPMENT GUIDE TABLETABLE OF CONTENTS Location 4 - 6 Economy 7 - 9 Accessibility & Transportation 10 - 11 International Business 12 - 15 Demographics 16 - 17 Talent & Workforce 18 - 25 Target Industries 26 - 27 Corporate Services 28 - 29 Health Care Management 30 - 32 Information Technology 33 - 35 Music & Entertainment 36 - 37 Advanced Manufacturing 38 - 39 Distribution & Trade 40 - 41 Livability 42 - 46 Contact Us 47 2 - TABLE OF CONTENTS TABLE OF CONTENTS - 3 LOCATIONLOCATION NASHVILLE Strategically located in the heart of the Tennessee Valley, the Nashville region is where businesses thrive and the creative spirit resonates across industries and communities. The Nashville economic market has 10 counties and a population of more than 1.9 million, making it the largest metro area in a five-state region. Many corporate headquarter giants call Nashville home, including Nissan North America, Bridgestone Americas, Dollar General, HCA Healthcare, AllianceBernstein, and Amazon. A national hub for the creative class, Nashville has the largest concentration of the music industry per capita in America. The Nashville region’s educated workforce not only provides an abundant talent pool for companies, but also bolsters the region’s vibrancy, artistic and musical essence, and Portland Springfield competitive edge in technology and Clarksville White Robertson House innovation. The Nashville region is Montgomery Sumner defined by a diverse economy, low Gallatin cost of living and doing business, a Goodlettsville Cheatham Hendersonville creative culture and a well-educated Ashland City population. Cultural diversity, unique neighborhoods, a variety of industries Charlotte Mt. Juliet Lebanon Davidson Wilson and a thriving creative community make Dickson Nashville Nashville’s economic market among the Dickson nation’s best locations for relocating, Brentwood La Vergne expanding and startup companies. -

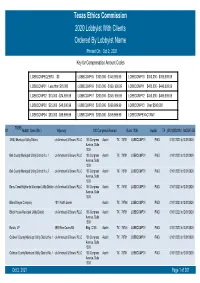

Texas Ethics Commission 2020 Lobbyist with Clients Ordered by Lobbyist Name Printed on Oct 2, 2021 Key for Compensation Amount Codes

Texas Ethics Commission 2020 Lobbyist With Clients Ordered By Lobbyist Name Printed On Oct 2, 2021 Key for Compensation Amount Codes LOBBCOMPEQZERO $0 LOBBCOMP05 $100,000 - $149,999.99 LOBBCOMP10 $350,000 - $399,999.99 LOBBCOMP01 Less than $10,000 LOBBCOMP06 $150,000 - $199, 999.99 LOBBCOMP11 $400,000 - $449,999.99 LOBBCOMP02 $10,000 - $24,999.99 LOBBCOMP07 $200,000 - $249, 999.99 LOBBCOMP12 $450,000 - $499,999.99 LOBBCOMP03 $25,000 - $49,000.99 LOBBCOMP08 $250,000 - $299,999.99 LOBBCOMP13 Over $500,000 LOBBCOMP04 $50,000 - $99,999.99 LOBBCOMP09 $300,000 - $349,999.99 LOBBCOMPEXACTAMT 70358 #1 Abbott, Sean (Mr.) Attorney 100 Congress Avenue Suite 1300 Austin TX (512)4352334 MODIFIED 3 B&J Municipal Utility District c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Bell County Municipal Utility District No. 1 c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Bell County Municipal Utility District No. 2 c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Berry Creek Highlands Municipal Utility District c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Blake Magee Company 1011 North Lamar Austin TX 78704 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Block House Municipal Utility District c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Bonzo, LP 3939 Bee Caves Rd. -

Private Equity Buyouts in Healthcare: Who Wins, Who Loses? Eileen Appelbaum and Rosemary Batt Working Paper No

Private Equity Buyouts in Healthcare: Who Wins, Who Loses? Eileen Appelbaum* and Rosemary Batt† Working Paper No. 118 March 15, 2020 ABSTRACT Private equity firms have become major players in the healthcare industry. How has this happened and what are the results? What is private equity’s ‘value proposition’ to the industry and to the American people -- at a time when healthcare is under constant pressure to cut costs and prices? How can PE firms use their classic leveraged buyout model to ‘save healthcare’ while delivering ‘outsized returns’ to investors? In this paper, we bring together a wide range of sources and empirical evidence to answer these questions. Given the complexity of the sector, we focus on four segments where private equity firms have been particularly active: hospitals, outpatient care (urgent care and ambulatory surgery centers), physician staffing and emergency * Co-Director and Senior Economist, Center for Economic and Policy Research. [email protected] † Alice H. Cook Professor of Women and Work, HR Studies and Intl. & Comparative Labor ILR School, Cornell University. [email protected]. We thank Andrea Beaty, Aimee La France, and Kellie Franzblau for able research assistance. room services (surprise medical billing), and revenue cycle management (medical debt collecting). In each of these segments, private equity has taken the lead in consolidating small providers, loading them with debt, and rolling them up into large powerhouses with substantial market power before exiting with handsome returns. https://doi.org/10.36687/inetwp118 JEL Codes: I11 G23 G34 Keywords: Private Equity, Leveraged Buyouts, health care industry, financial engineering, surprise medical billing revenue cycle management, urgent care, ambulatory care. -

THOMAS F. FRIST, JR., MD in First Person

THOMAS F. FRIST, JR., M.D. In First Person: An Oral History American Hospital Association Center for Hospital and Healthcare Administration History and Health Research & Educational Trust 2013 HOSPITAL ADMINISTRATION ORAL HISTORY COLLECTION THOMAS F. FRIST, JR., M.D. In First Person: An Oral History Interviewed by Kim M. Garber On January 17, 2013 Edited by Kim M. Garber Sponsored by American Hospital Association Center for Hospital and Healthcare Administration History and Health Research & Educational Trust Chicago, Illinois 2013 ©2013 by the American Hospital Association All rights reserved. Manufactured in the United States of America Coordinated by Center for Hospital and Healthcare Administration History AHA Resource Center American Hospital Association 155 North Wacker Drive Chicago, Illinois 60606 Transcription by Chris D‘Amico Photos courtesy of the Frist family, HCA, the American Hospital Association, Louis Fabian Bachrach, Micael-Renee Lifestyle Portraiture, Simon James Photography, and the United Way of Metropolitan Nashville EDITED TRANSCRIPT Interviewed in Nashville, Tennessee KIM GARBER: Today is Thursday, January 17, 2013. My name is Kim Garber, and I will be interviewing Dr. Thomas Frist, Jr., chairman emeritus of HCA Holdings, Inc. In the 1960s, together with his father, Dr. Thomas Frist, Sr., Dr. Frist conceived of a company that would own or manage multiple hospitals, providing high quality care and leveraging economies of scale. Founded in 1968, the Hospital Corporation of America, now known as HCA, has owned or managed hundreds of hospitals. Known as the First Family of Nashville, the Frists have made substantial contributions to Music City through their work with the Frist Foundations and other initiatives. -

Healthcare Real Estate

VALUE FOCUS REAL ESTATE Sector Focus: Healthcare Real Estate Second Quarter 2017 Healthcare Facilities 1 Macro Indicators 3 Industry Performance and M&A Activity 6 Publicly Traded Companies Hospitality 9 Residential 11 Healthcare 12 Commercial Real Estate 16 About Mercer Capital 22 www.mercercapital.com Mercer Capital’s Value Focus: Real Estate Industry Second Quarter 2017 Healthcare Facilities As of the most recent data in 2015, healthcare spending in the United States was $3.2 trillion. Average annual growth in national healthcare expenditures from 2015 to 2025 is expected to be approximately 5.6%. As a share of gross domestic product, national healthcare expenditure is expected to increase from 17.8% in 2015 to 19.9% by 2025. Demand for medical office buildings (MOBs) is driven primarily by demographic characteristics, rather than economic trends. This has contributed to more stable performance for the medical office building segment during a period when office space in general has underperformed. Consolidation continued in the industry during 2016, spurred by efforts to cut costs and offset lower insurance reimbursement rates. This trend has encouraged demand for larger office space and weakened the market for smaller, individual healthcare facilities, although ambulatory centers associated with larger hospitals are an exception. Merger and acquisition activity is expected to pick up in 2017, following an 8.0% increase in transactions in the first quarter. Of 27 transactions during the first quarter, three included organizations with revenues of $1 billion or greater. Average rents in the medical office space were $24.00 per square foot in 2016, which represents an 8.0% increase over the prior year and 8.3% above the $22.16 low observed in early 2013. -

2020 Annual Report

JULY 31, 2021 2021 Annual Report iShares U.S. ETF Trust • iShares Evolved U.S. Consumer Staples ETF | IECS | Cboe BZX • iShares Evolved U.S. Discretionary Spending ETF | IEDI | Cboe BZX • iShares Evolved U.S. Financials ETF | IEFN | Cboe BZX • iShares Evolved U.S. Healthcare Staples ETF | IEHS | Cboe BZX • iShares Evolved U.S. Innovative Healthcare ETF | IEIH | Cboe BZX • iShares Evolved U.S. Media and Entertainment ETF | IEME | Cboe BZX • iShares Evolved U.S. Technology ETF | IETC | Cboe BZX The Markets in Review Dear Shareholder, The 12-month reporting period as of July 31, 2021 was a remarkable period of adaptation and recovery, as the global economy dealt with the implications of the coronavirus (or “COVID-19”) pandemic. The United States, along with most of the world, began the reporting period emerging from a severe recession, prompted by pandemic-related restrictions that disrupted many aspects of daily life. However, easing restrictions and robust government intervention led to a strong rebound, and the economy grew at a significant pace for the reporting period, eventually regaining the output lost from the pandemic. Equity prices rose with the broader economy, as strong fiscal and monetary support, as well as the development of vaccines, made investors increasingly optimistic about the economic outlook. The implementation of mass vaccination campaigns and passage of two additional fiscal stimulus packages Rob Kapito further boosted stocks, and many equity indices neared or surpassed all-time highs late in the reporting President, BlackRock, Inc. period. In the United States, returns of small-capitalization stocks, which benefited the most from the resumption of in-person activities, outpaced large-capitalization stocks. -

Usef-I Q2 2021

Units Cost Market Value U.S. EQUITY FUND-I U.S. Equities 88.35% Domestic Common Stocks 10X GENOMICS INC 5,585 868,056 1,093,655 1ST SOURCE CORP 249 9,322 11,569 2U INC 301 10,632 12,543 3D SYSTEMS CORP 128 1,079 5,116 3M CO 11,516 2,040,779 2,287,423 A O SMITH CORP 6,897 407,294 496,998 AARON'S CO INC/THE 472 8,022 15,099 ABBOTT LABORATORIES 24,799 2,007,619 2,874,948 ABBVIE INC 17,604 1,588,697 1,982,915 ABERCROMBIE & FITCH CO 1,021 19,690 47,405 ABIOMED INC 9,158 2,800,138 2,858,303 ABM INDUSTRIES INC 1,126 40,076 49,938 ACACIA RESEARCH CORP 1,223 7,498 8,267 ACADEMY SPORTS & OUTDOORS INC 1,036 35,982 42,725 ACADIA HEALTHCARE CO INC 2,181 67,154 136,858 ACADIA REALTY TRUST 1,390 24,572 30,524 ACCO BRANDS CORP 1,709 11,329 14,749 ACI WORLDWIDE INC 6,138 169,838 227,965 ACTIVISION BLIZZARD INC 13,175 839,968 1,257,422 ACUITY BRANDS INC 1,404 132,535 262,590 ACUSHNET HOLDINGS CORP 466 15,677 23,020 ADAPTHEALTH CORP 1,320 39,475 36,181 ADAPTIVE BIOTECHNOLOGIES CORP 18,687 644,897 763,551 ADDUS HOMECARE CORP 148 13,034 12,912 ADOBE INC 5,047 1,447,216 2,955,725 ADT INC 3,049 22,268 32,899 ADTALEM GLOBAL EDUCATION INC 846 31,161 30,151 ADTRAN INC 892 10,257 18,420 ADVANCE AUTO PARTS INC 216 34,544 44,310 ADVANCED DRAINAGE SYSTEMS INC 12,295 298,154 1,433,228 ADVANCED MICRO DEVICES INC 14,280 895,664 1,341,320 ADVANSIX INC 674 15,459 20,126 ADVANTAGE SOLUTIONS INC 1,279 14,497 13,800 ADVERUM BIOTECHNOLOGIES INC 1,840 7,030 6,440 AECOM 5,145 227,453 325,781 AEGLEA BIOTHERAPEUTICS INC 287 1,770 1,998 AEMETIS INC 498 6,023 5,563 AERSALE CORP -

051820 Tractor Supply

OFFERING MEMORANDUM TRACTOR SUPPLY – HOHENWALD, TN 608 E Main Street • Hohenwald, TN 38462 Representative Photo NON- ENDORSEMENT AND DISCLAIMER NOTICE Confidentiality and Disclaimer The information contained in the following Marketing Brochure is proprietary and strictly confidential. It is intended to be reviewed only by the party receiving it from Marcus & Millichap and should not be made available to any other person or entity without the written consent of Marcus & Millichap. This Marketing Brochure has been prepared to provide summary, unverified information to prospective purchasers, and to establish only a preliminary level of interest in the subject property. The information contained herein is not a substitute for a thorough due diligence investigation. Marcus & Millichap has not made any investigation, and makes no warranty or representation, with respect to the income or expenses for the subject property, the future projected financial performance of the property, the size and square footage of the property and improvements, the presence or absence of contaminating substances, PCB's or asbestos, the compliance with State and Federal regulations, the physical condition of the improvements thereon, or the financial condition or business prospects of any tenant, or any tenant's plans or intentions to continue its occupancy of the subject property. The information contained in this Marketing Brochure has been obtained from sources we believe to be reliable; however, Marcus & Millichap has not verified, and will not verify, any of the information contained herein, nor has Marcus & Millichap conducted any investigation regarding these matters and makes no warranty or representation whatsoever regarding the accuracy or completeness of the information provided. -

2017 REGIONAL ECONOMIC DEVELOPMENT GUIDE 2 NASHVILLE ECONOMIC DEVELOPMENT GUIDE Table of Contents

NASHVILLE 2017 REGIONAL ECONOMIC DEVELOPMENT GUIDE 2 NASHVILLE ECONOMIC DEVELOPMENT GUIDE Table of contents 4 Location 28 Health Care Management 7 Economy 31 Information Technology 10 Accessibility & Transportation 34 Music & Entertainment 12 International Business 36 Advanced Manufacturing 16 Demographics 38 Distribution & Trade 18 Talent & Workforce 40 Arts, Culture & Entertainment 24 Target Sectors 43 Contact Us 26 Corporate Services Photo credit: Warne Riker NASHVILLEREGIONAL ECONOMIC PROFILE DEVELOPMENT - SECTION NAME GUIDE XX 3 Population growth +10.2% 2010: 1,755,446 2015: 1,935,107 NASHVILLE ECONOMIC MARKET Montgomery Robertson Sumner Cheatham +4.0% Davidson Dickson Wilson 2010: 6,346,105 Williamson 2015: 6,600,299 Rutherford TENNESSEE Maury LOCATION Nashville Strategically located in the heart of the Tennessee Valley, the Nashville region is where businesses 50% of the U.S. thrive and the creative spirit resonates across industries and communities. The Nashville population (150 million people) lives within 650 Economic Market has 10 counties and a population of more than 1.9 million, making it the miles of Nashville. largest metro area in a five-state region. Many corporate headquarter giants call Nashville home, including Nissan North America, Bridgestone Americas, Dollar General, Hospital Corporation of America and Gibson Guitar. A national hub for the creative class, Nashville has the strongest concentration of the music industry in America. The Nashville region’s educated workforce not only provides an abundant talent pool for companies, but also bolsters the region’s vibrancy, artistic and musical essence, and competitive edge in technology and innovation. The Nashville region is defined by a diverse economy, low costs of living and doing business, a creative culture and a well-educated population.